Deciding how to allocate your income toward retirement accounts is a critical component of wealth building in the 2026 fiscal year. With the IRS recently adjusting contribution limits and introducing new regulations for high earners, having a standardised approach to your 401(k) and IRA is more important than ever.

How We Selected Our 9 Actionable Steps to Maximize Your 401(k)

To develop this list, we analysed the 2026 IRS cost-of-living adjustments, the latest SECURE 2.0 Act implementation phases, and current market trends regarding expense ratios and employer matching benchmarks. Our selection prioritises immediate tax efficiency, the power of compounding through automation, and the strategic use of catch-up provisions for older investors.

The 9 Most Effective Ways to Maximize Your 401(k) and IRA in 2026

These steps are designed to help you navigate the complexities of modern retirement planning while ensuring you don’t leave any “free money” on the table.

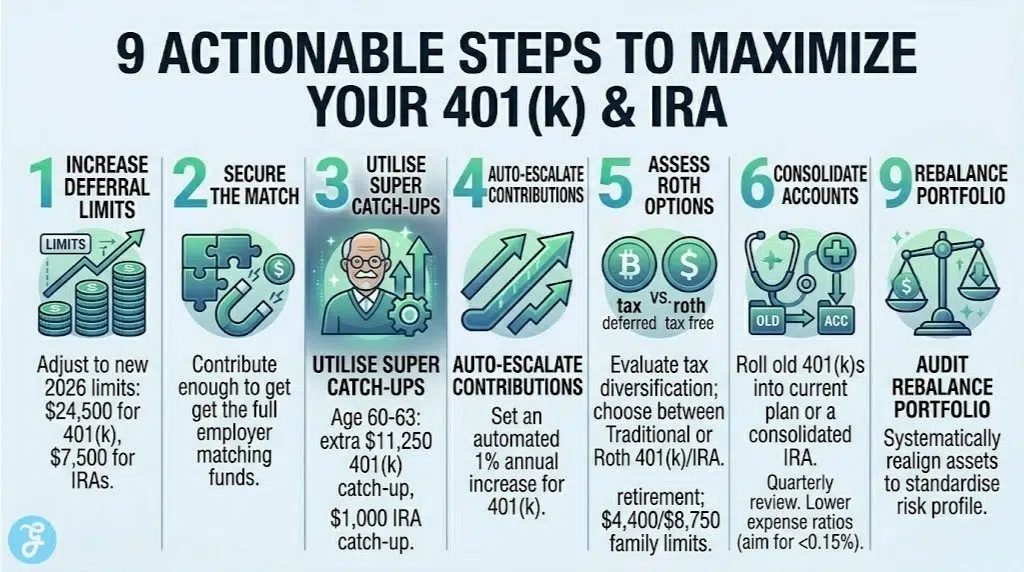

1. Increase Your Deferral to the 2026 Maximum

The IRS has increased the elective deferral limit for 2026 to $24,500 (up from $23,500 in 2025). Adjusting your payroll contributions early in the year ensures you stay on track to hit this new ceiling without a major “catch-up” crunch in December.

Best for: Investors with high disposable income looking to significantly reduce their current taxable salary.

Why We Chose It:

-

It allows you to shield more of your income from immediate taxation.

-

It maximises the amount of capital working for you in a tax-deferred environment.

-

It aligns your strategy with the latest federal inflation adjustments.

Things to consider: Ensure your monthly budget can handle the increased deduction before committing to the full amount.

2. Secure the Full Employer Match First

The employer match is essentially a 100% immediate return on your investment. If your company matches 50% of your contributions up to 6% of your salary, you should never contribute less than that 6% threshold.

Best for: Every employee regardless of income level or investment goals.

Why We Chose It:

-

It is the only guaranteed “risk-free” return available in the financial markets.

-

It significantly accelerates the growth of your nest egg through non-elective contributions.

-

It helps you reach the combined total contribution limit of $72,000 for 2026.

Things to consider: Check your plan’s “vesting schedule” to understand how long you must stay with the company to keep the matched funds.

3. Utilise the New “Super” Catch-Up Contributions

For those aged 50 and older, the 2026 catch-up limit has risen to $8,000. Furthermore, the SECURE 2.0 “super catch-up” for individuals aged 60 to 63 remains at $11,250, allowing these workers to contribute a total of $35,750 in elective deferrals.

Best for: Workers in the final decade of their career who need to bolster their savings rapidly.

Why We Chose It:

-

It provides a powerful late-stage boost to retirement savings.

-

It allows for significant tax deductions during peak earning years.

-

It accounts for the higher savings capacity often available to older professionals.

Things to consider: High earners (wages over $150,000 in 2025) must now make these catch-up contributions on a Roth basis.

4. Automate an Annual 1% Contribution Increase

Many plans now offer an “auto-escalation” feature. By setting your contribution to increase by just 1% on your work anniversary or after a performance review, you can scale your savings without feeling a major impact on your take-home pay.

Best for: Disciplined savers who want to remove emotion and manual effort from their retirement planning.

Why We Chose It:

-

It counters “lifestyle creep” by redirecting raises into long-term assets.

-

It standardises the growth of your portfolio over several decades.

-

It leverages the psychological benefit of “set and forget” finance.

Things to consider: Review your total percentage periodically to ensure you don’t accidentally exceed the annual IRS dollar limit.

5. Assess the Roth 401(k) Option for Tax Diversification

The 2026 rules have made Roth options more prominent. Unlike traditional 401(k)s, Roth contributions are made with after-tax dollars, meaning your withdrawals in retirement are completely tax-free.

Best for: Younger investors in lower tax brackets or high earners seeking “tax-free” buckets for retirement.

Why We Chose It:

-

It provides a hedge against future tax rate increases.

-

It offers greater flexibility when managing income levels in retirement to avoid Medicare surcharges.

-

It simplifies estate planning as heirs generally receive Roth assets tax-free.

Things to consider: Choosing Roth means you lose the immediate tax deduction on your current year’s return.

6. Consolidate and Standardise Old Retirement Accounts

Holding multiple 401(k)s from previous employers can lead to fragmented strategies and excessive fees. Rolling old accounts into your current 401(k) or a consolidated IRA makes it easier to manage your asset allocation.

Best for: Mid-career professionals who have changed jobs multiple times.

Why We Chose It:

-

It reduces administrative “clutter” and makes rebalancing significantly easier.

-

It often lowers total investment costs by moving funds into lower-fee institutional plans.

-

It prevents “lost” accounts that can occur over decades of employment.

Things to consider: Check if your current plan allows “roll-ins” and verify that the investment options are superior to your old plan.

7. Pair Your 401(k) with a Health Savings Account (HSA)

If you have a high-deductible health plan, the HSA is the “triple tax threat”: contributions are tax-deductible, growth is tax-free, and withdrawals for medical expenses are tax-free. In 2026, many savvy investors treat their HSA as a secondary retirement account.

Best for: Healthy investors who can afford to pay current medical bills out-of-pocket while letting the HSA grow.

Why We Chose It:

-

It offers tax advantages that even a 401(k) cannot match.

-

It provides a dedicated fund for healthcare costs, which are a major retirement expense.

-

It allows penalty-free withdrawals for any reason after age 65 (though income tax applies if not for medical use).

Things to consider: For 2026, the HSA contribution limit is $4,400 for individuals and $8,750 for families.

8. Conduct a Quarterly Audit of Investment Fees

The “silent killer” of retirement accounts is the expense ratio. Even a 1% fee can strip tens of thousands of pounds from your final balance over 30 years. Standardising a review of your fund fees ensures you are in the most cost-effective share classes.

Best for: Long-term investors focused on maximising their “net” returns.

Why We Chose It:

-

It is one of the few variables in investing that you can directly control.

-

It ensures you are not paying for “active management” that fails to beat the market.

-

It keeps more of your capital compounding in your account rather than going to the fund manager.

Things to consider: Look for low-cost index funds or target-date funds with expense ratios below 0.15%.

9. Rebalance Your Portfolio to Standardise Risk

Market fluctuations can cause your stock-to-bond ratio to drift away from your target. If stocks perform well, your portfolio might become too risky; if they underperform, you might be missing out on growth.

Best for: Investors who want to maintain a consistent risk profile regardless of market noise.

Why We Chose It:

-

It forces you to “sell high and buy low” in a systematic way.

-

It prevents emotional decision-making during market volatility.

-

It ensures your asset allocation matches your actual timeline to retirement.

Things to consider: Many 401(k) plans offer “automatic rebalancing” once or twice a year, which simplifies this process.

Comparing Your 2026 Retirement Options

To effectively apply Ways to Maximize Your 401(k), you must understand how different accounts interact with your specific financial situation. The table below provides a quick reference for the 2026 limits and tax treatments.

2026 Retirement Account Comparison Table

| Account Type | 2026 Contribution Limit | Tax Treatment | Catch-Up (Age 50+) |

| Traditional 401(k) | $24,500 | Pre-tax / Tax-deferred | $8,000 |

| Roth 401(k) | $24,500 | After-tax / Tax-free | $8,000 (Roth only for high earners) |

| Traditional IRA | $7,500 | Pre-tax (If eligible) | $1,100 |

| Roth IRA | $7,500 | After-tax / Tax-free | $1,100 |

Our Top 3 Picks and Why?

Of the nine steps outlined, the Employer Match, the 2026 Max Deferral, and Automated Increases are the most impactful. These three form the foundation of wealth: securing immediate returns, maximising tax shelter room, and ensuring consistent growth through psychological automation.

Buyer’s Guide: Choosing the Right 401(k) Investment Path

Selecting your fund lineup is often more daunting than setting the contribution percentage. Use this framework to standardise your investment choices within your plan.

The Selection Framework:

-

Time Horizon: If you have 20+ years, prioritise equities (stock funds) for growth.

-

Risk Tolerance: Can you stomach a 20% drop without panic selling? If not, increase your bond or cash allocation.

-

Fee Awareness: Always check the “Expense Ratio” column. The lower, the better.

Decision Matrix (Table):

| Choose Target Date Funds if… | Choose Self-Directed Funds if… |

| You want a “hands-off” approach. | You want to customise your sector exposure. |

| You want automatic risk reduction over time. | You are comfortable rebalancing manually. |

| You prefer a single, diversified fund. | You want to target specific low-cost index trackers. |

The Final Checklist: 5-point Audit for Your 401(k)

-

Have you adjusted your payroll to hit the new $24,500 limit for 2026?

-

Are you receiving every penny of your company’s matching contribution?

-

If you are 50+, have you designated your catch-up contributions correctly?

-

Have you checked your fund expense ratios in the last 6 months?

-

Is your current asset allocation still appropriate for your retirement date?

The Path to Financial Longevity in 2026

Maximising your retirement accounts is a marathon, not a sprint. By implementing these standardised steps—from capturing the match to auditing fees—you ensure that your 401(k) is a robust engine for your future independence. As tax laws continue to evolve, staying active in your account management will always be the best strategy for long-term success.