Building a robust retirement fund in the UK requires more than just regular savings; it demands a deep understanding of the government’s incentivized tax structures. The Self-Invested Personal Pension (SIPP) stands out as one of the most flexible tools available, primarily due to the generous SIPP tax relief benefits 2026 provides to both basic and high-rate taxpayers. By taking a proactive approach to your contributions and investment choices, you can effectively turn your tax liabilities into a compounding engine for your future nest egg.

Our Selection Methodology

To identify these eight actionable steps, we cross-referenced the 2025/26 and 2026/27 HMRC tax thresholds with the latest pension annual allowance regulations. Our focus was on “high-impact” moves—strategies that provide immediate tax rebates while maximizing the long-term compounding effect within a tax-free wrapper. We prioritized methods that cater to a range of earners, from those looking to reclaim higher-rate tax to individuals wishing to provide for non-earning family members. Each step was vetted for its legality under current UK pension law and its practicality for the modern DIY investor.

Step-by-Step Guide to Maximizing SIPP Tax Relief Benefits 2026

Taking control of your retirement doesn’t have to be overwhelming. The following steps provide a clear roadmap for utilizing your SIPP to its full potential, ensuring you capture every pound of government support available this year.

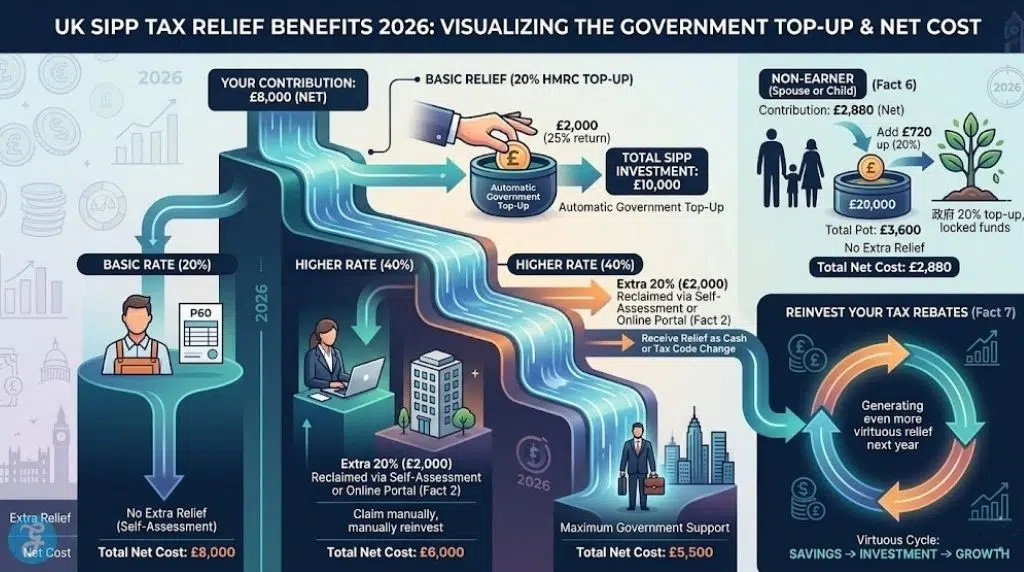

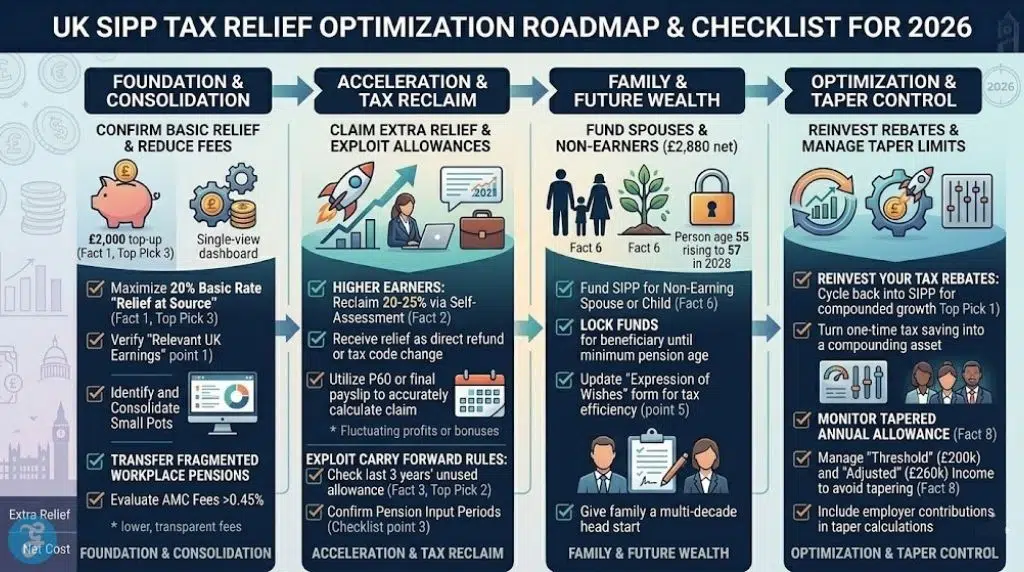

1. Maximize Your 20% Basic Rate “Relief at Source”

Every pound you contribute to a SIPP automatically triggers a 20% tax top-up from the government. For example, if you pay in £8,000, your provider will claim an additional £2,000 from HMRC, bringing your total investment to £10,000. This is an immediate 25% return on your net contribution before your money even hits the market.

Best for: Every UK taxpayer under age 75, regardless of their total annual income.

Things to consider: You can contribute up to 100% of your relevant UK earnings or £3,600 (whichever is higher) and still receive this automatic top-up.

While basic relief is automatic, higher earners must take an extra step to unlock the full value of their pension.

2. Reclaim Higher and Additional Rate Tax Relief

If you earn over £50,270, you are likely paying tax at 40% or 45%. While your SIPP provider handles the first 20%, you must manually claim the remaining 20% or 25% through your Self-Assessment tax return or HMRC’s new 2026 online portal. This is a critical component of maximizing SIPP tax relief benefits 2026.

Best for: Individuals in the higher or additional tax brackets who want to lower their overall tax bill.

Things to consider: The relief is often given as a tax code change or a direct refund, meaning it doesn’t automatically go into your pension pot unless you manually reinvest it.

If you have a high-income year, you may be able to exceed the standard yearly limits.

3. Exploit the “Carry Forward” Rules

The annual allowance for pension contributions in the 2025/26 and 2026/27 tax years is £60,000. However, if you haven’t used your full allowance from the previous three years (back to 2023/24), you can “carry forward” that unused space to make a much larger, tax-relievable contribution today.

Best for: Business owners with fluctuating profits or professionals who have received a significant bonus.

Things to consider: You must have been a member of a registered pension scheme during the years you are carrying forward from, even if you didn’t contribute anything at the time.

Consolidating your old accounts can also help you keep track of these allowances more effectively.

4. Consolidate Fragmented Workplace Pensions

Most workers accumulate multiple small pension pots throughout their careers. By transferring these into a single SIPP, you gain total control over your investment strategy and often benefit from lower, transparent fee structures.

Best for: Career-switchers who want a clear, “single-view” dashboard of their total retirement savings.

Things to consider: Before transferring, check for “Guaranteed Annuity Rates” or “Protected Tax-Free Cash” in your old policies, as these benefits may be lost upon transfer.

Once your funds are consolidated, your investment choices become the primary driver of growth.

5. Diversify Using Low-Cost Index Trackers

A SIPP gives you the freedom to invest in almost any asset class. In 2026, many savvy investors are shifting toward low-cost Global Index Trackers or ETFs to ensure broad market exposure while keeping management fees (which can eat into your tax relief gains) to a minimum.

Best for: Long-term investors who want to capture global growth without the risks of picking individual stocks.

Things to consider: While trackers are lower cost, they still carry market risk, so your asset allocation should shift toward bonds or cash as you approach retirement.

Don’t forget that you can also use your SIPP to build wealth for your loved ones.

6. Fund a SIPP for Non-Earning Spouses or Children

You can contribute up to £2,880 per year into a SIPP for someone who has no income (including children). The government will still add a 20% top-up, turning it into £3,600. This is a highly efficient way to move money out of your taxable estate while giving your family a head start.

Best for: Parents looking to build long-term wealth for their children or couples where one partner is not currently working.

Things to consider: The funds are locked away until the beneficiary reaches the minimum pension age (currently 55, rising to 57 in 2028).

To truly maximize the power of the system, you should look at how your tax refunds are used.

7. Reinvest Your Tax Rebates for Compounded Growth

When you receive a tax refund from your higher-rate relief claim, the most effective move is to pay that refund back into your SIPP. This creates a “virtuous cycle” where your tax relief generates even more tax relief in the following year.

Best for: Disciplined savers who want to accelerate their journey to financial independence.

Things to consider: Ensure that the reinvested refund doesn’t push you over your annual allowance for the new tax year.

Finally, keep a close eye on the income thresholds that can reduce your benefits.

8. Monitor the Tapered Annual Allowance

For very high earners (those with a “threshold income” over £200,000 and “adjusted income” over £260,000), the £60,000 allowance begins to taper down. In the most extreme cases, it can drop to just £10,000. Managing your income to stay below these levels is a vital part of SIPP tax relief benefits 2026.

Best for: Top-tier executives and successful business owners.

Things to consider: Employer contributions count toward your “adjusted income,” so these must be factored into your taper calculations.

Strategic Analysis

Deciding how much to contribute requires a balance between your current cash flow and your long-term goals. The table below illustrates how different tax brackets affect the “net cost” of a £10,000 SIPP investment.

| Tax Bracket | Initial Contribution | Automatic 20% Relief | Extra Relief (Self-Assessment) | Total Net Cost |

| Basic Rate (20%) | £8,000 | £2,000 | £0 | £8,000 |

| Higher Rate (40%) | £8,000 | £2,000 | £2,000 | £6,000 |

| Additional Rate (45%) | £8,000 | £2,000 | £2,500 | £5,500 |

| Non-Earner | £2,880 | £720 | £0 | £2,880 |

Our Top 3 Picks And Why?

-

Reinvesting Tax Rebates: This is our top pick because it utilizes the “math of the system” to turn a one-time tax saving into a multi-decade compounding asset.

-

The “Carry Forward” Strategy: We chose this for its ability to provide a massive one-off tax shield, which is invaluable during high-profit years or when receiving an inheritance.

-

Consolidation to Low-Cost Trackers: This is the best move for long-term health; reducing your annual management charge (AMC) by even 0.5% can result in tens of thousands of pounds more in your pot by retirement.

Preparation Checklist

Before you finalize your SIPP contributions for the 2026 period, ensure you have ticked these boxes:

-

Confirm your “Relevant UK Earnings” for the current tax year to ensure you don’t over-contribute.

-

Locate your P60 or final payslip to accurately calculate your higher-rate tax reclaim.

-

Check your “Pension Input Periods” for the last three years to verify your available Carry Forward amount.

-

Review the “Annual Management Charge” (AMC) of your current SIPP provider—anything over 0.45% may be excessive for a simple tracker portfolio.

-

Update your “Expression of Wishes” form to ensure your SIPP assets pass to your chosen beneficiaries tax-efficiently.

Securing Your Financial Independence

Utilizing the SIPP tax relief benefits 2026 offers is one of the most effective ways to build a tax-free nest egg in the UK. By combining disciplined contributions with a strategy that reclaims higher-rate tax and minimizes investment fees, you can significantly shorten your timeline to retirement. Whether you are just starting your career or looking to make a final push toward your goals, the SIPP remains an unparalleled vehicle for wealth preservation and growth in the modern era.

FAQ

How much is the SIPP annual allowance for 2026?

The standard annual allowance for the 2025/26 and 2026/27 tax years is £60,000, which includes contributions from you, your employer, and the government’s tax relief.

Can I get tax relief if I have no income?

Yes, you can contribute up to £2,880 (net) and the government will top it up to £3,600 (gross) using the 20% basic rate relief.

When can I access the money in my SIPP?

Under current rules, you can access your SIPP from age 55, though this is set to rise to age 57 in April 2028.

Is the tax relief added immediately?

The 20% basic rate relief is usually added to your account 6–11 weeks after your contribution, depending on your provider’s schedule with HMRC.