The United Kingdom is rapidly transitioning from a “wait-and-see” approach to becoming one of the most structured digital asset hubs in the world. As we move through 2026, the legislative groundwork laid in late 2025 is now being implemented, creating a clear distinction between regulated financial activities and the unregulated “wild west” of previous years.

How We Selected Our 12 Best UK Crypto Regulation 2025 Updates

To curate this list, we analysed the final Financial Services and Markets Act 2000 (Cryptoassets) Regulations 2025 laid in Parliament on 15 December 2025. Our selection was filtered based on the immediate operational impact for firms, the level of consumer protection introduced, and the strategic importance for the City of London’s global competitiveness. We prioritised developments that affect the broadest range of users, from retail investors to institutional liquidity providers.

12 Critical Updates On UK Crypto Regulation 2025 And Beyond

The following points represent the essential pillars of the UK’s new regulatory architecture, designed to bring cryptoassets into the same high-standard fold as traditional equities and bonds.

1. The Final Expansion of the Regulatory Perimeter

On 15 December 2025, the UK government officially expanded the regulatory perimeter to include “qualifying cryptoassets” and “qualifying stablecoins.” This means that activities like trading, safeguarding, and issuing these assets now fall under the direct supervision of the Financial Conduct Authority (FCA).

-

Best for: Providing legal certainty for institutional investors entering the space.

-

Why We Chose It:

-

It ends years of ambiguity regarding which tokens are “regulated.”

-

It subjects crypto firms to the same “fit and proper” tests as banks.

-

It enables the FCA to take direct enforcement action against non-compliant firms.

-

-

Things to consider: Firms not already registered for AML purposes face a steep learning curve to meet full FSMA authorisation standards.

2. The “FCA Gateway” Application Window

The FCA has announced a specific “application period” for firms wanting to undertake newly regulated crypto activities. This window is scheduled to open on 30 September 2026 and close on 28 February 2027, ahead of the full regime “go-live” date in October 2027.

-

Best for: Existing cryptoasset service providers (CASPs) looking to secure their UK future.

-

Why We Chose It:

-

It provides a structured timeline for firms to prepare their compliance stacks.

-

It includes transitional provisions for firms that apply within the window.

-

It prevents a “bottleneck” of applications on the final commencement date.

-

-

Things to consider: Missing this window could lead to a forced “run-off” and exit from the UK market.

3. Systemic Stablecoin Oversight by the Bank of England

For stablecoins used widely in payments, the Bank of England (BoE) has introduced a “systemic” regime. These issuers are regulated jointly by the BoE for financial stability and the FCA for conduct, ensuring that a collapse cannot threaten the wider UK economy.

-

Best for: Large-scale retail payment providers and “Big Tech” entrants.

-

Why We Chose It:

-

It mandates that 40% of backing assets must be held as unremunerated deposits at the Bank of England.

-

It requires 1:1 redemption at par value in central bank money.

-

It subjects systemic issuers to bank-like capital and liquidity requirements.

-

-

Things to consider: The “unremunerated” deposit requirement may significantly impact the profitability of stablecoin issuers.

4. Holding Limits for Sterling Stablecoins

To manage risks to the traditional banking system, the BoE has proposed temporary holding limits for sterling-denominated systemic stablecoins. These are expected to be set at £20,000 for individuals and £10 million for businesses.

-

Best for: Balancing innovation with the stability of commercial bank deposits.

-

Why We Chose It:

-

It prevents a massive, sudden drain of liquidity from the high-street banks.

-

It mirrors the proposed limits for a potential Digital Pound (Retail CBDC).

-

It allows the regulator to “throttle” adoption while observing market impact.

-

-

Things to consider: These limits may be viewed as a constraint on the utility of stablecoins for high-value transactions.

5. The Dedicated Crypto Market Abuse Regime

The 2025 Regulations introduce a bespoke market abuse regime tailored for cryptoassets. This prohibits insider dealing, unlawful disclosure of inside information, and market manipulation on any UK-authorised trading platform.

-

Best for: Protecting retail investors from “pump and dump” schemes and wash trading.

-

Why We Chose It:

-

It holds platform operators responsible for monitoring and reporting suspicious activity.

-

It applies to anyone trading on a UK platform, regardless of their physical location.

-

It adapts traditional market integrity rules to the unique 24/7 nature of crypto.

-

-

Things to consider: Defining “inside information” in a decentralised project remains a complex legal challenge.

6. Regulation of “Arranging Staking”

Staking is now a specifically regulated activity in the UK. Firms that offer staking services to retail clients must be authorised and must provide clear disclosures about the risks, including “slashing” and “lock-up” periods.

-

Best for: Retail users seeking passive yield with transparent risk profiles.

-

Why We Chose It:

-

It prevents platforms from mis-selling staking as “safe” interest-bearing accounts.

-

It requires the segregation of staked assets to protect them during insolvency.

-

It brings “staking-as-a-service” providers under professional conduct rules.

-

-

Things to consider: Purely decentralised, non-custodial staking remains largely outside the FCA’s direct perimeter.

7. Public Offers and Admissions to Trading

The UK has introduced a “Designated Activities Regime” for the public offering of cryptoassets. Much like a stock market IPO, certain crypto offers will now require an FCA-approved disclosure document (prospectus) unless they fall under specific exemptions.

-

Best for: Standardising the quality of information provided during token launches.

-

Why We Chose It:

-

It creates civil liability for directors who provide misleading information in disclosures.

-

It includes exemptions for “small offers” under £1,000,000.

-

It ensures that only “qualified” investors can access high-risk, unlisted tokens.

-

-

Things to consider: The cost of producing a compliant disclosure document may be prohibitive for smaller projects.

8. The Digital Securities Sandbox (DSS)

Entering its second full year in 2025, the DSS allows firms like HSBC and J.P. Morgan to test the issuance, trading, and settlement of traditional securities (bonds/equities) using DLT.

-

Best for: Investment banks and FMIs (Financial Market Infrastructures) experimenting with T+0 settlement.

-

Why We Chose It:

-

It provides a “safe space” where certain legislative requirements can be waived or modified.

-

It allows for the testing of “hybrid” instruments that blur the lines between crypto and securities.

-

It is a critical part of the UK’s plan to move to a T+1 (and eventually T+0) settlement cycle.

-

-

Things to consider: Participants must meet strict “Gate 1” and “Gate 2” approvals before handling live client assets.

9. Overseas Firm Territorial Scope

The new UK regime has a long reach. Any overseas firm that “directs” cryptoasset services at UK retail consumers must be authorised by the FCA, regardless of where the firm is based.

-

Best for: Ensuring a level playing field between UK-based and offshore exchanges.

-

Why We Chose It:

-

It prevents offshore firms from circumventing UK consumer protections.

-

It effectively bans “reverse solicitation” as a business model for mass-market retail.

-

It allows the FCA to block the websites or apps of non-compliant foreign providers.

-

-

Things to consider: Global firms may choose to geofence the UK entirely to avoid the high cost of local authorisation.

10. HMRC’s New Reporting Requirements (CARF)

In 2025, the UK implemented the Reporting Cryptoasset Service Providers Regulations. This aligns the UK with the OECD’s Crypto-Asset Reporting Framework (CARF), requiring platforms to collect and share user data with HMRC.

-

Best for: Ensuring tax transparency and reducing the “shadow economy” in crypto.

-

Why We Chose It:

-

It automates the sharing of transaction data between exchanges and tax authorities.

-

It introduces stiff penalties for firms that fail to register or report accurately.

-

It reflects the global move toward ending financial anonymity in digital assets.

-

-

Things to consider: Users should expect their 2026 tax returns to be “pre-populated” with data provided by their exchanges.

11. The Digital Pound “Design Phase” Conclusion

The Bank of England and HM Treasury are concluding the “Design Phase” of the Digital Pound (Retail CBDC) in 2026. While a final decision on “issuance” hasn’t been made, the technical blueprint is now clear.

-

Best for: Future-proofing the UK’s sovereignty over the national currency.

-

Why We Chose It:

-

It establishes the “platform model” where the BoE provides the ledger and private firms provide the wallets.

-

It prioritises “Privacy by Design,” ensuring the government cannot see personal spending data.

-

It focuses on “programmability” through APIs rather than the money itself being programmed.

-

-

Things to consider: Public trust remains a hurdle, with significant debate over “financial surveillance” concerns.

12. The Sunset of the “AML-Only” Registration

Firms that are currently “registered” with the FCA for anti-money laundering (AML) purposes must transition to “full authorisation” under FSMA by October 2027. The old AML-only register will eventually be phased out.

-

Best for: Professionalising the entire UK crypto ecosystem.

-

Why We Chose It:

-

It moves the industry from a “checks-only” regime to full-scale prudential and conduct oversight.

-

It ensures that only firms with robust capital and governance survive.

-

It allows authorised crypto firms to be treated as “financial institutions” by banks.

-

-

Things to consider: This transition is expected to lead to a wave of mergers and acquisitions in the UK fintech space.

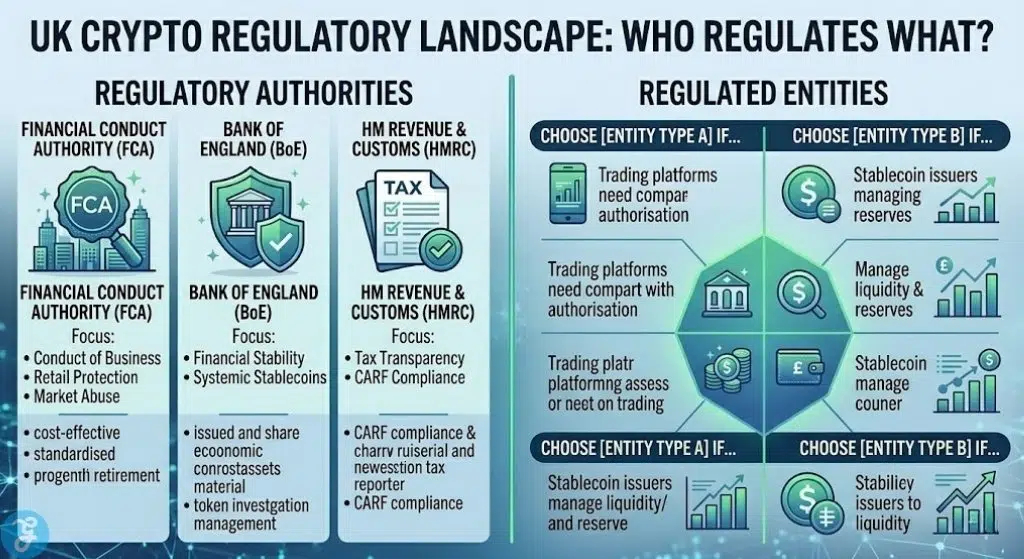

An Overview Of UK Crypto Regulation 2025 And Compliance Trends

The shift towards a “full-fat” regulatory regime is designed to make London the safest and most transparent place in the world to conduct digital asset business. By 2027, the distinction between a “crypto firm” and a “traditional finance firm” will have largely disappeared in the eyes of the law.

Overview Comparison Table

| Regulatory Area | Primary Regulator | Target Assets | Implementation Phase |

| Systemic Stablecoins | Bank of England | Sterling Pegged (Systemic) | Live (Consultation Finalised) |

| Trading Platforms | FCA | Qualifying Cryptoassets | Application Window (Q3 2026) |

| Market Abuse | FCA | All Authorised Platforms | Go-Live (October 2027) |

| Tax Reporting (CARF) | HMRC | All Service Providers | Live (Reporting starts 2026) |

Our Top 3 Picks and Why?

Of the 12 updates, the Final Expansion of the Regulatory Perimeter, the FCA Gateway Window, and the Systemic Stablecoin Regime are the most critical. These three pillars define whether a firm can legally exist in the UK, when they must apply for permission, and how the most important assets (stablecoins) must be backed to protect the public.

Buyer’s Guide: How to Choose the Right UK Crypto Platform by Yourself?

As the UK regime matures, choosing a platform is no longer about who has the lowest fees, but who has the strongest regulatory standing.

The Selection Framework:

-

Authorisation Status: Check the FCA Financial Services Register. Avoid firms that are only “temporarily registered” if you are looking for long-term stability.

-

Custody Arrangements: Ensure the firm uses UK-authorised “qualified custodians” and has clear segregation of assets.

-

Risk Disclosures: Under the new rules, a firm MUST show you clear, non-misleading risk warnings. If they “game” these warnings, they are likely non-compliant.

Decision Matrix (Table):

| Choose Platform A if… | Choose Platform B if… |

| You are a UK retail investor wanting FSCS-like protections (where applicable). | You are a professional trader seeking high leverage and offshore liquidity. |

| You prioritise holding a regulated Sterling Stablecoin. | You are comfortable with “unbacked” tokens and self-custody. |

| You need integrated tax reporting for HMRC. | You prioritised anonymity and decentralised governance. |

The Final Checklist: 5 Things to Verify Before Your Next UK Crypto Trade

-

Is the platform listed on the FCA register for “Cryptoasset Activities”?

-

Have you read the mandatory “Risk Summary” provided by the firm?

-

Does the firm have a clear UK-based subsidiary for its retail operations?

-

Are your stablecoin holdings compliant with the new “systemic” backing rules?

-

Does the firm provide a clear pathway for “redemption at par” for its stablecoins?

The Future of the UK’s Digital Pound and Beyond

The journey towards UK Crypto Regulation 2025 is not just about stopping “bad actors”; it is about building the infrastructure for the next 50 years of British finance. Whether it’s through the Digital Securities Sandbox or the eventual Digital Pound, the UK is clearly positioning itself as the global leader in regulated blockchain innovation.