Navigating the South African healthcare landscape in 2026 requires a clear understanding of how different plans impact both your physical well-being and your monthly budget. With medical inflation continuing to outpace general inflation, the choice between a comprehensive medical aid and a focused hospital plan has never been more critical for South African households.

How We Selected Our 9 Key Differences Between Health Plans

To ensure this guide provides practical value, we analyzed the 2026 benefit structures from the primary medical schemes available in the country. Our selection criteria focused on the factors that most frequently result in out-of-pocket expenses or billing surprises for members.

-

Financial Impact: We prioritized differences that significantly affect monthly premiums versus long-term savings.

-

Clinical Necessity: We looked at how each plan handles chronic conditions and emergency care.

-

Accessibility: We evaluated how network restrictions vary between these two types of cover.

The following criteria served as the foundation for our comparative analysis of the local health insurance market.

| Criteria | Importance | Focus Area |

| Out-of-Hospital Cover | High | GP visits, meds, and specialists |

| Premium Variance | High | Monthly affordability vs risk |

| Chronic Management | Medium | Number of conditions covered |

| Diagnostic Access | Medium | Blood tests and X-rays |

9 Vital Factors: Medical Aid vs Hospital Plan South Africa in 2026

Understanding these distinctions is the first step toward choosing a plan that aligns with your life stage and health profile. While both products provide a safety net, their daily utility varies drastically.

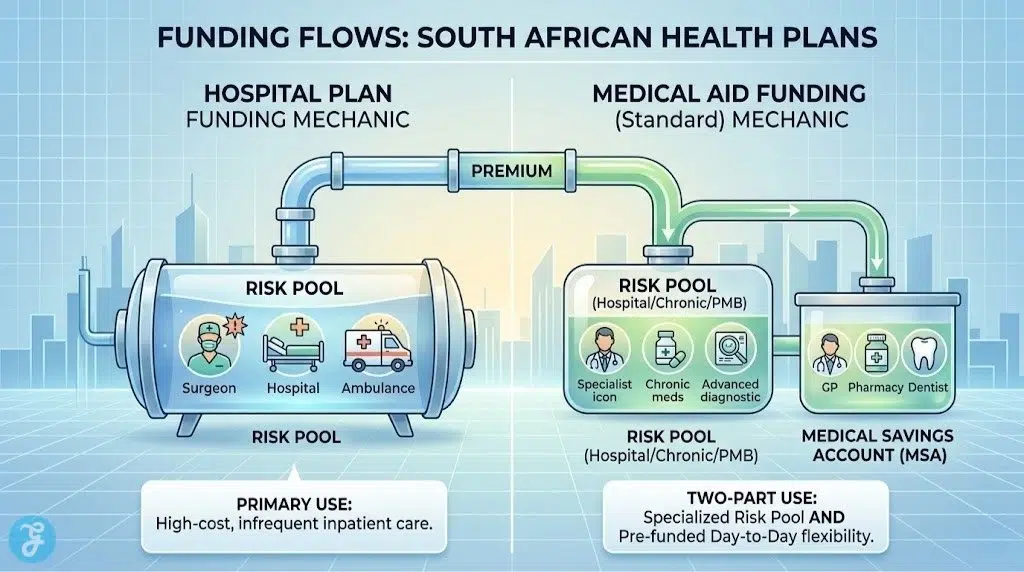

1. Day-to-Day Benefit Coverage

Comprehensive medical aid plans are designed to handle your everyday health needs, from a sudden flu to a routine check-up. These plans provide a dedicated pool of funds or defined benefits to cover general practitioner visits and prescribed medications without you needing to tap into your personal savings.

Best for: Families with young children or individuals who visit the doctor frequently.

Why We Chose It: This represents the primary functional difference that affects your daily wallet.

Things to consider: Hospital plans provide zero cover for these visits, meaning every GP trip is a cash expense.

2. Monthly Premium Affordability

There is a substantial price gap between these two tiers of cover, with hospital plans serving as the entry-level gateway to private healthcare. In 2026, hospital plans remain the most accessible option for young professionals, often costing significantly less than their comprehensive counterparts.

Best for: Healthy, budget-conscious individuals who only want protection against major medical events.

Why We Chose It: Cost is the most significant barrier to entry for private healthcare in South Africa.

Things to consider: A lower premium often correlates with a higher risk of out-of-pocket expenses for routine care.

3. Medical Savings Account (MSA) Access

Most mid-to-high-level medical aid plans include a Medical Savings Account, which is a portion of your monthly premium set aside for your exclusive use. This fund acts as a buffer for out-of-hospital expenses, giving you a sense of flexibility that basic hospital plans lack entirely.

Best for: Members who want a predictable “bucket” of money for dental, optical, or pharmacy needs.

Why We Chose It: The MSA is a unique financial tool within the South African medical scheme environment.

Things to consider: Once the MSA is depleted, you may enter a self-payment gap depending on your plan.

4. Chronic Medication Limits

While all South African plans must cover the 26 Chronic Disease List (CDL) conditions by law, comprehensive medical aids go much further. They often cover dozens of additional conditions, providing a much-needed lifeline for those managing more complex or rare health issues.

Best for: Individuals diagnosed with non-standard chronic conditions like acne, eczema, or depression.

Why We Chose It: Chronic medicine is a recurring, high-cost expense that can drain a personal budget quickly.

Things to consider: Hospital plans generally stick to the legal minimum, which may not cover your specific needs.

5. Specialist Consultation Rates

In the event of a serious health issue, you will likely need to see a specialist, and their billing often exceeds standard scheme rates. Comprehensive plans frequently cover these specialists at 200% or even 300% of the scheme rate, whereas hospital plans typically cap coverage at 100%.

Best for: High-risk individuals who may require surgery or advanced medical interventions.

Why We Chose It: This difference protects members from massive co-payment bills after a hospital stay.

Things to consider: Without high specialist cover, you will likely need to purchase separate Gap Cover.

6. Screening and Prevention Access

Modern medical aids have shifted toward a preventative model, offering a suite of wellness checks like pap smears and mammograms as part of the core benefit. While some hospital plans offer basic screenings, the comprehensive versions are far more exhaustive and incentivized through rewards programs.

Best for: Proactive individuals focused on long-term health maintenance and early detection.

Why We Chose It: Prevention is significantly cheaper and safer than treating a developed illness.

Things to consider: Check if your plan requires you to use specific network providers for these tests.

7. Out-of-Hospital Diagnostic Tests

If you need a blood test or an X-ray that is not related to a hospital admission, a comprehensive medical aid will usually pay for it from your savings or a dedicated benefit. On a hospital plan, these diagnostic procedures are almost always for your own account unless they are directly linked to a specific legal requirement.

Best for: Patients undergoing investigative treatments who have not yet been admitted to a ward.

Why We Chose It: Diagnostic costs are a common hidden expense that surprises new medical aid members.

Things to consider: High-end scans like MRIs often require a significant co-payment on lower-tier plans.

8. Dental and Optical Benefits

Comprehensive medical aids treat dental and optical care as essential components of health, often providing specific sub-limits for frames, lenses, and basic dentistry. Hospital plans view these as elective expenses, offering no financial support for your next pair of glasses or a tooth extraction.

Best for: Anyone with a history of vision issues or those who prioritize oral hygiene.

Why We Chose It: These are high-frequency needs that almost everyone encounters at least once a year.

Things to consider: Dental benefits on medical aid often come with strict managed care protocols.

9. Threshold Coverage Availability

The Threshold Benefit is a safety net found only on premium comprehensive plans. Once you have spent a certain amount on day-to-day claims, the scheme begins paying for your claims again, even if your savings are finished. Hospital plans do not have this feature.

Best for: Families who consistently exhaust their medical savings before the year ends.

Why We Chose It: It provides a unique level of unlimited peace of mind for high-usage households.

Things to consider: Plans with a threshold benefit are among the most expensive options on the market.

An Overview Of Medical Aid vs Hospital Plan South Africa

Choosing between these options requires a side-by-side comparison of how they handle different medical scenarios. The following breakdown highlights the core operational differences you will encounter during a typical benefit year.

| Feature | Comprehensive Medical Aid | Basic Hospital Plan |

| GP Visits | Covered (Savings or Benefit) | Out-of-pocket (Cash) |

| Emergency Room | Usually covered in full | Only if it leads to admission |

| Prescription Meds | Covered (Subject to limits) | Out-of-pocket (Cash) |

| Chronic Care | Extended list of conditions | Limited to 26 CDL conditions |

| Maternity | Full pre-natal and birth cover | Mostly birth and limited pre-natal |

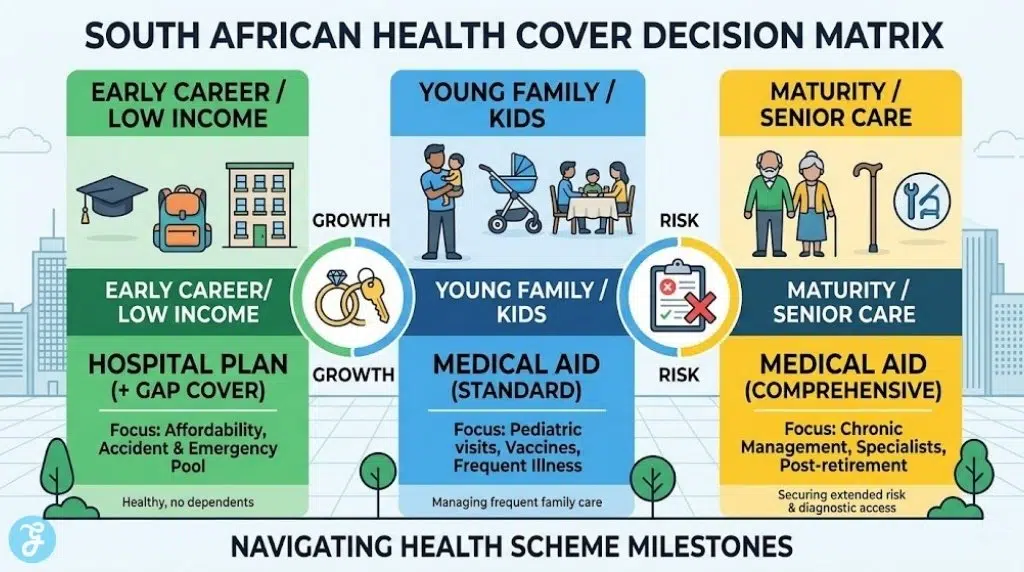

Our Top 3 Picks and Why?

-

The Young Healthy Professional: A hospital plan paired with a good Gap Cover is the most logical choice here. Since health risks are low and the budget is often tight, paying for day-to-day benefits you will not use is a waste of capital.

-

A Growing Family: Comprehensive medical aid is essential. With frequent pediatrician visits and the high cost of childhood medications, the upfront premium is easily recovered through the usage of benefits.

-

Retirees with Chronic Needs: High-level medical aid with an extended chronic list is non-negotiable. At this life stage, the risk of needing specialized care and expensive ongoing medication makes a basic hospital plan a dangerous financial gamble.

How to Choose the Right Medical Aid vs Hospital Plan South Africa by Yourself?

Making the final call involves a realistic assessment of your health history and your financial resilience. Use the following framework to determine which direction suits your current lifestyle.

The Selection Framework

-

Review Your Past Year: Look at your bank statements to see exactly how much you spent on out-of-hospital healthcare in 2025.

-

Assess Your Savings: If you had a large emergency tomorrow, could you pay it in cash? If not, a plan with higher specialist cover is better.

-

Check Provider Networks: Ensure the hospitals and doctors near your home are on the approved list for the plan you are considering.

-

Evaluate Family Planning: If you plan on starting a family in the next year, moving to a comprehensive plan now avoids waiting periods later.

The following matrix simplifies the decision-making process based on your specific health and financial profile.

| Choose Medical Aid if… | Choose a Hospital Plan if… |

| You have chronic conditions like Asthma. | You are young and have no known health issues. |

| You have children who need regular check-ups. | You have a healthy emergency fund for doctor visits. |

| You want the convenience of a swipe card. | You only want protection against major accidents. |

| You prefer fixed monthly costs over variable ones. | You want the lowest possible monthly commitment. |

The Final Checklist

-

Confirm that the plan covers the specific private hospital closest to your home.

-

Verify if your current chronic medication is on the scheme’s 2026 formulary.

-

Check the Late Joiner Penalty status if you are over the age of 35.

-

Compare the specialist coverage rate (is it 100%, 200%, or more?).

-

Ensure you understand the waiting periods for pre-existing conditions.

Strategizing Your Healthcare Spend for 2026

The decision between medical aid and a hospital plan is not just about healthcare; it is about financial risk management. By selecting a plan that matches your actual usage patterns rather than your fears, you can ensure that every Rand spent on premiums provides the maximum possible protection for you and your family as we move through 2026.

Frequently Asked Questions About Medical Aid vs Hospital Plan South Africa

Can I upgrade from a hospital plan to a medical aid at any time?

Answer: You can generally only upgrade at the end of the year for the following benefit year. However, some schemes allow upgrades during the year if you experience a life event like marriage or a new baby.

Does a hospital plan cover the emergency room?

Answer: Most hospital plans only cover the ER if the visit results in you being admitted to a ward. If you are treated and sent home, the bill is usually for your own account.

Is medical insurance the same as a hospital plan?

Answer: No, medical insurance is governed by different laws and usually pays out a fixed daily cash amount. A hospital plan is a medical scheme product that pays the hospital directly for actual costs.

Do both types of plans offer tax credits?

Answer: Yes, as long as the product is a registered medical scheme in South Africa, you can claim the Medical Schemes Fees Tax Credit on your annual tax return.

Which option is better for dental work?

Answer: Comprehensive medical aid is significantly better as it includes specific benefits for fillings and extractions. Hospital plans offer almost no dental coverage unless the procedure is related to a severe trauma.