Finland has long been a global leader in the evolution of money, having launched the world’s first electronic cash system, the Avant card, over three decades ago. As we navigate through 2026, the Bank of Finland (Suomen Pankki) is once again at the forefront of financial innovation, serving as a critical hub within the Eurosystem’s digital euro project. This exploration is not merely a technical exercise; it is a strategic effort to ensure that the Finnish banking system remains resilient, competitive, and autonomous in an increasingly digital global economy. By integrating cutting-edge technology with traditional central bank stability, Finland is defining how a modern nation can transition to a digital-first monetary anchor.

For those monitoring Finland CBDC Exploration, the progress made this year represents a definitive shift from theoretical research to real-world readiness.

Selection Methodology

To identify the most impactful ways the Finnish banking system is exploring Central Bank Digital Currency (CBDC), we analysed recent progress reports from the European Central Bank and the Bank of Finland’s 2026 strategic objectives. Our criteria focused on initiatives that provide tangible benefits to Finnish citizens and financial institutions, such as enhanced offline resilience, cross-border efficiency, and integration with national digital identity frameworks. Each method represents a core pillar of Finland’s commitment to maintaining a secure and inclusive payment ecosystem that bridges the gap between physical cash and the digital future.

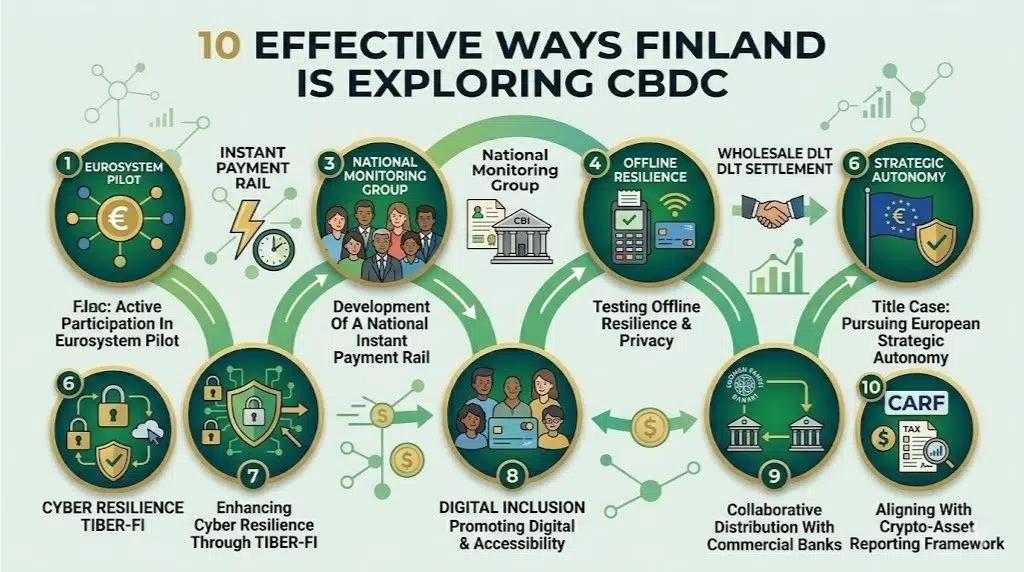

10 Effective Ways Finland’s Banking System Is Exploring Central Bank Digital Currency

The current exploration phase highlights a shift from research to practical, large-scale preparation. Finland is leveraging its advanced digital infrastructure to test how a digital euro could function in everyday retail purchases and complex wholesale settlements. These initiatives are designed to ensure that sovereign digital money is not just a replacement for cash, but a versatile tool that adds unique value to the Finnish economy while maintaining the highest standards of privacy.

1. Active Participation In The Eurosystem Preparation Phase

As a member of the Eurosystem, the Bank of Finland is deeply involved in the current 2026 preparation phase for the digital euro. This phase involves refining the technical rulebook and selecting providers for the digital platform. Finland provides critical input on how the currency should be distributed through existing commercial bank apps, ensuring a seamless experience for Finnish consumers.

Best for: Commercial banks, payment service providers, and fintech developers.

Why We Chose It:

● It ensures the Finnish banking sector has a direct influence on the design and functionality of the digital euro.

● It allows for the alignment of national infrastructure with broader European standards.

Things to consider: The final decision to issue the digital euro depends on the successful completion of this phase and the passing of EU legislation.

2. Development Of A National Instant Payment Rail

The Bank of Finland is coordinating a national instant payment solution that is independent of international card rails like Visa or Mastercard. This system, based on SEPA Instant standards, serves as a functional precursor to a CBDC by enabling real-time, 24/7 credit transfers. By building this “real-time” foundation, Finland is preparing its banks for the instant settlement requirements of a digital euro.

Best for: Retailers, small businesses, and peer-to-peer (P2P) payment users.

Why We Chose It:

● It reduces national dependence on non-European payment providers.

● It creates a modern settlement infrastructure that can easily host future CBDC transactions.

Things to consider: While highly efficient, this system currently relies on commercial bank money rather than central bank digital currency.

3. Leadership Of The National Monitoring Group

Since 2022, the Bank of Finland has led a National Monitoring Group consisting of commercial banks, service providers, and public authorities. In 2026, this group is focusing on the practical “user journey” of a digital euro, ensuring that the transition does not disrupt the stability of the Finnish financial system or the business models of local banks.

Best for: Financial policy makers, bank executives, and regulatory compliance officers.

Why We Chose It:

● It fosters a collaborative environment where the private sector can voice concerns and share technical insights.

● It ensures that the digital euro is designed to meet the specific needs of the Finnish market.

Things to consider: The group must balance the innovation of a CBDC with the need to protect bank deposits from sudden outflows.

4. Testing Offline Resilience And Privacy

A key area of Finland CBDC Exploration is the development of an offline payment feature. This functionality allows users to make digital payments even when internet connectivity is lost, providing a cash-like level of privacy and security. For a country like Finland, with a vast geography and high emphasis on national security, offline resilience is considered a critical requirement for any digital currency.

Best for: Citizens in rural areas, emergency responders, and privacy-conscious consumers.

Why We Chose It:

● It mimics the “sovereign” nature of physical cash in a digital format.

● It ensures that the payment system remains functional during power outages or cyber disruptions.

Things to consider: Offline transactions require specialized hardware or secure elements within smartphones to prevent double-spending.

5. Wholesale DLT Settlement Via Pontes And Appia

Beyond retail payments, Finland is participating in the Eurosystem’s Pontes and Appia initiatives. These projects explore how Distributed Ledger Technology (DLT) can be used to settle wholesale financial transactions—such as bond trades or interbank transfers—in central bank money. A solution for DLT-based cash settlement is expected to launch in the third quarter of 2026.

Best for: Institutional investors, hedge funds, and large-scale financial institutions.

Why We Chose It:

● It brings the efficiency of blockchain technology to traditional wholesale banking.

● It reduces settlement times and counterparty risks for high-value financial transactions.

Things to consider: This requires significant technical upgrades to the existing TARGET services used by the Bank of Finland.

6. Pursuing European Strategic Autonomy

Finland’s exploration is driven by a desire to strengthen Europe’s strategic autonomy in the payments sector. Currently, the majority of digital payments in Finland are processed by entities outside the euro area. By developing a digital euro and supporting local instant payment solutions, the Bank of Finland aims to regain control over the “rails” on which the national economy runs.

Best for: National security strategists and proponents of European economic sovereignty.

Why We Chose It:

● It safeguards the Finnish economy from external geopolitical shifts.

● It encourages the growth of a local, innovative fintech ecosystem within the Eurosystem.

Things to consider: Achieving full autonomy will require a high level of adoption by both merchants and consumers.

7. Enhancing Cyber Resilience Through TIBER-FI

As part of the CBDC journey, Finland has implemented the TIBER-FI framework (Threat Intelligence-based Ethical Red Teaming). This initiative tests the cyber resilience of the entire Finnish financial sector against sophisticated threats. This is essential for a CBDC, as the digital euro must be “bulletproof” against state-sponsored cyber-attacks and large-scale fraud.

Best for: Cybersecurity professionals and financial stability analysts.

Why We Chose It:

● It ensures that the digital infrastructure supporting a CBDC is tested under realistic conditions.

● It builds public trust in the security of digital sovereign money.

Things to consider: These “red teaming” exercises are highly resource-intensive and require constant updates to match evolving threats.

![]()

8. Promoting Digital Inclusion And Accessibility

Finland is prioritising the development of CBDC tools that are accessible to everyone, including the elderly and those with disabilities. The Bank of Finland is exploring dedicated “payment cards” or simplified devices that allow people to use the digital euro without needing a smartphone or an internet connection, ensuring no citizen is left behind in the cashless transition.

Best for: The elderly, digitally vulnerable groups, and individuals without smartphones.

Why We Chose It:

● It upholds the principle of money as a public good available to all citizens.

● It prevents the “digital divide” from excluding vulnerable people from the modern economy.

Things to consider: The cost of distributing and maintaining physical CBDC devices must be balanced against their social utility.

9. Collaborative Distribution With Commercial Banks

The Finnish model for CBDC exploration relies on a “two-tier” system. Suomen Pankki issues the digital currency, but private commercial banks handle the distribution and customer service. This ensures that the digital euro complements existing banking services rather than competing with them, allowing banks to offer value-added services on top of the digital euro platform.

Best for: Retail bank customers and existing financial service providers.

Why We Chose It:

● It leverages the existing relationships and infrastructure of commercial banks.

● It prevents the central bank from becoming a direct competitor to private financial institutions.

Things to consider: Banks will need to invest in updating their front-end systems to support digital euro wallets.

10. Aligning With The Crypto-Asset Reporting Framework

While CBDCs are not cryptocurrencies, Finland is using the implementation of the Crypto-Asset Reporting Framework (CARF) in 2026 as a regulatory baseline. This framework ensures transparency and compliance across all digital assets. By leading the EU in CARF adoption, Finland is creating a regulated environment where a digital euro can coexist safely with other tokenised assets.

Best for: Tax authorities, regulatory bodies, and digital asset service providers.

Why We Chose It:

● It establishes a clear legal and reporting environment for all forms of digital value.

● It prevents the digital euro ecosystem from being used for illicit activities or tax evasion.

Things to consider: Compliance requirements for CARF are stringent and may pose challenges for smaller fintech startups.

Strategic Analysis Of Finland’s CBDC Progress

The following table provides a comparison of the key pillars within Finland’s digital currency strategy and their current stage of development as of mid-2026.

Managing the transition requires a balance between technical innovation and national financial security.

| Initiative Pillar | Primary Objective | Current 2026 Status |

| Retail Digital Euro | Consumer Payments | Preparation Phase |

| Instant Payments | Non-Card Rails | National Implementation |

| Wholesale DLT | Interbank Settlement | Pilot Launch (Q3 2026) |

Our Top 3 Picks And Why?

Of the ten strategies currently being explored, these three represent the most vital contributions to Finland’s future financial stability.

-

National Instant Payment Rail: This is a “quick win” that provides immediate benefits to the economy while building the necessary infrastructure for a full CBDC.

-

Offline Resilience Testing: For a nation with Finland’s security profile, the ability to pay without a network is a non-negotiable feature for digital sovereign money.

-

Wholesale DLT Settlement: By launching the Pontes and Appia solutions in 2026, Finland is positioning its institutional banks at the forefront of the global tokenised economy.

Preparation Checklist

If you are a financial stakeholder or a merchant operating in the Finnish market, use this checklist to ensure you are ready for the digital currency shift.

● Review Infrastructure: Assess whether your current payment terminals can support potential digital euro wallets or offline NFC payments.

● Monitor Legislation: Keep a close watch on the European Parliament’s progress on the digital euro regulation expected late this year.

● Enhance Cybersecurity: Align your internal security protocols with the TIBER-FI standards to ensure resilience against digital asset threats.

● Evaluate Liquidity: Commercial banks should model the potential impact of deposit shifts into digital euro accounts once the holding limits are finalised.

Pioneering The Future Of Sovereign Money

Finland’s journey toward a Central Bank Digital Currency is a testament to its legacy as a digital innovator. By actively shaping the digital euro project and building national instant payment alternatives, Suomen Pankki is ensuring that the Finnish people continue to have access to safe, public money in an increasingly private, digital world. The move away from traditional card rails toward a sovereign digital ecosystem marks the beginning of a new chapter in European financial history. Those who adapt to these changes now will be best positioned to thrive in the regulated, efficient, and resilient economy of tomorrow.