The current fiscal climate in Britain has placed unprecedented pressure on property investors, with recent legislative shifts making the disposal of buy-to-let assets more costly than ever. For many investors, the rise in UK Capital Gains Tax (CGT) has significantly eroded potential profits, transforming what was once a straightforward exit strategy into a complex tax puzzle. However, by understanding the reliefs and allowances available under HMRC rules, landlords can legally and ethically minimise their liability.

This guide provides a strategic roadmap for those looking to protect their hard-earned equity in a tightening regulatory environment.

How We Selected These Tax Mitigation Strategies

Our selection process for these strategies involved a comprehensive review of current HMRC manuals and the latest Finance Act updates as of early 2026. We prioritised methods that offer the highest potential savings while remaining fully compliant with anti-avoidance legislation. Each strategy has been vetted for its practical applicability to individual landlords, ensuring that whether you own a single flat or a diverse portfolio, there is a clear path to reducing your UK Capital Gains Tax burden.

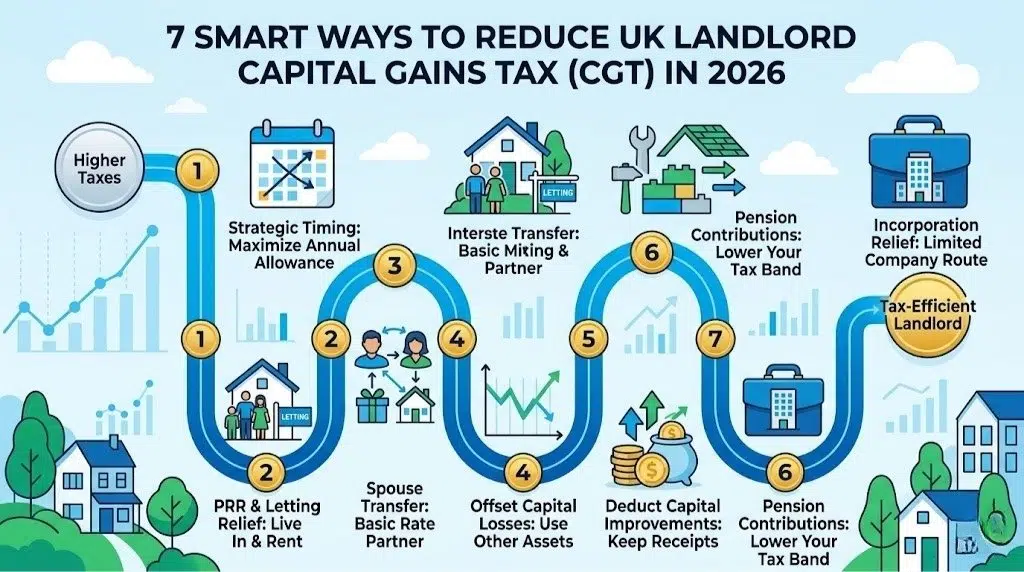

7 Smart Ways To Reduce UK Capital Gains Tax For Landlords

The following strategies represent a blend of traditional tax planning and modern structural shifts. By moving away from reactive disposal and towards proactive fiscal management, property owners can ensure they are not paying a penny more in UK Capital Gains Tax than is legally required. These methods focus on timing, expense tracking, and ownership structures to provide a multifaceted approach to tax efficiency.

1. Maximising The Annual Exempt Amount Through Strategic Timing

The annual CGT allowance remains a vital tool for reducing your overall bill. By timing the exchange of contracts across two different tax years, a landlord or a couple can effectively double their tax-free threshold. This is particularly effective for those disposing of multiple assets or lower-value properties where the gain is closer to the exemption limit.

Best for: Individual landlords or couples selling property with moderate capital growth.

Why We Chose It:

- It is the most straightforward “day-one” strategy for any investor.

- It requires zero upfront cost, relying purely on administrative timing.

Things to consider: The relevant date for CGT is the date contracts are exchanged, not the completion date.

2. Leveraging Private Residence Relief And Letting Relief

If you lived in the property as your main home before letting it out, you are entitled to Private Residence Relief (PRR). While Letting Relief was significantly restricted in 2020, it still applies if you shared occupancy with a tenant. Correctly calculating the “final period of ownership” exemption—currently set at the final nine months—can shave thousands off your final bill.

Best for: Landlords who previously occupied their rental property as their primary residence.

Why We Chose It:

- PRR is one of the most generous reliefs in the UK tax system.

- It rewards landlords for their history with the property rather than just their current status.

Things to consider: You must be able to prove “quality of occupation” to HMRC to satisfy residency requirements.

3. Transferring Ownership To A Spouse Or Civil Partner

Inter-spouse transfers occur on a “no gain, no loss” basis, meaning no UK Capital Gains Tax is triggered at the point of transfer. If one partner is in a lower income tax bracket or has their full annual CGT allowance unused, transferring a portion or the entirety of the property before sale can significantly lower the effective tax rate from 24% to 18% (for residential property).

Best for: Married couples or civil partners where one person is a basic-rate taxpayer.

Why We Chose It:

- It allows for “income splitting” which lowers the marginal rate of tax applied to the gain.

- It effectively doubles the available annual exempt amount for the household.

Things to consider: The transfer must be an unconditional gift and completed well before the exchange of contracts.

4. Offsetting Capital Losses From Other Assets

The tax system allows you to carry forward capital losses from previous years or offset losses incurred in the same tax year against your gains. This includes losses from the sale of other properties, shares, or even certain unlisted securities. It is essential to report these losses to HMRC within four years of the end of the tax year in which they occurred.

Best for: Investors with a diverse portfolio of assets beyond just residential property.

Why We Chose It:

- It turns a financial setback into a strategic tax advantage.

- Losses can be “banked” indefinitely if reported correctly, providing a future tax shield.

Things to consider: You cannot use capital losses to reduce your income tax, only your capital gains.

5. Deducting Allowable Capital Expenditure

Many landlords fail to keep adequate records of “capital improvements” made during their period of ownership. Unlike revenue expenses (like minor repairs), capital expenditure—such as building an extension, installing a new security system, or adding a conservatory—can be deducted from the final sale price when calculating your gain.

Best for: Long-term landlords who have significantly upgraded their properties over time.

Why We Chose It:

- It directly reduces the taxable gain by increasing the “cost base” of the asset.

- It ensures you are only taxed on the genuine profit, not the money you reinvested.

Things to consider: You must retain invoices and receipts as evidence for HMRC in the event of an audit.

6. Utilising Pension Contributions To Lower Your Tax Band

The rate of UK Capital Gains Tax you pay depends on your total taxable income. If your gain pushes you into the higher-rate tax bracket, you may pay 24% on the gain. By making a significant “one-off” contribution to a SIPP or personal pension, you can effectively lower your taxable income, potentially keeping more of your gain within the 18% tax threshold.

Best for: Landlords who are hovering near the threshold between basic and higher-rate tax.

Why We Chose It:

- It provides a double benefit: reducing tax today while building wealth for retirement.

- It is a completely legal way to “manage” your marginal tax rate.

Things to consider: Ensure you do not exceed your annual pension allowance, which could trigger a separate tax charge.

7. Incorporating Your Property Portfolio

For landlords with multiple properties, moving the assets into a limited company structure can offer long-term CGT benefits. While the initial transfer may trigger CGT, “Incorporation Relief” can sometimes defer this gain. Once inside a company, the disposal of assets is subject to Corporation Tax rather than CGT, which can often be more favourable depending on the company’s profit levels.

Best for: Portfolio landlords planning to hold and grow their assets over decades.

Why We Chose It:

- It provides a more professionalised structure with better interest deductibility.

- It allows for easier succession planning and lower tax rates on retained profits.

Things to consider: This is a high-cost strategy that requires professional legal and tax advice to execute correctly.

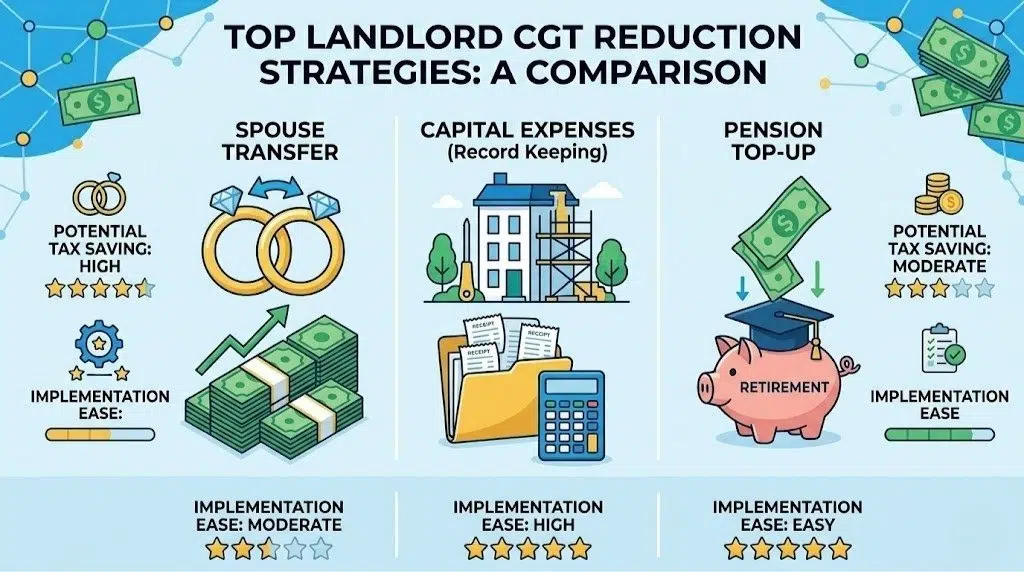

Comparative Analysis Of Tax Savings

To help you prioritise which method might suit your current circumstances, we have outlined a comparison of the most common strategies and their typical impact on your tax return.

The following table illustrates the potential efficiency of each strategy based on ease of implementation and financial impact.

| Strategy | Implementation Ease | Potential Tax Saving |

| Spouse Transfer | Moderate | High |

| Capital Expenses | High (Record Keeping) | Moderate |

| Pension Top-up | Easy | Moderate |

Our Top 3 Picks For Efficiency And Ease

When evaluating which strategies provide the best “bang for your buck” with the least administrative friction, these three options stand out as the gold standard for UK property owners.

-

Transferring to a Spouse: It is the most effective way to utilise two tax-free allowances and access lower tax bands instantly.

-

Deducting Capital Improvements: It is often overlooked but provides a significant reduction in taxable profit by simply keeping better records.

-

Strategic Timing: It costs nothing to wait until a new tax year to exchange contracts, yet it can save thousands in a single move.

Professional Compliance Checklist

If you are preparing to sell a property in 2026, ensure you have checked the following boxes to remain compliant with HMRC and minimise your UK Capital Gains Tax.

● Valuation Accuracy: Ensure you have a professional valuation for the date of acquisition and disposal.

● Record Retrieval: Collate all invoices for structural improvements and legal fees from the original purchase.

● Reporting Deadlines: Remember that you must report and pay any CGT due on UK residential property within 60 days of completion.

● Spouse Verification: If transferring ownership, ensure the deed of trust is correctly executed before the sale process begins.

Securing Your Financial Future

Managing UK Capital Gains Tax is not about evasion; it is about utilising the legitimate reliefs provided by the government to ensure the UK’s rental sector remains viable for private investors. While the tax burden has undoubtedly increased, those who apply these strategies with precision will find themselves in a much stronger financial position. By taking the time to plan your exit today, you can protect the legacy of your property investment for tomorrow.