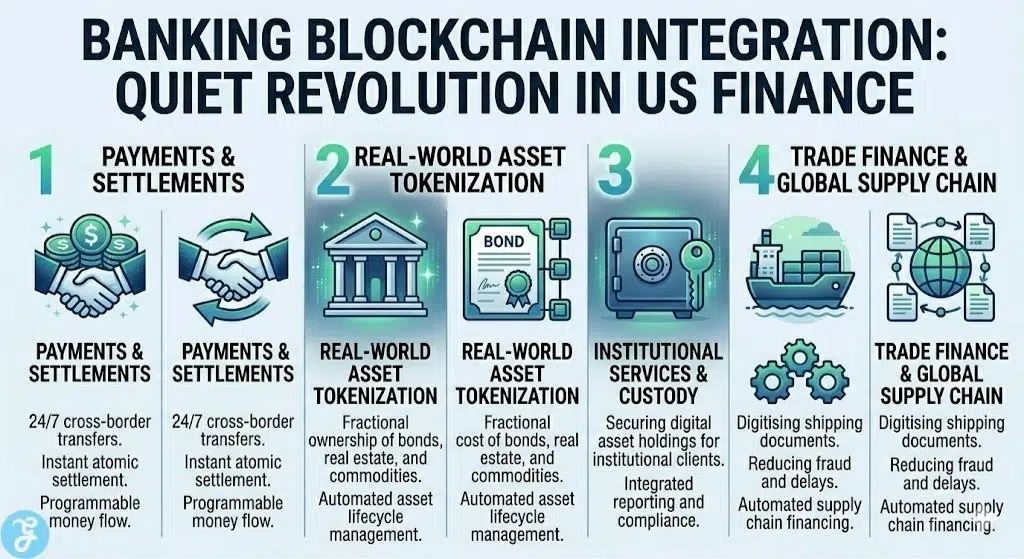

The integration of blockchain technology within the American banking sector has moved far beyond the experimental “pilot” phase. In 2026, the world’s largest financial institutions are now deploying distributed ledger technology (DLT) at a production scale to modernise everything from intraday lending to global liquidity management.

How We Selected Our 15 Best Banking Blockchain Integrations

To identify these developments, we analysed quarterly earnings reports, partnership announcements from the Canton Network, and technical whitepapers from the Bank for International Settlements (BIS). Our selection was filtered by three criteria: the volume of capital currently moving through these systems, the level of regulatory approval granted in 2025, and the specific efficiency gains—such as T+0 settlement—that these integrations provide compared to legacy SWIFT and Fedwire systems.

15 Strategic Ways US Banks Are Using Blockchain In 2026

The following points represent the quiet infrastructure revolution currently occurring inside the world’s most powerful financial institutions.

1. JPM Coin and the Kinexys Rebrand

JPMorgan Chase has evolved its Onyx division into Kinexys, a platform that now processes over $1 billion in daily transactions. By using JPM Coin, corporate clients can move US Dollars and Euros 24/7 across the bank’s global network without waiting for traditional banking hours.

-

Best for: Multi-national corporations managing global treasury operations.

-

Why We Chose It:

-

It enables “atomic settlement,” where the transfer of assets and payment happens simultaneously.

-

It eliminates the need for nostro/vostro account reconciliation.

-

-

Things to consider: It remains a permissioned, “walled garden” system available only to JPMorgan’s institutional clients.

2. The Canton Network’s Interoperability

Backed by Goldman Sachs, BNY Mellon, and Cboe, the Canton Network acts as a “blockchain of blockchains.” It allows different financial institutions to link their private ledgers together for real-time synchronization of data and value.

-

Best for: Synchronising complex trades across different banks without a central intermediary.

-

Why We Chose It:

-

It preserves privacy while allowing applications to “talk” to one another.

-

It handles over $6 trillion in tokenized real-world assets (RWAs).

-

-

Things to consider: Participating banks must run their own validator nodes, which requires significant technical overhead.

3. Tokenized Collateral Networks (TCN)

Banks are now tokenizing Money Market Fund (MMF) shares to be used as collateral in derivatives and repo trades. This allows a bank to “move” collateral in seconds rather than the typical 24–48 hours required for traditional settlement.

-

Best for: Hedge funds and banks needing to meet margin calls instantly.

-

Why We Chose It:

-

It unlocks liquidity in assets that were previously “trapped” during settlement.

-

It reduces the systemic risk of failed trades during periods of market volatility.

-

-

Things to consider: The legal framework for “rehypothecation” (reusing collateral) on-chain is still being refined by the SEC.

4. Citigroup’s CIDAP Platform and Solana

Citigroup has integrated its Citi Institutional Digital Assets Platform (CIDAP) with the Solana blockchain to tokenize and settle promissory notes. This marks a rare instance of a major US bank leveraging a high-speed public network for core financial products.

-

Best for: Global distribution of private debt and commercial paper.

-

Why We Chose It:

-

It leverages Solana’s sub-second finality to achieve near-instant settlement.

-

It abstracts the complexity so clients don’t need to manage their own digital wallets.

-

-

Things to consider: The choice of a public network introduces different security and regulatory scrutiny compared to private chains.

5. Project Agorá and Cross-Border Wholesale CBDCs

Led by the Federal Reserve Bank of New York and the BIS, Project Agorá is testing a “unified ledger” for cross-border payments. It combines tokenized commercial bank deposits with wholesale central bank money on a single, programmable platform.

-

Best for: Replacing the slow and expensive correspondent banking model.

-

Why We Chose It:

-

It addresses “cut-off times” and time-zone differences that delay global payments.

-

It integrates compliance checks (KYC/AML) directly into the payment’s smart contract.

-

-

Things to consider: A full launch is not expected until the latter half of 2026 following rigorous testing.

6. Goldman Sachs’ GS DAP™ Platform

Goldman Sachs has deployed a dedicated Digital Asset Platform (GS DAP™) to facilitate the issuance of digital bonds. By digitising the bond lifecycle, the bank has reduced the administrative burden of interest payments and redemptions.

-

Best for: Sovereign and corporate bond issuances.

-

Why We Chose It:

-

It automates the entire “lifecycle” of the bond through smart contracts.

-

It provides a real-time golden record of ownership for all participants.

-

-

Things to consider: Secondary market liquidity for these digital bonds is currently lower than for traditional paper-based bonds.

7. Intraday Repo Markets via Broadridge

The repurchase agreement (repo) market is the plumbing of the US financial system. Banks like UBS and SocGen now use Broadridge’s DLT-based repo platform to execute and settle overnight loans in minutes, saving millions in capital costs.

-

Best for: Banks needing to balance their books at the end of the business day.

-

Why We Chose It:

-

It handles over $4 trillion in monthly volume.

-

It allows for “intraday” repos, where a bank can borrow money for just a few hours.

-

-

Things to consider: This integration is largely invisible to everyone except the bank’s head of treasury.

8. Franklin Templeton’s Tokenized Money Funds

The BENJI token, representing shares in the Franklin OnChain U.S. Government Money Fund, is now natively available on multiple blockchains. This allows investors to hold a regulated, interest-bearing asset that can be moved as easily as a stablecoin.

-

Best for: Crypto-native companies needing a safe, yield-bearing place for their cash.

-

Why We Chose It:

-

It is a traditional SEC-registered fund using DLT for its primary record-keeping.

-

It is interoperable across Ethereum, Stellar, and Polygon.

-

-

Things to consider: It still requires a rigorous “off-chain” KYC process to access.

9. The Regulated Liability Network (RLN)

The RLN is a collaboration between giants like Citi, Wells Fargo, and Mastercard. It seeks to create a shared ledger for all “regulated liabilities,” including deposits, to allow for instant, programmable transfers between different institutions.

-

Best for: Creating a “universal” digital dollar that isn’t a CBDC or a private stablecoin.

-

Why We Chose It:

-

It maintains the current two-tier banking system while adding 24/7 capabilities.

-

It prevents the “fragmentation” of money that occurs with too many separate bank tokens.

-

-

Things to consider: It is still in an advanced “experimentation” phase in 2026.

10. Programmable Payments for IoT

Banks are moving toward “streaming” payments. Using blockchain, a corporate client can set a smart contract to automatically pay a logistics provider the moment a GPS sensor confirms a delivery has arrived at a warehouse.

-

Best for: Supply chain finance and automated machine-to-machine payments.

-

Why We Chose It:

-

It removes the manual “invoice and wait” cycle.

-

It reduces the risk of non-payment for vendors.

-

-

Things to consider: This requires high-quality “oracles” to feed real-world data into the blockchain.

11. Digital Debt Servicing

Beyond issuance, banks are using blockchain to manage the complex “servicing” of debt—collecting interest, managing defaults, and handling secondary sales—without the need for thousands of manual emails and spreadsheets.

-

Best for: Managing large portfolios of syndicated loans.

-

Why We Chose It:

-

It creates a “single source of truth” for the loan’s status.

-

It allows for fractional ownership of large loans, increasing market depth.

-

-

Things to consider: Legacy legal documents must be completely “mapped” into code for this to work.

12. Real-Time Forex (FX) Settlement

Traditional FX trades often take two days (T+2) to settle. Blockchain integrations allow banks to swap currencies nearly instantly (Payment-versus-Payment), significantly reducing the risk that one party defaults during the wait.

-

Best for: Reducing “Herstatt Risk” in global currency markets.

-

Why We Chose It:

-

It frees up billions in capital that banks currently hold in “reserve” for pending trades.

-

It allows for more precise pricing in volatile currency markets.

-

-

Things to consider: This requires the simultaneous availability of both currencies in tokenized form.

13. Distributed Ledger for Trade Finance

By digitising the “Bill of Lading” and other shipping documents on a blockchain, banks like Bank of America are reducing the fraud and delays associated with the physical mailing of paperwork for global shipping.

-

Best for: Importers and exporters who currently rely on paper documents.

-

Why We Chose It:

-

It reduces the time for a trade credit to be approved from weeks to days.

-

It provides an immutable history of the goods being shipped.

-

-

Things to consider: It requires all parties in the shipping chain (ports, customs, carriers) to be on the same network.

14. Tokenized Deposits for Retail Payments

Several regional banks are exploring “Deposit Tokens” as a way to allow customers to send money instantly to users at other banks, bypass the slow ACH (Automated Clearing House) network.

-

Best for: Instant peer-to-peer payments that don’t rely on third-party apps like Venmo.

-

Why We Chose It:

-

The money stays within the regulated banking system.

-

It is eligible for FDIC insurance, unlike most private stablecoins.

-

-

Things to consider: Adoption depends on widespread cooperation between competing banks.

15. Institutional-Grade Crypto Custody

Major custodians like BNY Mellon and State Street have integrated digital asset sub-custody into their core systems. This allows pension funds and insurance companies to hold Bitcoin and Ethereum alongside their traditional stocks and bonds.

-

Best for: Institutional investors who need institutional-grade security and reporting.

-

Why We Chose It:

-

It uses “MPC” (Multi-Party Computation) technology to protect private keys.

-

It provides a single consolidated report for all an investor’s assets.

-

-

Things to consider: Regulatory capital requirements for banks holding crypto remain high in early 2026.

An Overview Of Blockchain Integration And Future Banking Trends

The “quiet” nature of this integration is by design. Rather than launching consumer-facing apps, banks are focused on upgrading the “plumbing” of the financial system to save costs and increase speed.

Overview Comparison Table

Before these technologies go mainstream, it is helpful to see how they differ in their primary application.

| Initiative | Lead Institution | Blockchain Type | Focus Area |

| Kinexys (JPM Coin) | JPMorgan Chase | Private (Quorum) | Intraday Cash & Repo |

| Canton Network | Digital Asset / Consortium | Permissioned Public | Multi-Bank Interop |

| Project Agorá | BIS / Fed NY | Unified Ledger | Cross-Border Wholesale |

| BENJI Token | Franklin Templeton | Public (Stellar/Poly) | Tokenized MMF |

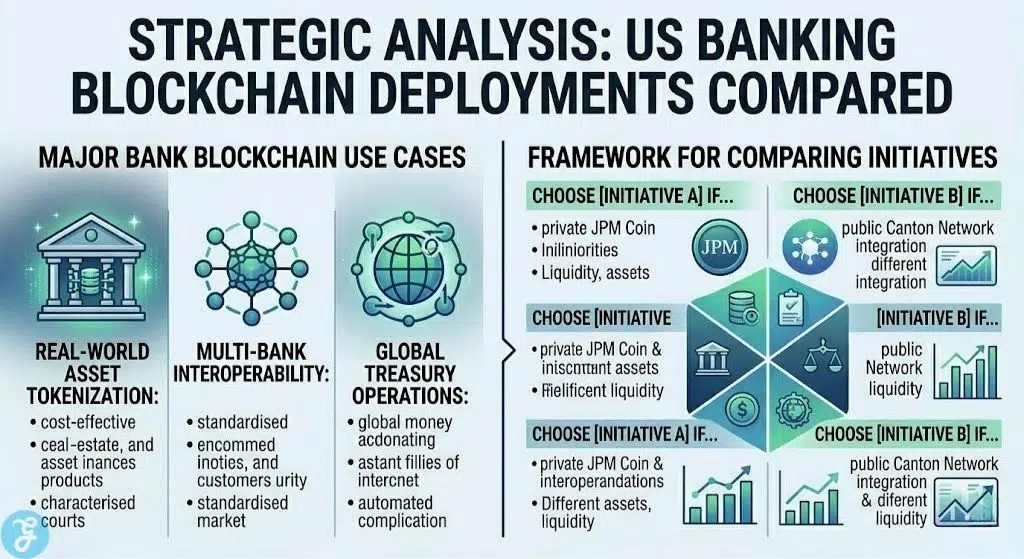

Our Top 3 Picks and Why?

Of the 15 developments, the Kinexys (JPM Coin), the Canton Network, and Project Agorá are the most transformative. These initiatives represent the most successful attempts to solve the three biggest problems in finance: 24/7 liquidity, cross-bank communication, and the inefficiency of global correspondent banking.

Buyer’s Guide: How to Choose the Right Blockchain-Enabled Bank by Yourself?

If you are a corporate treasurer or high-net-worth investor, your choice of banking partner now depends on their technical “stack” as much as their balance sheet.

The Selection Framework:

-

Network Access: Does the bank participate in a shared network like Canton or RLN, or are they a “silo”?

-

Asset Mobility: Can your collateral be tokenized and moved 24/7 to meet margin calls?

-

Settlement Speed: Does the bank offer T+0 (instant) settlement for FX and bond trades?

Decision Matrix (Table):

| Choose Bank A if… | Choose Bank B if… |

| You need high-volume, global USD transfers (JPMorgan). | You need to tokenize and distribute private debt (Citi/Solana). |

| You are an institution holding Bitcoin ETFs (BNY Mellon). | You are a corporate looking for automated smart contract payments. |

The Final Checklist: 5 Things to Ask Your Relationship Manager

-

Does the bank offer 24/7 internal ledger transfers for corporate accounts?

-

Is there a pathway for us to tokenize our existing cash or bond positions?

-

What blockchains (private or public) does the bank currently support for settlement?

-

Does the bank provide integrated reporting for both traditional and digital assets?

-

How is the bank participating in the Federal Reserve’s DLT pilot programmes?

The Invisible Foundation of 21st Century Finance

Blockchain in banking is no longer a “future” technology; it is the current operating system for the world’s most sophisticated trading desks. While most retail customers will never see a “wallet” or a “hash,” they will benefit from a faster, more stable, and more efficient global economy as these 15 integrations continue to scale.