The New Zealand crypto landscape is shifting from a period of “light-touch” oversight to a structured regulatory framework. For 2026, the focus has moved toward global transparency and defining how digital assets integrate with the local economy. Whether you are a casual trader in Auckland or a fintech developer in Wellington, understanding these shifts is the only way to ensure your portfolio stays on the right side of the law.

How We Selected Our 9 Crypto Regulations in New Zealand Facts

To ensure these “insider tips” provide real value, we analyzed the latest 2026 directives from the Financial Markets Authority (FMA) and Inland Revenue (IRD). We prioritized facts that affect your bottom line—specifically the launch of the OECD’s Crypto-Asset Reporting Framework (CARF) and the IRD’s increasingly sophisticated data-matching capabilities. We also looked at recent High Court precedents that define exactly how your digital property is protected under Kiwi law.

9 Insider Tips for Crypto Regulation in New Zealand

The regulatory environment in Aotearoa is becoming much more transparent. While this adds a layer of security, it also requires more diligence from every participant. Here are the nine essential updates for the current landscape.

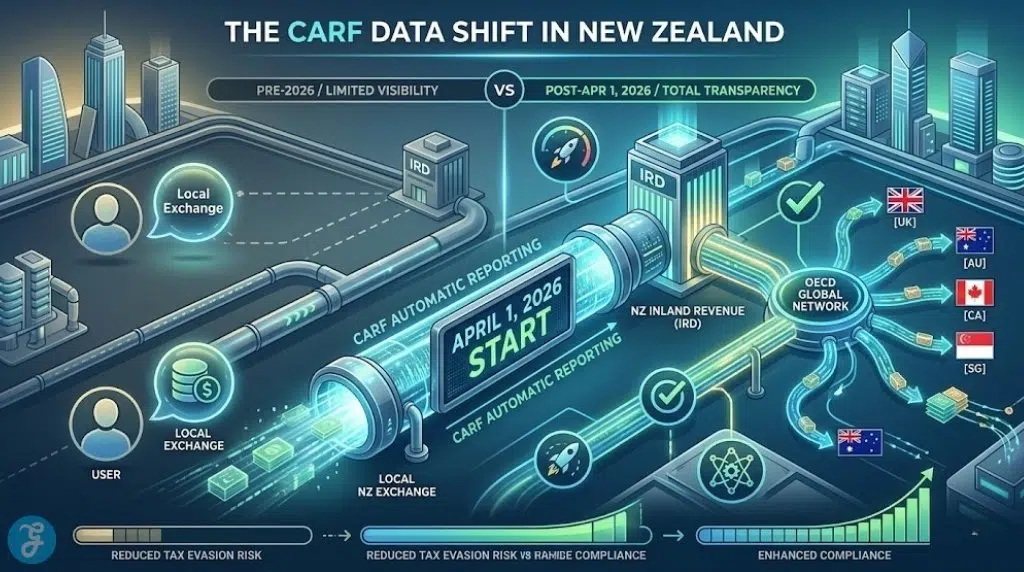

1. The CARF Reporting Era Begins April 1st

The most significant legislative shift in New Zealand’s crypto history is the official launch of the Crypto-Asset Reporting Framework (CARF). As of April 2026, all NZ-based exchanges and custodial service providers are legally required to report detailed transaction data directly to Inland Revenue. This is part of a global effort to eliminate tax evasion, meaning the “privacy” of local exchange accounts has essentially ended.

Key Detail: All transactions are now automatically shared with the IRD.

Why We Chose It:

-

It is a mandatory shift that affects every registered user in NZ.

-

It links Kiwi tax data with over 40 other participating nations.

-

It signals the end of “anonymous” trading within the local ecosystem.

Things to consider:

-

Ensure your exchange has your correct tax residency and IRD number on file to avoid account freezes.

2. NZDD Stablecoin Isn’t a “Financial Product”

In a landmark clarification, the FMA confirmed that the New Zealand dollar-pegged stablecoin (NZDD) is not classified as a “debt security.” Because it is a 1:1 representation of fiat and does not pay interest, it avoids the heavy disclosure requirements typically seen in traditional finance. This provides a “green light” for local businesses to use NZD-pegged tokens for payments without massive legal overhead.

Key Detail: No interest means less red tape for payment tokens.

Why We Chose It:

-

It lowers the barrier for local merchants to accept crypto.

-

It provides a clear legal distinction between “payment tools” and “investments.”

-

It fosters home-grown fintech innovation within a safe legal harbor.

Things to consider:

-

If a stablecoin starts offering “yield” or interest, it may instantly revert to being a regulated financial product.

3. The “Travel Rule” Is Now Fully Enforced

New Zealand’s version of the Travel Rule is in full effect for 2026. For any transfer of virtual assets over $1,000 NZD, the originating exchange must transmit the sender and beneficiary information to the receiving institution. This aligns NZ with global AML/CFT (Anti-Money Laundering) standards and is a core requirement for any business on the Financial Service Providers Register (FSPR).

Key Detail: Transfers over $1,000 are no longer private between exchanges.

Why We Chose It:

-

It is a mandatory compliance pillar for all local VASPs (Virtual Asset Service Providers).

-

It prevents NZ from being flagged as a high-risk jurisdiction for money laundering.

-

It standardizes how Kiwi exchanges interact with the global banking system.

Things to consider:

-

Direct “wallet-to-wallet” transfers (self-custody) are treated differently than exchange-to-exchange transfers.

4. Crypto Is Officially Personal Property for Tax

Following the precedent set by the Ruscoe v Cryptopia ruling, the IRD treats crypto-assets as a form of personal property. This means there is no “capital gains tax” in the traditional sense; instead, any profit made from selling or exchanging crypto is treated as regular income. If you bought with the intent to sell for a profit, your gains are taxed at your marginal rate (up to 39%).

Key Detail: Intention determines taxability.

Why We Chose It:

-

It is the settled legal foundation for all crypto activity in NZ.

-

It provides a familiar framework for anyone who has traded stocks or gold.

-

It clarifies that assets held on an exchange belong to the user, not the exchange.

Things to consider:

-

You can often claim losses on trades to offset other taxable income—keep meticulous records.

5. IRD Is Using “Data Matching” for Audits

Inland Revenue has significantly upgraded its technical capabilities. They now use advanced data-matching tools to cross-reference bank records with data from both local and offshore exchanges. If you have been moving large sums of money from an exchange to your NZ bank account without declaring it, the IRD likely already has a record of the discrepancy.

Key Detail: The IRD can see your “off-ramp” bank transfers.

Why We Chose It:

-

It warns users that “offshore” no longer means “hidden.”

-

It encourages proactive disclosure to avoid heavy penalties.

-

It highlights the increased enforcement budget for the 2026 tax year.

Things to consider:

-

Voluntary disclosure of past errors usually results in significantly lower penalties than an IRD-led audit.

6. Expanded FMA Sandbox for Fintech Pilots

The FMA has expanded its regulatory “sandbox,” allowing companies to test new crypto products in a controlled environment. This allows startups to operate with limited regulatory relief while the FMA observes the technology. It is designed to ensure that consumer protections are built into the product from day one rather than retrofitted later.

Key Detail: A safe space for NZ-based crypto startups to innovate.

Why We Chose It:

-

It shows a shift from a “cautious” approach to an “active support” model.

-

It provides a path for companies to gain FMA approval before a mass-market launch.

-

It helps regulators stay ahead of the technical curve.

Things to consider:

-

Participation requires absolute transparency and frequent reporting to the FMA.

7. DIA Is the Primary AML Supervisor

While the FMA handles “investments,” the Department of Internal Affairs (DIA) is the primary supervisor for Anti-Money Laundering for most crypto businesses. If you are running a crypto-related service in NZ, your primary compliance relationship is likely with the DIA. They ensure you have robust processes to detect and deter illicit financial flows.

Key Detail: The DIA watches the “business” of crypto, not just the assets.

Why We Chose It:

-

It clarifies which government agency has authority over your business operations.

-

It ensures the “on-ramps” and “off-ramps” to the NZ economy remain secure.

-

It standardizes the “KYC” (Know Your Customer) requirements across the industry.

Things to consider:

-

Small businesses or “crypto ATMs” are not exempt from DIA oversight.

8. A Multi-Year Roadmap for Stablecoin Legislation

The government is currently following a phased Stablecoin Roadmap. This year, the focus is on introducing specific legislation to define how “fiat-referenced” tokens fit within the national financial system. Expect to see new standards for 1:1 redemption rights and mandatory reserve audits being drafted throughout late 2026.

Key Detail: Regulation is becoming “bespoke” rather than “one-size-fits-all.”

Why We Chose It:

-

It provides a predictable timeline for institutional investors.

-

It aims to solve the “debanking” issue by making crypto businesses more “bankable.”

-

It focuses on protecting the NZ dollar’s stability.

Things to consider:

-

These rules will likely target issuers of stablecoins more than the individuals using them.

9. “Fair Dealing” Rules Protect You from Scam Ads

Even if a specific crypto asset isn’t a “financial product,” any business promoting crypto in New Zealand must comply with Fair Dealing laws. This prohibits misleading, deceptive, or unsubstantiated statements. If a local influencer or company promises “guaranteed returns,” the FMA has the power to issue stop orders and heavy fines instantly.

Key Detail: Consumer protection laws apply to crypto marketing.

Why We Chose It:

-

It is the primary shield against “pump and dump” schemes in the local market.

-

It holds local promoters accountable for the claims they make on social media.

-

It provides a clear legal path for recourse if you are misled by a local entity.

Things to consider:

-

These rules only apply to NZ-based entities; offshore scams remain difficult for the FMA to touch.

An Overview Of Crypto regulation in New Zealand

The Kiwi regulatory system is a “team effort” between several different government departments. Understanding this hierarchy is key to staying compliant.

Overview Comparison Table

| Agency | Primary Role | 2026 Focus Area |

| Inland Revenue (IRD) | Tax & Reporting | CARF Implementation (April 1st) |

| FMA | Consumer Protection | Fintech Sandbox & Guidelines |

| DIA | AML/CFT Supervision | VASP Compliance & Travel Rule |

| Reserve Bank (RBNZ) | Financial Stability | Stablecoin Systemic Risk |

Our Top 3 Picks and Why?

-

The CARF Reporting Era: This is the most important “insider” fact because it changes the fundamental nature of crypto privacy in NZ on April 1st.

-

Taxation as Personal Property: We chose this because the “Intention Test” is the number one thing the IRD looks for during an audit.

-

Fair Dealing Protections: This takes the third spot as it is the most effective tool for cleaning up the local market and protecting new investors.

Operating in New Zealand is about balancing the high degree of freedom we have with the high degree of transparency the government now requires.

-

The Residency Test: If you are an NZ tax resident, you must report global gains, regardless of where the exchange is located.

-

The Intention Test: Be honest about why you bought the asset. If it was for profit, it is taxable income.

-

The Local Platform Test: Using an NZ-based, FSPR-registered exchange gives you the strongest level of consumer protection under local law.

The Final Checklist:

-

Download a complete 2025/2026 transaction history before the April 1st CARF deadline.

-

Categorize your holdings by “intent” (long-term investment vs. personal use).

-

Confirm your chosen exchange is registered on the NZ Financial Service Providers Register.

-

Consult a tax professional who specializes in the specific Crypto regulation in New Zealand framework.

Securing Your Digital Future in Aotearoa

New Zealand is building a framework that moves crypto from the “fringes” into a regulated, transparent financial sector. By staying ahead of the CARF reporting rules and understanding your tax obligations, you can build a portfolio that is both profitable and legally secure. The “insider” secret for 2026 is simple: treat your crypto as serious property, keep perfect records, and use the local protections that are now in place.