A startup funding guide should not make fundraising sound cleaner than it is. The neat version says you start with an idea, raise a little pre-seed money, build traction, raise seed, pitch VCs, negotiate a term sheet, and keep going until the company either exits or becomes profitable. That version is tidy enough for a diagram. It is also incomplete enough to get founders into trouble.

Real funding decisions are messier. You might take a small angel check before the company is incorporated properly. You might stack SAFEs without modeling the next round. You might win a grant that helps the technology but slows the commercial roadmap. You might run a crowdfunding campaign that validates demand but creates fulfillment pressure. You might chase a higher valuation and sign a term sheet that makes the next two years harder.

Funding is not just money. It is timing, control, dilution, legal structure, investor expectations, and the kind of company you are agreeing to build.

That is why founders need to understand the full funding system before raising startup capital, not just the next check. The wrong capital can buy time and still damage the company. The right capital should help you prove the next milestone with fewer hidden costs.

This guide connects the major startup funding paths founders face: early funding instruments, venture capital, pitch decks, crowdfunding, grants, term sheets, and cap table management. Each one looks separate on paper. In practice, they all collide on the same question: what are you giving up to get the money, and will that trade still make sense when the company hits pressure?

Startup Funding Guide: Start With the Type of Company You Are Building

The first funding decision is not “Who will give us money?”

It is “What kind of company are we building?”

A venture-scale software company, a hardware startup, a biotech company, a local services business, a climate technology company, and a consumer product brand do not need the same capital path. They have different timelines, margins, risks, proof points, and expectations.

Venture capital works best when the company can become very large and grow fast enough to justify the risk. Grants and non-dilutive programs may fit research-heavy or public-benefit technologies. Crowdfunding can work for products people understand quickly and want to support before they exist at scale. Customer-funded pilots may beat investor money when the market is willing to pay early. Bootstrapping may be healthier when control, profitability, or focus matters more than speed.

The funding source should match the company’s actual risk.

If the risk is technical, money should help prove the technology works. If the risk is demand, money should help prove people will pay. If the risk is distribution, money should help test customer acquisition. If the risk is manufacturing, money should help validate cost, supply chain, quality, and delivery.

Founders get lost when they raise money for vague movement. “Growth” is not enough. “Hiring” is not enough. “Runway” is not enough. The money needs to buy a specific step toward a more fundable or more durable company.

Before choosing any funding path, answer these questions plainly:

- What milestone does this money unlock?

- What proof will exist after the money is spent?

- Who will care about that proof?

- What does this capital cost in equity, control, time, or obligations?

- Does this funding path make the next funding path easier or harder?

A startup funding guide is only useful if it forces that discipline. Otherwise, it becomes a menu of money sources without a strategy.

Funding Rounds Explained Without the Theater

Funding rounds are supposed to reflect progress, not just ambition.

Pre-seed usually funds early company formation, prototype work, customer discovery, first hires, and initial proof that the problem is real. At this stage, investors are often betting on the founders, the market, and early signals more than polished financial performance.

Seed funding should move the company from early promise to clearer proof. That might mean revenue, retention, pilots, product usage, manufacturing validation, regulatory progress, or a repeatable wedge into the market.

Series A is where the questions get sharper. The company needs more than a good story. It needs evidence that the product solves a real problem, customers behave in a repeatable way, and the business can scale with more capital.

Later rounds depend heavily on growth quality, margins, sales efficiency, retention, market size, team maturity, and whether the company can keep expanding without burning money blindly.

The names of funding rounds matter less than the proof behind them.

A “seed” company with real revenue, strong retention, and a clear sales motion may be much stronger than a “Series A” company with a bigger deck and weak repeatability. A pre-seed hardware startup with a serious prototype and paid pilot interest may be more credible than a software startup with thousands of sign-ups and no one paying.

Founders should not raise because the market says it is time. They should raise when the company can make a clear argument for why more capital creates a stronger business.

This matters when talking to startup investors. Investors do not fund stages in the abstract. They fund risk reduction. The round needs to show what has been learned, what remains uncertain, and why this new money is the right amount to attack the next risk.

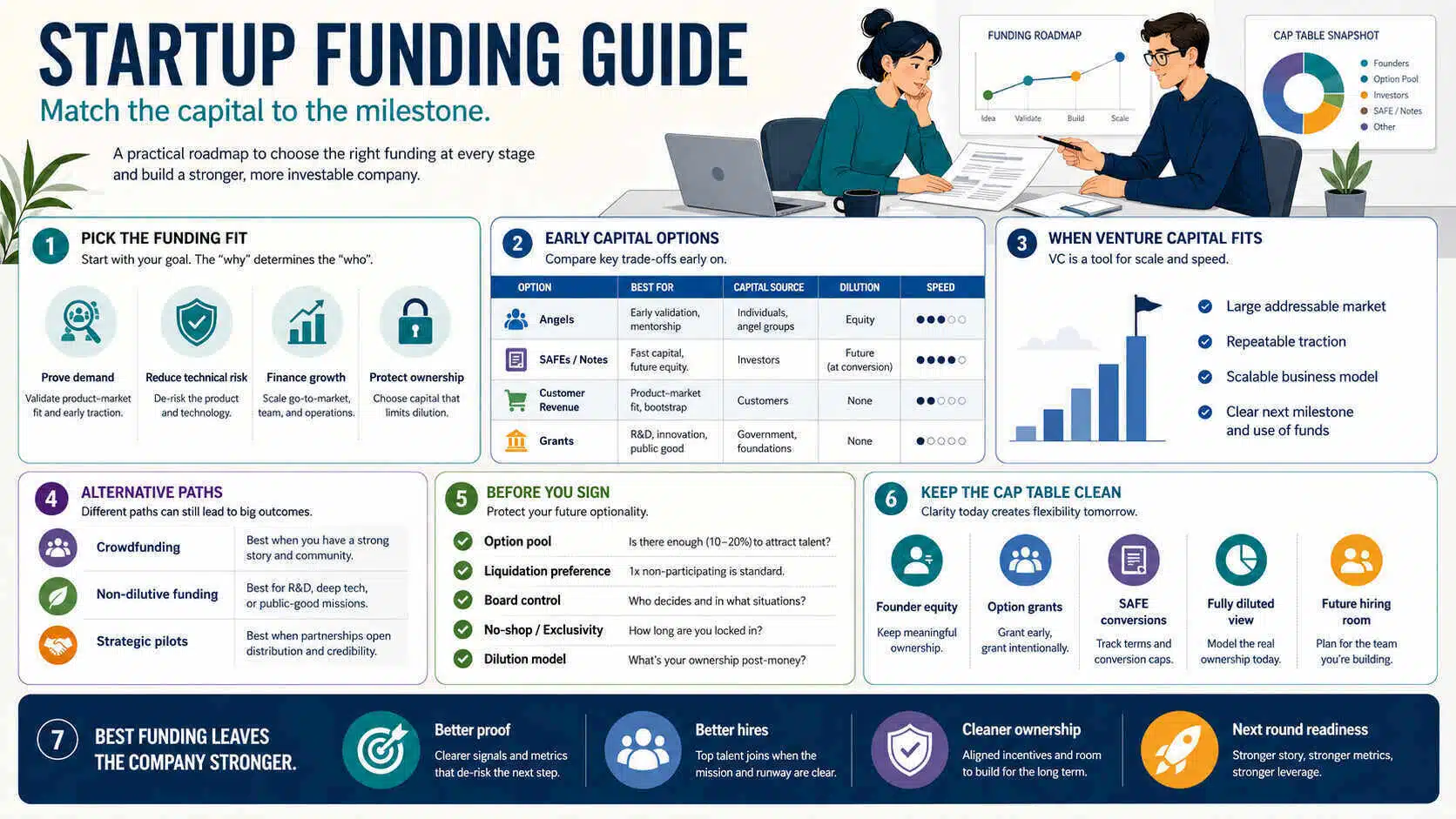

Choose Early Checks Carefully: Notes, SAFEs, and Dilution

Early money often arrives through convertible notes or SAFEs because priced equity rounds can be slower and more expensive to close.

That speed is useful. It can also make founders careless.

Convertible notes are debt instruments that convert into equity later, usually during a future priced round. They may include interest, maturity dates, valuation caps, and discounts. A note can be simple enough at first, but it still creates obligations. Debt language matters. Maturity dates matter. Interest and conversion mechanics matter.

SAFEs are not debt. They are agreements that convert into equity later under defined conditions. They can move quickly and reduce friction, which is why many early-stage startups use them. But SAFEs are not free from dilution. They simply delay the moment when the dilution becomes visible.

The biggest founder mistake is stacking early checks without modeling the priced round.

A $100,000 SAFE here, a $250,000 SAFE there, a few angel checks on different caps, then a bridge SAFE before seed. Each one feels manageable when signed alone. Together, they can consume far more ownership than the founder expected once the company raises a priced round.

Post-money SAFEs make ownership easier to understand because the investor’s ownership is expressed more directly. That clarity helps, but it can also expose how quickly several SAFEs add up. A founder who treats each small check as harmless may discover that a meaningful share of the company has already been sold before the seed round lead arrives.

Before signing another note or SAFE, model:

- Founder ownership now

- Founder ownership after conversion

- Option pool needs

- Incoming investor ownership in the priced round

- Dilution under different round sizes and valuations

- What happens if the next round takes longer than planned

Early instruments should help the company reach the next real milestone. They should not create a cap table puzzle that makes the next investor hesitate.

Map the VC Fundraising Process Before You Start

The venture capital process is not a pile of investor meetings. It is a sales process with legal, financial, and trust layers attached.

Founders who treat it casually lose momentum. They start outreach before the deck is ready. They pitch investors who do not fund their stage. They confuse polite interest with real movement. They wait until diligence to clean documents. They begin when runway is already thin.

A better VC process starts before the first email.

You need to know how much you are raising, what milestone the money buys, which investors fit your stage and sector, what proof you already have, and what objections will come up first.

The investor list should be built around fit, not fame. A fund that does not invest at your stage is not a useful target. A fund with check sizes far above or below your raise may not be helpful. A firm with direct portfolio conflicts may pass no matter how strong the company is.

Once outreach begins, track it like a pipeline. Warm intros, cold outreach, first calls, partner meetings, diligence requests, reference calls, and term sheet conversations all need follow-up. Founders who rely on memory lose control of the process.

The strongest VC processes create momentum. That does not mean fake scarcity or performative urgency. It means investors know the round is organized, the materials are clean, the story is consistent, and the founder can move from interest to decision without drifting for months.

VC fundraising is hard enough when the company is strong. Do not make it harder with sloppy sequencing.

Build a Fundraising Deck Investors Can Repeat

A pitch deck does not need to explain everything. It needs to make the company easy to understand and hard to dismiss.

The best fundraising deck gives an investor enough clarity to repeat the company to another partner after one read. That is the test. If the investor cannot say who the customer is, what pain exists, why now matters, what the product changes, and what proof exists, the deck is not doing its job.

Founders often build decks from the inside out. They include too many features, too much product history, too many market claims, and too many slides that require live narration. The investor does not read with founder patience. They skim, judge, pause, and decide whether the next meeting deserves time.

The first slides need to make the business obvious. Not small. Not simplistic. Obvious.

If you sell SOC 2 automation to mid-market SaaS teams, say that. If you help logistics teams cut empty truck miles, say that. If you build workflow tools for dental clinic billing teams, say that. Do not hide the company behind “AI-powered transformation” language that could belong to any startup.

The traction slide needs to prove the right thing. Waitlists do not prove payment. Downloads do not prove retention. Revenue with weak repeat usage may not prove durability. A good deck chooses metrics that defend the actual story: net retention, sequential month-on-month growth, pipeline quality, cohort behavior, paid pilots, transaction volume, repeat usage, or conversion rates.

The go-to-market slide deserves more honesty than most founders give it. “Content, partnerships, and paid ads” is not a strategy. Investors want to know who buys, how you reach them, what sales motion fits the contract value, and what has already shown early promise.

Deck examples from famous startups can help founders study clarity, but they should not become costumes. A consumer marketplace deck from another era will not automatically work for a technical B2B company today. Learn the judgment, not the slide style.

A fundraising deck is not decoration. It is the first pressure test of whether the founder can explain the business clearly.

Use Crowdfunding Only When the Crowd Already Cares

Crowdfunding can be powerful, but it is not a shortcut around demand.

Reward crowdfunding works best when the product is tangible, easy to understand, visually clear, and close enough to delivery that backers can trust the promise. A startup Kickstarter campaign can work for hardware products, games, design goods, creative tools, consumer products, and other offers that people can grasp quickly.

Equity crowdfunding is different. It asks the crowd to invest in the company, not just buy or support a product. That brings securities rules, disclosures, platform requirements, investor communication, and future cap table considerations.

Both models demand preparation.

The mistake is thinking the platform brings the audience. It usually does not. A platform can amplify momentum, but the early crowd needs to exist before launch. That means email lists, community, press outreach, creator partnerships, customer demand, product proof, or existing fans who are ready to act.

Reward crowdfunding also creates fulfillment risk. Backers expect the promised product. If manufacturing costs rise, shipping gets messy, or stretch goals destroy margins, the campaign can become a public operational problem.

Equity crowdfunding creates different pressure. It may turn customers and community members into investors, which can be useful for mission-driven or consumer-facing companies. But it also creates disclosure obligations and expectations from many small investors.

Crowdfunding works when the crowd already has a reason to care. It fails when the founder launches into silence and hopes the internet will provide demand.

Add Non Dilutive Capital Without Chasing Free Money

Grants and non-dilutive funding can be excellent when they fit the company’s real risk.

They can help research-heavy startups, climate companies, biotech teams, hardware startups, defense technologies, deep tech tools, and other businesses that need to prove technical or public-benefit milestones before traditional financing becomes easier.

But “non-dilutive” does not mean free in the practical sense.

Startup grants, SBIR/STTR awards, tax credits, government contracts, customer-funded pilots, corporate innovation programs, and prize competitions all come with tradeoffs. They may require applications, reporting, restrictions, reimbursement timing, compliance work, or roadmap alignment with the funder’s goals.

A grant that helps prove a prototype survives real operating conditions can be extremely valuable. A grant hunt that pulls the founder away from customers for three months can become expensive distraction.

The right test is simple: does this money unlock a milestone that customers, investors, regulators, or partners will care about?

If yes, non-dilutive funding can strengthen the company before the next raise. If no, the company may be chasing funding because it exists.

Customer-funded pilots deserve special attention. They are not always labeled as non-dilutive funding, but they can be among the cleanest forms of early capital. A customer pays because the problem matters, and the company gets money plus market validation. The tradeoff is scope control. One customer should not quietly turn the product into a custom internal tool.

Use non-dilutive capital with a milestone strategy. Do not turn the company into a grant-writing machine.

Negotiate the Term Sheet Beyond Valuation

The term sheet is where the funding round becomes a set of consequences.

Valuation matters, but it is only one part of the deal. The option pool, liquidation preference, board structure, protective provisions, pro rata rights, anti-dilution language, no-shop length, side letters, and legal fee caps can all change what the financing really means.

A higher valuation with aggressive terms can be worse than a lower valuation with cleaner terms. Founders should model the deal before reacting to the headline number.

Option pool treatment is one of the first pressure points. If the pool is increased before the financing, existing shareholders absorb the dilution. If it is increased after, the new investor shares in it. That difference changes the effective price of the round.

Liquidation preference affects exit outcomes. A clean 1x non-participating preference is very different from participating preferred or a multiple liquidation preference. The difference may not matter in a huge exit, but it can matter a lot in a middle outcome where the company sells for less than the dream case.

Board control and protective provisions shape how the company operates after the close. Investors deserve protection on major company actions. They should not need approval over ordinary execution. Watch thresholds carefully. A consent right over major debt is different from one that slows normal working capital decisions.

The no-shop clause also deserves attention. A short exclusivity period may be reasonable when the investor is ready to close. A long no-shop with unresolved diligence can trap the company if the deal drags or falls apart.

Term sheet negotiation is not about being difficult. It is about understanding which terms change ownership, control, future financing, and exit outcomes.

Keep the Cap Table Clean Before Every Round

Cap table management is not finance housekeeping. It is ownership control.

A messy cap table makes fundraising harder, hiring harder, diligence slower, and founder decision-making weaker. If the spreadsheet does not match the legal documents, the spreadsheet is not truth. It is a liability.

The cap table needs to reflect founder shares, investor securities, option grants, SAFEs, notes, warrants, advisor equity, vesting schedules, repurchases, exercises, and fully diluted ownership. Every entry should tie back to documents and approvals.

Founder equity should be clean early. Vesting, repurchase rights, IP assignments, and clear ownership records protect the company if a founder leaves. Skipping those pieces because everyone trusts each other is how dead equity problems begin.

Equity tracking also matters for employees and advisors. Vague promises become disputes. If the company intends to issue equity, document it, approve it, and track it. If it does not intend to issue equity, do not imply ownership casually.

Cap table software can help once the company has multiple security types, options, SAFEs, notes, or institutional investors. But software does not fix bad inputs. It only supports discipline. The company still needs clean documents, current approvals, and accurate modeling.

Before every round, founders should know:

- Current founder ownership

- Fully diluted ownership

- Issued and available option pool

- SAFE and note conversion impact

- Advisor and employee grants

- Side letters or special rights

- What the proposed financing does to ownership

A clean cap table makes the company easier to trust. A messy one makes every investor wonder what else the founder has not tracked.

How to Match Funding Sources to the Right Milestone

Founders often compare funding sources by availability. That is the wrong filter.

Compare them by milestone.

If the company needs to prove technical feasibility, grants, SBIR/STTR, research partnerships, or strategic pilots may fit. If the company needs to prove customer demand, paid pilots, pre-orders, crowdfunding, or founder-led sales may be stronger. If the company needs to scale a repeatable growth engine, venture capital may make more sense. If the company needs flexibility without a venture-scale outcome, revenue, debt, or smaller strategic checks may be healthier.

The right funding source should make the next proof point more credible.

A pre-seed software company may need angel checks and customer validation. A hardware startup may need non-dilutive funding and prototype validation before taking venture money. A consumer product brand may use crowdfunding to test demand and finance production. A deep tech company may combine grants, customer pilots, and venture capital over time.

The danger is mixing funding sources without understanding their combined consequences.

A company might stack SAFEs, run equity crowdfunding, promise advisor equity, win a grant with roadmap restrictions, and then try to raise a clean VC round. That can work if managed carefully. It can also create a cap table and obligation mess.

Every funding choice should answer one question: does this make the next serious company milestone easier to reach?

If not, it may be capital with a hidden cost.

What Startup Investors Actually Want to See

Startup investors are not all the same, but most serious investors are looking for the same broad pattern: a real problem, a strong team, a large enough market, early proof, and a path to a much bigger company.

That proof changes by stage.

At pre-seed, a strong founder-market fit, serious customer discovery, early usage, technical insight, or a sharp wedge may matter more than revenue. At seed, investors expect clearer evidence: paid pilots, early revenue, retention, pipeline quality, product usage, or a customer segment that behaves consistently. At Series A, the bar rises again. Investors look for repeatability, growth quality, retention, sales efficiency, and a business model that can absorb more capital productively.

The mistake is treating investor conversations as persuasion only.

A good funding process is not just about making the company sound attractive. It is about showing what risk has already been reduced and what risk the next round will attack. The best founders do not hide weaknesses. They explain them clearly, show what they have learned, and connect the raise to a specific plan.

Investors can handle risk. They are paid to take risk. What they do not like is confusion, inconsistency, or founder fog.

If the deck says one thing, the model says another, and the cap table says a third, trust drops quickly. If the founder cannot explain how the money becomes progress, the conversation weakens. If the valuation assumes a company that does not match the traction, investors pull back.

Funding is a confidence game, but not in the fake sense. It is confidence built through clarity.

The Founder’s Funding Stack Should Be Deliberate

Most companies do not use just one funding source forever.

A strong capital path may combine founder savings, customer revenue, small angel checks, SAFEs, grants, crowdfunding, tax credits, venture rounds, and later debt or strategic capital. That is not automatically messy. It becomes messy when the founder does not understand how the pieces interact.

A good funding stack has a sequence.

Early money proves the first risk. The next money proves the next risk. Each step makes the company more credible, not just more funded.

For example, a hardware founder might start with prototype grants, run paid pilots, use a small SAFE round to finance engineering, then raise seed once manufacturing and demand are clearer. A software founder might start with angel checks, prove retention with early customers, raise seed, then use a priced round to build a repeatable go-to-market engine. A consumer product founder might validate demand through reward crowdfunding before deciding whether equity capital makes sense.

The wrong funding stack creates contradiction.

The company raises venture money but does not have a venture-scale plan. It takes grants that pull the roadmap away from customers. It raises crowdfunding money without a delivery plan. It gives away too many pro rata rights. It issues options without tracking them. It signs a term sheet without modeling the cap table.

Capital should compound. It should not create cleanup work.

The Practical Funding Plan Before You Raise

Before raising money, founders should write a plain funding plan.

Not a beautiful investor-facing plan. A working plan.

It should answer:

- What stage is the company actually at?

- What proof exists today?

- What proof is missing?

- How much money is needed to reach the next milestone?

- Which funding source matches that milestone?

- What does that funding cost in dilution, control, time, or obligations?

- What does the cap table look like after the raise?

- What happens if the milestone takes twice as long?

- What happens if the next round is smaller or lower priced than expected?

This plan does not need to be perfect. It needs to force the founder to stop treating capital as abstract progress.

Money is only useful if it helps the company become stronger. A big round with weak discipline can hide problems. A smaller amount of well-matched capital can force focus and produce cleaner proof.

Founders should also decide what they are not willing to do. Not every investor is worth taking. Not every grant is worth applying for. Not every crowdfunding campaign should launch. Not every term sheet should be signed. Not every valuation is worth the hidden terms attached to it.

A startup funding guide can explain the options, but the founder still has to choose the path that fits the company in front of them.

The Funding Path Should Leave the Company Stronger

Startup funding is not a scoreboard.

A company is not better because it raised more money, announced a bigger valuation, or attracted a famous investor. It is better when the funding helps the team build something customers want, prove a sharper milestone, hire the right people, and keep enough ownership and control to stay motivated.

The danger is that fundraising can feel like success before the business has earned it. A term sheet feels like victory. A crowdfunding campaign feels like traction. A grant feels like validation. A SAFE feels harmless because the dilution has not hit yet. A clean cap table feels boring until it saves the next round from delays.

Funding choices age. Some age well. Others become expensive later.

Use this startup funding guide as a pressure test, not a checklist. Match the capital to the milestone. Understand the instrument before signing it. Build the deck so investors can repeat the story. Choose crowdfunding only when the crowd has a reason to care. Use non-dilutive money when it de-risks the company. Negotiate terms beyond valuation. Keep the cap table clean before the next round makes cleanup harder.

The best funding path does not just get money into the bank.

It leaves the company easier to build after the money arrives.