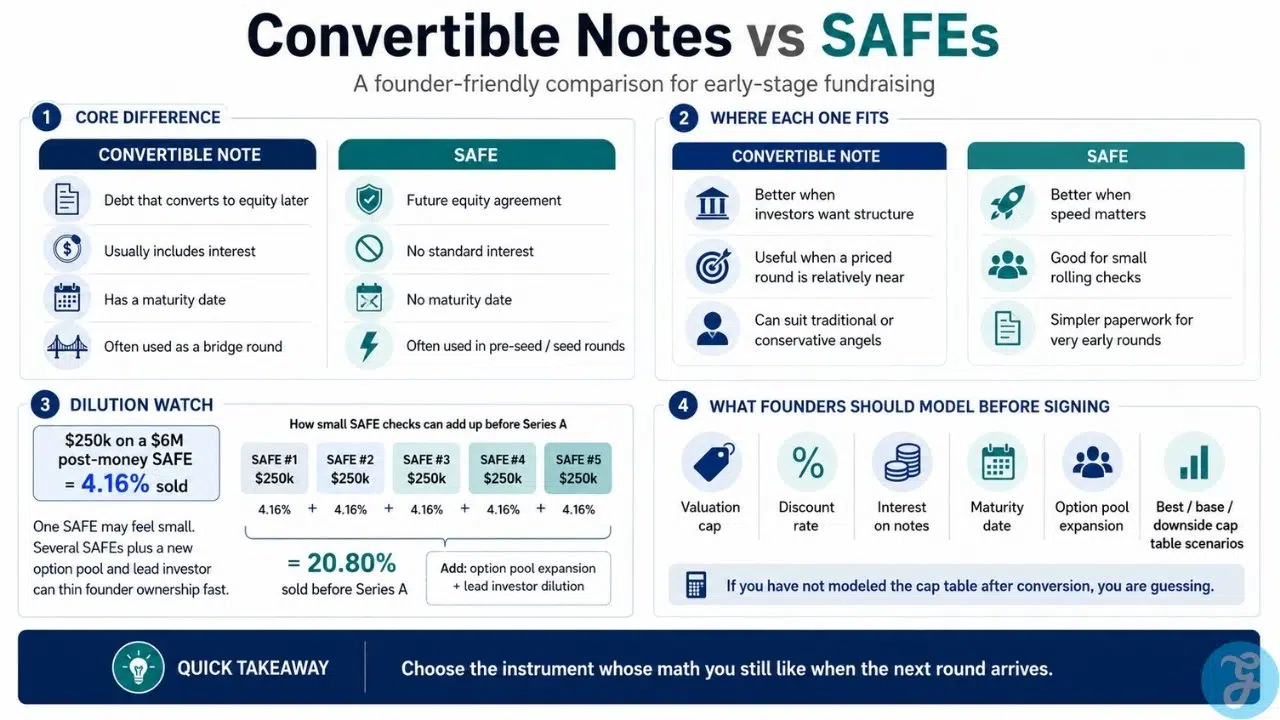

Convertible notes vs SAFEs is one of the first serious fundraising choices a startup founder has to make. What looks like routine legal paperwork at the beginning can quickly affect dilution, investor leverage, future round dynamics, and how clean the cap table looks before the company ever reaches a priced round.

Both options are early stage funding instruments built for the same basic problem: the startup needs cash now, but the founder and investors are not ready to agree on a fixed company valuation. A priced equity round takes time, negotiation, legal fees, and more structure than many early startups can handle.

Convertible notes and SAFEs reduce that friction by letting a startup take in capital now while delaying the valuation conversation until a future financing round. The important difference is that they do not treat that capital the same way, which is why understanding the mechanics of a SAFE vs convertible note structure matters before the conversion event arrives.

The Debt Reality of Convertible Notes

A convertible note is a short-term debt instrument, which means the investor is legally lending money to the company. Instead of receiving shares right away, the investor’s principal amount, and usually accrued interest, converts into preferred stock when the company raises its next priced equity round.

That debt structure feels familiar to many traditional angel investors and institutional funds because it gives them more downside protection. They invest before the company has been fully priced, then receive better economics later through a valuation cap, a discount rate, or both.

A valuation cap sets the highest company valuation used to calculate the investor’s conversion price, while a discount lets the investor buy into the next round at a lower price than new investors. Together, these terms reward early backers for taking risk before the market has assigned a clearer value to the company.

The part founders sometimes underestimate is the maturity date. Many convertible notes mature after 12 to 24 months, and if the company has not raised a qualified financing by then, the note does not disappear. The company may need to renegotiate an extension, repay the note, or give investors more leverage at a difficult moment.

That does not make convertible notes a bad option, but it does mean founders should treat them like real obligations with real consequences.

The SAFE Route: Speed Over Deadlines

A SAFE, or Simple Agreement for Future Equity, was popularized by Y Combinator to make early startup financing faster and lighter. Unlike a convertible note, a SAFE is usually not treated as debt; it is a contract that gives the investor the right to receive equity later.

That structure allows a standard SAFE to avoid maturity dates, repayment obligations, and interest rates. For a young company, this can be a major relief because there is no loan deadline sitting on the balance sheet while the team is still trying to prove the business.

Founders often like SAFEs because they are standardized, familiar in startup circles, and easy to close on a rolling basis. A founder can agree on the main economic terms, usually a valuation cap or a discount, and move forward without turning every small check into a full legal project.

The problem is that this ease can hide the future cost. A founder may sign four, five, or six SAFEs over several months and feel like the round is going well because there is no immediate pressure. The harder moment usually comes later during Series A diligence, when everything gets entered into a spreadsheet and the founder realizes a meaningful chunk of the company has already been promised away.

Demystifying the Post-Money SAFE

The dilution risk becomes much more visible with a post-money SAFE. YC introduced this framework to give investors and founders clearer ownership math, so instead of leaving everyone guessing about the investor’s future stake, the post-money structure shows what the investor is effectively buying.

Let’s say you take a $250,000 check on a $6 million post-money cap. Right then and there, you have sold exactly 4.16% of the company to that investor before the new money in the priced round comes in. That kind of clarity can be useful, especially when several checks close at different times.

The problem starts when multiple SAFEs stack up. If one post-money SAFE represents 5%, another represents 4%, and another represents 3%, the company has already committed about 12% before the lead Series A investor negotiates anything.

Then the new investor wants ownership, the employee option pool may need to expand, and earlier investors may have participation rights. By the time all of that is included, the founder’s remaining stake can look much thinner than expected.

A post-money SAFE is not inherently dangerous, but it becomes unforgiving when founders do not track cumulative dilution after each signature.

Caps and Discounts: The Real Math

Whether you use convertible notes vs SAFEs, valuation caps and discounts drive the real economics of the deal. A valuation cap is not a placeholder; it sets an economic ceiling for the investor’s conversion price.

Picture a founder who raises a small pre-seed check on a $5 million cap because the terms feel quick and painless. A year later, the company raises a priced round at a much higher valuation. That early investor does not convert at the new round’s higher price. They convert using the lower capped price, which means they receive more shares for taking the earlier risk.

That may be fair. It is also why founders should not shrug at the cap just because it sits inside a short document.

A discount works differently. If the next round price is $1.00 per share and the investor has a 20% discount, that investor converts at $0.80 per share. That gives the early investor a pricing advantage over new investors because they backed the company earlier.

Some instruments include both a cap and a discount, and in many cases, the investor receives whichever method produces the better result. Founders should not treat these as small terms buried in the paperwork because they decide how much ownership changes hands when the instrument converts.

How to Choose the Right Tool

Choosing between a SAFE vs convertible note should not come down to what sounds popular in founder circles. The right choice depends on the round, the investors, the timeline, and the amount of structure both sides need.

| Scenario | Better Fit | Why It Works |

|---|---|---|

| Very early pre-seed or seed round | SAFE | Keeps legal costs lower, closes faster, and avoids debt pressure |

| Bridge to a near-term priced round | Convertible note | Works as short-term capital with a clearer timeline |

| Traditional or conservative angels | Convertible note | Gives investors interest, maturity terms, and more legal protection |

| Small rolling checks from several backers | SAFE | Reduces admin work and avoids tracking interest across different closing dates |

| Founder wants speed above structure | SAFE | Standard terms can move the round forward quickly |

| Investor wants more downside protection | Convertible note | Debt terms give the investor more leverage if things go sideways |

Neither instrument is automatically founder-friendly. A poorly structured SAFE can hurt worse than a fair note, while a clean note can work well if the company has a clear path to its next round.

Do not choose the document with the friendlier name. Choose the one whose math still makes sense when the next round gets expensive.

The Pitfall of Deferred Dilution

The biggest mistake founders make with these instruments is treating them as “not real dilution yet,” when the dilution is real but delayed.

A convertible note can grow over time because interest accrues before conversion. A SAFE can quietly build future equity obligations even without an interest clock ticking. A post-money SAFE can make the ownership easier to calculate, but it does not make the dilution painless.

Before signing anything, founders should build a basic pro forma cap table to see the actual impact. It does not need to impress anyone. It needs to show the ugly version of the future too, otherwise you are just lying to yourself.

At minimum, model these three outcomes:

- A strong priced round at a high valuation

- A realistic middle-case round

- A weaker round where the valuation comes in lower than expected

The model should include every SAFE, every convertible note, accrued interest, valuation caps, discounts, option pool expansion, and the new investor’s expected ownership target.

If a founder cannot look at that model and explain how much of the company they will own after conversion, they are not ready to sign the paperwork. The point is not to slow the round down for no reason. The point is to avoid celebrating fast money now and regretting the ownership math later.

The Bottom Line Before You Sign

Convertible notes vs SAFEs is not just a paperwork decision. It decides how much dilution you accept, how much pressure you carry, and how much flexibility you keep before the next round.

A SAFE may look easier because there is no maturity date or interest clock, but that does not make it harmless. A convertible note may look more formal because it is debt, but that structure can be useful when everyone knows a priced round is close. The mistake is treating either document as a shortcut instead of a financing decision with real cap table consequences.

Do not pick the instrument because another founder used it, an investor prefers it, or the template looks simple. Pick it because you understand what it does to the cap table after conversion.

The right instrument should help you close the current round without making the next one feel like a nasty surprise.