The venture capital process looks clean from the outside. You build a company, pitch investors, get a term sheet, pass due diligence, and close the round. Nice story. Very neat. Mostly incomplete.

In real life, VC fundraising feels more like running a sales process while your AWS bill is spiking, your lead engineer just quit, and your biggest customer is threatening to churn. You’re selling the future, defending the present, explaining the past, and trying not to sound desperate while runway keeps shrinking in the background.

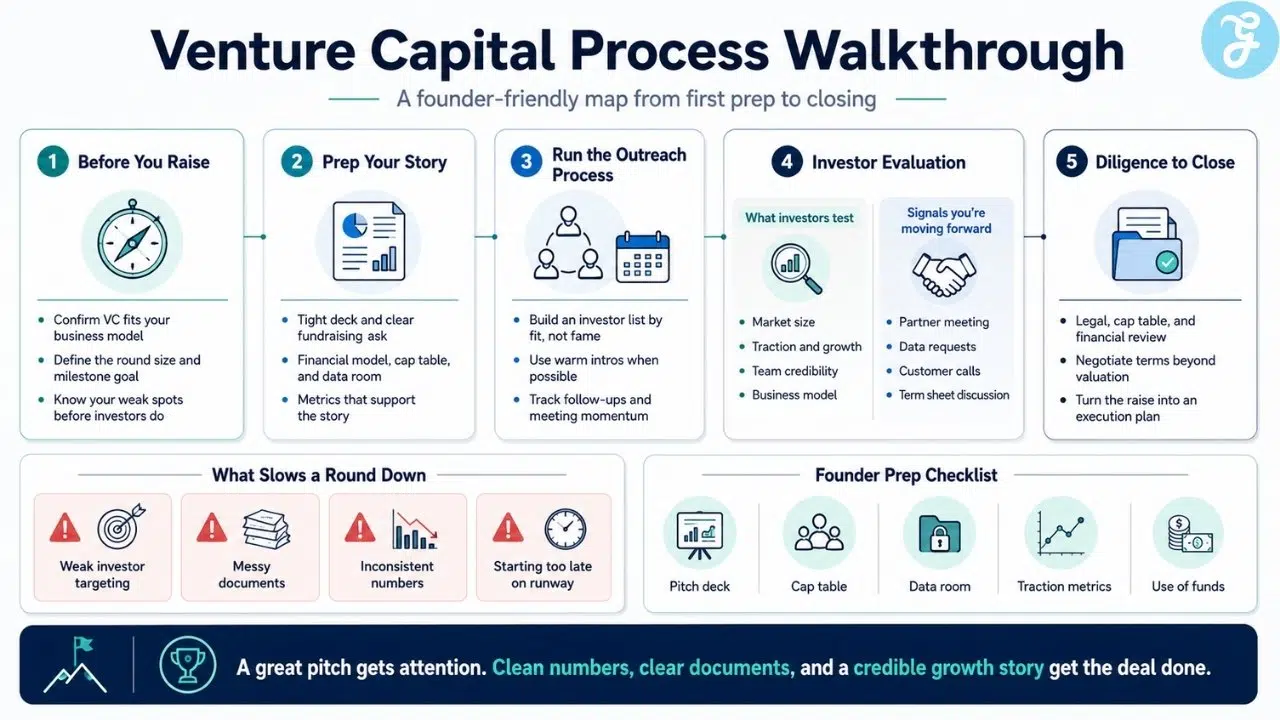

Raising VC money doesn’t have to become chaos, but you need to understand the order of the process before you start taking meetings. Venture capital isn’t just about convincing one investor to like your company. It’s about creating enough confidence, timing, competition, and proof that an investor feels comfortable wiring money into a high-risk business.

Some stages are obvious, like pitching and term sheet negotiation. Others are easier to underestimate, like investor targeting, data room preparation, partner alignment, and VC due diligence. Skip those, and the round can drag for months while you keep wondering why “great meeting” never turns into a check.

This walkthrough breaks down how the venture capital process usually works, where founders lose momentum, and what to prepare before the first serious investor conversation.

What the Venture Capital Process Actually Means

The venture capital process is the path a startup follows to raise money from professional investors who fund high-growth companies in exchange for equity.

That sounds simple, but the process isn’t just a pitch deck followed by a yes or no. A VC firm is usually evaluating several things at once: the market, the team, the product, traction, financials, ownership structure, risks, exit potential, and whether the investment fits the fund’s own strategy.

You may think the question is, “Do they like my startup?” The investor is asking something colder: “Can this company become large enough to return meaningful money to our fund?”

A solid business isn’t always a venture-backable business. A profitable services company, a niche SaaS tool, or a steady local marketplace may be impressive, but it may not match the return profile a venture fund needs. VC money is built for companies that can grow very large, usually fast, with a market big enough to justify the risk.

Before you enter the process, be honest about whether venture capital fits the company. If the business needs patient growth, control, or early profitability more than aggressive scaling, another funding path may be healthier.

Stage 1: Decide Whether VC Funding Fits the Company

The first step in VC fundraising happens before outreach. You need to decide whether venture capital is the right kind of money.

VC money can help you hire faster, build faster, expand into a larger market, and take risks the business couldn’t afford from revenue alone. It can also raise expectations immediately. Once venture investors come in, the company is usually expected to chase a much larger outcome.

When you raise VC money, you’re accepting more than capital. You’re accepting a growth path, a board relationship, reporting expectations, dilution, and pressure to eventually produce a venture-scale exit. That may be exactly right for a company attacking a large market with a product that can scale quickly. It may be wrong for a company that would be healthier growing steadily with customer revenue.

Use a simple test. If the company can plausibly become large enough to make a venture fund’s ownership stake matter, VC may fit. If the best realistic outcome is a strong but moderate business, think carefully before selling equity for money that expects outsized returns.

Taking VC money isn’t inherently good or bad. The real danger is cashing the check without understanding the hyper-growth treadmill it puts you on.

Stage 2: Build a Fundraising Strategy Before You Pitch

Many founders start with a list of famous investors. That’s backwards.

Start with the actual fundraising strategy: how much you need, what milestone the money should reach, what type of investor fits the round, and what proof you can show today.

A pre-seed founder with a prototype and a handful of early users shouldn’t run the same process as a Series A company with revenue, retention data, and a clear go-to-market motion. The investor list, pitch, diligence expectations, and timeline all change.

Before outreach, answer the uncomfortable questions:

- How much runway will this round buy?

- What milestone will make the next round easier?

- Why is now the right time to raise?

- Which investors actually fund this stage and sector?

- What objections will investors raise first?

- What part of the story is still weak?

Every startup has a weak point. Maybe the market is hard to size. Maybe revenue is early. Maybe churn hasn’t been tested yet. Maybe the product works, but distribution is still fuzzy.

Don’t pretend the weak point doesn’t exist. The investor will find it anyway. Know the weakness, explain it plainly, and show how this round helps you solve it.

Stage 3: Prepare the Pitch Materials and Data Room

The pitch deck gets the attention, but it’s only one part of the fundraising package.

At minimum, you’ll need a strong deck, a short written blurb, a clean financial model, a cap table, customer or usage data, and a basic data room. The exact documents depend on the stage, but the goal is the same: make it easy for investors to understand the company and hard for them to doubt that you’re organized.

A pitch deck shouldn’t try to answer every question. It should create enough conviction to earn the next meeting.

A good deck usually covers:

- The problem

- The customer

- The product

- Market size

- Traction

- Business model

- Go-to-market plan

- Competition

- Team

- Financial snapshot

- Fundraising ask

- Use of funds

The data room does a different job. It supports the deeper work. Investors may ask for incorporation documents, cap table details, financial statements, customer contracts, intellectual property records, employment agreements, product metrics, legal history, tax documents, and prior financing documents.

Don’t wait until VC due diligence starts to clean this up. If the cap table says one thing, the deck says another, and the model quietly assumes something else, investors will notice. Same with missing founder IP assignments, unexplained contractor work, or revenue numbers that change depending on which spreadsheet someone opens.

Investors don’t expect your company to be flawless. They expect your cap table, your pitch deck, and your financial model to actually agree with each other.

Stage 4: Build the Investor List Carefully

A poorly targeted investor list doesn’t just waste your time. It skews your perspective with irrelevant feedback.

If you pitch the wrong investors, the rejections may not mean the company is weak. They may simply mean the company doesn’t fit that fund’s stage, check size, geography, sector, ownership target, or investment thesis.

Build the list around fit, not fame.

Look at:

- Stage focus

- Sector focus

- Typical check size

- Geography

- Recent deals

- Partner interests

- Portfolio conflicts

- Fund size

- Follow-on capacity

- Whether they lead rounds or follow

The lead investor question matters because some funds are happy to write smaller checks after someone else leads, while others want to set terms and take a board seat. If you only talk to followers, you may hear plenty of interest and still fail to close because nobody wants to lead.

That’s the fundraising version of everyone saying they’ll come to dinner once someone else books the restaurant.

Group your investor list into tiers, then run the process in batches. Don’t pitch the dream investor first while the story is still rough. Use early conversations to sharpen the pitch, learn objections, and improve the materials before the highest-priority meetings.

Stage 5: Start Outreach and Manage Momentum

VC fundraising is part storytelling and part pipeline management.

Warm introductions still matter in many markets because investors use trusted referrals as a filter. A strong intro from a founder, operator, angel, lawyer, or portfolio company can help your pitch get read faster. Cold outreach can work too, but it needs to be sharp, specific, and easy to evaluate.

Keep your outreach email brief. Explain what the company does, why it matters now, what traction exists, and why the investor is a relevant fit.

Don’t try to secure an investment through a cold email. Your only goal right now is to get them on a 15-minute call.

Once meetings begin, manage momentum like a real process. Track every conversation. Note objections. Follow up quickly. Keep investors updated when traction improves. Don’t let conversations drift into vague friendliness.

A common mistake is confusing politeness with interest. Investors are often friendly. They may say the market is exciting, the founder is impressive, and the product is interesting. None of that means the firm is moving toward a term sheet.

Watch what they do next. Another meeting, partner involvement, customer calls, data requests, specific deal questions, or a request to begin diligence tells you far more than a warm compliment.

Stage 6: Handle First Meetings and Partner Meetings Differently

The first investor meeting is usually about curiosity and fit.

The investor wants to know whether you’re credible, whether the problem matters, whether the market is large enough, and whether the company has a shot at becoming fund-returning. Your job is to tell a clear story, not drown the room in every detail.

A strong first meeting usually answers three things:

- Why this problem matters

- Why this company can win

- Why now is the right moment

If the investor is interested, the process may move to deeper meetings, partner meetings, technical reviews, customer references, or market calls. This is where the bar changes. You’re no longer just pitching one person; you’re giving that person enough ammunition to convince their own partnership.

This shift is critical because your internal champion still needs to sell the deal inside the firm. Make that easier. Give them clean metrics, sharp positioning, clear responses to objections, and a credible reason why the company can become large.

Treating every meeting the same is a mistake. The first meeting creates interest. The later meetings need to create conviction.

Stage 7: Understand the Term Sheet

A term sheet is the investor’s proposed deal framework. It’s not money in the bank.

Founders often celebrate the term sheet, and fair enough. It’s a major milestone. It’s also where the most important economic and control terms begin to harden.

A VC term sheet usually includes:

- Investment amount

- Pre-money or post-money valuation

- Option pool expectations

- Liquidation preference

- Board composition

- Pro rata rights

- Protective provisions

- Founder vesting terms

- Information rights

- Exclusivity period

- Closing conditions

Valuation gets the headline, but don’t stare at valuation alone. A higher valuation with harsher terms can be worse than a slightly lower valuation with cleaner rights. Option pool treatment, liquidation preferences, board control, and protective provisions can matter a lot later.

Take exclusivity seriously too. Once you sign a no-shop or exclusivity clause, you may be restricted from talking to other investors for a set period. That can be reasonable, but don’t treat it like a harmless paragraph. If the term sheet falls apart during diligence, you may have lost time and momentum.

Before signing, model the round. Read the control terms. Ask what the investor actually wants beyond ownership. And use a startup lawyer. Saving legal fees at the term sheet stage can become very expensive later.

Stage 8: Prepare for VC Due Diligence

VC due diligence is where investor interest turns into verification.

At this stage, the investor checks whether the story holds up. They may review the product, market, financials, customers, legal structure, cap table, team, technology, intellectual property, compliance risks, and prior financing documents.

Don’t treat diligence like an exam you can cram for. If the company’s records are sloppy, diligence becomes a scavenger hunt. The investor asks for one document, then another, then a clarification, then a mismatch appears, then lawyers get involved, and suddenly the round has lost two weeks.

Investors know your startup is messy behind the scenes. They just want you to be organized, honest, and upfront about where the bodies are buried.

Common diligence areas include:

| Diligence Area | What Investors Usually Check |

|---|---|

| Corporate records | Formation documents, board approvals, stock issuances, prior financing docs |

| Cap table | Founder shares, investor ownership, options, SAFEs, notes, warrants |

| Financials | Revenue, expenses, burn rate, runway, cash use, projections |

| Customers | Contracts, retention, concentration risk, references, pipeline |

| Product and technology | Roadmap, architecture, security, scalability, technical debt |

| Legal and compliance | Litigation, taxes, employment matters, regulatory exposure |

| IP ownership | Founder assignments, contractor agreements, patents, trademarks, code ownership |

| Team | Founder roles, key hires, compensation, employee agreements |

The hardest diligence problem isn’t a known weakness. It’s a surprise. If there’s a customer concentration issue, say it. If a founder left, explain it. If a contractor built early product code and the IP assignment was cleaned up later, show the paper trail.

Investors can usually handle risk. What they don’t like is discovering risk after you acted like there was none.

Stage 9: Negotiate the Final Documents

After the term sheet and VC due diligence, the deal moves into final legal documents.

For priced rounds, this can include a stock purchase agreement, investors’ rights agreement, voting agreement, right of first refusal and co-sale agreement, amended certificate of incorporation, board consents, disclosure schedules, and other closing documents. The exact package depends on the jurisdiction, stage, and deal structure.

This is where the process may slow down again. The investor has said yes. Diligence is mostly done. Everyone wants the round closed. Then the lawyers start marking up documents, and small points can suddenly feel larger than expected.

Some terms are routine. Others deserve careful attention.

Watch for:

- Board control

- Protective provisions

- Founder vesting resets

- Option pool size

- Information rights

- Pro rata rights

- Drag-along terms

- Liquidation preference details

- Anti-dilution protection

- Investor consent rights

You don’t need to become a lawyer. You do need to understand what you’re agreeing to. “Market standard” isn’t a magic phrase. Sometimes it means fair and common. Sometimes it means the other side would prefer you stop asking questions.

Negotiate the terms that matter, accept the ones that are truly standard, and don’t burn goodwill fighting over every comma.

Stage 10: Close the Round and Handle the First 30 Days After

Closing is the point where documents are signed and money is wired. It sounds like the finish line, but it’s really the start of the investor relationship.

The first 30 days after closing matter more than founders think. Investors want to see that you can turn capital into disciplined execution. That doesn’t mean spending aggressively just because the round closed. It means moving against the plan that justified the raise in the first place.

Quickly align on:

- Board schedule

- Reporting cadence

- Hiring plan

- Budget and burn rate

- Milestones for the next round

- Key risks to monitor

- How investors can help

This is also the moment to avoid the post-fundraise ego spike. Raising VC money isn’t success. It’s fuel. You still have to earn the valuation, grow into the story, and make the next financing easier than the last one.

Use the close as a reset. Clean up investor communication, tighten the operating rhythm, and turn the fundraising story into an execution plan.

What to Prepare Before Raising VC Money

You don’t need every answer before pitching, but you can’t walk in empty-handed.

At minimum, prepare these:

| Item | Why It Matters |

| Clear fundraising ask | Investors need to know how much you’re raising and why |

| Use of funds | Shows how the money turns into measurable progress |

| Updated cap table | Helps investors understand ownership and dilution |

| Financial model | Shows revenue, burn, runway, and assumptions |

| Traction metrics | Proves the company is moving, not just describing a market |

| Customer evidence | Supports demand, retention, and willingness to pay |

| Legal documents | Reduces friction during VC due diligence |

| Founder story | Explains why this team should win |

| Competitive view | Shows you understand the market honestly |

| Next-round milestone | Connects today’s raise to tomorrow’s financing logic |

The most useful preparation isn’t decoration. A beautiful deck won’t hide weak thinking for long. Know your numbers, your customers, your risks, and the reason this round exists.

If the money doesn’t clearly buy progress, the investor will feel it.

Common Mistakes That Slow Down the Venture Capital Process

Most fundraising mistakes aren’t dramatic. They’re small delays, vague answers, weak targeting, and messy documents that slowly drain momentum.

A few problems show up again and again:

- Pitching investors who don’t fund your stage

- Starting outreach too late in the runway

- Asking for money before the milestone story is clear

- Treating every investor conversation as equally serious

- Overvaluing verbal enthusiasm

- Hiding weak metrics instead of explaining them

- Having inconsistent numbers across the deck, model, and data room

- Waiting until diligence to fix corporate documents

- Signing a term sheet without understanding control terms

- Choosing valuation over investor fit

The runway mistake deserves special attention. Fundraising almost always takes longer than founders want it to take. Starting when the bank account is already too thin puts you in a weaker position, even if the company is good.

VCs can smell time pressure. Sometimes they’re polite about it. The cap table won’t be.

The Practical Takeaway Before You Start

The venture capital process isn’t just a sequence of pitch meetings. It’s a trust-building process with money at the end.

A sharp deck and a warm intro can get you in the room, but they won’t survive weak numbers, messy documents, or a story that falls apart during VC due diligence. Raising VC money only helps if the company can turn that capital into a stronger position before the next round.

Do the boring work early. Clean the cap table. Know the numbers. Build the right investor list. Figure out your dilution math before the term sheet arrives, not when you’re under a ticking clock.

Explain the risk before someone else finds it. That’s how the venture capital process becomes less mysterious and a lot less painful.

Frequently Asked Questions (FAQs) About the Venture Capital Process

What is the venture capital process?

The venture capital process is the path a startup follows to raise funding from VC investors. It usually includes fundraising strategy, investor outreach, pitch meetings, partner review, term sheet negotiation, VC due diligence, final legal documents, and closing.

How long does VC fundraising take?

The timeline depends on the company’s stage, market, traction, investor demand, and legal complexity. Expect the process to take months, not a few casual calls. Waiting until runway is almost gone usually makes the round harder.

What do VCs look for before investing?

VCs usually look for a large market, strong team, clear product value, early traction, growth potential, clean ownership structure, and a believable path to a major outcome. They also want to understand risks before committing.

What happens during VC due diligence?

During VC due diligence, investors verify the company’s claims and review documents related to financials, customers, cap table, legal records, intellectual property, product, team, and risks. The goal is to confirm that the investment opportunity matches the pitch.

Is a term sheet legally binding?

A term sheet is often non-binding on the main investment terms, but some parts, such as confidentiality or exclusivity, may be binding. Review any term sheet with a startup lawyer before signing.

What is the hardest part of raising VC money?

The hardest part is often not the pitch itself. It’s creating enough investor conviction while keeping the process moving. Weak targeting, messy documents, unclear milestones, and slow follow-up can make even a promising company harder to fund.