Did a late payment or high balance suddenly drop your credit score? You are not stuck. Recent negative marks hurt the most, but taking immediate action can help you rebuild credit score fast and recover much sooner than expected.

Start by pulling official credit reports from Equifax, Experian, and TransUnion to dispute any damaging errors immediately. Next, focus on lowering overall credit utilization and setting up automatic bill pay to guarantee consistent, on-time payments every single month. Beyond these fundamental habits, leverage smart financial tools like Experian Boost, rent reporting services, secured credit cards, and dedicated credit builder loans to actively generate a positive payment history.

Grab those latest financial statements and implement this simple, steady, and realistic approach. With the right actionable strategies firmly in place, transforming your financial standing is completely within reach.

Understand Your Credit Score

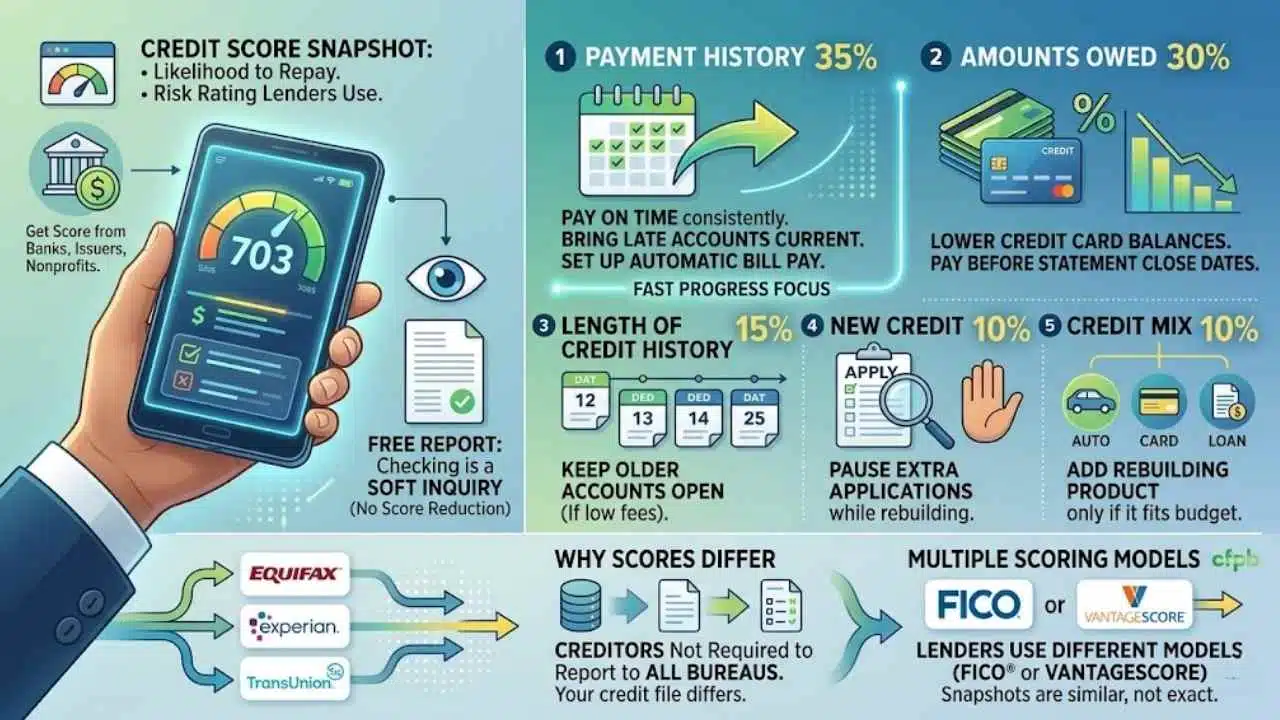

Your credit score is really a snapshot of how lenders see your borrowing habits right now. If you want fast progress, you need to know which parts of that snapshot can change in the next billing cycle and which ones take longer.

The Consumer Financial Protection Bureau explains that you can have more than one score because lenders may use different scoring models, and the information can come from different credit reporting agencies. That is why your FICO® score and your VantageScore may not match exactly.

What is a credit score?

Fast credit score gains usually come from fixing report errors, getting current on any missed payments, and cutting card balances before the next statement closes.

A credit score is a three-digit number that estimates how likely you are to repay what you borrow. Your credit reports hold the raw details, and the score turns those details into a risk rating lenders can read quickly.

Your free credit reports do not usually include a free score, so you may need to get your FICO® score or VantageScore from a card issuer, bank, or nonprofit counselor. Checking your own report is a soft inquiry, which means it does not lower your score.

| FICO® factor | Weight | What to do first |

|---|---|---|

| Payment history | 35% | Bring late accounts current and set up automatic bill pay |

| Amounts owed | 30% | Pay down credit card balances before the statement closing date |

| Length of credit history | 15% | Keep older accounts open if they do not charge costly fees |

| New credit | 10% | Pause extra applications while you rebuild |

| Credit mix | 10% | Add a rebuilding product only if it fits your budget |

How is a credit score calculated?

FICO says payment history counts for 35% of the score, amounts owed counts for 30%, length of credit history counts for 15%, and both new credit and credit mix count for 10% each. That tells you where to spend your energy first: on-time payments and lower balances.

Recent and severe late payments usually do more damage than older ones, which is why getting current matters so much. Lowering credit card balances can help quickly because card issuers usually report balances every month, often based on the statement balance that appears on your billing statement.

Your reports can also differ because creditors are not required to report to every bureau. If one lender reports to Experian and TransUnion but not Equifax, your credit file can look different at each bureau, and your score can move differently too.

Evaluate Your Current Credit Situation

Before you try to fix anything, get clear on what is actually hurting you. A smart rebuild starts with facts, not guesses.

Request and review your credit report

In the latest CFPB guidance, U.S. consumers can review their reports online weekly from Equifax, Experian, and TransUnion through the official annual credit report service, and Equifax is also offering six extra free reports every 12 months through December 31, 2026. That gives you a real chance to catch mistakes and track progress without paying for a monitoring subscription.

- Pull all three reports at the same time so you can compare them side by side.

- Check your name, address, employers, account status, balances, and every late payment entry.

- Look for closed accounts listed as open, duplicate collection items, or accounts that are not yours.

- Match each account to your bank accounts, loan records, and credit card statements.

- Write down each card’s due date and statement closing date, because both dates matter for rebuilding.

- Get a free score from a bank, card issuer, or nonprofit credit counseling agency so you can track your FICO® score or VantageScore each month.

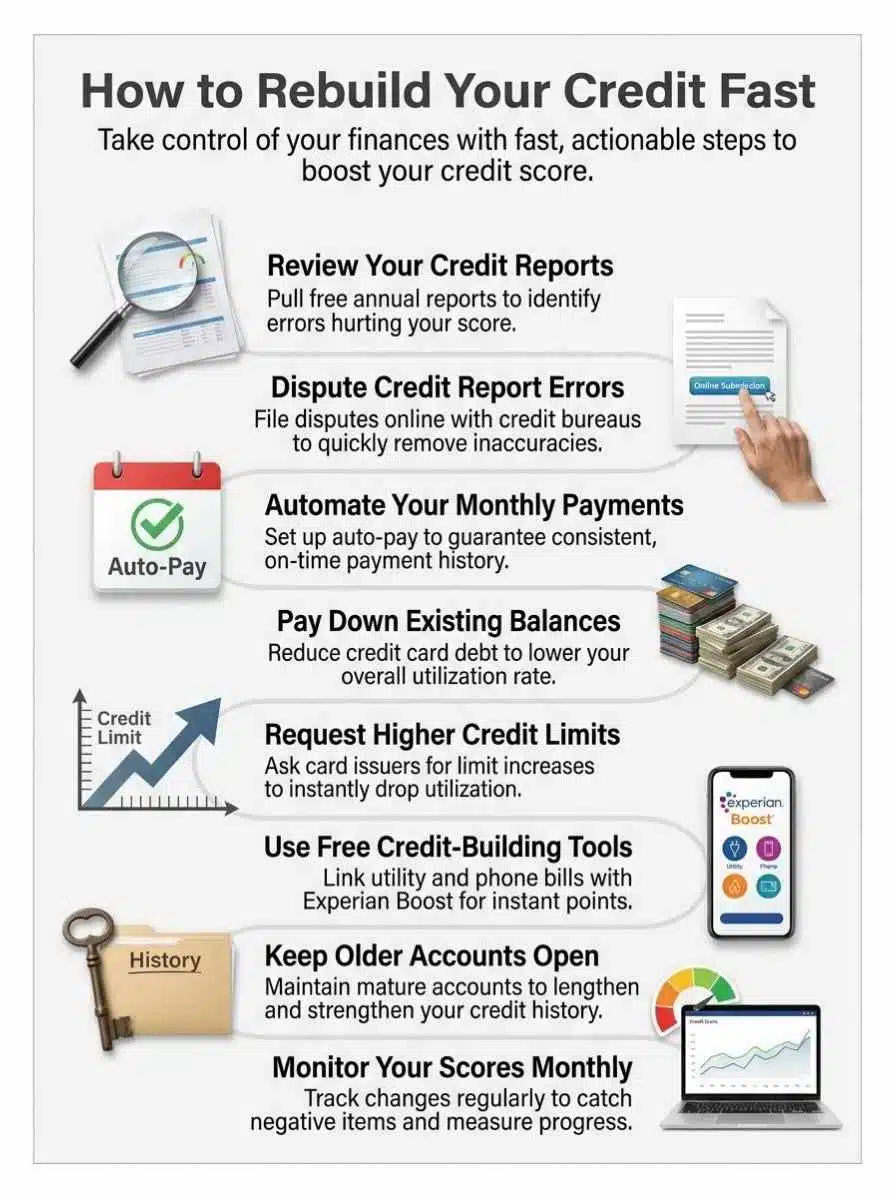

Dispute inaccuracies on your report

If an item is wrong, dispute it with the bureau that shows the error and with the company that supplied the information. The CFPB says you already have the legal right to dispute inaccurate information for free, so you do not need to hire a credit repair company to do this step for you.

Accurate negative information usually cannot be removed early, and most negative items stay on a report for seven years, with some items, like bankruptcy, staying longer. That is why you want to focus on deleting errors, not paying for empty promises.

- File a separate dispute with each bureau that shows the mistake, because fixing one report does not automatically fix the others.

- Attach copies of proof, such as statements, canceled checks, payoff letters, or identity documents.

- Be specific about what is wrong: wrong balance, wrong date, wrong account, duplicate item, or not your account.

- Credit reporting companies generally must investigate within 30 days, and some cases can stretch to 45 days.

- After the investigation ends, you should receive the result and an updated report if a correction was made.

Steps to Rebuild Your Credit Score Fast

If your goal is to raise your credit score as fast as possible, focus on the actions that can change what lenders see in the next 30 to 45 days. These are the moves that usually create the quickest traction.

| Fast move | Why it can work quickly | Best for | Watch for |

|---|---|---|---|

| Dispute report errors | Incorrect negatives can be removed after investigation | Anyone who spots a mistake | You need proof and patience during the review period |

| Pay down balances before the statement closes | Lower reported utilization can help by the next reporting cycle | People with high card usage | Paying after the due date is not the same as lowering the reported balance |

| Request a higher credit limit | A larger limit can reduce utilization without adding debt | People with solid recent payment history | Some issuers may use a hard inquiry |

| Use Experian Boost | It can add eligible bills to your Experian file at no cost | People with thin files or limited positive history | It does not help every score or every lender decision |

Pay your bills on time, every time

This is the big one. Payment history carries the most weight in FICO®, and both FICO and the CFPB make it clear that on-time payments are the strongest signal of healthy credit behavior.

If you are behind, get current first. Then protect the streak by turning on automatic bill pay for at least the minimum due and adding calendar reminders a few days before each due date.

Lower your credit card balances

High credit utilization can drag a score down even if you never miss a payment. The CFPB says experts advise keeping your balances at no more than 30% of your total credit limit, and lower is usually better.

Here is the faster play: pay your card before the statement closing date, not just by the due date. Since many issuers report the statement balance, an early payment can shrink the balance that lands on your credit report.

Request higher credit limits

A higher limit can help quickly because it lowers your utilization ratio without opening a new account. This works best if your spending stays the same and your recent on-time payments are strong.

Ask your issuer how it handles credit limit requests before you submit one. The CFPB notes that a lender may pull your credit to evaluate a limit increase, and a hard inquiry can cause a small short-term dip.

Avoid applying for unnecessary credit

New credit accounts can slow your rebuild because they create hard inquiries and lower your average account age. FICO says new credit accounts make up 10% of the score, so extra applications can work against you while you are trying to recover.

Freeze the impulse to open store cards, buy-now-pay-later offers, or random promotional accounts. If you really do need a loan, shop efficiently, because FICO can treat certain rate-shopping inquiries for one loan as a single event when they are coded that way.

Utilize Credit-Building Tools

The right tool can add positive activity to your credit file, but no tool fixes bad habits. Pick one that fits your budget, then use it consistently.

| Tool | How it helps | Best use case | Key detail |

|---|---|---|---|

| Secured credit card | Adds revolving credit activity and payment history | You need a card but cannot qualify for a standard one | Requires a refundable security deposit |

| Credit builder loan | Adds installment payment history and savings | You need structure and can handle fixed payments | These often run for six to 24 months |

| Rent reporting | Turns on-time rent into credit data when reported | You rent and pay on time | Ask which bureaus receive the data |

| Experian Boost | Adds eligible household bills to your Experian file | You want a free add-on | It affects only Experian-based scoring uses |

Use secured credit cards

A secured credit card requires a refundable deposit, but it works like a regular credit card once the account is open. The CFPB lists secured cards as one of the safest ways to start or rebuild a long credit history when you do not qualify for a standard card yet.

Keep this simple: put one small recurring charge on the card, keep the balance low, and pay it in full every month. That gives you steady revolving credit activity without making it easy to overspend.

Build credit through rent payments

Rent can help more than many people realize. The CFPB’s company list notes that Experian includes some positive rent data from Experian RentBureau in standard Experian credit reports, and VantageScore says rent and utility data can count when it is reported to the nationwide bureaus.

Before you sign up for a rent-reporting service, ask your landlord or the provider a few clear questions. You want to know whether it reports positive payments, how often it reports, and which bureaus receive the data.

- Does it report to one bureau or all three?

- Does it report every month without gaps?

- Are only missed payments reported, or are on-time payments reported too?

- Is there a monthly fee that would strain your budget?

Consider Experian Boost for utility and phone bills

Experian Boost is free and can add eligible utility, telecom, internet, streaming, insurance, and some rent payments to your Experian credit file. Experian says you generally need at least three eligible payments in the last six months, including one in the last three months, for a bill to qualify.

As of 2026, Experian says users who receive a boost gain an average of 14 points on FICO® Score 8 based on Experian data. The trade-off is important: not all lenders use Experian credit files, and Experian’s own disclosure says most mortgage lenders do not consider scores affected by Boost.

Maintain Healthy Credit Habits

Once your score starts moving up, your next job is to protect the progress. Good credit grows from small habits that repeat month after month.

- Keep balances low compared with your total credit limits.

- Pay every bill on time, even if you can only automate the minimum due at first.

- Watch old accounts for fraud or surprise fees instead of ignoring them.

- Check your credit reports and score on a set schedule.

Keep older credit accounts open

Older accounts help because they support your average account age and your total available credit. The CFPB also warns that closing a card can raise your utilization ratio, which can pull your score down.

If an older card has no annual fee and you can manage it safely, keep it open and use it lightly. A tiny purchase every few months plus autopay can keep the account active without building debt.

Diversify your credit types responsibly

Credit mix matters, but it is a smaller factor than payment history and amounts owed. That means you should never open multiple products just to chase the mix portion of your score.

A better approach is to add one tool that fills a real gap. The CFPB describes credit builder loans as savings-linked loans that usually run from six to 24 months, which can be helpful if you need installment history and can afford the payment.

Regularly monitor your credit score

During an active rebuild, check your credit reports often and your score at least once a month. Weekly report access makes it easier to catch changes quickly, especially after a dispute, a payoff, or a missed payment correction.

Use a score service from your bank, card issuer, or nonprofit counselor, and look at the same model each month so you are comparing apples to apples. Your credit file may update before your score service refreshes, so give changes a little time to show up.

Seek Professional Assistance if Needed

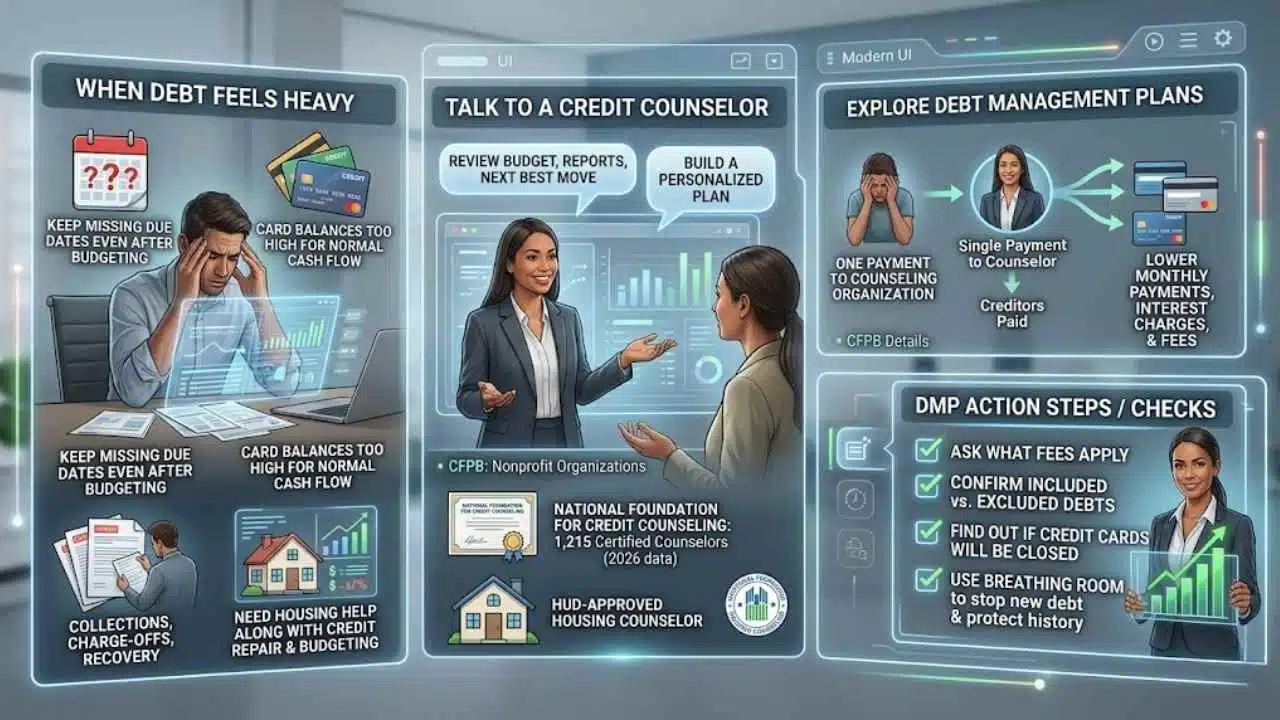

You do not have to figure out every part of this alone. If debt feels heavy or your reports are a mess, outside help can save you time and bad decisions.

- You keep missing due dates even after making a budget.

- Your card balances are too high to pay down with normal monthly cash flow.

- You are dealing with collections, charge-offs, or bankruptcy recovery.

- You need housing help along with credit repair and budgeting support.

Talk to a credit counselor

Nonprofit credit counseling can help you review your budget, your credit reports, and your next best move. The CFPB says credit counseling organizations are usually nonprofit and can help you build a budget, review debts, and create a personalized plan.

For a practical starting point, the National Foundation for Credit Counseling says it has 1,215 certified counselors serving all 50 states and U.S. territories in 2026. If your credit issues connect to rent, housing, or a future home purchase, a HUD-approved housing counselor can also be a smart call.

Explore debt management plans

A debt management plan can help if your main problem is high unsecured debt, not a lack of credit tools. The CFPB says a debt management plan lets you make one payment to the counseling organization, which then pays your creditors, and it can lower monthly payments, interest charges, and fees.

- Ask what fees apply before you enroll.

- Confirm which debts are included and which are not.

- Find out whether any credit cards will be closed during the plan.

- Use the breathing room to stop new debt and protect your payment history.

Final Thoughts

You can rebuild your credit score faster than you might expect if you start with the right problems. Pull your credit report, fix errors, get current on any missed payments, and pay down card balances before the next statement closes. If you need extra help, use one smart tool, like a secured credit card, rent reporting, a credit builder loan, or Experian Boost, and back it up with automatic bill pay. If the debt load is too heavy, a nonprofit credit counseling agency can help you map out the next move.

Small, steady actions build a stronger credit history. Stick with them, and better loan options, lower costs, and more peace of mind get closer every month.

Frequently Asked Questions (FAQs) About Rebuilding Your Credit Score Fast

1. How can I rebuild my credit score fast?

Start with on-time payments, cut balances to lower credit utilization, and fix errors on your credit report. Open a credit-builder loan or a Visa secured card, use it small, and pay it off each month.

2. How fast will my score improve?

You can see small wins in a month, big gains often take three to twelve months.

3. Should I pay off collections or old debts?

Yes, pay what you can, collections hurt your score. Ask for a written pay-for-delete or a settlement that says the debt is paid. Paying old debt usually helps faster than leaving it to linger, tame the beast sooner.

4. Should I use credit monitoring or credit counseling?

Use free credit monitoring to spot errors and fraud fast. A nonprofit credit counseling agency can set a clear plan, pick one with good reviews.