Navigating New Zealand’s retirement landscape in 2026 requires a significant shift in strategy. As of today, April 1, 2026, the KiwiSaver rules have undergone their most substantial transformation in over a decade. The transition from a 3% to a 3.5% minimum contribution rate is more than just a payroll adjustment; it is a fundamental reset of the “social contract” between employees, employers, and the state. With the government co-contribution halved and high-earners now excluded from certain benefits, KiwiSaver Optimization 2026 is no longer about “set and forget.” It is about actively managing your contributions and tax settings to ensure you aren’t leaving thousands of dollars on the table during your working life.

How We Selected Our 12 Best KiwiSaver Optimization 2026 Facts

To assemble this guide, we analyzed the final 2025 Budget implementation notes and the 2026/27 Inland Revenue (IRD) operational guidelines. Our selection prioritized the most recent “shocks” to the system, such as the halving of the government top-up and the specific new rules for 16- and 17-year-olds. We focused on the technical “leaks” that most members miss, including Prescribed Investor Rate (PIR) errors and the impact of Employer Superannuation Contribution Tax (ESCT). These 12 facts were chosen because they represent the highest-leverage changes you can make today to secure a more comfortable retirement or a larger first-home deposit in the current year.

12 Essential Realities for KiwiSaver Optimization 2026

The following insights detail the technical shifts and strategic opportunities available to New Zealanders navigating the scheme this year.

1. The New 3.5% Contribution Floor

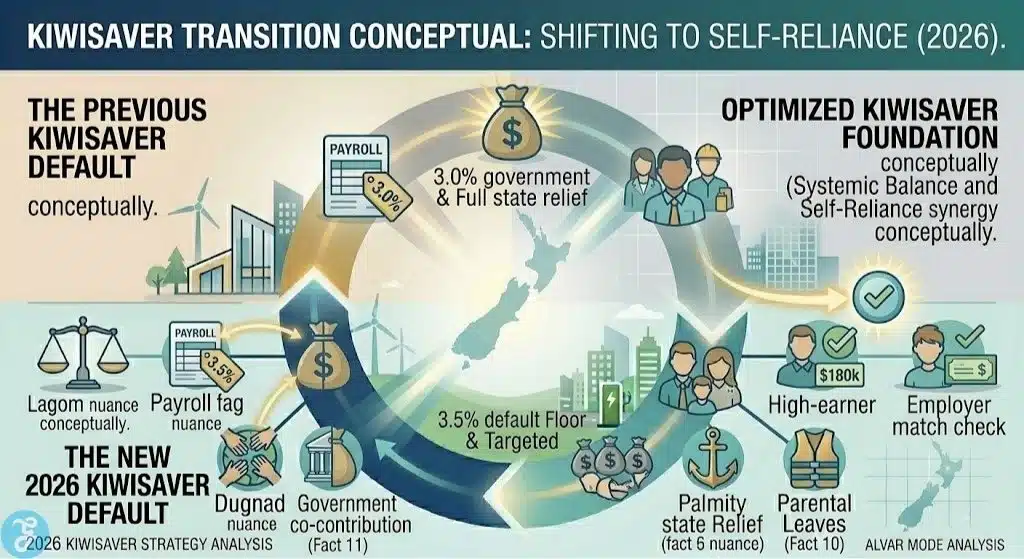

From today, April 1, 2026, the default minimum contribution rate for both employees and employers has officially increased from 3% to 3.5%. If you were previously on the 3% rate, this change happens automatically. This “forced” increase is designed to combat the growing retirement savings gap in New Zealand.

Best for: average wage earners who haven’t reviewed their rates in years.

Why We Chose It:

-

It is the most significant structural change to KiwiSaver in 2026.

-

It leverages “autopilot” to boost your long-term compounding returns significantly.

Things to consider:

-

You will notice a small drop in your take-home pay this week as the higher rate kicks in.

2. The “3% Opt-Down” Employer Risk

While the new default is 3.5%, you can apply to the IRD for a temporary “rate reduction” back to 3% for 12 months. However, there is a catch: if you opt down to 3%, your employer is also legally permitted to drop their match to 3%.

Best for: individuals facing temporary financial tight spots who still want some employer match.

Why We Chose It:

-

It highlights a hidden “penalty” for trying to maximize take-home pay.

-

It shows how a 0.5% saving in your pocket could cost you 1% in total retirement growth.

Things to consider:

-

Some generous employers may still contribute 3.5% even if you drop to 3%, but they are not required to.

3. The Government Contribution Has Been Halved

As of the 2025/26 year (impacting the payment you receive in July 2026), the government co-contribution has been cut from 50 cents per dollar to 25 cents. The maximum annual “free money” from the state is now just $260.72, down from the previous $521.43.

Best for: self-employed members and those on “savings suspensions.”

Why We Chose It:

-

It represents a major reduction in the “guaranteed ROI” of the scheme.

-

It changes the “lump sum” math for those who manually top up their accounts.

Things to consider:

-

You still need to contribute $1,042.86 annually to get the full (now smaller) $260 top-up.

4. The $180,000 High-Earner Exclusion

In a 2026 policy shift toward targeted welfare, the government has completely removed the annual co-contribution for anyone earning over $180,000 per year. If you fall into this bracket, your manual top-ups will no longer trigger the $260.72 payment.

Best for: senior professionals and high-income earners.

Why We Chose It:

-

It marks the first time KiwiSaver benefits have been means-tested by income.

-

It forces high earners to look at other tax-efficient investment vehicles outside of KiwiSaver.

Things to consider:

-

Your employer is still required to provide the 3.5% match regardless of your income level.

5. 16- and 17-Year-Olds Get a 3.5% Head Start

Starting April 1, 2026, employers are now required to provide the compulsory 3.5% match for employees aged 16 and 17. Previously, these younger workers received no employer match and no government co-contribution.

Best for: teenagers in part-time work and parents looking to build their children’s wealth.

Why We Chose It:

-

It is a powerful “time-value of money” win for younger Kiwis.

-

It encourages early financial literacy and “skin in the game” for school-aged workers.

Things to consider:

-

16- and 17-year-olds are also now eligible for the (halved) government co-contribution.

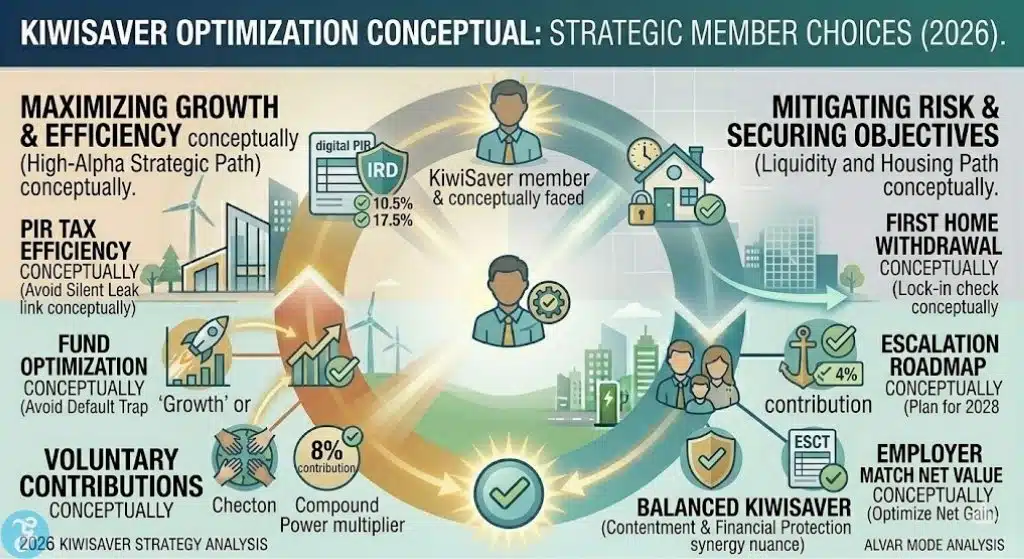

6. The PIR “Silent Leak”

Your KiwiSaver returns are taxed at your Prescribed Investor Rate (PIR). If you haven’t updated this to match your current income, you might be paying 28% tax when you should be paying 10.5% or 17.5%. In 2026, the IRD has automated most of this, but it is still your responsibility to confirm the rate.

Best for: anyone whose income has fluctuated significantly in the last two years.

Why We Chose It:

-

Using the wrong PIR is the most common way to accidentally “bleed” retirement savings.

-

Overpaid PIE tax is generally not refundable if you have provided the wrong rate.

Things to consider:

-

Check your PIR through myIR; it’s based on your income from the previous two tax years.

7. ESCT: Your Employer’s 3.5% Isn’t 3.5%

When your employer contributes to your KiwiSaver, that money is taxed before it hits your account. This is the Employer Superannuation Contribution Tax (ESCT). If your employer says they are matching your 3.5%, the actual amount that enters your fund is 3.5% minus a tax of 10.5% to 39% (depending on your salary).

Best for: members doing exact retirement projections and “net worth” tracking.

Why We Chose It:

-

It clears up the confusion about why “Employer Contributions” on statements are always lower than expected.

-

It shows the true net value of the employer match for high earners.

Things to consider:

-

For most, the net employer match is still the single best “guaranteed” return you’ll ever find.

8. The $1,000 “Locked” Reserve for First Homes

If you are using KiwiSaver for a first-home deposit in 2026, you cannot empty the account. You must leave at least $1,000 in your fund. This “lock-in” is designed to keep the account active so you can continue saving for retirement after your house purchase.

Best for: first-home buyers calculating their maximum available deposit.

Why We Chose It:

-

It’s a “surprising” hurdle that can leave buyers $1,000 short on settlement day if not planned for.

-

It underscores that KiwiSaver’s primary purpose remains retirement, not just housing.

Things to consider:

-

You also cannot withdraw any funds transferred from an Australian Superannuation scheme.

9. The 0.5% Increase Compounding Power

While 0.5% sounds small, for a 25-year-old on an average salary, the jump from 3% to 3.5% (matched by the employer) can result in an extra $80,000 to $120,000 in their account by age 65, assuming standard market returns.

Best for: younger members who feel the 0.5% pay cut is a burden.

Why We Chose It:

-

It provides the mathematical “why” behind the 2026 rate hike.

-

It visualizes the massive impact of small, consistent changes over decades.

Things to consider:

-

This effect is doubled because the employer is also forced to increase their 0.5% share.

10. The Default Fund “Limbo” Trap

If you don’t choose a fund, you are assigned to a “Default Fund.” While these were moved from Conservative to Balanced in 2021, staying in a default fund for 20 years can cost a younger worker hundreds of thousands in potential growth compared to a “Growth” or “Aggressive” fund.

Best for: “passive” members who have never logged into their provider’s portal.

Why We Chose It:

-

Default settings are designed for safety, not for maximizing your specific life stage.

-

2026 data shows that “Growth” funds have significantly outperformed “Balanced” over the last 5 years.

Things to consider:

-

Changing funds takes less than two minutes and is usually free.

11. The First Home Grant is Gone

A surprising fact for those who haven’t bought a home since 2024 is that the First Home Grant (the extra $5,000–$10,000 from the government) was discontinued in May 2024. In 2026, the only “housing” help from KiwiSaver is your own withdrawal and the First Home Loan (low deposit) scheme.

Best for: parents giving advice to children based on “old” rules.

Why We Chose It:

-

It clears up common misinformation about available state subsidies for buyers.

-

It places more emphasis on KiwiSaver Optimization 2026 to build the deposit manually.

Things to consider:

-

You can still withdraw the “halved” government contributions you’ve earned over the years.

12. The 2028 Roadmap: 4% is Coming

The 2026 increase to 3.5% is only Phase 1. The government has already legislated that the minimum rate will jump again to 4% on April 1, 2028. This long-term roadmap allows you to plan your household budget for the next three years.

Best for: long-term budgeters and business owners planning labor costs.

Why We Chose It:

-

It signals a permanent shift toward a high-contribution retirement model.

-

It helps members normalize the idea of gradual “savings escalations.”

Things to consider:

-

Increasing to 4% (or even 8%) now gets the compounding engine started even earlier.

A Strategic Summary of KiwiSaver in 2026

The 2026 landscape for KiwiSaver is one of “self-reliance.” With the government reducing its direct financial support and increasing the mandatory “self-funding” rates, the message is clear: your retirement is your responsibility. By mastering the 3.5% floor, correcting your PIR tax “leaks,” and ensuring your fund choice matches your age rather than a default setting, you can turn these structural changes into a massive personal advantage. KiwiSaver remains New Zealand’s most accessible wealth-building tool, provided you take the wheel and drive it toward your specific goals.

Visualizing KiwiSaver Optimization: Rates and Returns

The tables below provide a clear look at how the 2026 changes affect your money and help you visualize the impact of your choices.

2026 Contribution and Tax Comparison

The following data outlines the new standard settings for the 2026/27 financial year.

Our Top 3 Picks and Why?

-

The 3.5% Default Floor: This is our top pick because it’s a “set-and-forget” win. By increasing the floor, the system is forcing better outcomes for millions of Kiwis without them having to lift a finger.

-

Correcting the PIR Tax Leak: We chose this because it’s a “free” gain. You don’t have to contribute more; you just have to stop the government from taking more than they’re owed on your returns.

-

16/17-Year-Old Employer Match: This is an essential pick for 2026 because it changes the trajectory of a young person’s life. Two extra years of compounding in their teens is worth more than a decade of savings in their 50s.

How to Optimize Your KiwiSaver by Yourself?

You don’t need a financial advisor to make the most of the 2026 changes. Most of the optimization is just “digital housekeeping” in your provider’s app or on the IRD website.

The Selection Framework

-

Assess Your “Time to Goal”: If you are 20+ years from retirement and not buying a house soon, a “Growth” fund is almost always mathematically superior to “Balanced.”

-

Calculate Your “Tax-Free” ROI: Even with the halved government contribution, a $1,043 contribution that gets $260 back is a 25% instant return. No bank account or stock market can guarantee that.

-

Review Your Payslip: Check that your employer has updated their match to 3.5% as of April 1, 2026. Payroll errors are common during rate transitions.

-

Check Your Australian Transfers: If you have money from an Aussie Super, remember it cannot be used for a first home. Keep this “locked” portion separate in your calculations.

The decision matrix below helps you decide which 2026 adjustment to prioritize based on your current life stage.

Decision Matrix

The Final Checklist: 5-Point KiwiSaver Health Check

-

Log into myIR and confirm your PIR is correct for your 2024/25 and 2025/26 income.

-

Check your latest payslip to ensure your contribution and employer match are both at 3.5%.

-

Switch your fund type if your investment horizon (time until withdrawal) has changed.

-

Set up an automatic payment of $20/week if you are self-employed to hit the $1,043 government target.

-

Mark April 1, 2028, in your calendar for the next jump to 4%.

Empowering Your Future in the 3.5% Era

The 2026 KiwiSaver updates are a clear message from the New Zealand government: the era of large state subsidies is ending, and the era of self-funded retirement is here. While the halving of the government co-contribution is a setback, the compulsory increase to 3.5% provides a more stable, long-term engine for your wealth. By being proactive—optimizing your tax rates, picking the right fund for your age, and ensuring you get every cent of your employer’s match—you can navigate this new standard with confidence. In the world of KiwiSaver Optimization 2026, the biggest risk isn’t the market; it’s staying on “default.”