Did an unfamiliar purchase, duplicate billing, or zombie subscription make a credit card balance spike? Initiating a credit card charge dispute is the most effective way to fight back, limit potential interest fees, and protect the account’s payment due date.

According to the Consumer Financial Protection Bureau, swift action is crucial. Consumers generally have exactly 60 days from the initial statement date to mail a formal written error notice. Following submission, the card issuer must officially acknowledge the complaint within 30 days. The complete investigation must then conclude within two billing cycles, never exceeding 90 days. Understanding these strict timelines guarantees proper evidence is gathered early, critical deadlines are successfully met, and the consumer’s financial security remains completely intact.

Understanding Credit Card Charges

Before you dispute the charge, figure out what kind of problem you are looking at. That one step tells you whether you should call customer service, contact the merchant, freeze the card, or mail a formal billing dispute right away.

In the CFPB’s 2025 market report, the biggest dispute categories on general-purpose cards in 2024 were services not received at 21% and canceled purchases or credits not issued at 18%. That is a strong reason to save delivery records and cancellation proof, not just your receipt.

Common types of credit card charges

Most charge errors fall into a few buckets. If you label the issue correctly, your paperwork gets easier and your consumer rights are clearer.

- Duplicate charges: The same purchase appears twice. Save the receipt and screenshot both line items, because this is a classic billing error.

- Wrong amount or missing credit: The merchant billed more than the receipt shows, or a promised refund never posted. Attach the receipt, return record, or cancellation email.

- Unauthorized charges: You did not make the purchase and did not allow anyone else to use the card. Call the issuer at once, ask for the card to be blocked or replaced, and follow up in writing.

- Subscription or membership fees after cancellation: This often happens with streaming plans, app renewals, service plans, and even groups such as an AARP membership. Your cancellation confirmation is the key document.

- Goods or services not received as agreed: A charge for something you never accepted, never received, or never got in the promised condition can qualify for dispute. Tracking records, appointment logs, and service emails help here.

- Pending hotel or rental holds: These can look like real charges even when they are still temporary authorizations. Ask the merchant when the hold should fall off before you file.

Difference between charge errors and fraudulent charges

A charge error usually starts with a real transaction that posted the wrong way, like a double billing, a wrong dollar amount, or a credit that never appeared. A fraudulent charge starts with use you did not authorize at all.

That difference matters. If a person was once allowed to use your credit card, the charge may still count as authorized until you tell the issuer that person no longer has permission.

| What you see | What it usually means | Best next move |

|---|---|---|

| Merchant billed twice | Billing error | Save the receipt, contact the merchant, then send a written notice if it is not fixed fast |

| Strange merchant name you do not recognize | Possible fraud or a confusing statement descriptor | Check recent emails and digital receipts first, then call the issuer if it still makes no sense |

| Refund promised but never posted | Missing credit | Gather the return confirmation and include it with your dispute |

| Small test charge followed by bigger activity | Possible fraud pattern | Lock the card, report unauthorized charges, and ask for a replacement card |

If you want the exact terms for your account, compare your cardmember agreement with the CFPB credit card agreement database. It can help you confirm billing dispute addresses, grace periods, and how your issuer handles unauthorized charges.

One of the most useful consumer protection rules in this process is simple: send your notice to the billing dispute address, not the payment address.

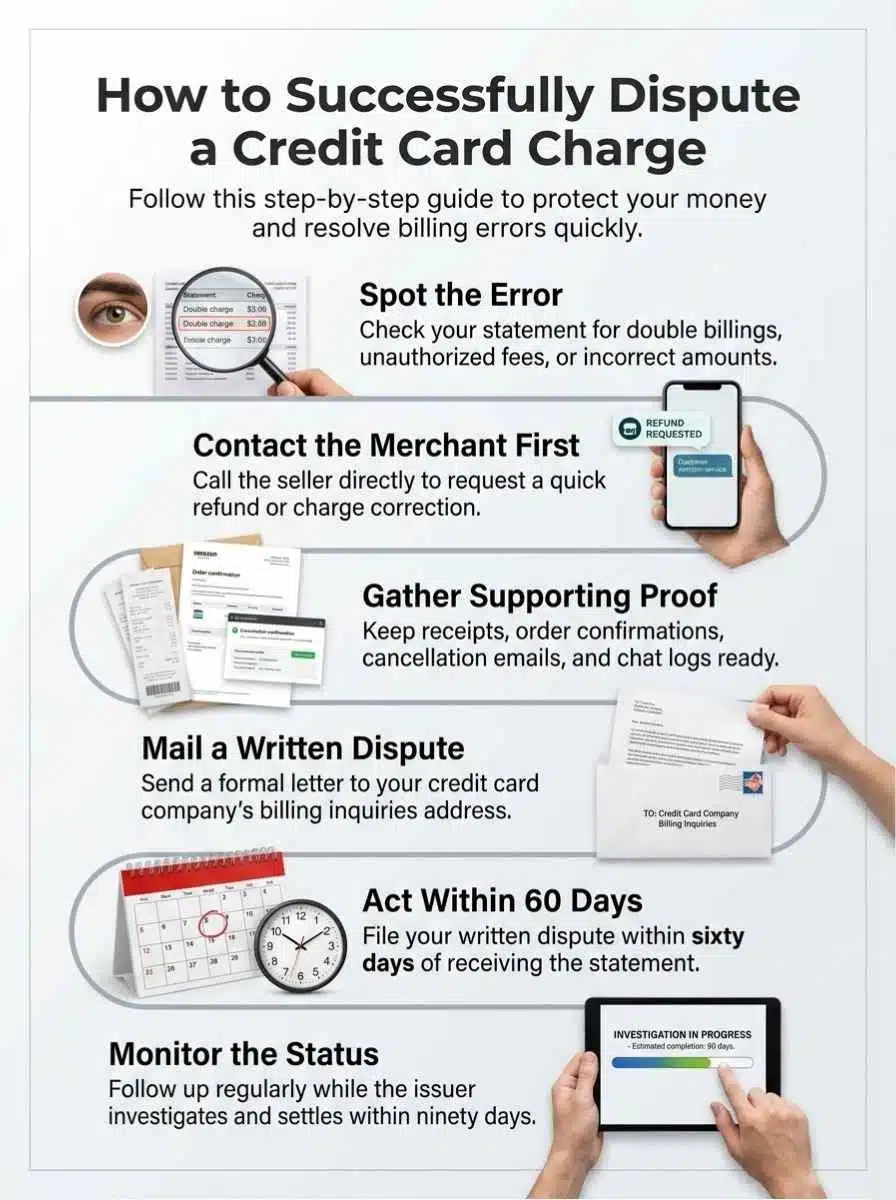

Steps to Dispute a Credit Card Charge

If you want to dispute a credit card charge successfully, follow the steps in order. A fast phone call can solve some issues, but the written notice is what protects your legal position.

Review the details of the charge

Start with the statement line itself: date, merchant name, amount, and whether the transaction is posted or still pending. Then match it against receipts, order numbers, shipping notices, travel confirmations, health or caregiving invoices, or any subscription emails you still have.

In the CFPB’s 2025 consumer credit card market report, up to 24% of disputed transactions in one survey were tied to statement descriptions people did not recognize. That is why it pays to search your inbox, app history, and rewards accounts before assuming fraud.

- Circle the exact line item in question.

- Write down why it is wrong in one sentence.

- Save a copy of the statement page and the receipt.

- Note the date the first statement showing the error was sent.

Contact the merchant directly

For many charge errors, the merchant is the fastest fix. A store manager, travel desk, medical office, contractor billing team, or subscription service can often reverse a duplicate or wrong charge before the issuer finishes its review.

The FTC warns consumers not to let a slow seller process push them past their legal deadline with the card issuer. If the 60-day clock is getting close, contact the merchant and prepare your written notice at the same time.

- Ask for a refund, corrected receipt, or written confirmation of cancellation.

- Write down the representative’s name and any case number.

- If the issue involves goods or services, state exactly what was missing or wrong.

- Keep chat transcripts and follow-up emails in one folder.

For a pure billing error, you do not have to wait for the merchant to answer before mailing your notice to preserve your rights. If the problem involves defective or undelivered goods and the seller will not help, federal claims and defenses rights may also help, especially if the purchase was over $50 and made in your home state or within 100 miles of your billing address.

Notify your credit card issuer

Call first so the bank, lender, or card/account holder can flag the transaction. If the issue looks like fraud, ask the issuer to freeze or replace the card and turn on fraud detection alerts in the mobile app.

Then send your written billing dispute to the issuer’s billing inquiries address. That address may be different from the place where you send your regular payment.

Major issuers such as Chase and Capital One now let cardholders lock a card in the app while they review suspicious activity. That quick step can stop fresh charges while the investigation process begins.

Submit a formal dispute

Your letter does not need legal jargon. It just needs the right facts, sent on time, with copies of proof.

- Your name and account number

- The dollar amount in dispute

- The transaction date and merchant name

- A short explanation of the billing error or unauthorized charge

- Copies of receipts, tracking records, cancellation proof, or chat logs

Once the issuer receives your notice, the usual timeline is an acknowledgment within 30 days and a full resolution within two billing cycles, no more than 90 days. Send copies, not originals, and keep everything in one folder.

If you manage household personal finance, travel reimbursements, retirement spending, or contractor bank records, a clean file makes follow-up much easier. It also gives you a clear record if you later need the Consumer Financial Protection Bureau or your state Office of the Attorney General.

A phone call starts the conversation. A written billing error notice starts the legal clock.

Tips for a Successful Credit Card Dispute

A strong dispute is simple: move fast, stay organized, and make the facts easy to verify. That approach helps customer service teams, fraud units, and investigators see the problem without guessing.

Don’t delay filing the dispute

The 60-day window runs faster than most people think, especially if the charge appears during travel, a move, or a busy caregiving season. If you wait through several rounds with the merchant, you can weaken the strongest part of your consumer protection rights.

You can still dispute a charge even if you already paid it. What matters most is whether you sent the notice on time and backed it up with clear records.

Keep all receipts and documentation

Good records turn a vague complaint into a clear case. Keep the statement page, receipt, cancellation proof, emails, chat transcripts, screenshots, shipping updates, and notes from every call.

This matters because the issuer should do a real review of the facts. That is much easier when your file clearly shows what happened and when it happened.

| If the problem is… | Best proof to attach |

|---|---|

| Duplicate charge | Receipt, statement screenshot, and both transaction dates |

| Canceled membership or subscription | Cancellation email, chat transcript, and final billing screen |

| Travel, health, or caregiving service not provided | Booking record, provider message, and any refund promise |

| Unauthorized charges | Statement page, fraud report number, and notes from your call with the issuer |

Be clear and concise in your communication

Your goal is not to tell the whole story in dramatic detail. Your goal is to make it easy for the issuer to see the exact error.

- Use one sentence to describe the problem.

- List the amount and transaction date exactly as shown.

- Attach proof in date order.

- Ask for written confirmation of the dispute.

If a charge includes tax or shipping because the entire purchase is wrong, dispute the full incorrect transaction. If the tax or shipping line is the only issue, that is usually a merchant correction issue, not a classic billing error case.

Follow up regularly on the status of the dispute

Once you send the letter, track the investigation process like a project. Save the mailing proof, write down every case number, and check whether the issuer sent the required acknowledgment.

The CFPB says you do not have to pay the disputed amount or related interest charges while the issuer investigates, but you still need to pay the undisputed part of your bill by the payment due date. That one habit protects your credit while the case is still open.

If the issuer denies the claim and the answer still does not fit the facts, ask what documents it relied on and consider escalating the matter with the CFPB. The bureau says it generally works to get a company response within 15 days after a complaint is submitted.

What to Do in Cases of Fraudulent Charges

Fraud moves faster than ordinary billing errors, so your first job is to contain the damage. Think in this order: stop new activity, document what happened, then protect the rest of your identity.

Recognizing signs of fraud

Fraud does not always start with a huge purchase. It often begins with a tiny test transaction, a purchase from a place you have never used, or a burst of digital wallet charges you never approved.

- Small test charge: Treat even a charge under a dollar as a warning sign and review the whole account that day.

- Foreign or out-of-pattern purchase: If it does not match your recent travel or online shopping, lock the card and call the issuer.

- New account activity: If you also see credit inquiries or mail for accounts you never opened, the problem may be identity theft, not just one bad transaction.

- Medical or government identifiers exposed: If your Medicare or Social Security information was part of the breach, widen your response beyond the card and check your credit reports too.

| Card type | Federal liability baseline in the United States | Why speed matters |

|---|---|---|

| Credit card | Unauthorized charges are capped at $50 under federal law | Fast reporting helps block new charges and keeps the case simple |

| Debit card | Loss can rise to $500 if you wait more than 2 business days after learning the card was lost or stolen, and can grow further after 60 days | Money may leave your bank account directly, so delay hurts more |

Reporting fraud to your card issuer

Call the issuer as soon as you see unauthorized charges. Ask it to freeze or replace the card, reverse the suspicious activity, and note your fraud report number.

The FTC says an initial fraud alert on your credit file lasts one year and can be placed by contacting one nationwide credit bureau, while credit freezes are free and have to be placed with each bureau. If the fraud looks bigger than one card, take both steps.

After the call, send the written dispute and keep copies of everything. If the merchant, issuer, or a scammer is still causing trouble, report fraud and scams to the FTC, use the federal identity theft recovery tools, and consider contacting your state Office of the Attorney General.

If a suspicious charge is on a debit card instead of a credit card, move even faster. The liability rules are much less forgiving.

Final Thoughts

A wrong credit card charge feels personal, but the fix is usually very practical. Check the transaction, save your proof, contact the merchant if it makes sense, and send a written billing dispute before the deadline runs out. Keep paying the undisputed part of the bill so your account stays current.

If the charge turns out to be fraud, lock the card, replace it, and protect the rest of your identity fast. Clear records, quick action, and steady follow-up give you the best chance to dispute the charge successfully.

Frequently Asked Questions (FAQs) About Credit Card Charge Dispute

1. How do I start a dispute on a credit card charge?

Check your statement, mark the wrong charge, and gather receipts or emails. Call the merchant first, often they fix it on the spot, it saves time and a headache. If that fails, call your card issuer, report the billing error, file a dispute and send documentation.

2. What proof do I need to win a dispute?

Send receipts, order confirmations, emails, screenshots, and the billing statement that shows the charge, keep copies. Good documentation makes your case clear to customer service and the bank.

3. How long does a chargeback or dispute take?

It can take weeks, sometimes up to 90 days, but many cases close in 30 to 60 days. Timelines vary by issuer, so ask about the expected timeline when you file.

4. Will I have to pay while the dispute is open?

Your card issuer may give a provisional credit, so the charge might be removed from your balance while they investigate. If the dispute loses, the issuer will put the charge back, so keep your proof handy.