The transition into 2026 has confirmed Ireland’s position as the primary bridge for global fintech firms entering the European Economic Area. As the European Union implements its most transformative digital finance regulations in a generation, including MiCA and the latest Payment Services directives, the Central Bank of Ireland (CBI) has emerged as the most sought after regulator for firms requiring a robust passporting license. This strategic dominance is not accidental but the result of a deliberate national policy to marry the technical density of the “Silicon Docks” with the regulatory pedigree of the International Financial Services Centre (IFSC).

Benchmarking Ireland Against EU Fintech Competitors 2026

To understand why global players are prioritizing Dublin over other hubs, we evaluated the current licensing environment across the Eurozone. We analyzed lead times for authorization, the maturity of local innovation sandboxes, and the specific readiness for the Markets in Crypto-Assets (MiCA) framework. Ireland’s ability to offer a predictable path to EU market access remains its most significant competitive advantage.

The following table compares the strategic positioning of Ireland against other major European fintech jurisdictions.

| Feature | Ireland (The Gateway) | Lithuania (The Tech Hub) | Luxembourg (The Institutional Hub) |

| Primary Advantage | Common Law and US Tech Links | High Speed Authorisation | Private Equity and Fund Tech |

| MiCA Readiness | Early Implementer (CASP active) | High Adoption | Moderate Implementation |

| Talent Density | 9/10 (Finance and Tech) | 7/10 (Tech focused) | 8/10 (Finance focused) |

| Language | English (Sole Native Post-Brexit) | Dual Language | Multilingual |

| Regulatory Tone | Pragmatic and Supportive | Innovative and Fast | Formal and Structured |

10 Reasons Ireland Is the EU’s Preferred Fintech Licensing Gateway

The convergence of regulatory maturity and geographic positioning has made Ireland the definitive choice for firms navigating the 2026 EU financial landscape. These ten factors represent the core reasons why the jurisdiction continues to attract the world’s leading digital finance innovators.

1. Comprehensive MiCA CASP Authorization

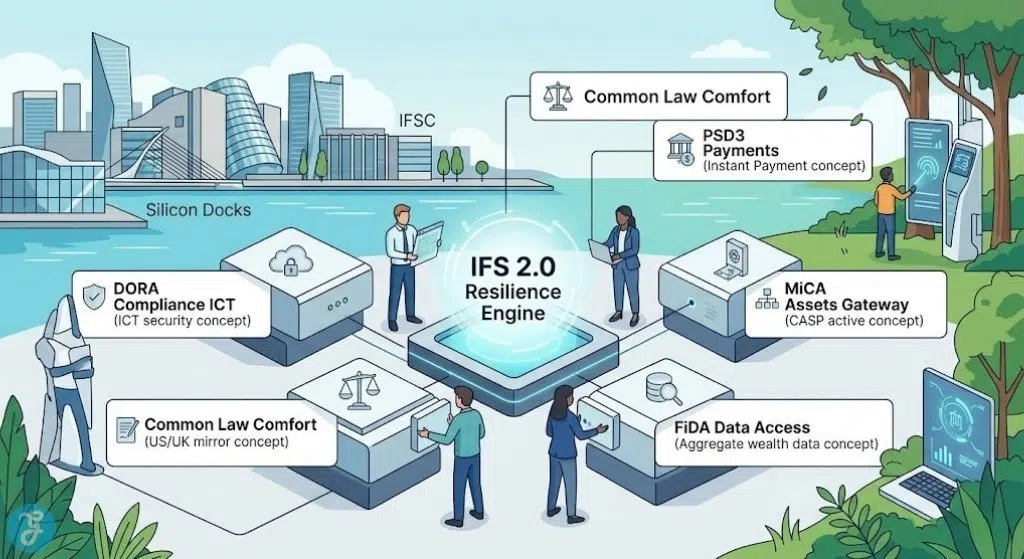

As of early 2025, Ireland was among the first EU nations to fully open applications for Crypto Asset Service Providers (CASPs) under the MiCA framework. For firms dealing in digital assets, getting an Irish license is a “golden ticket” because it allows them to legally provide services to all 27 EU member states through a single regulatory relationship. The Central Bank of Ireland has already integrated these requirements into its existing supervisory structure, providing a clear and reliable roadmap for authorization.

Best for:

-

Cryptocurrency exchanges and digital wallet providers seeking immediate EU wide legitimacy.

Why We Chose It:

-

Ireland is a first mover in implementing the full MiCA framework.

-

The CASP license provides a stable legal environment for high growth tech firms.

-

It eliminates the need for multiple licenses across different European countries.

Things to consider:

-

The transitional period for older VASP registrations ends in late 2025.

2. The CBI Innovation Sandbox Programme 2026

The Central Bank of Ireland has significantly expanded its Innovation Sandbox for the 2026 cycle. This programme allows fintechs to test new products, such as agentic AI financial assistants or tokenized payment systems, in a controlled environment with direct regulatory oversight. Unlike more rigid jurisdictions, the Irish sandbox provides a dedicated relationship manager who helps firms navigate the “grey areas” of emerging technology before they commit to a full license application.

Best for:

-

Startups and scaling firms with highly innovative or “untested” financial products.

Why We Chose It:

-

It provides a low risk environment to test the safety of emerging AI and blockchain tools.

-

The 2026 programme includes specific workstreams for frictionless money movement.

-

It fosters a collaborative rather than adversarial relationship with the regulator.

Things to consider:

-

Admission to the sandbox is competitive and based on the potential impact of the innovation.

3. English Language and Common Law System

Following Brexit, Ireland remains the only native English speaking country in the Eurozone that operates under a Common Law legal system. For US and UK based fintech firms, this provides an unparalleled level of cultural and legal comfort. Contracts and regulatory filings do not require translation, and the legal principles regarding property and finance are familiar to global investors. This reduces the administrative “friction” of expansion and lowers the legal costs associated with entering the EU.

Best for:

-

Transatlantic firms and UK neobanks looking for a seamless “mirror” of their existing legal structures.

Why We Chose It:

-

It is the most accessible entry point for firms from the Anglosphere.

-

Common Law provides a flexible framework for innovative financial instruments.

-

It avoids the linguistic barriers found in other major European finance hubs.

Things to consider:

-

While the language is familiar, the specific EU directives differ from UK and US domestic laws.

4. Advanced Preparation for PSD3 and PSR

Ireland has positioned itself at the forefront of the transition from PSD2 to the newer Payment Services Directive 3 (PSD3) and Payment Services Regulation (PSR). The Irish regulator is actively helping firms prepare for the enhanced fraud prevention and open banking requirements that take effect in 2026. This forward looking stance ensures that Irish licensed firms are not caught off guard by the new rules regarding instant payments and data sharing.

Best for:

-

Payment service providers (PSPs) and neobanks who prioritize long term regulatory compliance.

Why We Chose It:

-

Proactive guidance from the CBI reduces the risk of “regulatory shock.“

-

It ensures a level playing field between traditional banks and non-bank PSPs.

-

Ireland’s infrastructure is already optimized for the 2025 instant payment mandates.

Things to consider:

-

Compliance requirements for fraud protection are significantly higher under the new PSR rules.

5. The “Silicon Docks” Tech and Finance Crossover

Dublin’s Silicon Docks district is home to the European headquarters of nearly every major global tech company, from Google to Stripe. This proximity has created a unique talent ecosystem where financial experts understand cloud architecture and developers understand regulatory reporting. In 2026, this crossover is vital for building “AI first” fintech products that require deep expertise in both cybersecurity and financial stability.

Best for:

-

Firms that require a high density of senior engineering and compliance talent in the same location.

Why We Chose It:

-

The presence of world leading tech firms provides a constant influx of global expertise.

-

It fosters a culture of innovation that is rare in more traditional finance centers.

-

The local ecosystem supports a wide range of regtech and cybersecurity partners.

Things to consider:

-

High demand for talent makes recruitment competitive and increases operational costs.

6. Proximity to US Markets and Timezone Advantages

Ireland acts as the perfect temporal bridge between the US East Coast and the rest of the European Union. Its geographic location allows firms to manage their European operations during the late afternoon in New York, facilitating real time collaboration with US parent companies. This advantage has made Dublin the preferred “operations hub” for over 430 international financial institutions that require 24/7 global coverage.

Best for:

-

US based fintechs that want to maintain close operational control over their European expansion.

Why We Chose It:

-

The five hour time difference with New York allows for significant overlapping work hours.

-

Strategic location as a gateway for transatlantic data and financial services.

-

Unrivalled access to both the EU Single Market and global financial networks.

Things to consider:

-

High office rents in Dublin’s central business districts should be factored into the expansion budget.

7. Stable Political and Pro-Business Environment

In an era of shifting global trade pacts and political volatility, Ireland has remained a pillar of stability within the EU. The government’s “Ireland for Finance” strategy 2026-2030 has secured cross party support for maintaining a competitive tax regime and high regulatory standards. This predictability is a primary ranking factor for boards of directors who are wary of the “jurisdiction risk” found in less stable markets.

Best for:

-

Large scale institutional players that require a multi decade commitment to a single jurisdiction.

Why We Chose It:

-

Long term government commitment to the growth of the financial services sector.

-

Consistent and transparent tax policies, including R&D tax credits for fintech innovation.

-

Strong “Value-Chain Advancement” metrics that show the health of the local economy.

Things to consider:

-

Discussions around corporate tax reform at the OECD level are ongoing but largely manageable.

8. The Rise of “IFS 2.0” and Digital Finance Hubs

The Irish government and industry groups are currently developing “IFS 2.0,” which involves the creation of a dedicated physical hub for fintech startups in Dublin. Inspired by projects like France’s Station F, this hub will provide structured engagements between indigenous startups and large established firms. This centralized ecosystem ensures that new arrivals in Ireland can quickly network with the partners and investors they need to scale.

Best for:

-

Early stage fintechs that need access to established banking partners and venture capital.

Why We Chose It:

-

It provides a “one-stop shop” for fintech firms at all stages of development.

-

The focus is on building domestic capacity in critical areas like AI and digital finance.

-

It facilitates the “embedded finance” trend by linking startups with major insurers and wealth managers.

Things to consider:

-

Firms must actively engage with local industry groups like Ibec to maximize these networking opportunities.

9. Financial Data Access (FiDA) Readiness

The new Financial Data Access (FiDA) framework is set to expand consent based data sharing far beyond the original “Open Banking” rules. Ireland is leading the way in establishing the digital public infrastructure required for responsible data sharing across savings, investments, and insurance. Fintechs that use an Irish license are better positioned to build holistic wealth management products that can leverage this wider data pool across the entire EU.

Best for:

-

Personal finance managers and investment platforms that rely on aggregate data.

Why We Chose It:

-

Ireland’s tech infrastructure is already built for high volume API data sharing.

-

Strong focus on consent management and data governance from the local regulator.

-

It enables the creation of more personalized and inclusive financial products.

Things to consider:

-

Firms must meet strict DORA (Digital Operational Resilience Act) standards for ICT security.

10. Superior EU Passporting Efficiency

Ultimately, the most practical reason for choosing Ireland is the “efficiency of the passport.” Once authorized by the CBI, a fintech can offer its services throughout the European Economic Area without ever needing another license. Ireland’s reputation as a “high standard” regulator means that other EU nations trust the Irish authorization, leading to fewer administrative hurdles when marketing services in major markets like Germany, France, or Spain.

Best for:

-

Scalable digital platforms that intend to serve tens of millions of customers across the EU.

Why We Chose It:

-

The Irish license is recognized and respected by regulators across the globe.

-

It provides the most direct and reliable path to the EU Single Market.

-

Regulatory processes are harmonized with broader EU standards for ease of operation.

Things to consider:

-

The initial authorization process is rigorous and requires a significant presence in Ireland.

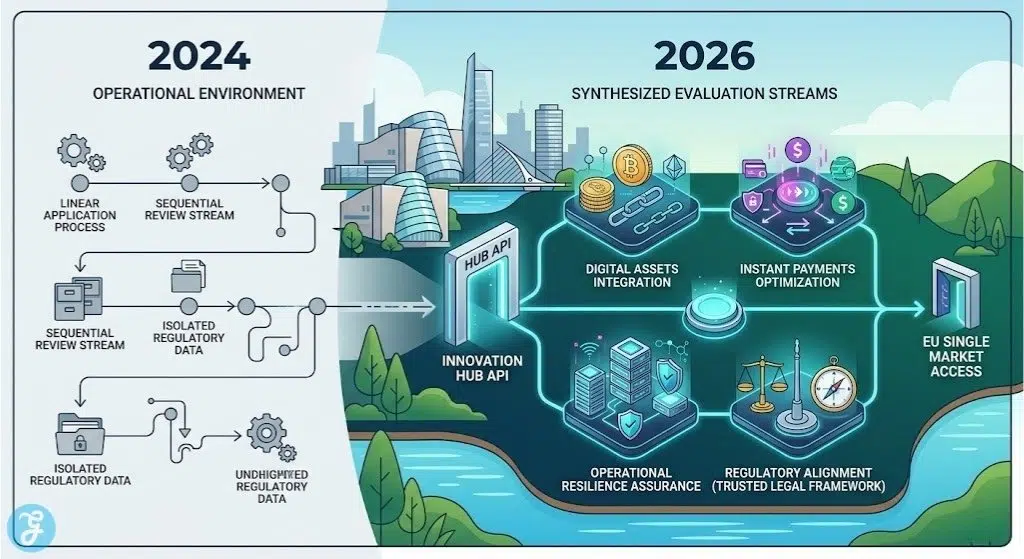

Strategic Roadmap for Irish Fintech Authorization

Securing an EU license is a significant undertaking that requires careful planning and a local presence. The following table provides a high level checklist for firms entering the Irish market in 2026.

This data represents the standard requirements for a firm seeking CASP or PSP authorization this year.

| Phase | Strategic Requirement | Key Stakeholder |

| Preparation | Legal assessment of the license scope (MiCA vs PSD3) | Central Bank of Ireland (CBI) |

| Incorporation | Registration of an Irish legal entity with local directors | Companies Registration Office |

| Governance | Hiring of resident “Pre-Approval Function” (PCF) roles | Local Executive Search |

| Operational | Implementation of ICT security under DORA standards | Chief Information Officer |

| Submission | Comprehensive application via the CBI portal | Legal and Compliance Team |

Our Top 3 Critical Success Factors and Why?

While all ten reasons make Ireland a powerful gateway, these three are the most critical for a successful 2026 launch.

-

MiCA Implementation Speed: Being licensed early for crypto assets is the only way to capture the surging European digital asset market before competitors.

-

Regulatory Proactivity: Engaging with the CBI Innovation Hub early ensures that your business model is aligned with the latest EU directives.

-

Local Talent Integration: Building a local team that understands the Irish tech and finance culture is vital for long term operational success.

How to Audit Your EU Expansion Readiness?

Before you begin the formal application process in Dublin, you should perform a thorough internal audit to ensure your firm is ready for the rigors of the Central Bank of Ireland’s oversight.

-

Review Your PCF Candidates: Ensure you have identified high quality resident directors who meet the “fitness and probity” standards of the CBI.

-

Test Your DORA Compliance: Audit your ICT systems to ensure they can withstand the resilience testing required under the Digital Operational Resilience Act.

-

Map Your EU Footprint: Decide whether you will use the Irish license primarily for “passporting” or if you intend to build a full local operations hub.

-

Assess Your Capital Reserves: Verify that your firm meets the specific minimum capital requirements for the license type you are seeking.

The following table can help you decide which regulatory path to take based on your current product offering.

| Pursue a CASP License if… | Pursue a PSP/EMI License if… |

| Your primary business involves the exchange or custody of crypto assets. | Your primary business involves payments, transfers, or e-money issuance. |

| You want to utilize the MiCA transitional regime in 2025. | You are preparing for the transition to PSD3 and PSR. |

| You are targeting the institutional and retail digital asset market. | You are building a consumer neobank or business payment platform. |

The Final Fintech Licensing Checklist

-

Schedule a preliminary meeting with the CBI Innovation Hub to discuss your business model.

-

Secure a physical office address within the International Financial Services Centre or Silicon Docks.

-

Appoint a qualified Irish resident Head of Compliance and Head of Anti-Money Laundering.

-

Finalize your 2026-2028 business plan including three year financial projections for the Irish entity.

-

Register for the CBI Innovation Sandbox if your product uses emerging AI or blockchain tech.

Securing the Future of Global Digital Finance

The selection of Ireland as a licensing base is more than just a regulatory choice. It is a strategic commitment to being at the center of the world’s most advanced digital finance ecosystem. By utilizing the EU’s Preferred Fintech Licensing Gateway, firms are not just getting a license to operate; they are gaining a seat at the table where the future of European finance is being designed. As the EU continues to lead the world in digital regulation, the firms that choose Ireland in 2026 will be the ones that define the global standard for innovation and trust.

Frequently Asked Questions (FAQs) on EU’s Preferred Fintech Licensing Gateway

How long does it take to get a fintech license in Ireland?

Answer: The timeline varies depending on the complexity of the firm, but generally, the Central Bank of Ireland aims to process complete applications within 6 to 12 months.

Do I need to have a physical office in Ireland to get a license?

Answer: Yes, the regulator requires “substance” in the jurisdiction, meaning you must have a physical office and key decision making staff based in Ireland.

Can an Irish fintech license be used in Switzerland or the UK?

Answer: An Irish license provides “passporting” rights across the 27 EU member states and the EEA, but separate arrangements are required for non EU countries like the UK or Switzerland.

What is the minimum capital requirement for an Irish EMI license?

Answer: The initial capital requirement for an Electronic Money Institution (EMI) is typically 350,000 Euro, though the CBI may require more based on your specific business risk profile.

Can I use my existing US compliance policies for the Irish regulator?

Answer: While your US policies provide a good foundation, they must be heavily localized to comply with specific Irish AML laws and EU directives like MiCA and PSD3.