Choosing the right credit card can feel overwhelming when bills stack up and options seem endless. Many people spend heavily on travel or groceries but end up with cards that offer low rewards and high fees.

This mismatch often leads to frustration—like forcing a solution that doesn’t fit real financial needs. As a result, users may miss out on valuable benefits or fall into unnecessary debt by selecting the wrong card.

To choose the right credit card, it’s essential to focus on spending habits, credit score, and key features such as rewards programs, interest rates, and annual fees. Reviewing credit reports through platforms like Experian or CreditKarma.com and comparing options like the Chase Sapphire Preferred® Card for travel rewards or the Wells Fargo Active Cash® Card for cashback can make the process easier.

A smart comparison helps identify the best fit, maximize rewards, and avoid costly credit card mistakes.

Know Your Financial Goals and Spending Habits

Start by looking at your daily life. Think about how you spend money each month, like on groceries or travel. This ties right into your personal finance picture. The best credit card for you depends on three key factors: your spending habits, credit profile, and what features matter most to you.

Understanding your financial needs is a crucial first step in determining which type of credit card is right for you. Rewards programs are an important feature to consider when selecting a credit card that matches your lifestyle.

Your wallet as a toolbox, folks, you want the right tool for the job, not a hammer when you need a screwdriver.

Knowing your spending habits helps you pick a card that rewards your lifestyle, says Emily Sherman from NerdWallet.

Credit limit and security features are more factors to evaluate when choosing the right credit card for your financial needs and lifestyle. Do you chase rewards cards for that sweet cash back? Or maybe you eye low-interest options to tackle debt.

A friend once grabbed a rewards card without checking habits, ended up with points on stuff he never buys, what a bummer. Match card features to your goals, and you’ll avoid that trap.

Talk to yourself like, Do I splurge on dining out with a Capital One Savor Cash Rewards Credit Card in mind?

Check Your Credit Score

Your credit score acts like a financial report card, showing lenders how reliable you are with money. Pull your report for free from AnnualCreditReport.com, and look at scores from Equifax or TransUnion to spot any issues before you pick a card.

How to check and interpret your credit score

Credit scores play a big role in picking the right credit card. They shape what options you qualify for, like low-interest cards or rewards programs.

- Head to annualcreditreport.com for a free credit report from the three main credit bureaus, Equifax, TransUnion, and Experian, which you can get once a year without any cost. This site lets you pull reports that show your payment history, debts, and other details that feed into FICO scores. Think of it as peeking under the hood of your financial engine, spotting any red flags early.

- Contact credit unions or services like CardMatch™ to access your FICO scores, often for free or a small fee, and compare them against benchmarks where 670 or above opens doors to better credit card options. Scores below that might point you toward secured credit cards to build credit. It’s like checking your team’s scorecard before the big game, you know where you stand.

- Interpret your score by looking at factors like on-time payments, which make up 35% of FICO scores, and credit utilization, aiming to keep it under 30% for a boost. High scores mean lower APR offers, while low ones suggest focusing on debt management first. Picture it as a report card, good grades get you perks like cash back credit cards.

- Use tools from the Ohio Credit Union League or Firefighters Community Credit Union to understand score ranges, where excellent credit above 800 qualifies you for top cards like the Chase Freedom Unlimited® or Discover it® Cash Back. These groups offer tips on improving scores through consistent habits. It’s a bit like training for a marathon, steady effort pays off in better credit card features.

- Review promotional offers and introductory offers tied to your score, such as 0% APR on balance transfers with cards like the Citi® Diamond Preferred® Card, which suit those with solid credit profiles. Low scores might limit you to secured credit cards, but improving them unlocks rewards like travel perks on the Capital One Venture Rewards Credit Card. Think of your score as a key, it opens doors to credit card benefits that match your lifestyle.

- Factor in expert advice from folks like Nouri Zarrugh, who stresses that understanding your credit profile helps in comparing credit card types and avoiding high fees and charges. A strong score supports goals like earning cash back or managing debt with low-interest credit cards. It’s akin to having a financial map, guiding you to the best path without detours.

Importance of credit score in selecting a credit card

Your credit score acts like a financial report card, showing lenders how you handle money. It shapes which cards you qualify for, from rewards-packed options to those that build up shaky credit.

Think of it this way, a strong score, say above 700, unlocks premium perks like cash back or travel points. Sites like The Motley Fool offer solid credit card comparison tools to match your score with top picks.

You check it for free through services on a secure server, spotting any issues fast.

Folks with limited or damaged credit often grab secured cards to improve their standing, while others chase low-interest deals to cut debt. This score ties straight into your credit profile, one of three key factors for finding the best fit alongside spending habits and must-have features.

Consumers pick cards that save on interest or earn rewards based on their score’s strength. Low scores might mean starting small, but steady payments boost it over time, opening better doors.

Identify Your Credit Card Needs

Think about what perks excite you most, like earning points on everyday buys or getting money back on gas and groceries. Ask yourself if slashing interest rates matters more, or if shifting old debts to a fresh card could ease your wallet’s load, sparking smarter choices ahead.

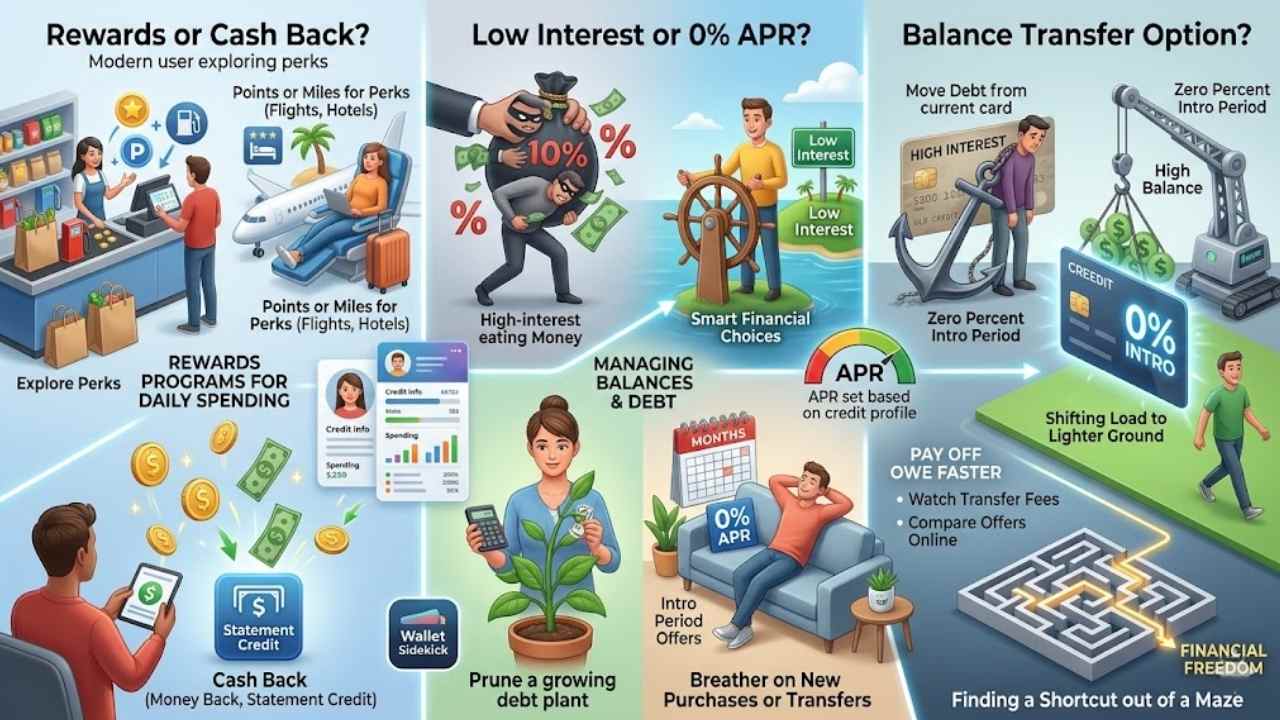

Do you want rewards or cash back?

Rewards programs can make a big difference in your daily spending. You earn points or miles on purchases, like groceries or gas. These turn into perks, such as free flights or hotel stays.

Cash back gives you money right back, often as a statement credit. Pick what fits your life, you know, if travel excites you or if straight savings feel better.

Rewards programs are an important feature to consider when selecting a credit card that matches your lifestyle.

Consumers choose cards that earn rewards to save on interest or build credit. Your spending habits guide this choice, along with your credit profile and key features. Think of it like picking a sidekick for your wallet; one that boosts your fun or pads your pocket.

Cards with these options help if you want to improve limited credit too.

Are you looking for low interest or 0% APR?

Think about your monthly balances. Do you carry them over often? High interest can eat into your wallet like a sneaky thief. Pick a card with a low interest rate if you aim to cut down debt.

This move saves you money in the long run. Cards with 0% APR offers give you a breather, sometimes for months, on new purchases or transfers.

Go for the lowest APR you can snag based on your credit. It fits right into smart strategies for picking cards. Low rates shine when balances run high, helping you pay off what you owe without extra pain.

Match this to your habits, and you’ll feel in control, like steering your own financial ship.

Do you need a balance transfer option?

You carry a high balance on your current card, and debt weighs you down like an anchor. A balance transfer option lets you move that debt to a new card with a low interest rate, often zero percent for an intro period.

This move saves money on interest, helping you pay off what you owe faster. Shifting your load to lighter ground, where fees don’t pile up as quick.

Look for cards that fit if you aim to lower debt. They come with low APR, so you qualify for the best deal possible. Watch those transfer fees, though, like finance charges that sneak in.

Compare offers online, and pick one that matches your push to cut costs. It’s like finding a shortcut out of a financial maze, making every payment count more.

Compare Different Types of Credit Cards

Picking the perfect plastic pal means sizing up options that match your daily grind, like cards that pile on points for gas and groceries or ones that slash rates for big buys, so dig into these picks below to snag the winner for your wallet.

Rewards credit cards

Rewards credit cards give you points, cash back, or miles for your everyday buys. Picture swiping your card at the grocery store and earning extra dough, like a little bonus for grabbing milk and bread.

These cards shine if you spend a lot on gas, dining out, or travel. They match your lifestyle by rewarding what you already do, turning routine shopping into perks. Folks with solid credit profiles often snag the best ones, as they tie into your spending habits and what features you value most.

You can pick rewards cards that earn big on categories like groceries or flights. Consumers opt for them to rack up benefits, unlike cards that just build credit or cut interest costs.

Think of it as a smart side kick in your wallet, helping you save while you spend. Rewards programs stand out as a key feature, especially if your habits lean toward frequent purchases.

Just check the terms to avoid surprises, and compare offers to find one that fits without extra fees.

Travel credit cards

Travel credit cards shine for folks who love hitting the road or jetting off to new spots. They dish out points or miles on purchases like flights, hotels, and dining out. You book a trip to Paris, and your card racks up bonus rewards that cut costs on your next adventure.

Folks with strong credit profiles snag the best perks, like free checked bags or airport lounge access. These cards fit lifestyles full of wanderlust, turning everyday spending into dream vacations.

Compare offers to match your habits; some team up with airlines like Delta or United for extra miles.

You chase low fees with these cards, especially if you’re new to them. Skip high annual charges by picking ones with no fees at first. Watch for cash advance fees that sneak up. Aim for cards that reward your travel style, whether you fly often or road-trip across states.

Your spending habits guide the choice, so think about how you use money on the go. Rewards programs boost value, lining up with what excites you most about exploring.

Secured credit cards

Secured credit cards act like a safety net for folks rebuilding their credit. You put down a cash deposit, and that sets your credit limit right away. People with limited or damaged credit often pick these to boost their scores over time.

They fit well if rewards or low interest aren’t your top goals yet. Think of it as training wheels for your finances, helping you ride steady without big falls.

Many secured cards skip the annual fee, which makes them smart for starters. Watch those finance charges and cash advance fees, though; they can sneak up on you. Your spending habits and credit profile guide the choice here.

Pair this with cards that earn rewards or save on interest later, once your score improves. Security features add extra peace of mind, too.

Low-interest credit cards

Low-interest credit cards shine for folks who carry balances month to month. They cut down on those pesky interest costs, like a trusty shield against growing debt. You juggle bills, and bam, a card with rock-bottom APR saves you cash over time.

Aim for the lowest Annual Percentage Rate you qualify for; it acts as your secret weapon in the debt battle. Folks with high balances find these cards a real lifesaver, helping lower debt without the extra sting.

Watch for sneaky fees that pop up, such as finance charges or cash advance costs. Consumers pick these to save on interest, especially if credit needs a boost from limited or damaged scores.

Rewards might take a back seat here, but hey, who needs bells and whistles when steady savings keep your wallet happy? Cards with no annual fee suit first-timers, making the choice feel like a walk in the park.

Evaluate Rates, Fees, and Terms

Pick a credit card with eyes wide open, folks, by sizing up the interest rate that hits your balance each month. Spot those yearly costs and sneaky extra charges right away, like a detective on a budget hunt, to dodge any wallet woes down the line.

Annual percentage rate (APR)

APR stands for annual percentage rate, and it shows the cost of borrowing money on your credit card each year. You pay this interest on unpaid balances. Aim for the lowest APR you can qualify for, folks, because it saves you cash in the long run.

Think of it like shopping for a car loan; a lower rate means less hassle on your wallet. If you carry a high balance often, and you’re chipping away at debt, grab a card with a low interest rate to ease the burden.

That strategy fits right into your goal of lowering what you owe.

Watch out for finance charges and cash advance fees too, as they add up fast when you evaluate options. These extras can sneak up like unexpected guests at a party, boosting your total costs.

Credit card companies list APR clearly in their terms, so read them closely. Your credit score plays a big role here; a strong one unlocks better rates. Pair this with your spending habits, and you find a card that matches your life without breaking the bank.

Credit cards often come with annual fees that hit your wallet each year. Pick one with no annual fee if you’re grabbing your first card, as it keeps things simple and saves money right away.

These fees can add up, like a sneaky tax on your spending. Watch out for hidden charges too, folks. Finance charges pile on when you carry a balance, and cash advance fees bite hard if you pull money from an ATM.

Spot these early to avoid nasty surprises, like finding extra pickles on your burger when you hate them.

Issuers bury these costs in the fine print, so read it like a detective novel. Compare offers side by side to dodge the traps. Low fees mean more cash in your pocket for what you love, whether that’s travel or treats.

Talk to friends about their card woes; you might hear a funny story about a fee that snuck up like a bad blind date. Choose wisely, and your card fits your life without the extra baggage.

Research and Compare Credit Card Offers

You know, finding the perfect card feels like hunting for treasure, so grab your laptop and check out sites like Credit Karma or NerdWallet to line up deals fast. Watch those intro bonuses and zero-interest periods, they might just turn a good pick into a great one, if you dig a bit deeper.

Online comparison tools

Online tools make comparing credit cards a breeze. You jump online, enter your details, and sites like Credit Karma or NerdWallet spit out options side by side. They show you APRs, annual fees, and rewards programs all in one spot.

This saves time, like skipping a wild goose chase through bank websites. Picture yourself spotting a cash back card that fits your grocery runs perfectly, without the headache.

These tools highlight promotional offers, too, such as 0% intro APR for balance transfers. They help you dodge higher fees by revealing hidden charges upfront. Folks often find low-interest cards this way, matching their debt payoff plans.

One user I know laughed about discovering a travel card with no foreign transaction fees, right when planning a trip abroad. It feels empowering, doesn’t it, to grab the best deal with just a few clicks.

Understanding promotional offers

Credit card companies often roll out promotional offers to attract new users, like zero percent APR for the first year or bonus rewards points after you spend a certain amount. These deals sound tempting, right? Imagine you’re eyeing a card with a sweet sign-up bonus that matches your love for travel perks.

Banks design these to hook you, but smart shoppers dig deeper. They check if the offer aligns with their spending habits and financial goals. For instance, if you carry a balance, grab that low-interest promo to slash debt faster.

Rewards programs shine here too, offering cash back or points that fit your lifestyle, say, extra miles for frequent flyers.

Spot the fine print in these promotions, folks, because hidden fees can sneak up like a plot twist in your favorite show. Credit issuers might waive annual fees for the first year, then charge them later, so compare offers side by side to dodge those surprises.

Aim for the lowest APR you qualify for, especially if high balances are your norm. Secured cards sometimes come with intro deals to build credit, while low-interest options help if debt reduction tops your list.

Tools like comparison websites let you filter these promos by your credit score and needs, making the hunt feel less like a chore. Keep an eye on finance charges and cash advance fees that could eat into your savings.

Tips for Applying for the Right Credit Card

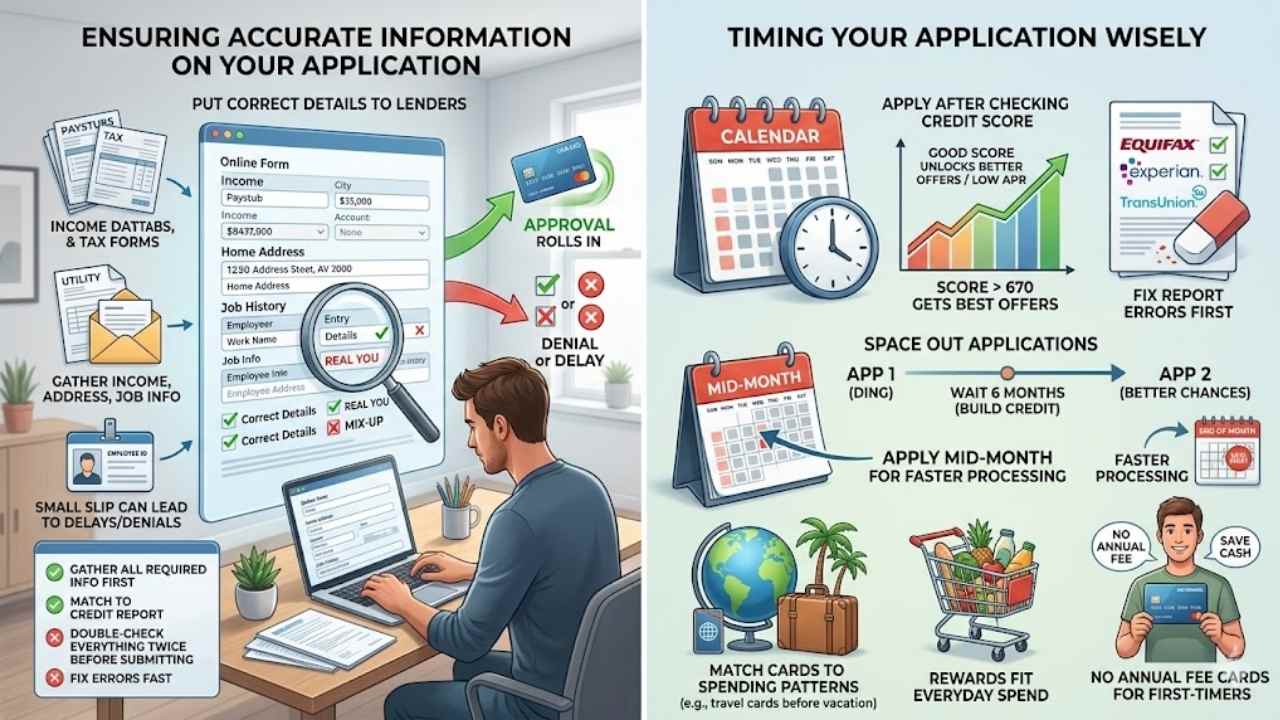

Double-check every detail on your application form, from your home address to your yearly salary, to avoid any slip-ups that could tank your approval odds. Pick the perfect moment to submit, say right after boosting your credit report with on-time payments, and watch those offers roll in—curious for more tricks?

Ensuring accurate information on your application

Put the right details on your credit card application. You want lenders to see the real you, not some mix-up that could tank your chances. Think of it like telling a story where every fact lines up, no plot holes.

Gather your income data, address history, and job info first. Make sure it matches what shows on your credit report. A small slip, like a wrong digit in your Social Security number, can lead to denials or delays.

Check everything twice before you hit submit. Lenders use this info to check your credit profile and decide on approval. If you spot errors, fix them fast. This step ties into your financial goals, like aiming for low APR or rewards that fit your spending habits.

Applying with spot-on details; it’s like giving yourself a head start in the race for the best card.

Timing your application wisely

You time your credit card application to boost approval odds. Apply after you check your credit score, as lenders review it closely. Scores above 670 often unlock better offers, like low APR cards.

Fix errors on your report first, pulling from Equifax or other major bureaus. This step aligns with your financial goals, matching habits to rewards or low-interest options.

Space out applications to avoid dings on your score from hard inquiries. Wait six months between tries if denied, giving time to build credit. Apply mid-month, when lenders might process faster, dodging end-of-month rushes.

Tie this to your spending patterns; for example, seek travel cards before vacation season. Cards with no annual fee suit first-timers, saving cash while you compare rates and fees.

Final Words

You’ve learned to match credit cards with your spending habits, check your credit score for better options, and pick rewards or low-interest features that fit your life. These steps keep things simple, so you grab the right card without wasting time or cash.

Smart choices like this boost your finances, cut down debt, and rack up perks that make daily buys more fun. Head to sites like Credit Karma or NerdWallet for quick comparisons and fresh deals.

Switched to a cash-back card after tracking my grocery runs, and it saved me hundreds, talk about a game changer. Go ahead, apply these tips today, and watch your wallet thank you.

Frequently Asked Questions (FAQs) About Choosing the Right Credit Card

1. How do I pick a credit card that fits my daily habits?

Think about your spending, like if you travel a lot or eat out often, and match it to cards with rewards for those things. It’s like finding a shoe that fits just right, you know? Don’t forget to check the fees, they can sneak up on you.

2. What if I’m always on the go, does that change my credit card choice?

Yes, a travel rewards card might be your best buddy for miles and perks.

Watch out for high interest rates, they can bite like a bad investment. Annual fees add up too, so compare them side by side. And late payment penalties? Ouch, avoid those by paying on time, every time.

4. How can I compare credit cards without getting overwhelmed?

Start with your lifestyle needs, then look at APR and bonuses online. Tools like comparison sites make it easy, almost like chatting with a friend for advice.