Finland continues to stand out in the Nordic region for its structured approach to investment income, which is particularly relevant as we move through the 2026 fiscal year. For anyone managing assets in this landscape, understanding the mechanics of the Finland Capital Gains Tax is not just about compliance but also about identifying opportunities for significant tax savings.

This guide provides a detailed look at the current rules to help you navigate your financial obligations with precision.

How We Selected Our 12 Best Finland Capital Gains Tax Facts

Our selection process involved a deep dive into the latest 2026 tax code updates provided by the Finnish Tax Administration (Vero). We prioritized facts that have the highest impact on individual net returns and those that apply to the widest range of common investment scenarios. Each fact was chosen based on its relevance to modern trading habits, legislative changes, and its potential for providing legitimate tax relief through exemptions.

A Detailed Guide to the 12 Finland Capital Gains Tax Insights

The following points represent the core of the Finnish capital gains system. Understanding these will give you a clear roadmap for reporting and planning your investment activities throughout the year.

1. The Two-Tiered Progressive Rate

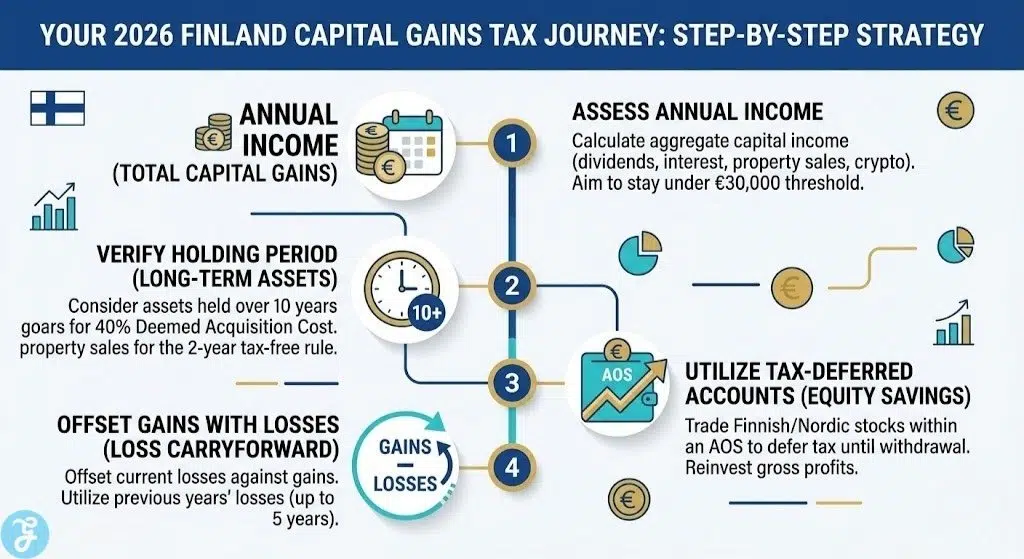

The Finnish system for capital income is not a simple flat rate but a two-step progressive model. For 2026, the base rate remains 30% for all taxable capital income up to €30,000. If your total capital income for the year exceeds this amount, the portion above the threshold is taxed at 34%.

Best for: investors with varying levels of annual capital income.

Why We Chose It:

-

It is the foundational rule for almost all asset disposals in Finland.

-

It requires careful timing of sales to avoid unnecessary 34% bracket exposure.

-

It applies to the aggregate of all your capital income, including rents and dividends.

Things to consider:

-

Calculating your total expected income before year-end is crucial for stay under the higher bracket.

2. Primary Residence Tax-Free Status

Selling your home in Finland can be entirely tax-exempt under specific conditions. To qualify, you must have owned the property and used it as your permanent residence for a continuous period of at least two years.

Best for: homeowners and people relocating within Finland.

Why We Chose It:

-

This represents the most significant tax-free gain available to the public.

-

It supports social and geographic mobility for the workforce.

Things to consider:

-

Even a short break in residency can restart the two-year clock.

3. The €1,000 Micro-Transaction Exemption

Finland offers a “de minimis” rule to simplify the lives of casual sellers. If the total sales prices of all your assets sold during the calendar year do not exceed €1,000, any profit made is completely tax-exempt.

Best for: casual sellers of household items or minor stock holdings.

Why We Chose It:

-

It removes the burden of reporting very small profits.

-

It provides a clear threshold for non-professional investment activity.

Things to consider:

-

This limit applies to the total sales price (selling price), not the profit (gain).

4. Standard Deemed Acquisition Cost

The “deemed acquisition cost” is a unique Finnish tool that allows you to deduct a percentage of the sale price instead of the actual purchase price. If you have owned an asset for less than 10 years, you can deduct 20% of the sale price as your “cost.”

Best for: assets that have seen extreme growth or where records are lost.

Why We Chose It:

-

It acts as a “floor” for your tax deductions.

-

It simplifies the tax process for high-growth assets.

Things to consider:

-

You cannot deduct additional selling expenses like broker fees if you choose this method.

5. Long-Term Holding Deemed Cost

For assets held for 10 years or more, the deemed acquisition cost increases significantly. In these cases, you can deduct 40% of the sale price as the cost, which drastically reduces the taxable portion of the gain.

Best for: long-term investors and those inheriting legacy assets.

Why We Chose It:

-

It rewards long-term holding and financial stability.

-

It is often more beneficial than using the actual purchase price for older assets.

Things to consider:

-

The 10-year clock starts from the date of the original acquisition or inheritance.

6. Partial Exemption for Listed Dividends

Dividends from companies listed on a public stock exchange receive a 15% tax exemption. This means only 85% of the dividend is taxed as capital income, resulting in an effective tax rate of either 25.5% or 28.9%.

Best for: income-oriented stock market investors.

Why We Chose It:

-

It encourages investment in publicly traded companies.

-

It aligns Finnish policy with broader European investment incentives.

Things to consider:

-

Dividends from non-listed companies have an entirely different and more complex set of rules.

7. Five-Year Loss Deduction Window

Investment losses are not permanent if you play your cards right. In Finland, you can deduct capital losses from your capital gains in the same year, and if there is a remaining loss, you can carry it forward for five subsequent years.

Best for: active traders and those managing a volatile portfolio.

Why We Chose It:

-

It provides a vital safety net for investment risks.

-

It allows for multi-year tax planning and recovery.

Things to consider:

-

Losses must be reported in the year they occur to be eligible for future carryforwards.

8. 30% Withholding on Bank Interest

Unlike other capital income, interest earned on bank deposits in Finland is subject to a flat 30% “tax at source.” This is usually handled automatically by your bank, so you do not need to report it on your tax return.

Best for: conservative savers who prefer automated compliance.

Why We Chose It:

-

It is one of the few truly “flat” components of the system.

-

It offers the highest level of administrative simplicity for the taxpayer.

Things to consider:

-

This flat rate applies regardless of whether your other capital income is over €30,000.

9. Equity Savings Account (AOS) Benefits

The Equity Savings Account is a powerful vehicle that allows for tax-deferred growth. Within this account, you can buy and sell stocks without paying capital gains tax until you decide to withdraw funds from the account.

Best for: retail investors looking to maximize compound growth.

Why We Chose It:

-

It is the most modern and tax-efficient way to trade stocks in Finland.

-

It allows for a “gross” reinvestment of profits.

Things to consider:

- Deposits into the account are capped at €100,000 as of 2026.

10. New 2026 Crypto Reporting Standards

The 2026 tax year brings stricter transparency for digital assets. Crypto service providers are now required to share more data with the tax authorities, making it essential for users to report every trade, including crypto-to-crypto exchanges.

Best for: cryptocurrency traders and digital asset holders.

Why We Chose It:

-

This is the most significant regulatory change for the 2026 fiscal year.

-

It emphasizes the move toward a fully transparent digital economy.

Things to consider:

-

High-volume traders should use specialized software to track FIFO (First-In, First-Out) calculations.

11. Foreign Tax Credit Integration

Finland actively works to prevent double taxation for its residents through a credit system. If you pay tax on a capital gain in another country, that amount can typically be deducted from your Finnish tax liability for that same income.

Best for: expats and investors with international portfolios.

Why We Chose It:

-

It protects global investors from being penalized for cross-border activity.

-

It follows international tax treaty standards.

Things to consider:

-

You must provide proof of tax paid abroad to claim the credit.

12. Tax on Indirect Finnish Real Estate Gains

Non-residents are now subject to Finnish tax if they sell shares in a foreign entity that primarily holds Finnish real estate. This rule ensures that profits derived from Finnish land and buildings remain within the Finnish tax net.

Best for: international real estate investors and corporate funds.

Why We Chose It:

-

It addresses complex indirect ownership structures.

-

It ensures fairness between resident and non-resident property owners.

Things to consider:

-

This rule is often triggered if more than 50% of the entity’s value comes from Finnish property.

An Overview Of 12 Finland Capital Gains Tax Considerations

Looking at these facts as a whole, it is clear that the Finnish system is designed to be predictable yet progressive. The key for any investor in 2026 is to recognize that “capital gains” is an umbrella term covering many different types of income, each with its own specific set of deductions and reporting timelines.

Overview Of 12 Finland Capital Gains Tax Facts

To make the best decisions, it is helpful to see how these various categories compare in terms of their typical tax burden and ease of management. The following section provides a structured breakdown for quick reference.

Overview Comparison Table

The table below outlines the primary differences in treatment across major asset classes under the current Finland Capital Gains Tax framework.

| Asset Type | Primary Tax Rate | Reporting Ease | Top Benefit |

| Listed Stocks | 30% or 34% | High (Automatic) | 15% Dividend Exemption |

| Primary Home | 0% | Moderate | Fully Tax-Free after 2 years |

| Bank Interest | 30% (Flat) | Very High (Source) | No manual reporting |

| Crypto Assets | 30% or 34% | Low (Manual) | Loss offset capability |

| Long-term Land | 30% or 34% | Moderate | 40% Deemed Cost deduction |

Our Top 3 Picks and Why?

-

The 2-Year Residence Exemption: This is our top pick because it is the most powerful wealth-building tool in the country. Avoiding a 30% tax on a home sale can save a family tens of thousands of euros.

-

The 40% Deemed Acquisition Cost: We chose this for its unique ability to rescue investors from poor record-keeping or extreme inflation on assets held for decades.

-

The Equity Savings Account (AOS): This is the gold standard for the modern stock investor. The ability to reinvest profits without an immediate tax bite is essential for long-term portfolio growth.

How to Choose the Right Finland Capital Gains Tax Strategy by Yourself?

Choosing a strategy requires you to look at your personal timeline and the type of assets you prefer. Finland’s tax code is relatively fixed, but how you interact with it can significantly change your effective tax rate.

The Selection Framework

-

Assess Your Holding Time: If you have held an asset for nearly 10 years, it is almost always better to wait until the 10th anniversary to sell so you can use the 40% deemed cost.

-

Review Your Annual Limits: Before selling a small asset, check if your total sales for the year are under €1,000. If you are at €950, selling another item for €100 will make your entire profit taxable.

-

Check Your Bracket: If you are nearing the €30,000 threshold in capital income, consider pushing some sales into the next calendar year to stay in the 30% bracket.

-

Match Losses with Gains: Use your capital losses proactively. If you have “paper losses” in your portfolio, selling them in the same year as a big gain can neutralize your tax bill.

To help you decide which path to take for a specific asset, refer to the decision matrix below.

| If your priority is… | Choose this action… | Because… |

| Long-term wealth | Open an Equity Savings Account | Taxes are deferred, allowing your money to work harder for longer. |

| High-profit land sales | Use Deemed Acquisition Cost | It likely provides a bigger deduction than your original cost basis. |

| Maximum simplicity | Focus on Bank Deposits | The 30% withholding is handled entirely by the bank. |

| Selling a high-value home | Wait for the 24-month mark | Selling at 23 months could cost you 30% of your entire profit. |

The Final Checklist

-

Verify the exact date of purchase for any asset you plan to sell.

-

Check your MyTax portal for any carried-forward losses from the previous five years.

-

Calculate your total expected capital income to see if you will hit the 34% tier.

-

Ensure you have digital records for all cryptocurrency trades for 2026 compliance.

-

Confirm your residency status in your primary home if you are planning to sell tax-free.

Mastering Your Finnish Investment Tax Strategy

Navigating the Finnish tax landscape in 2026 requires a mix of patience and precise record-keeping. While the tiered system is straightforward, the real value lies in the details, such as the deemed acquisition costs and the specific exemptions for primary residences. By staying proactive and using the tools provided by the Tax Administration, you can ensure that your investment journey in Finland is as tax-efficient as possible.