Denmark has long been a global benchmark for the “Nordic Model,” combining high taxes with a robust social safety net. However, as we move through March 2026, the conversation around Denmark’s wealth tax 2026 has reached afever pitch. Between the implementation of the massive “Top-Top Tax” and Prime Minister Mette Frederiksen’s controversial new wealth levy proposal, the rules for high-net-worth individuals are being completely rewritten.

Understanding these nuances is no longer just for tax professionals; it is vital for anyone looking to understand how the world’s “happiest country” plans to fund its future.

Our Selection Methodology

To identify these ten critical facts, we synthesized the latest 2026 Danish Ministry of Taxation reports, the legislative details of the January 1st Tax Reform, and the ongoing policy debates leading up to the snap election. We prioritized information that contrasts sharply with international perceptions—such as the reality that Denmark actually abolished its wealth tax decades ago before the current 2026 push to reinstate it. Each point was selected for its immediate relevance to high earners, investors, and residents navigating the 2026 fiscal landscape.

Breaking Down Denmark’s Wealth Tax 2026 Landscape

The Danish tax system is in a state of historic transition, moving from a traditional progressive model to an even more granular structure designed to target the ultra-wealthy.

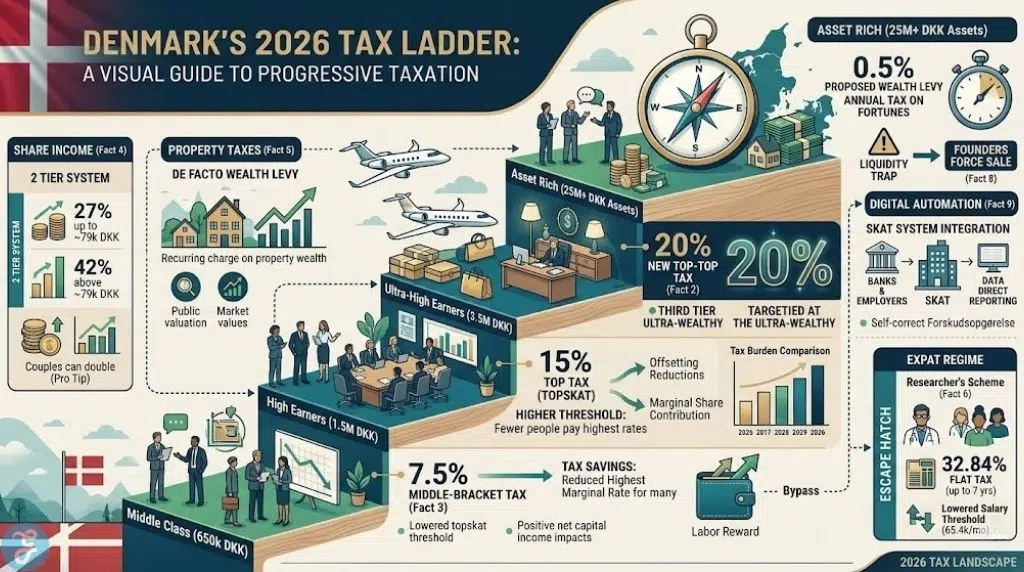

1. The Rebirth of a Discarded System

Many are surprised to learn that Denmark actually abolished its traditional net wealth tax back in 1997. For nearly 30 years, the country operated without a direct levy on assets. However, as part of her 2026 campaign, Mette Frederiksen has proposed reinstating a 0.5% annual wealth tax on fortunes exceeding 25 million DKK to fund smaller school classes.

Best for: Understanding the political shift from 1990s liberalism back toward aggressive wealth redistribution.

Things to consider: This proposal is the central pillar of the 2026 election; its survival depends entirely on the coalition negotiations following this month’s vote.

This proposed levy is designed to sit alongside a brand-new income tax bracket that launched earlier this year.

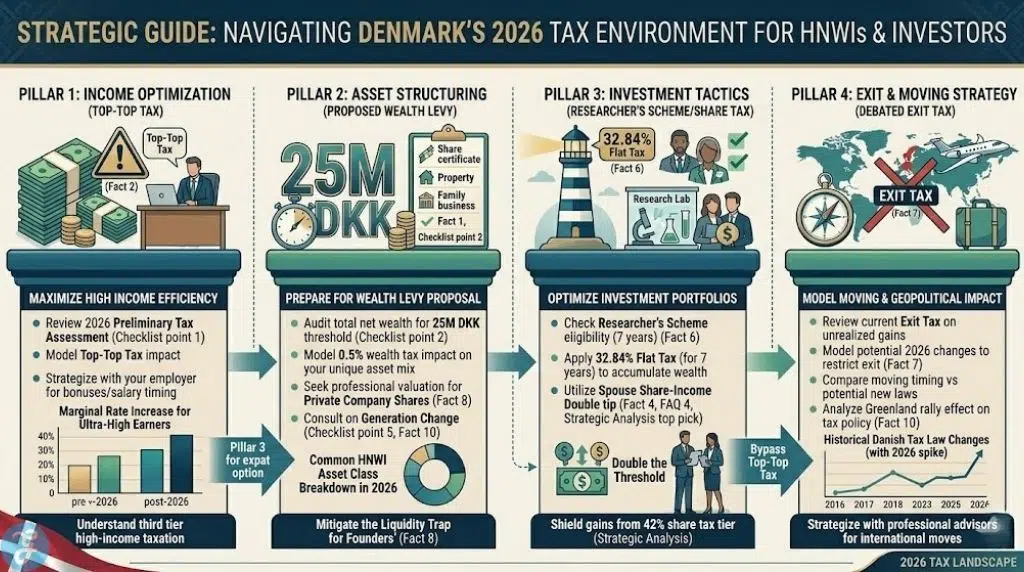

2. The Implementation of the “Top-Top Tax”

As of January 1, 2026, a new “top-top-bracket tax” has been introduced. This is a 20% state tax on personal income exceeding approximately 2.6 million DKK. This third tier of high-income taxation is designed to ensure that the highest earners contribute a larger marginal share than ever before in modern Danish history.

Best for: C-suite executives and successful entrepreneurs whose annual compensation packages exceed the multi-million DKK mark.

Things to consider: The net effect of this tax only kicks in fully above 3.1 million DKK due to offsetting reductions in other tax categories, making the math surprisingly complex.

While income is being taxed more heavily at the top, middle-income earners are actually seeing a different trend.

3. The “Middle-Bracket” Tax Return

The 2026 reform didn’t just target the rich; it reintroduced a “middle-bracket tax” of 7.5%. Paradoxically, this was actually designed to reduce the number of people paying the standard “top tax” (topskat) by raising the threshold for the highest brackets.

Best for: The roughly 285,000 Danes who will no longer pay the highest marginal rates on their moderate professional salaries.

Things to consider: While the threshold is higher, the inclusion of positive net capital income in this bracket means your investment gains could still push you into a higher tax tier.

Beyond income, the way Denmark taxes investments is among the most progressive in the world.

In 2026, Denmark continues to use a two-tier system for share income (dividends and capital gains). While the first 79,400 DKK is taxed at a manageable 27%, everything above that is hit with a 42% rate, one of the highest in the OECD.

Best for: Investors with significant equity portfolios who are looking for a tax-efficient way to liquidate gains.

Things to consider: Married couples can double this threshold to 158,800 DKK, which is a critical “pro tip” for Danish family wealth planning.

Real estate also serves as a secondary, indirect form of wealth taxation.

5. Property Taxes as a De Facto Wealth Levy

Even without a formal net wealth tax, Denmark’s property value tax acts as a recurring charge on your most significant asset. Owners pay a percentage based on the public valuation of their home, which effectively functions as an annual tax on housing wealth.

Best for: Homeowners in high-demand areas like Copenhagen where property values have skyrocketed over the last decade.

Things to consider: Recent reforms have linked these taxes more closely to current market values, ending the “tax freeze” that previously protected long-term owners.

For those coming from abroad, there is a specialized “escape hatch” from these high rates.

6. The 2026 Expat Tax Regime Expansion

To stay competitive, Denmark has made its “Researcher’s Scheme” even more accessible in 2026. Qualifying international experts can opt for a flat tax rate of 32.84% for up to seven years, completely bypassing the top-top tax and the proposed wealth levy.

Best for: Highly skilled foreign professionals and researchers being recruited by Danish tech and pharma giants.

Things to consider: The minimum salary threshold was lowered to 65,400 DKK per month in 2026, making it much easier for mid-career talent to qualify.

However, leaving Denmark once you have built wealth can be just as expensive as staying.

7. The Looming “Exit Tax” Debate

Following the precedent set by Norway, Danish politicians are currently debating a more restrictive exit tax for 2026. This would prevent wealthy individuals from moving to low-tax jurisdictions like Switzerland to realize gains made while residing in Denmark.

Best for: High-net-worth individuals considering a move out of the country before new legislation is potentially passed.

Things to consider: Currently, Denmark already has an exit tax on “unrealized” gains on shares, but the 2026 proposal aims to make these rules even more difficult to circumvent.

Start-up founders are particularly vocal about the dangers of these new proposals.

8. The “Liquidity Trap” for Founders

A major point of 2026 contention is that the proposed wealth tax would apply to “paper wealth”—the estimated value of private company shares. This means founders could be forced to sell parts of their company just to pay the tax on shares that haven’t been sold yet.

Best for: Tech entrepreneurs and family business owners whose wealth is tied up in illiquid assets.

Things to consider: Business leaders from Lego, Maersk, and Vestas have warned that this could lead to capital flight and reduced innovation.

Despite these hurdles, the system is designed to be incredibly automated.

9. Digital Automation of Wealth Reporting

One of the reasons Denmark’s wealth tax 2026 is so effective (and difficult to avoid) is the integration of the “Skat” system. Banks, employers, and even some international financial institutions report data directly to the Danish authorities.

Best for: The average taxpayer who wants to ensure compliance without hiring a dedicated accountant.

Things to consider: While automated, you are still legally responsible for correcting the “forskudsopgørelse” (preliminary assessment) if your investment income changes mid-year.

Finally, the 2026 environment is being heavily influenced by external geopolitical factors.

10. The “Greenland Effect” on Tax Policy

Prime Minister Frederiksen’s surge in the 2026 polls—and her ability to push for wealth taxes—is partly attributed to her strong stance against foreign interests in Greenland. This “rally around the flag” effect has given her the political capital to propose fiscal measures that were previously unthinkable.

Best for: Geopolitical observers tracking how national identity influences economic policy.

Things to consider: If the election results in a more centrist coalition, many of these “rich-tax” proposals may be watered down in exchange for business-friendly concessions.

Strategic Analysis

Navigating the Denmark’s wealth tax 2026 environment requires a clear understanding of where you sit on the income and asset spectrum. The table below compares the effective tax burden before and after the 2026 reforms for different earner profiles.

| Earner Category | Annual Income (DKK) | Pre-2026 Marginal Rate | 2026 Marginal Rate | Key Change |

| Middle Class | 650,000 | ~52% | ~42-49% | Middle-tax shift (Savings) |

| High Earner | 1,500,000 | ~56% | ~56% | Higher Top-Tax Threshold |

| Ultra-High Earner | 3,500,000 | ~56% | ~60.5% | New “Top-Top Tax” Layer |

| Asset Rich | 25M+ Assets | 0% | 0.5% (Proposed) | New Wealth Tax Levy |

Our Top 3 Picks And Why?

-

The Researcher’s Scheme (Expat Tax): This is our top pick for global talent. It is the only legal way to cap your Danish tax liability at a flat 32.84%, making it the most powerful tool for wealth accumulation in Denmark.

-

The 2026 Middle-Tax Shift: We chose this because it is the “hidden winner” of the reform. For the first time in years, hundreds of thousands of professionals will see a genuine reduction in their marginal tax rate.

-

The Spouse Share-Income Double: This is the most essential “day-to-day” tip. By splitting your equity holdings with a spouse, you effectively shield double the amount of capital gains from the brutal 42% tax tier.

Preparation Checklist

If you are a high earner or asset holder in Denmark, ensure you have completed these steps for 2026:

-

Review your 2026 Preliminary Tax Assessment (forskudsopgørelse) to ensure the new “Top-Top” thresholds are reflected.

-

Audit your total net wealth—if you are near the 25M DKK mark, begin modeling the impact of the proposed 0.5% levy.

-

Check your eligibility for the Researcher’s Scheme if you have been in Denmark for less than 7 years; the 2026 rules may now include you.

-

Ensure all foreign assets are declared; the 2026 automation makes “hidden” offshore wealth more detectable than ever.

-

Consult with a specialist regarding “Generation Change” (generationsskifte) if you plan to pass on a family business, as the wealth tax rules for these are still in flux.

The evolution of Denmark’s wealth tax 2026 represents a bold experiment in balancing social equity with economic competitiveness. While the new “Top-Top Tax” and the wealth tax proposals create significant hurdles for the ultra-wealthy, the simultaneous easing of taxes for the middle class shows a government trying to reward labor while taxing capital. For those living in or moving to Denmark, success in this new era requires a sharp eye on policy shifts and a proactive approach to utilizing the specialized schemes designed to keep the country attractive to global talent.

FAQs

Is there currently a wealth tax in Denmark?

As of today, there is no net wealth tax, but there is a major proposal to reinstate a 0.5% levy for those with assets over 25 million DKK.

What is the “Top-Top Tax”?

It is a new 2026 tax of 20% on the portion of your personal income that exceeds 2,592,700 DKK (after AM-tax).

Do I pay tax on my home’s value every year?

Yes, Denmark uses a property value tax and a land tax, which act as recurring annual charges based on the valuation of your real estate.

Share income is taxed at 27% for the first 79,400 DKK and 42% on anything above that threshold.

By using an ISA-style “Aktiesparekonto,” you can invest a limited amount (approx. 135,900 DKK in 2026) at a lower flat rate of 17%, though this is capped.