Credit cards can be a convenient way to handle everyday purchases, but interest charges can quickly add up and quietly drain your finances. A few small expenses—groceries or gadgets—can turn into a growing balance if not managed properly, especially when only minimum payments are made.

It’s similar to a slow leak in your budget, steadily reducing your hard-earned money month after month.

A key point to understand is the grace period offered by most credit cards, which allows you to avoid interest entirely if the full balance is paid by the due date. This benefit, typically outlined in agreements from issuers like Bank of America or Capital One, is one of the most effective ways to avoid credit card interest completely.

This post explores practical strategies such as using 0% intro APR offers, balance transfers, autopay setups, and budgeting tools to help control spending and prevent unnecessary debt.

It also highlights how good credit habits can support better credit scores, leading to improved rates and long-term financial stability.

How Does Credit Card Interest Work?

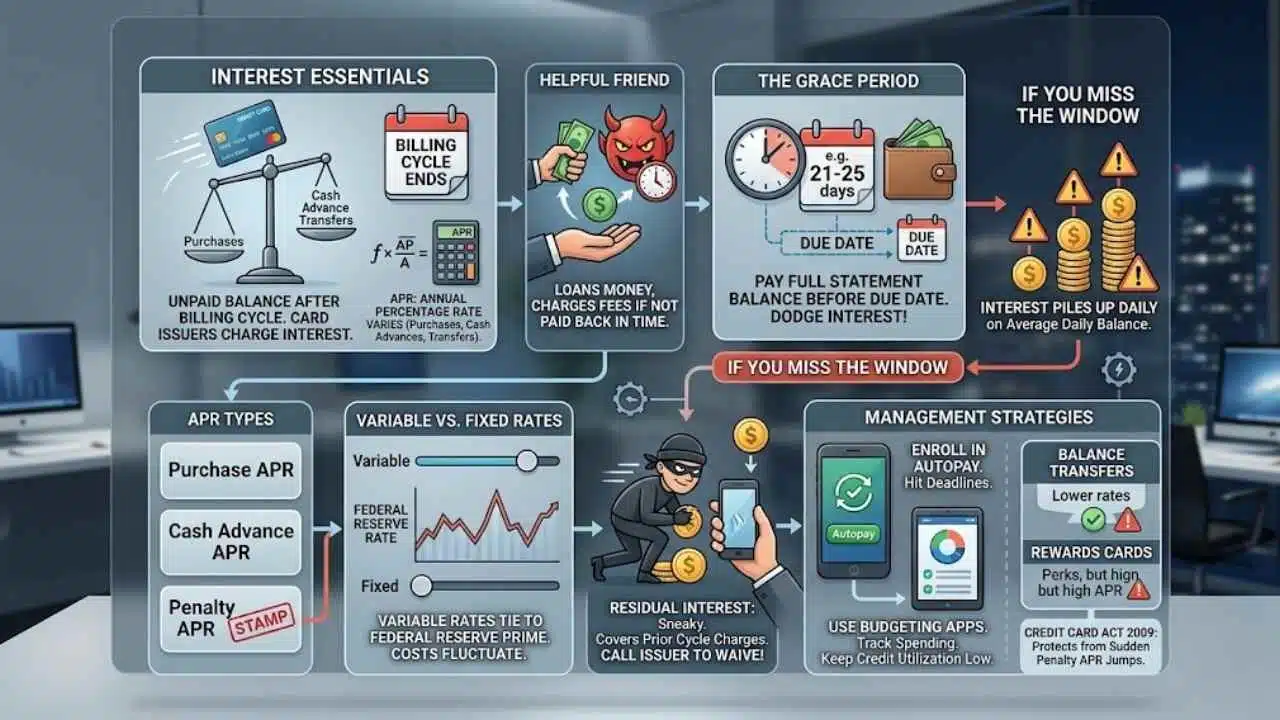

Credit card issuers charge interest on unpaid balances, and that hits after the billing cycle ends. They calculate this fee using the annual percentage rate, or APR, which can vary for purchases, cash advances, or balance transfers.

Your credit card as a helpful friend who loans you money, but that pal starts charging fees if you don’t pay back in time. Companies offer a grace period, often 21 to 25 days, letting you dodge interest by paying the full statement balance before the due date.

Miss that window, though, and interest piles up daily on the average balance. You face different rates like purchase APR for buys, cash advance APR for withdrawals, or penalty APR for late payments.

Residual interest sneaks in too, even after you pay off the balance, as it covers charges from the prior cycle. Call your issuer; they might cut or waive that sneaky fee.

Understanding the terms of your credit card agreement, including grace periods and interest rates, is essential for avoiding unnecessary interest charges. – Consumer Financial Protection Bureau

Folks often overlook how variable interest rates tie to the Federal Reserve prime rate, making costs fluctuate. Fixed interest rates stay steady, but most cards use variables. Enroll in autopay to hit deadlines, or use a budgeting app to track spending and keep credit utilization low.

Balance transfers to a card with promotional APR can slash fees, yet watch for transfer fees. Rewards credit cards tempt with perks, but high APRs bite if you carry debt. Santander Bank or Citi might offer low rates; check Bankrate for comparisons.

Debt management pros like Meredith Hoffman or Jacqueline DeMarco suggest paying more than the minimum to shrink interest fast. The Credit Card Act of 2009 curbs surprise hikes, protecting you from sudden penalty APR jumps.

Key Strategies to Avoid Credit Card Interest

Your credit card as a sneaky fox, always ready to pounce with APR charges if you let your guard down. Let’s outsmart it with smart moves that keep your wallet happy, like mastering payment methods to dodge those fees entirely.

Pay Your Balance in Full Each Month

Your credit card as a trusty sidekick in personal banking, but one that bites back with annual percentage rate charges if you slip up. You dodge those bites by paying your full statement balance by the due date each month.

This simple move in financial responsibility keeps interest at bay, plain and simple. Credit card companies give you a grace period, that handy window to settle up without a single penny in extra costs.

Life throws curveballs, like unexpected bills from auto loans or home loans, yet sticking to this habit turns the tide. Pay more than the minimum, and you slash any potential interest on your balance.

Folks, it’s like outrunning a slow-moving storm; you stay dry by moving fast.

Master your credit card agreement terms, including those grace periods and interest rates, to steer clear of traps. Enroll in autopay for on-time payments, a smart payment method that acts like your personal guard against slip-ups.

Track spending with a budgeting app, tying into saving and budgeting goals, maybe even linking to your checking accounts or savings accounts. Credit and debt management gets easier this way, folks.

Think of it as chatting with a friend over coffee; “Hey, I paid in full again, no interest sneaking up.” This approach builds strong habits, avoiding the drag of lingering charges.

Leverage Your Grace Period

Credit card companies give you a grace period to dodge interest charges on purchases. This time frame lets you pay the full statement balance by the due date, and poof, no APR hits your wallet.

Think of it like a free pass in the game of credit & debt, where smart players win big on saving & budgeting. American Express and Discover often offer solid grace periods, so check your card’s terms to spot the exact window.

You avoid interest completely with responsible habits, like paying balances in full each billing cycle. Read your credit card agreement closely; it spells out grace periods and interest rates to keep you out of unnecessary charges.

Avoid Cash Advances

Cash advances hit you with high fees and interest right away, no grace period in sight. They charge sky-high APRs that make your debt grow fast, like weeds in a garden. Skip them altogether and use other options, such as a personal loan or buy now, pay later plans, to dodge those costs.

Credit card companies love these advances because they rack up balance transfer APR quickly, but you can outsmart that trap. Think of it as steering clear of a money pit; opt for travel credit cards with rewards instead for smarter spending.

Cash advances are like borrowing from a shark – the interest bites hard and fast, says financial expert Raina He.

People often grab cash from ATMs with their cards, but that move skips any grace period and piles on fees. Interest starts ticking the second you take the money, unlike regular purchases.

Avoid this by planning ahead with a budget or even a certificate of deposit for emergencies. Enroll in autopay to keep balances low and call your issuer if residual interest sneaks in after payoff.

Use 0% Intro APR Offers Wisely

Snagging a credit card that lets you borrow money without paying a dime in interest for months, like getting a free pass on a shopping spree – dive deeper to learn smart moves that keep you out of debt traps.

Best Practices for 0% Intro APR Cards

Zero percent intro APR cards offer a smart way to dodge interest on purchases or balances for a set time. You can use them to your advantage if you follow some key habits, like paying on time and understanding the terms.

- Pick a card with a long intro period to give yourself more breathing room, say 12 to 21 months, so you can chip away at debt without that pesky APR kicking in. A 0% APR credit card serves as a viable option for eliminating interest charges on your existing balance, much like finding a free pass in a game of financial tag. Check the credit card agreement for details on grace periods and rates, because understanding these terms helps you steer clear of unnecessary charges.

- Apply online through your browser to compare offers quickly, but clear your cookies first to avoid skewed ads that might push the wrong card your way. This step keeps things fair, like wiping the slate clean before a big decision. Enroll in autopay right away to ensure on-time payments, tying into how paying your full statement balance by the due date each month stands as the primary way to avoid credit card interest charges.

- Transfer balances from high-interest cards to this new one, choosing a low or no-fee option to maximize savings. Balance transfer to a credit card with a lower interest rate proves an effective strategy to save on credit card interest, almost like moving your stuff to a cheaper apartment. Pay off the transferred balance before the intro period ends, and make multiple payments per month if needed to stay ahead.

- Avoid cash advances at all costs, since they often slap on fees and interest right away, bypassing that sweet 0% deal. Think of it as dodging a hidden trap in what seems like a clear path. Credit card companies offer a grace period during which you can pay your full balance without incurring interest, so leverage that to keep things interest-free.

- Monitor your spending with a budgeting app to track every dollar, preventing you from racking up more than you can handle. Paying more than the minimum payment helps reduce the total interest you will owe on your credit card balance, even if the intro rate shields you temporarily. Tie this into broader goals, like funneling saved money into investing and retirement accounts such as an IRA, turning short-term wins into long-term gains.

- Watch out for residual interest that might linger even after you pay off your balance, a sneaky charge that can catch you off guard. Calling your credit card company may provide options to avoid or reduce residual interest charges, so pick up the phone and chat like you’re negotiating with an old friend. This fits with maintaining responsible payment habits and paying balances in full each billing cycle to avoid credit card interest completely.

- Consider how your credit score impacts the offers you get, since better scores often snag lower rates post-intro. Enrolling in a hardship program with your credit card issuer can help you manage and potentially reduce interest charges if times get tough. For technical stuff like filling out forms, note that details from things like FAFSA can teach you about organized financial planning, applying that discipline here to use the card wisely.

Avoiding Pitfalls During Intro Periods

You snag a 0% intro APR card to wipe out interest on your balance. Pitfalls can sneak up, though, and turn that sweet deal sour if you don’t watch out.

- Watch for residual interest that lingers even after you pay off your balance, folks, because this sneaky charge pops up from interest accrued between your statement date and payoff. Credit card companies calculate it on the average daily balance, so it hits hard if you miss the details in your agreement. Call your issuer right away, as they might waive or cut it down, saving you bucks you can stash for investing and retirement goals instead.

- Skip new purchases on that 0% intro APR card during the promo period, readers, since many cards slap regular APR on fresh buys right away, no grace period attached. Imagine tossing extra charges into a money pit; that racks up interest fast and eats into your plan to eliminate charges on the existing balance. Focus payments on the transferred debt first to keep things clean and avoid this trap.

- Pay more than the minimum each month to chip away at your balance before the intro ends, because sticking to minimums leaves a hefty amount exposed to sky-high APR once the deal expires. Credit scores play into this too, as better scores snag lower rates later, but don’t let small payments drag you down. Think of it like dodging a financial avalanche; aggressive payoffs build momentum and shield your wallet.

- Read your credit card agreement like a treasure map, spotting grace periods and how they tie into the intro offer, to dodge unnecessary interest charges that creep in if you miss a deadline. Many folks overlook these terms, landing in hot water, but you can steer clear by marking due dates on your calendar. This habit keeps your payments responsible and aligns with using a 0% APR card as a smart tool for nixing interest on old debts.

- Enroll in a hardship program if money gets tight during the intro, as your issuer might slash rates or pause interest, giving you breathing room to pay off without extra costs piling up. Think of it as a lifeline in rough seas; it helps manage balances and reduces charges, but act fast by calling them up. Combine it with autopay for on-time hits, ensuring you maintain those good habits that avoid interest completely.

- Transfer balances wisely to a low or no-fee card with 0% intro APR, but calculate the timeline so you pay it off before the period ends, avoiding a jump to standard annual percentage rate that balloons your debt. Folks often underestimate this, like betting on a horse that trips at the finish; pick cards with long intros and low fees to maximize savings. This strategy shines for eliminating interest, but only if you budget tightly and track every penny.

Utilize Balance Transfers Effectively

Choosing a Low or No-Fee Balance Transfer Card

Pick a balance transfer card with low fees to cut costs right away. You move your debt to this new card, often with a lower APR, and save on interest. Balance transfer to a credit card with a lower interest rate is an effective strategy to save on credit card interest.

Look for cards that charge no fee or a small one, say 3 percent. A 0% APR credit card is a viable option for eliminating interest charges on your existing balance. Compare offers online, folks, because that can feel like finding money in an old coat pocket.

Check the terms, including that grace period, to dodge surprises. Understanding the terms of your credit card agreement, including grace periods and interest rates, is essential for avoiding unnecessary interest charges.

Call the issuer if you spot residual interest lurking; they might help reduce it. Enrolling in a hardship program with your credit card issuer can help you manage and potentially reduce interest charges.

Paying Off the Transferred Balance on Time

You move your debt to a card with a lower interest rate, and that cuts your costs right away. Balance transfer to a credit card with a lower interest rate saves you big on credit card interest.

Pick a 0% APR credit card, it wipes out interest on your old balance for a set time. Pay the full transferred amount before the intro period ends, or high rates kick in. Credit card companies give a grace period, so use it to settle up without extra fees.

Your savings growing like a nest egg for investing and retirement goals. Make those payments on time, every time, and watch your money work for you instead of the banks.

Set up autopay, it keeps you from missing due dates. Pay more than the minimum each month, that shrinks your debt faster and dodges interest buildup. Call your card issuer if residual interest pops up after payoff, they might cut or drop it.

Enroll in a hardship program if times get tough, it could lower your rates and ease the load. Understand your card’s terms, like grace periods and APR details, to stay ahead. Keep payments responsible, pay balances in full each cycle, and you avoid interest for good.

Track everything with a budgeting app, it spots overspending early.

Additional Tips to Avoid Interest

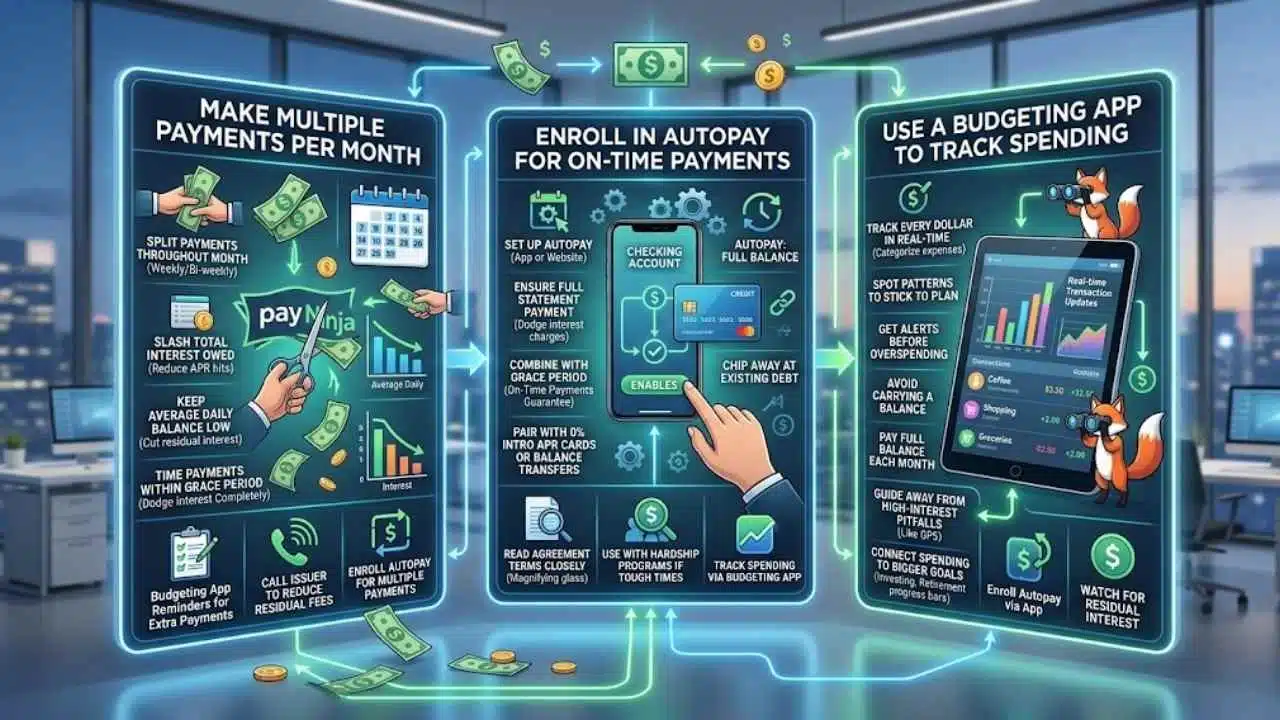

You know how dodging credit card interest can feel like outsmarting a sneaky fox, well, try splitting your payments throughout the month to keep that balance low, set up automatic payments so you never miss a due date and rack up late fees, or grab a handy app like Mint to watch your spending like a hawk—all these moves help you stay ahead without paying a dime extra in APR charges, so stick around for even more ways to keep your wallet happy.

Make Multiple Payments Per Month

You might think paying once a month is enough, but splitting up your payments can supercharge your fight against interest. This approach acts like a sneaky ninja, chopping down your balance before interest has a chance to build up.

- Split your payments throughout the month to pay more than the minimum, which slashes the total interest you owe on your credit card balance, as fact shows this tactic reduces what APR hits you with.

- Time these extra payments right within your grace period, so you dodge interest charges completely, much like slipping through a closing door before it shuts.

- Watch how multiple payments keep your average daily balance low, cutting down on that pesky residual interest that can sneak up even after you think you’ve paid off everything.

- Grab a budgeting app to track your spending and set reminders for those extra payments, turning what could be a hassle into a smooth habit that saves you cash.

- Imagine you’re at the grocery store and remember to toss in an extra payment via your phone app, nipping interest in the bud before it blooms.

- Call your credit card company if residual interest pops up, they might offer ways to reduce or avoid it, giving you a lifeline when balances linger.

- Combine this with responsible habits, like understanding your card’s terms on grace periods and interest rates, to avoid unnecessary charges and keep your APR from biting.

- Enroll in autopay for those multiple hits, ensuring on-time payments that maintain your grace period and prevent interest from accruing on purchases.

- Think of it as feeding a parking meter before it expires, multiple small payments prevent the interest ticket from showing up on your statement.

- Use this strategy alongside low-interest cards, where your credit score influences rates, helping you sidestep high APR and funnel saved money toward investing or retirement goals.

Enroll in Autopay for On-Time Payments

Autopay sets up your credit card payments to pull straight from your bank account each month. This simple tool stops late fees and interest from sneaking up on you.

- Set up autopay through your credit card issuer’s app or website, and link it to your checking account for seamless transfers; this ensures you pay your full statement balance by the due date each month, dodging interest charges as fact one highlights, much like an automatic pilot keeping your finances on course.

- Choose to autopay the full balance instead of just the minimum, since paying more than the minimum cuts down on total interest you might owe, per fact three; imagine it as feeding a small fire before it turns into a blaze, keeping your APR from biting into your budget.

- Combine autopay with your grace period, that window credit card companies give to pay without interest, as in fact two; this combo acts like a safety net, ensuring on-time payments that let you avoid charges completely, especially if you maintain responsible habits from fact nine.

- Watch out for residual interest that can linger even after payoff, noted in fact six; autopay helps by keeping payments consistent, but call your issuer to explore options for reducing it, like fact seven suggests, turning a potential headache into a quick fix.

- Pair autopay with a 0% intro APR card for new purchases or balances, drawing from fact five; this setup eliminates interest on existing debt while automatic payments chip away at it, freeing up cash you could direct toward investing and retirement goals.

- Use autopay after a balance transfer to a lower interest rate card, as fact four recommends; select a low or no-fee option and let autopay handle timely payoffs, preventing old high APR from haunting your transferred balance like a ghost from past spending.

- Enroll in autopay alongside a hardship program if times get tough, per fact eight; this can lower interest rates temporarily while automatic payments keep things steady, offering breathing room without derailing your path to zero interest.

- Read your credit card agreement terms closely before setting up autopay, covering grace periods and interest rates from fact ten; knowledge here empowers you to tweak settings for full balance payments, ensuring you sidestep unnecessary charges with ease.

- Track everything with a budgeting app once autopay runs, tying into broader tips; this monitors spending against your APR, helping you stay ahead and channel savings into areas like investing and retirement for long-term wins.

Use a Budgeting App to Track Spending

Your credit card like a sneaky fox, always ready to pounce with interest charges if you slip up. Grab a budgeting app, folks, and turn the tables. These tools let you track every dollar you spend in real time.

You see where your money goes, from coffee runs to online shopping sprees. This habit helps you stick to a plan and pay your full statement balance by the due date each month, dodging that pesky APR altogether.

Apps like Mint or YNAB act as your financial sidekick, sending alerts before you overspend. They tie into your accounts, categorize expenses, and even forecast your cash flow. By spotting patterns early, you avoid carrying a balance that racks up interest.

Credit card interest can vanish completely with responsible habits, like using these apps to monitor and adjust your spending.

Think of budgeting apps as a GPS for your wallet, guiding you away from high-interest pitfalls. They help you make multiple payments per month if needed, chipping away at balances faster.

Understanding your card’s terms, including grace periods and interest rates, becomes a breeze with app insights. You might even link this tracking to bigger goals, like saving for investing and retirement.

Enroll in autopay through the app for on-time payments, but watch for any residual interest that could linger after payoff. Call your issuer if that happens; they might reduce it. Balance transfers to low-APR cards show up clearly in these apps, letting you pay off transferred amounts on time.

With empathy for those tight months, know that hardship programs from issuers can ease interest burdens, and apps flag when to seek them. Stay ahead, readers, and laugh off those interest woes with smart tracking.

Other Factors to Consider

Your credit score shapes the interest rates lenders offer you on cards, so a strong one can cut your costs big time. Low-interest cards also pack perks like easier debt management, making them a smart pick if you carry a balance now and then.

How Credit Scores Impact Interest Rates

Credit scores act like a report card for your money habits, and they directly shape the annual percentage rate, or APR, you get on credit cards. Lenders check these scores to decide risk levels.

High scores signal reliability, so companies offer lower interest rates as a reward. Think of it like earning a discount for good behavior; pay bills on time, keep debt low, and watch those rates drop.

Low scores? They scream trouble to lenders, leading to sky-high APRs that bite into your wallet. Build strong habits, like paying full balances each cycle as fact nine suggests, and you pave the way for better deals.

Smart moves with credit boost scores over time, tying into bigger goals like investing and retirement planning. Understand card terms, including grace periods and rates from fact ten, to dodge extra charges.

Enroll in hardship programs if needed, per fact eight, to ease interest burdens while improving your score. Balance transfers to lower-rate cards, as in fact four, help too, cutting costs and showing lenders you’re in control.

Picture your score as a key that unlocks savings; nurture it, and it opens doors to low-interest options that free up cash for future dreams.

Benefits of Low-Interest Credit Cards

Low-interest credit cards pack a punch when you want to keep more money in your pocket.

| Benefit | Details |

|---|---|

| Save on charges | These cards cut down what you pay in fees over time, especially if you carry a balance. Think of them as a shield against high costs that eat into your budget. |

| Easier debt payoff | Pay more than the minimum each month. This move slashes the total interest on your balance, like knocking out a foe before it grows stronger. |

| Smart balance shifts | Move debt to a card with a lower rate. You save big on interest this way, turning a tough spot into a smoother ride. |

| Zero percent options | Grab a 0% APR card for your current balance. It wipes out interest charges, giving you breathing room to pay off what you owe without extra hits. |

| Build good habits | Maintain responsible payments and clear balances fully each cycle. You dodge interest altogether, like steering clear of a storm on the horizon. |

| Know your terms | Grasp your card agreement details, such as grace periods and rates. This knowledge stops needless charges, much like reading a map before a trip. |

Final Thoughts

You’ve learned to dodge credit card interest by paying your full balance each month, using grace periods, and steering clear of cash advances. These steps keep things simple and save you money without much effort.

Why not check your next statement and try paying it off right away? Smart habits like these build strong finances and cut stress from high APR charges. For more help, explore budgeting apps or chat with your bank about low-rate options.

Once, I skipped interest for a year by juggling balance transfers wisely, and it felt like winning a small jackpot. Take charge today, and watch your savings grow like a well-tended garden.

Frequently Asked Questions (FAQs) on How to Avoid Credit Card Interest

1. What’s APR, and how can it mess with my wallet if I don’t watch out for credit card interest?

APR stands for annual percentage rate, it’s basically the cost you pay for borrowing money on your credit card. To avoid it completely, pay your full balance each month before the due date, like dodging a sneaky fee that piles up. That way, you keep more cash for fun stuff, or even investing and retirement plans.

2. Can I really skip credit card interest forever, without any tricks?

Sure, use the grace period wisely; that’s the time between your purchase and when interest kicks in. Just pay off everything in that window, and boom, no interest. It feels like outsmarting the system, doesn’t it?

3. What’s a smart move to dodge interest while thinking about my future savings?

Look into zero percent APR promotional offers on new cards, transfer your balance there, and pay it down fast. This frees up money you would’ve lost to interest, perfect for boosting your investing and retirement goals. Remember, it’s like giving your finances a fresh start, but stay disciplined to avoid new debt.

4. How does budgeting help me avoid credit card interest and build wealth?

Budgeting keeps you from overspending, so you pay balances in full and skip that pesky interest. Tie it to your investing and retirement strategy by saving what you don’t spend on fees.