Navigating the various bank account types doesn’t have to feel overwhelming. While a standard checking account easily manages your daily expenses, selecting the right high-yield savings account, money market account, or certificate of deposit (CD) ensures your cash actively grows instead of sitting idle.

Simplify your personal finance strategy by assigning a specific, real-world job to every account. This targeted approach makes it easy to bypass hidden fee traps and build a highly efficient banking setup. Learn how to seamlessly organize your money to cover routine bills, protect a robust emergency fund, and accelerate your long-term financial goals.

Basics of Bank Accounts

The four basic bank account types are still the ones that matter most for personal banking in the US: checking accounts, savings accounts, money market accounts, and certificates of deposit, or CDs. Each one solves a different problem, so the smartest move is to give every account one clear job.

The Federal Deposit Insurance Corporation insures checking, savings, money market deposit accounts, and CDs up to $250,000 per depositor, per insured bank, per ownership category. That detail matters more than most readers realize, because two accounts at the same bank do not automatically double your protection if they are titled the same way.

There is one useful 2026 update worth knowing. In the latest FDIC guidance, insured banks must display the official digital FDIC sign on bank websites, apps, and certain ATMs starting March 1, 2026, so you have a faster way to verify that an online bank account is actually backed by federal deposit insurance.

If you use a credit union instead of a bank, the safety net is similar. Credit unions such as Greater Nevada Credit Union use NCUA insurance rather than FDIC insurance, and the standard federal share insurance limit is also $250,000.

- Checking account: best for paychecks, bills, debit card spending, and cash access.

- Savings account: best for emergency savings and short goals you may need soon.

- Money market account: best for a larger cash cushion when you want savings features plus a little more access.

- Certificate of deposit (CD): best for money you can leave alone until a set date.

Pick accounts that match your plan, not your fear.

Main Types of Bank Accounts

You do not need every account type on day one. Most readers do best with a checking account for spending, a savings account for an emergency fund, and then either a money market account or a certificate of deposit for a specific goal.

| Account type | Best use | Access level | Rate pattern | Main trade-off |

|---|---|---|---|---|

| Checking account | Daily spending, direct deposit, bill pay | Highest | Usually low | Fees and overdrafts can erase value |

| Savings account | Emergency fund, sinking fund, next goal fund | High, but not meant for purchases | Variable | Some banks still set transfer limits or excess withdrawal fees |

| Money market account | Larger cash reserve, short-term savings | High to moderate | Variable | Minimum balance rules are often stricter |

| Certificate of deposit (CD) | Fixed-date savings goal | Low until maturity | Usually fixed | Early withdrawal penalties |

Checking Accounts

A checking account is your spending account. It is where direct deposit lands, where bills get paid, and where your debit card, ATM withdrawals, online banking, and tools like Zelle usually live.

What matters most here is not a flashy bonus. It is whether the account keeps fees low, supports the way you spend, and makes mobile banking easy enough that you will actually use it.

The best checking accounts in 2026 are giving readers more than the old basic setup. As of May 2026, Capital One says its 360 Checking has no monthly fees, no minimums, no overdraft fees, and access to 70,000-plus fee-free ATMs, while Discover says its Cashback Debit account has no monthly fee and pays 1% cash back on up to $3,000 in monthly debit card purchases.

Community banks can still be strong options too. Mid Penn Bank’s Simply Free Non-Interest Checking account highlights no monthly service fee, mobile check deposit, and Zelle, which is a nice mix if you want local service without giving up digital tools.

- Look for: no monthly maintenance fee, strong mobile app, easy bill pay, and wide ATM access.

- Nice extras: cashback on debit purchases, early direct deposit, or free paper checks.

- Watch closely: out-of-network ATM fees, overdraft fees, and minimum balance rules.

- Best fit: readers who need one simple hub for paychecks and everyday spending.

One more fee saver is easy to miss. The CFPB says your bank cannot charge overdraft fees on one-time debit card and ATM transactions unless you opt in, so if you hate surprise charges, review that setting before you ever swipe the card.

Savings Accounts

A savings account is where you park money you do not want to spend by accident. It is the workhorse for an emergency fund, short-term goals, sinking funds, and the cash cushion that keeps your checking account from doing too much.

This is also where interest rates make a real difference. In Bankrate’s May 2026 roundup, top high-yield savings accounts reached 4.21% APY, while the FDIC’s March 2026 national rate for plain savings was 0.39%.

That rate gap is not small. On a $10,000 balance, a 4.21% account earns about $382 more per year than a 0.39% account before taxes, which is why many readers move emergency savings out of a basic branch savings account and into a HYSA.

American Express and Capital One both advertise no monthly fees and no minimum balance on their main online savings products. That is the kind of account feature you want, because a higher APY loses its shine fast if the bank starts charging you for carrying a smaller balance.

The old federal six-withdrawal rule also trips people up. The Federal Reserve removed that Regulation D limit in 2020, but banks can still set their own transfer limits or excess withdrawal fees, so always read the current fee schedule before you treat a savings account like a second checking account.

A savings account keeps cash safe, and it helps you hit real goals without guessing how much of your checking balance is actually available.

Money Market Accounts

A money market account sits between checking and savings. It is built for readers who want better interest rates than a basic savings account, but still like having limited check-writing or debit card access.

This can work well for a larger emergency fund or a short-term savings pool for property taxes, insurance, or a planned purchase. You get more flexibility than a CD, but you still need to watch minimum balance rules because many money market accounts get less attractive once your balance drops.

Do not confuse a money market account with a money market mutual fund. A money market account is a bank deposit product and can be FDIC-insured, while a money market mutual fund is an investment product and is not covered by FDIC insurance.

Rates also vary more than readers expect. Bankrate’s national average money market yield was 0.43% in early May 2026, yet some online offers were far higher, so you need to compare actual APYs instead of assuming every money market account is a high-yield option.

That shows up clearly in real products. Greater Nevada Credit Union’s posted money market tiers in 2026 were modest, which is a good reminder that even solid financial institutions can be great for service and weak on yield, or the other way around.

Understanding Certificates of Deposit (CDs)

A certificate of deposit, or CD, pays a fixed rate for a fixed term. If you know roughly when you will need the money, this account can be a clean choice because it removes temptation and locks in the rate.

Think of a CD as a deadline tool. If you are saving for a car down payment next spring or tuition due in 12 months, a CD can keep that money separated from your spending account and protected from rate drops.

Shopping matters here too. In May 2026, Bankrate listed top CD rates up to 4.20% APY, while its national average 1-year CD was 1.95%, so picking the first CD your everyday bank offers can leave a lot of interest on the table.

The downside is access. If you pull funds early, many banks charge a penalty that can eat part of your interest, and in some cases even nibble at principal if you exit very early.

- Use a standard CD if you know the date and want a fixed return.

- Use a no-penalty CD if the goal date is fuzzy but you still want more yield than a checking account.

- Use a CD ladder if you want part of your cash maturing every few months instead of all at once.

Essential Bank Account Types for You

If you want the short answer, here it is: most readers only need two or three bank accounts to cover daily spending, emergency savings, and planned goals. You do not need a giant stack of accounts, but you do need clear roles.

Everyday Spending Needs

Start with one checking account that handles your paycheck, rent or mortgage, utilities, and card spending. This is your bills account and main spending account, so convenience matters more here than squeezing out a tiny bit of interest.

If your cash flow feels chaotic, a second checking account can help. Personal finance forum threads in 2026 keep coming back to the same trick: one account for fixed bills, one for flexible spending, because seeing separate balances makes money management much easier.

Fees should drive the decision. Bank of America’s current disclosure for Advantage Plus Banking lists a $12 monthly fee unless you meet a waiver, such as a qualifying direct deposit of at least $250 or a $1,500 minimum daily balance, and Citi’s current pricing lists $15 for Regular Checking and $5 for Access Checking unless you meet its waiver terms.

- Pick a checking account with a debit card you can freeze and unfreeze in the app.

- Turn on balance alerts and bill reminders inside online banking.

- Consider a separate bills account if your income arrives on irregular dates.

- If cash deposits matter, confirm that the bank’s ATM network accepts them before you open the account.

For daily spending, simple beats fancy. A no-fee checking account with solid mobile banking is usually better than an account that promises rewards but punishes you with a missed minimum balance.

Setting Up an Emergency Fund

Your emergency fund needs two things at the same time: safety and fast access. That is why a high-yield savings account is still the best first stop for most readers.

Fidelity’s emergency fund guidance says to start with $1,000 and build toward three to six months of essential expenses. That range gives you a practical target without pushing you into analysis mode for weeks.

- Use a separate savings account: keeping emergency savings away from your main checking account creates a useful speed bump before impulse transfers.

- Choose yield with access: a HYSA is usually the sweet spot because it pays interest without locking the money.

- Test transfers early: move a small amount in and out before you need the account for a real emergency.

- Use windfalls on purpose: the IRS allows you to split a tax refund into up to three accounts with Form 8888, which makes a refund a great way to seed emergency savings.

- Avoid using investing money as your first emergency layer: selling assets and waiting for settlement adds stress at the exact moment you want less of it.

A common pro tip from personal finance forums is to hold the emergency HYSA at a different bank than your main checking account. That helps in two ways: you are less likely to dip into it, and you still have backup cash access if fraud freezes your primary debit card.

Planning for Long-term Savings

For long-term savings, the right home depends on the timeline. Bank accounts are great for money you must protect, but they are the wrong tool for goals that are many years away and need growth.

| Timeline | Best home | Why it fits |

|---|---|---|

| Less than 12 months | HYSA or money market account | Keeps cash liquid for near-term bills or planned purchases |

| 1 to 3 years | CD or CD ladder | Locks in a rate for a known goal date |

| More than 5 years | Retirement or investment account, not a standard bank account | Gives long-term money a better shot at outgrowing inflation |

If retirement is the goal, bank accounts should play a support role, not the starring role. The IRS says the 2026 IRA contribution limit is $7,500 and the 2026 401(k) limit is $24,500, which is why long-term savings often belong in tax-advantaged retirement accounts once your emergency fund is covered.

That does not mean bank accounts stop mattering. A CD can still be perfect for a one-year home repair fund, a tuition payment due next fall, or a planned move where preserving the cash matters more than chasing investment returns.

Accounts for Specific Financial Goals

This is where multiple bank accounts can really improve financial management. Separate accounts turn vague intentions into visible targets.

- Sinking fund: open a separate savings account for car repairs, holiday spending, travel, or annual insurance bills.

- Joint household money: if two people own a qualifying joint account at the same bank, FDIC coverage can reach $500,000 because each co-owner gets up to $250,000 in the joint category.

- Medical costs: if you are HSA-eligible, the IRS says 2026 contribution limits are $4,400 for self-only coverage and $8,750 for family coverage.

- Kids and family goals: linked savings accounts can help parents track school, activities, or teen spending without mixing those dollars into everyday cash.

- Business money: keep rental or side-hustle funds out of personal checking accounts so taxes, security deposits, and operating cash stay easy to track.

There is one overlooked FDIC detail for business owners. If you are a sole proprietor, a DBA account does not get its own separate insurance bucket, it is generally combined with your single accounts at the same bank, so large balances may need more planning than you expect.

Selecting Your Ideal Bank Account

The best bank account is the one that fits your actual habits, not the one with the prettiest ad. Match each account to a goal, then compare fees, access, insurance, and interest rates in that order.

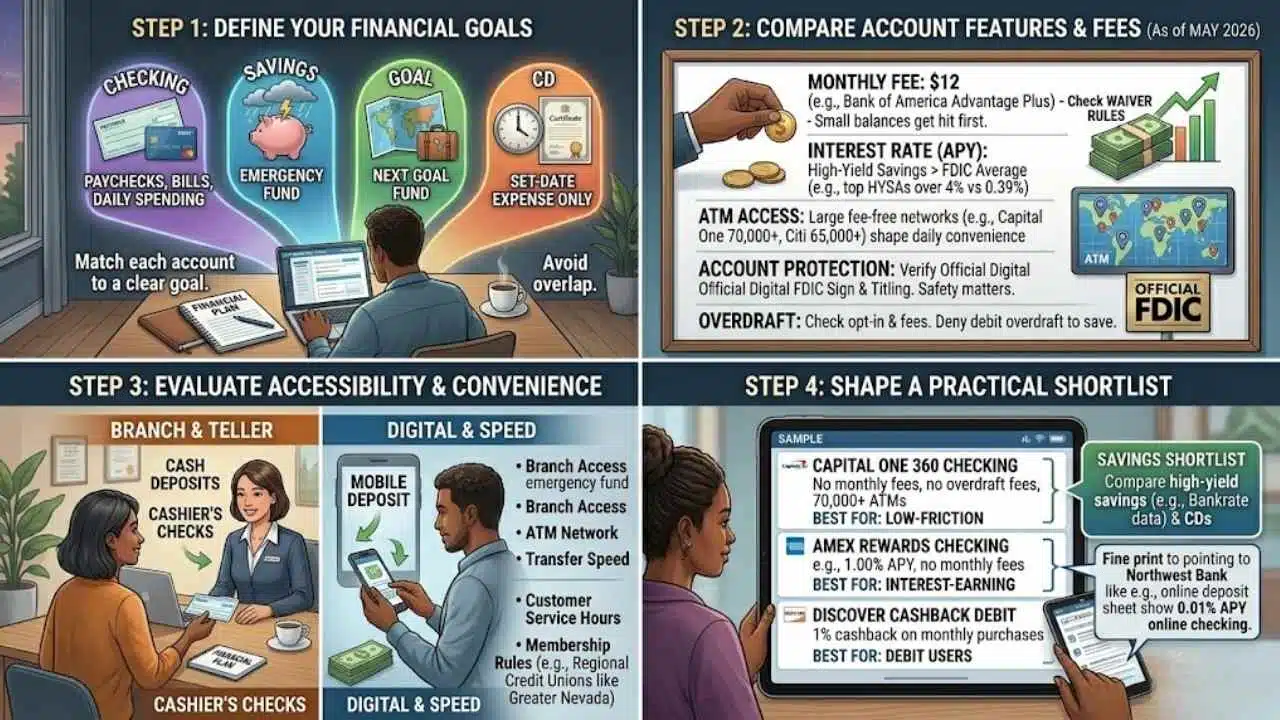

Define Your Financial Goals

Before you compare banks, decide what each dollar is supposed to do. That step keeps you from opening random account types that sound useful and then sit there overlapping each other.

- Choose one checking account for paycheck deposits, bills, and debit card spending.

- Pick one savings account for your emergency fund and keep it separate from daily spending.

- Create one next goal fund for a vacation, car repair, or annual expense.

- Use a CD only for money tied to a date you already know.

- If you share expenses, decide whether you want joint checking, separate checking, or both.

- Review your setup once a month inside your banking app so your accounts still match your financial goals.

Compare Account Features and Fees

As of May 2026, official account disclosures and major rate trackers make one thing clear: small details decide whether a bank account helps you or quietly drains you.

| Feature | What to check | Why it matters | Quick read |

|---|---|---|---|

| Monthly maintenance fee | Exact fee and waiver rules | Small balances get hit first | Bank of America Advantage Plus lists $12 monthly unless you qualify for a waiver |

| Minimum balance | Daily or average minimum needed | Missing it can wipe out interest | Some legacy accounts waive fees only if you keep a set balance all month |

| Interest rate / APY | Current APY and whether it is variable | The gap between average and top offers is huge | Top HYSAs in May 2026 were above 4%, while the FDIC national savings rate was 0.39% |

| Overdraft settings | Debit card opt-in, linked savings transfer, fee amount | One setting can save repeated fees | Declining debit overdraft coverage can cut surprise charges |

| ATM access | Fee-free network size and reimbursement policy | Cash access shapes day-to-day convenience | Capital One lists 70,000-plus fee-free ATMs and Citi lists 65,000-plus |

| Mobile and online banking | Mobile deposit, alerts, transfers, card controls, Zelle | Good tools make money management easier | Mid Penn Bank includes mobile check deposit and Zelle on checking |

| Account protection | FDIC or NCUA insurance and account titling | Safety matters more than a flashy bonus | Always verify the insurance sign and the ownership category |

| Transparency | Readable fee sheet and plain-language disclosures | Confusing terms usually cost more later | If you cannot explain the fee rules in one minute, keep shopping |

Evaluate Accessibility and Convenience

Convenience is personal. Some readers want branches and a live teller, while others would gladly trade branches for better interest rates and a stronger mobile app.

- Branch access: useful if you deposit cash, need cashier’s checks, or like in-person help.

- ATM network: crucial if you withdraw cash often or travel.

- Transfer speed: important if your emergency fund lives at a separate bank.

- Customer service hours: worth checking before fraud or a locked debit card forces the issue.

- Membership rules: some credit unions are great, but eligibility can be regional or employer-based.

This is also where local and regional financial institutions can shine. Greater Nevada Credit Union, for example, has strong digital banking tools and specialty savings options, but membership is tied to Nevada connections, so readers should always confirm access rules before assuming a credit union is open nationwide.

Many experienced savers keep at least two institutions in play, one for daily spending and one for savings. It adds a little complexity, but it can also give you backup access if one bank has an outage, fraud hold, or frozen card.

Finding High Interest or Low Fee Accounts

If you want a practical shortlist, start with accounts that make their value obvious in one sentence. That usually means low or no fees, competitive APYs, and clear digital tools.

| Example account | What stands out | Best for |

|---|---|---|

| Capital One 360 Checking | No monthly fees, no minimums, no overdraft fees, 70,000-plus fee-free ATMs | A low-friction everyday checking account |

| American Express Rewards Checking | As of May 2026, American Express lists 1.00% APY, no monthly fees, and no minimum balance | Readers who want an online checking account that still earns interest |

| Discover Cashback Debit | No monthly fee and 1% cash back on up to $3,000 in monthly debit card purchases | Debit card users who want a simple perk |

| Bank of America Advantage Plus Banking | Large branch footprint, but a $12 monthly fee unless you meet waiver rules | Readers who value in-person service and can satisfy the waiver |

| Citi checking options | Large ATM network, but service fees apply unless you meet account conditions | Readers who want wide ATM access and understand the fee rules |

Keep the same mindset with savings accounts. Bankrate can help you compare high-yield savings accounts, money market accounts, and CDs side by side, but always confirm the current rate and fee sheet on the bank’s own product page before you open anything.

Also read the fine print on interest-bearing checking. Northwest Bank’s online deposit sheet from March 24, 2026 showed 0.01% APY on its online checking products and noted balance requirements for earning that yield, which is a good example of why the words “interest-bearing” do not automatically mean “worth it.”

Enhancing Financial Success Through Bank Accounts

You do not build financial freedom by collecting random bank accounts. You build it by giving each account one clear job and reviewing it often enough that your setup keeps pace with your life.

- Account 1: one checking account for paychecks, bills, and regular spending.

- Account 2: one savings account for emergency savings.

- Account 3: one goal account, either a HYSA, money market account, or certificate of deposit, for planned expenses.

After that, only add more if the extra account solves a real problem. A joint checking account can simplify household bills, a separate sinking fund can stop annual expenses from ambushing your budget, and an HSA can keep medical money organized and tax-advantaged.

Check your rates, fees, and account features at least quarterly. If a better option shows up, move your money with purpose instead of staying loyal to an account that has stopped helping your financial plan.

The right bank accounts make money management calmer. You spend from one place, save in another, and stop asking your checking balance to tell you everything at once.

Final Thoughts

The bank accounts most readers actually need are simple: a checking account for daily spending, a savings account for an emergency fund, and then a money market account or CD only if a specific goal calls for it.

Start with the accounts that protect your cash and reduce fees. Then shop for better interest rates, clearer online banking, and account features that make your financial goals easier to reach.

If you open one account this month, make it the one that fixes your biggest gap first. For many readers, that means a fee-friendly checking account or a high-yield savings account that finally gives emergency savings a proper home.

Frequently Asked Questions (FAQs) About Essential Bank Account Types

1. What is generative AI for marketing?

Generative AI for marketing uses large language models to make ai generated content and to help create content and marketing materials.

2. How does it make marketing content?

It can automate content creation and write posts, emails, ads, and other marketing materials fast.

3. Can it help with SEO and keyword research?

Yes, marketing generative AI can help businesses identify SEO-friendly keywords, do keyword research, and support market research.

4. Can it analyze customer data and predict behavior?

Yes, it can analyze customer data, predict consumer behavior, handle customer inquiries, and power marketing automation to personalize customer interactions.

5. Do I still need humans if I use generative AI?

Yes, human oversight is important, even though generative AI promises speed; people must check accuracy, keep up to date information, and match the intended audience. Software developers can also help use generative AI to make highly realistic images or product demo videos, and to analyze data for better results.