Moving abroad is a thrilling life adventure that introduces a complex new set of financial responsibilities. One of the primary concerns for British citizens relocating overseas involves figuring out exactly what they owe to HM Revenue and Customs compared to the tax authority in their new destination. Handling these obligations incorrectly can easily lead to massive fines, missed savings opportunities, or the nightmare scenario of paying taxes twice on the exact same income.

This comprehensive guide breaks down precisely how to handle your finances across international borders with absolute confidence. From understanding your official residency status to properly leveraging international agreements, these practical steps will guide you through the process. By taking a proactive approach to your financial planning, you can remain fully compliant with the law while keeping a much larger portion of your hard earned wealth. Mastering the UK expat tax rules is the key to enjoying your new life without looking over your shoulder.

| Consideration | Description | Importance |

| Financial Obligations | Understanding what is owed to HM Revenue and Customs | High |

| Double Taxation | Paying taxes twice on the exact same income | Critical to avoid |

| Compliance | Following legal requirements in both countries | Essential |

1: Master the Statutory Residence Test

The absolute foundation of your entire tax situation rests entirely on whether the government still legally considers you a resident. The Statutory Residence Test is the official mechanism HM Revenue and Customs uses to make this crucial determination. This comprehensive assessment looks closely at exactly how much time you physically spend in the country alongside your ongoing personal and economic ties. The test is carefully split into three main parts including automatic overseas tests, automatic UK tests, and the sufficient ties test.

If you spend fewer than sixteen days in the country during a given tax year, you are usually classified immediately as a non resident. Conversely, spending one hundred and eighty three days or more firmly establishes you as a resident for tax purposes. For individuals falling somewhere in between these extremes, the authorities will closely scrutinize your family connections, property ownership, and employment to make a final binding decision.

| Test Component | Condition | Residency Result |

| Automatic Overseas | Fewer than sixteen days spent in country | Non resident |

| Automatic Resident | One hundred eighty three days or more | Resident |

| Sufficient Ties | Moderate days spent plus family or work links | Depends on specific ties |

2: Tell Authorities You Are Leaving

You cannot simply pack your bags and move overseas without formally notifying the relevant authorities about your departure. You have a strict legal obligation to inform HM Revenue and Customs about your exact moving date and future intentions. If you typically complete a Self Assessment tax return, you will need to fill out the SA109 form to officially declare your non resident status. For individuals who do not normally file a yearly return, completing form P85 is the required mandatory procedure.

This vital document lets the authorities know you are leaving and helps them calculate if you are owed a tax refund from your most recent employment. Submitting these forms promptly stops the government from sending you unexpected tax bills while you are trying to settle comfortably into your new life abroad. Handling this paperwork early is an essential part of managing your UK expat tax rules effectively.

| Form Name | User Profile | Primary Purpose |

| SA109 | Self Assessment filers | Declare non resident status |

| P85 | Standard employees | Notify departure and claim refund |

| Notification | All expats | Prevent unexpected future bills |

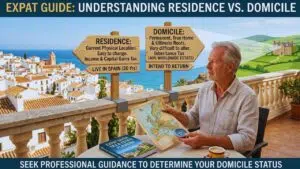

3: Learn the Difference Between Residence and Domicile

Many expats mistakenly confuse being a resident with being domiciled, but these two concepts mean drastically different things to the tax authorities. Residence is strictly about where you physically live right now, while domicile relates to where your permanent, true home is located. You could comfortably live in Spain for twenty consecutive years and be a Spanish resident, but still remain domiciled in Britain if you intend to return eventually. Your domicile status strongly and directly impacts your exposure to inheritance tax regulations.

Even if you have been living as an expat for multiple decades, maintaining a British domicile means your worldwide estate might still be subject to a massive forty percent inheritance tax upon your passing. Understanding this critical distinction allows you to plan your estate properly and protect your family wealth. It is highly recommended to seek professional guidance to determine your exact domicile status clearly.

| Legal Concept | Definition | Primary Tax Impact |

| Residence | Current physical living location | Income and capital gains |

| Domicile | Permanent home and ultimate roots | Inheritance tax exposure |

| Status Change | Very difficult to alter legally | Requires permanent severing of ties |

4: Take Advantage of Double Taxation Agreements

Absolutely no one wants to pay taxes on the exact same income twice in two separate countries. Fortunately, the government has carefully negotiated double taxation agreements with over one hundred and thirty countries to prevent this unfair scenario. These international treaties specifically dictate which country possesses the primary right to tax specific types of income like pensions, property rental yields, or standard wages. If both jurisdictions technically have the right to tax your earnings, the agreement usually permits you to claim tax relief in one nation for the taxes already paid in the other.

It is crucial to remember that you often have to apply for this beneficial relief actively because it is almost never applied automatically. You might need to secure a formal certificate of residence from your new country to prove you are actively paying local taxes there. Leveraging these agreements is a cornerstone of smart UK expat tax rules management.

| Agreement Feature | Mechanism | Benefit |

| Primary Right | Dictates which country taxes first | Creates clear rules |

| Tax Relief | Offsets taxes paid abroad | Prevents double paying |

| Active Claim | Requires formal application | Unlocks financial savings |

5: Set Up the Non Resident Landlord Scheme

Countless expats choose to keep their original domestic homes and rent them out for extra income while living abroad. If you pursue this popular strategy, you must understand that your rental income remains completely taxable in your home country regardless of where you live. If you live overseas for more than six months of the year, letting agents or tenants are legally forced to deduct basic rate tax directly from your rent before paying you.

To entirely avoid this frustrating upfront deduction and receive your rental income in full, you need to apply for the Non Resident Landlord Scheme. You must complete form NRL1 and submit it to the authorities for formal approval. You will still have to declare this rental income and pay any final tax due through an annual Self Assessment return. However, utilizing this scheme drastically improves your month to month cash flow and financial flexibility.

| Scheme Detail | Action Required | Result |

| Default Rule | Tenant or agent deducts tax | Reduced monthly cash flow |

| NRL1 Form | Apply for formal exemption | Receive rent without upfront deduction |

| Final Tax | Declare on annual return | Pay correct tax later |

6: Manage Your Pensions Carefully

Retirement funds are heavily regulated by strict laws, and relocating abroad fundamentally changes how you can interact with your existing pension pots. If you are classified as a non resident, you can typically only continue receiving beneficial tax relief on new pension contributions for up to five years after you leave. Furthermore, the total amount of relief you can claim during this five year window is usually capped at a specific limit. When the time eventually comes to withdraw your accumulated pension, the tax you owe depends entirely on the specific double taxation agreement between the two nations.

Certain countries will classify your foreign pension as standard regular income and tax it accordingly under their local laws. Conversely, other jurisdictions might offer generous tax free withdrawals or special lower rates for imported retirement funds. Always thoroughly verify the specific treaty details before cashing in any portion of your retirement savings.

| Pension Aspect | Non Resident Rule | Action Needed |

| Contributions | Relief limited to five years | Monitor time limits closely |

| Withdrawals | Governed by international treaties | Check local tax treatment |

| Taxation | Varies wildly by destination | Consult specific agreements |

7: Understand Capital Gains Tax on Property

Selling residential property while living overseas comes with incredibly strict reporting rules that you cannot ignore. You can no longer completely escape capital gains taxes simply by holding non resident status during the sale. If you sell a residential property, you are legally mandated to report the transaction and pay any Capital Gains Tax owed within exactly sixty days of the completion date. This aggressive sixty day rule applies unconditionally even if you are living abroad and even if you make zero profit on the actual sale.

The final tax bill is calculated exclusively on the gain made since April 2015 rather than the total historical gain since you originally purchased the real estate. Failing to meet this tight deadline guarantees a severe financial penalty from the authorities. Proper management of these specific UK expat tax rules is absolutely critical for property investors.

| Reporting Rule | Requirement | Consequence of Failure |

| Time Limit | Sixty days from completion | Severe automatic fines |

| Applicability | All non resident sellers | Mandatory compliance |

| Tax Calculation | Based on gains since April 2015 | Fairer baseline assessment |

8: Handle Savings Accounts Correctly

Individual Savings Accounts represent a fantastic tax free wrapper for local residents, but they lose some of their magic when you move away. You are perfectly allowed to keep your existing accounts fully open and continue benefiting from the domestic tax free interest and dividend payments. However, you are strictly prohibited from depositing any new money into these specific accounts during the tax years you qualify as a non resident. Furthermore, your newly adopted country of residence might not recognize the special tax free status of these foreign accounts at all.

This lack of recognition means you could easily end up having to pay local taxes on the interest or investment gains you generate. You must carefully evaluate whether keeping these accounts open makes logical financial sense under your new local tax regime. Sometimes moving the funds to a more locally efficient vehicle is a smarter long term strategy.

| Account Rule | Permitted Action | Restriction |

| Existing Funds | Can remain in the account | Continue earning interest |

| New Deposits | Strictly prohibited | Cannot add new money |

| Local Taxation | Destination country rules apply | May lose tax free status |

9: Keep Your Student Loan Payments on Track

Your legal obligation to repay a domestic student loan absolutely does not vanish simply because you cross an international border. The Student Loans Company fully expects you to continue making regular monthly payments while you are living and working overseas. You are required to diligently fill out an Overseas Income Assessment form so the organization can properly calculate your new obligations. This precise calculation is based entirely on your new foreign salary and the official cost of living index in your specific destination country.

The minimum repayment threshold changes significantly depending on exactly where in the world you decide to live. If you attempt to ignore this responsibility, the company will aggressively charge penalty interest rates on your balance. They also possess the legal authority to take severe court action to recover the money owed, which can ruin your financial reputation.

| Loan Requirement | Action | Penalty for Ignoring |

| Notification | Submit Overseas Income Assessment | Account falls into arrears |

| Repayment | Continue monthly payments | High penalty interest rates |

| Threshold | Adjusted based on destination | Potential legal action |

10: Decide on Voluntary National Insurance

National Insurance contributions serve as the fundamental building blocks that pay for your future state pension and other vital social benefits. When you move abroad permanently or temporarily, your mandatory payroll contributions usually stop immediately. To eventually qualify for a full state pension, you currently need to accumulate thirty five full qualifying years on your record. If moving abroad creates a damaging gap in your contribution history, you have the option to make voluntary Class 2 or Class 3 payments.

Choosing to make these voluntary payments is an excellent way to keep your record completely topped up and secure your future. Class 2 contributions in particular are incredibly affordable if you are actively working in a foreign country. This strategy is universally considered one of the smartest and most reliable financial investments any expat can make for their golden years.

| Contribution Type | Cost | Benefit |

| Mandatory | Stops upon leaving | Not applicable |

| Class 2 Voluntary | Very affordable if working abroad | Builds state pension years |

| Class 3 Voluntary | More expensive option | Fills gaps if not working |

11: Track Your Days Meticulously

If your official non resident status depends heavily on keeping your return visits below a certain numerical threshold, casually guessing your travel dates is a massive risk. The tax authorities possess the power to launch a deep investigation into your residency status many years after the tax year has ended. You will need absolute, irrefutable proof of exactly where you were located on any given day during the period in question. It is strongly advised to maintain a highly detailed spreadsheet logging your flights, boarding passes, train tickets, and hotel bookings.

Even simple credit card receipts showing local purchases can serve as excellent supporting evidence during a formal audit. A day typically counts as a full day in the country if you are physically present there at midnight. Keeping incredibly tight records is the only guaranteed way to save yourself from unexpected and devastating tax bills down the line.

| Record Keeping | Evidence Type | Purpose |

| Travel Logs | Boarding passes and flight tickets | Prove entry and exit dates |

| Financial Proof | Credit card receipts | Prove physical location |

| Midnight Rule | Presence at end of day | Determines day count |

12: File Your Self Assessment on Time

Even if you are currently living on the opposite side of the planet, strict domestic tax deadlines still apply to your financial affairs. The official tax year runs rigidly from April 6 to April 5 the following calendar year without exception. If you have any ongoing domestic income to declare, such as property rental yields, you must file your return promptly. You are required to submit this online return by January 31 following the immediate end of the relevant tax year.

Because you are an expat, you cannot utilize the standard free online software provided by the government to file a non resident return. You must purposefully acquire specialized commercial software or hire a qualified professional accountant to handle the submission. Missing this critical deadline triggers an immediate automatic fine, even if you ultimately do not owe a single penny in taxes.

| Filing Requirement | Deadline | Consequence of Missing |

| Online Return | January 31 | Immediate automatic fine |

| Paper Return | October 31 | Escalating financial penalties |

| Filing Method | Commercial software required | Cannot use standard portal |

13: Hire a Cross Border Tax Specialist

Navigating the complex maze of tax laws is difficult enough when dealing with just one single country. When you attempt to combine the intricate tax codes of two entirely different nations, the risk of making an incredibly expensive mistake skyrockets exponentially. A standard high street accountant in your home country might not understand the specific local laws of your new destination at all. Similarly, a local accountant in your new city will almost certainly lack any meaningful knowledge regarding UK expat tax rules.

You urgently require an experienced advisor who specializes specifically in cross border taxation for your exact jurisdiction pairing. This dedicated professional can optimally structure your financial assets and ensure you actively claim every single treaty relief available to you. Investing in expert advice pays for itself by preventing catastrophic errors and handling the stressful paperwork on both sides of the border flawlessly.

| Advisor Type | Knowledge Base | Suitability for Expats |

| Domestic Accountant | Home country only | High risk of missing foreign rules |

| Foreign Accountant | Destination country only | High risk of missing domestic rules |

| Cross Border Specialist | Both jurisdictions and treaties | Optimal protection and planning |

Final Thoughts

Managing your finances while living abroad does not have to be an overwhelming burden if you take the right preparatory steps early on. By thoroughly understanding your residency status and taking full advantage of international double taxation treaties, you can legally protect your hard-earned money from unnecessary deductions. It is always a much smarter strategy to proactively inform the authorities about your move rather than waiting for an unexpected audit to catch you completely off guard. Keeping immaculate, daily records of your travel dates and financial transactions will serve as your absolute strongest defense if your status is ever officially questioned in the future.

Remember that seeking professional guidance from a dedicated cross-border specialist is a brilliant investment that easily pays for itself by preventing catastrophic mistakes. Mastering the UK expat tax rules ultimately empowers you to fully embrace and enjoy your exciting new international lifestyle with complete peace of mind. Careful and deliberate planning guarantees your wealth remains entirely secure across multiple jurisdictions for many years to come.