Navigating the world of federal taxes can feel like a maze, especially when we are talking about what happens to your assets after you pass away. For 2025, we have seen some significant bumps in the numbers that dictate how much you can leave to your heirs tax free. These thresholds are at historic highs right now but there is a major ticking clock that every wealthy family needs to understand. Let us break down the essential numbers you need to know for this specific tax year.

How We Selected Our 7 Best US Estate Tax Thresholds 2025 Facts

To pick the most important facts for this year we looked at the current IRS inflation adjustments and the looming legislative deadlines. We prioritized information that has the biggest impact on immediate estate planning and long term wealth transfer strategies. We also made sure to include the specific dollar amounts that will trigger a tax bill for most American families.

7 US estate tax thresholds 2025 Facts Every Taxpayer Needs

Understanding these specific rules can save your heirs millions of dollars in unnecessary tax payments. Here are the most critical updates for the 2025 tax year.

1. The Individual Exemption Amount Is $13.99 Million

The IRS has officially raised the individual lifetime exemption limit to nearly 14 million dollars for 2025. This is the total amount of money and property you can give away during your life or at your death without being hit by the federal estate tax. It represents a significant jump from previous years and provides a massive window for high net worth individuals to protect their wealth. If your total estate is under this number you generally do not have to worry about the federal tax bill.

Key Limit: $13,990,000 for individual filers.

Why We Chose It:

-

This is the primary number that determines whether your estate is taxable or not.

-

It reflects the latest inflation adjustments provided by the federal government.

-

Understanding this base limit is the starting point for every estate plan.

Things to consider:

-

Total estate value includes your home, life insurance policies, and retirement accounts.

While the individual number is high the benefit for married couples is twice as large.

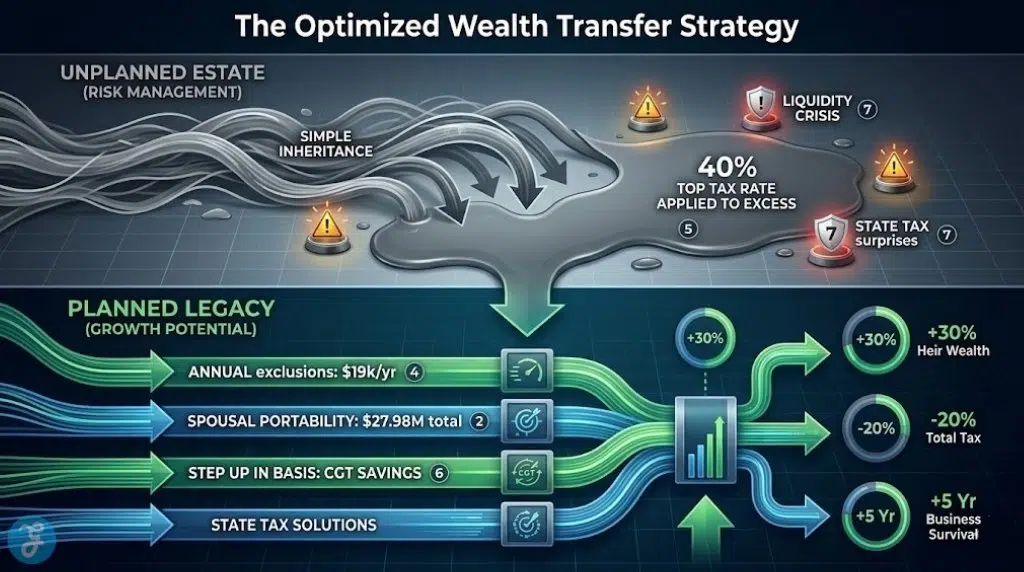

2. Married Couples Can Shield $27.98 Million

Federal law allows married couples to combine their individual exemptions to protect a massive amount of wealth. In 2025 a husband and wife can collectively pass down nearly 28 million dollars to their children or other heirs completely tax free. This is made possible through a rule called portability which allows a surviving spouse to use any leftover exemption from their partner. It is one of the most powerful wealth transfer tools available in the US tax code.

Key Limit: $27,980,000 for married couples.

Why We Chose It:

-

Most high net worth planning centers around maximizing this combined threshold.

-

Portability ensures that the first spouse’s exemption is not wasted if they die early.

-

It allows for massive multi generational wealth transfers without government intervention.

Things to consider:

-

You must file a specific tax return after the first spouse dies to claim the portability benefit.

Even with these high limits you need to be aware of the upcoming legislative cliff.

3. The 2025 Sunset Clause Is Fast Approaching

The current record high thresholds are not permanent and are scheduled to expire at the end of 2025. This is known as the sunset provision of the Tax Cuts and Jobs Act of 2017. Unless Congress passes new legislation the exemption limits will drop by about half starting on January 1 2026. This means that an estate that is currently tax free could suddenly owe millions of dollars in taxes just by waiting a few months too long.

Key Date: December 31 2025.

Why We Chose It:

-

This is the most urgent piece of news for anyone with an estate over 7 million dollars.

-

It creates a “use it or lose it” scenario for the current high exemptions.

-

Planning for the sunset takes months or even years of legal preparation.

Things to consider:

-

Gift tax rules allow you to use the high exemption now even if the limits drop later.

Giving money away while you are still alive can also help reduce your taxable estate.

4. Annual Gift Tax Exclusion Hits $19,000

In addition to the multi million dollar lifetime limit you can also give smaller amounts to individuals every year without any paperwork. For 2025 this annual exclusion has increased to 19 thousand dollars per recipient. This means you and your spouse could give a child 38 thousand dollars in a single year without touching your lifetime exemption. It is a simple and effective way to slowly move money out of your estate over time.

Key Limit: $19,000 per person per year.

Why We Chose It:

-

It is the easiest way for families to reduce their taxable estate without complex trusts.

-

There is no limit on how many people you can give this amount to each year.

-

These gifts do not require you to file a gift tax return with the IRS.

Things to consider:

-

Payments made directly to medical providers or schools for tuition do not count toward this limit.

If you do go over these limits the tax rates are quite steep.

5. Top Federal Estate Tax Rate Remains 40 Percent

If your estate exceeds the 2025 thresholds the portion above the limit is subject to a flat tax rate. Currently the top federal estate tax rate is 40 percent which can take a massive bite out of a family’s inheritance. This tax is typically due within nine months of the date of death which can create a liquidity crisis if the estate consists mostly of real estate or a family business. Proper planning usually involves finding ways to pay this bill without selling off family assets.

Tax Rate: 40 percent on the taxable portion.

Why We Chose It:

-

It highlights why planning is so critical for families near the threshold.

-

This is one of the highest tax rates in the entire federal system.

-

Knowing the rate helps you calculate the potential “cost” of failing to plan.

Things to consider:

-

Some states have their own estate taxes that are separate from the federal rate.

While the tax is high there are rules that help heirs when they eventually sell inherited property.

6. Step Up In Basis Provides Massive Capital Gains Savings

When you inherit an asset its tax “basis” is adjusted to its current market value on the date of the original owner’s death. This is known as a step up in basis and it can save heirs a fortune in capital gains taxes. For example if you inherit a house that was bought for 100 thousand dollars but is worth 1 million today your new basis is 1 million. If you sell it immediately you owe zero capital gains tax.

Term: Step Up in Basis.

Why We Chose It:

-

It is often more valuable than the estate tax exemption itself for many families.

-

It encourages families to hold onto appreciated assets until death.

-

It works regardless of whether the estate is large enough to pay estate taxes.

Things to consider:

-

This rule does not apply to assets held in certain types of irrevocable trusts.

Finally we must consider that state laws can be much stricter than federal laws.

7. State Level Estate Tax Thresholds Are Often Lower

Many people assume they are safe because their estate is under the 14 million dollar federal limit but their state might feel differently. There are 12 states and the District of Columbia that have their own estate taxes with much lower thresholds. In places like Oregon or Massachusetts the tax can kick in on estates as small as 1 or 2 million dollars. You must check your specific state laws to ensure you are not leaving a surprise bill for your family.

Term: State Estate Tax.

Why We Chose It:

-

This is a common trap for people living in high tax states.

-

State taxes are often ignored until it is too late to plan around them.

-

It creates a double tax burden for some very wealthy individuals.

Things to consider:

-

Some states have an inheritance tax which is paid by the person receiving the money.

To help you keep these numbers straight we have organized them into a quick reference guide.

An Overview Of 7 US estate tax thresholds 2025

The 2025 tax year is a unique window of opportunity for wealthy families before the laws change significantly.

Overview Comparison Table

Below is a breakdown of the key figures and dates you need to keep in mind for your 2025 planning.

| Tax Provision | 2025 Threshold | Impact Level | Strategy Type |

| Individual Lifetime Exemption | $13,990,000 | High | Lifetime Planning |

| Married Couple Exemption | $27,980,000 | High | Spousal Portability |

| Annual Gift Exclusion | $19,000 | Low | Immediate Gifting |

| Top Federal Tax Rate | 40% | Critical | Asset Protection |

| Sunset Provision | Dec 31 2025 | Urgent | Legacy Strategy |

While all of these facts are important three of them stand out as the most critical for immediate action.

Our Top 3 Picks and Why?

-

The 2025 Sunset Clause: This is our number one pick because it represents a hard deadline that will change the financial lives of millions of people overnight if they do not act.

-

The Individual Exemption Amount: We chose this as the runner up because it is the fundamental number that determines who needs to plan and who does not.

-

Step Up In Basis: This takes the third spot because it provides a massive tax break for almost every American family regardless of their total wealth.

Now that you know the rules let us look at how you can apply them to your own situation.

Buyer’s Guide: How to Choose the Right US estate tax thresholds 2025 Strategy?

Choosing a strategy depends entirely on where your total net worth sits relative to these historic limits. You should not treat a 5 million dollar estate the same way you treat a 30 million dollar estate.

Here is the general framework for deciding how much you need to worry about estate taxes:

-

The Valuation Test: Calculate the current fair market value of everything you own including businesses and life insurance.

-

The Location Test: Determine if you live in a state with its own independent estate or inheritance tax.

-

The Time Test: Decide if you want to use your exemption now while it is high or wait and risk the 2026 sunset.

To help you decide which path to take we have created a simple decision matrix.

| Choose this strategy… | If your primary financial situation is… |

| Simple Annual Gifting if… | Your estate is well below the 14 million dollar limit but you want to help heirs now. |

| Aggressive Lifetime Giving if… | Your estate is over 7 million dollars and you want to “lock in” the 2025 exemption. |

| Spousal Portability Filing if… | You are a surviving spouse who wants to protect their partner’s unused exemption. |

| Irrevocable Trust Planning if… | You want to remove highly appreciated assets from your taxable estate forever. |

Before you meet with an attorney you should have a few things ready.

The Final Checklist:

-

Gather a complete list of all assets and their current estimated market values.

-

Review all life insurance policies to see if they are owned by you or a trust.

-

Check the beneficiary designations on all your retirement accounts.

-

Determine your state’s specific estate tax threshold and current tax rates.

-

Schedule a meeting with an estate planning attorney before the mid 2025 rush.

Securing Your Family Legacy

The 2025 tax year is essentially the final call for the highest estate tax exemptions we have ever seen in American history. By understanding these thresholds and the looming sunset clause you can take proactive steps to keep your hard earned wealth within your family. Whether you are gifting small amounts annually or setting up complex trusts the key is to move before the calendar turns to 2026.