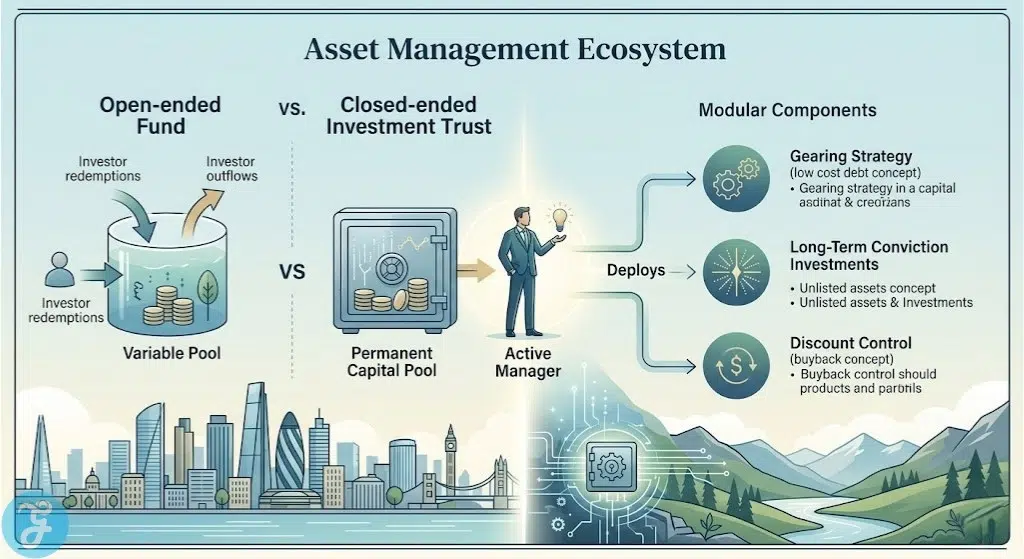

The UK investment trust sector in 2026 is at a historic inflection point. Following a prolonged period where many trusts traded at significant discounts to their underlying assets, a series of regulatory breakthroughs and shifting interest rate expectations have created a unique window for savvy investors. While the broader market has been volatile, the closed-ended structure of investment trusts continues to provide tools—such as gearing and income reserves—that are simply unavailable to standard open-ended funds.

Strategic Foundations for 2026 Investment Trust Selection

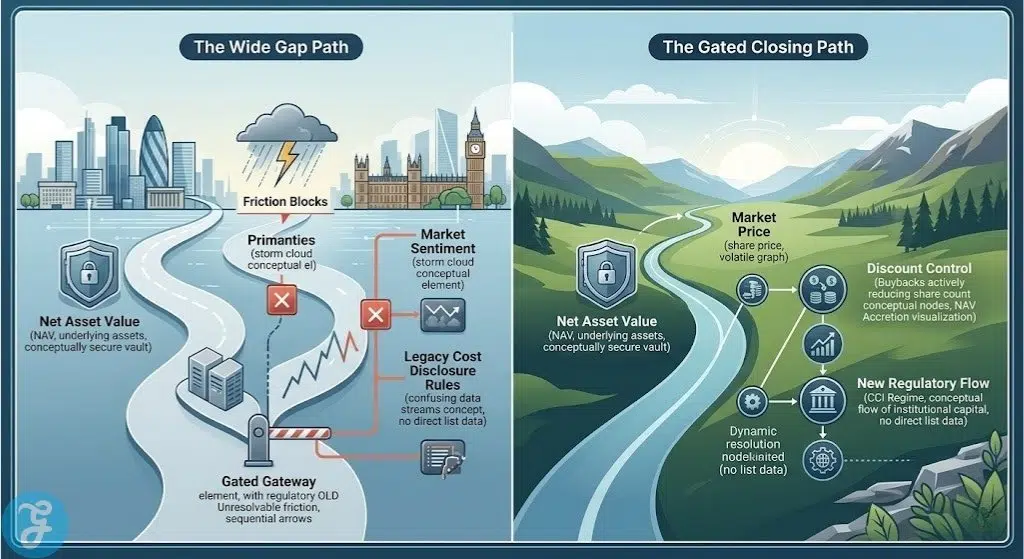

To identify the most effective strategies for the current year, we analyzed the impact of the Financial Conduct Authority’s (FCA) recent cost-disclosure reforms alongside the performance of the “Dividend Heroes” during the late-2025 inflationary blip. Our selection focuses on maximizing the structural advantages of trusts, specifically targeting the narrow “Gated” connection between share price and Net Asset Value (NAV) that currently defines the UK market.

We utilized the following benchmarks to evaluate the best tactical approaches for 2026.

-

Discount Volatility: Prioritizing trusts with active buyback programs or Discount Control Mechanisms (DCM).

-

Revenue Reserve Strength: Assessing the ability of trusts to maintain dividend growth even during earnings fluctuations.

-

Gearing Efficiency: Evaluating how trusts are using borrowed capital to amplify returns as interest rates begin their projected 2026 decline.

-

Regulatory Alpha: Analyzing the impact of the new Consumer Composite Investments (CCI) regime on fund-of-fund inflows.

By filtering these developments through the lens of the 2026 economic recovery, we identified seven expert strategies for navigating the current trust landscape.

7 Expert Strategies for UK Investment Trusts in 2026

The current era of trust investing is defined by a shift from “defensive survival” to “opportunistic growth.” These seven tips provide the strategic roadmap needed to capitalize on the structural efficiencies of the UK’s unique investment trust market.

The most significant change in recent years involves how costs are reported to the end investor.

1. Capitalize on the Cost Disclosure Regulatory Pivot

As of April 6, 2026, the UK has officially entered the optional transition period for the new Consumer Composite Investments (CCI) regime. This reform effectively ends the “double counting” of investment trust costs that previously deterred many multi-asset fund managers. By allowing ongoing charges to be reflected primarily in the share price rather than as a separate “pulled-through” expense, many trusts are now more attractive to professional wealth managers, potentially driving a wave of new institutional demand.

Best for: Investors looking to “front-run” institutional inflows as professional fund-of-fund managers return to the sector.

Why We Chose It:

-

It removes a major artificial barrier that has kept many trusts at double-digit discounts for years.

-

The transparency of the new regime makes it easier to compare trusts against standard ETFs and unit trusts.

-

It specifically benefits sectors like infrastructure and private equity that were hardest hit by old disclosure rules.

Things to consider: The full “wall of money” expected from this change may take several quarters to manifest as discretionary managers rebalance.

While regulatory changes provide a tailwind, the underlying valuations in the UK market offer a secondary “value gap” to exploit.

2. Target the “Double Discount” in Domestic Small-Caps

In 2026, UK small and mid-cap companies continue to trade at lower price-to-earnings multiples than their global peers, despite a robust domestic recovery. When you buy a UK Smaller Companies investment trust, you are often buying a basket of already-cheap stocks at a further discount to their Net Asset Value (NAV). This “double discount” offers a significant margin of safety and a higher potential for capital appreciation as the UK economy outpaces early-2026 G7 growth estimates.

Best for: Growth-oriented investors who want exposure to a domestic UK recovery at a significant valuation entry point.

Why We Chose It:

-

Domestic UK firms have lagged behind the FTSE 100 rally, creating a clear “catch-up” potential.

-

Investment trusts in this sector often have long-tenured managers who understand the intrinsic value of small-cap niche leaders.

-

Small-cap trusts typically use gearing effectively to boost returns during the early stages of a bull market.

Things to consider: Small-cap trusts can be highly volatile during periods of geopolitical uncertainty or sudden currency fluctuations.

The ability to use debt is one of the primary structural advantages of the trust model over standard funds.

3. Leverage Gearing as a Tactical Recovery Tool

As the Bank of England continues to signal rate cuts throughout 2026, the cost of borrowing for investment trusts is falling. Trusts use gearing (borrowing to invest) to amplify their exposure to the market. In a rising market, a geared trust will significantly outperform its non-geared peers. The expert move this year is to identify trusts that have successfully locked in low-cost, long-term debt while the market was at the bottom, setting them up for outsized gains during the recovery.

Best for: Investors with a higher risk tolerance who want to maximize their returns during a projected market upswing.

Why We Chose It:

-

Gearing allows the trust to own more assets than its share capital would normally permit.

-

Falling interest rates reduce the “drag” of debt, making the gearing more accretive to shareholders.

-

It is a structural feature that open-ended funds (OEICs) cannot replicate.

Things to consider: Gearing works in reverse during a market downturn, magnifying losses just as effectively as it magnifies gains.

For income-focused investors, the track record of a trust is more than just a marketing statistic.

4. Monitor the “Dividend Hero” Multi-Year Cushion

The Association of Investment Companies (AIC) “Dividend Heroes” are trusts that have increased their payouts for 20 or more consecutive years. In 2026, these trusts are utilizing their revenue reserves—money set aside during good years—to maintain dividend growth despite the inflationary pressures of 2025. This “smoothing” effect provides a level of income certainty that is particularly valuable for retirees or those building a passive income stream.

Best for: Income-seeking investors who require a predictable and growing yield to combat long-term inflation.

Why We Chose It:

-

Trusts can hold back up to 15 percent of their annual income to support dividends in leaner years.

-

The list includes several trusts with over 50 years of consecutive annual increases.

-

This feature makes them arguably the most reliable income vehicles in the UK financial landscape.

Things to consider: A high yield is not a guarantee of capital growth; some high-yielding trusts may see their NAV erode over time.

Not all trusts allow their share price to drift too far from the value of their holdings.

5. Prioritize Active Discount Control Mechanisms (DCM)

The wide discounts seen across the sector in 2024 and 2025 have led many boards to implement aggressive Discount Control Mechanisms (DCM). These mechanisms, often involving mandatory share buybacks, aim to keep the share price trading within a tight range of the NAV (usually within 5 percent). Investing in a trust with a proven DCM reduces the “discount risk”—the danger that a good investment in underlying assets is ruined by a widening gap in the share price.

Best for: Cautious investors who want to minimize the technical volatility associated with closed-ended funds.

Why We Chose It:

-

It provides a “floor” for the share price, as the trust will buy back shares if the discount widens too far.

-

Buybacks at a discount are actually “NAV-accretive,” meaning they increase the value for remaining shareholders.

-

It signals a board that is highly proactive and aligned with shareholder interests.

Things to consider: A DCM can be suspended in extreme market conditions if the trust needs to preserve cash.

The alternative asset space provides higher yields but requires a careful eye on the regulatory environment.

UK infrastructure trusts entered 2026 trading at massive discounts—some exceeding 30 percent—and offering yields as high as 10 percent. While these are attractive, experts are watching the government’s ongoing consultation on energy subsidies. The tip for 2026 is to favor “core” infrastructure (like social housing or transport) over purely renewable energy trusts until the subsidy framework is fully clarified, ensuring your high yield isn’t undermined by a policy shift.

Best for: Yield-hungry investors who are comfortable with the complexity of private and physical assets.

Why We Chose It:

-

Infrastructure assets often have inflation-linked contracts, providing a natural hedge.

-

The current discounts are among the widest in the history of the asset class.

-

The physical nature of the assets provides a diversification benefit away from traditional stocks and bonds.

Things to consider: These trusts are sensitive to long-term gilt yields; if interest rates stay higher for longer, these trusts may struggle to recover.

The final strategy involves using the trust structure to gain access to companies that aren’t on the stock market.

7. Utilize Private Equity Trusts for Liquid Access to Growth

Private equity has traditionally been the domain of large institutional investors, but investment trusts like Pantheon International or HarbourVest provide a liquid way for individuals to participate. In 2026, many of these trusts still trade at substantial discounts because the market is skeptical of their internal valuations. However, for long-term investors, this is the most effective way to capture the “illiquidity premium” of private companies while maintaining the ability to sell your shares on the London Stock Exchange.

Best for: Long-term investors looking for high-growth potential outside of the standard FTSE or S&P 500 indices.

Why We Chose It:

-

Private equity has historically outperformed public markets over 10 and 20-year horizons.

-

The trust structure is the only way for retail investors to access these sophisticated managers.

-

Active management in this sector involves helping companies grow, not just picking stocks.

Things to consider: The “lumpy” nature of private equity exits means performance can be flat for years before a sudden spike.

Comparing Trust Strategies in the 2026 Recovery

The choice between different investment trust sectors depends heavily on whether you prioritize immediate income, capital protection, or long-term growth. The table below compares the primary trust categories available to UK investors this year.

The following data summarizes the current average metrics across the most popular AIC sectors.

| Strategy Category | Avg. Discount (Apr 2026) | Avg. Yield | Primary Driver | Best Feature |

| UK Smaller Companies | 12.5% | 2.8% | Domestic Recovery | Double Discount |

| Dividend Heroes | 4.2% | 4.5% | Income Smoothing | 20+ Year Record |

| Infrastructure | 28.0% | 8.2% | Asset Revaluation | Inflation Linkage |

| Private Equity | 31.0% | 1.5% | Portfolio Exits | Unlisted Growth |

| Global Equity | 5.5% | 1.8% | World Tech/Growth | Diversification |

Our Top 3 Critical Selection Factors and Why?

While the entire sector is offering value, these three factors will determine which investors see the most significant gains in the second half of 2026.

-

Management of the Discount: The gap between price and NAV is where the “free lunch” exists, but only if the board has a clear plan to close it.

-

Gearing Strategy: In a falling interest rate environment, trusts with clever gearing will pull ahead of the pack.

-

Regulatory Flow: The FCA’s CCI regime is a “coiled spring” for the sector; those positioned before the institutional money returns will benefit most.

How to Audit Your Investment Trust Portfolio?

Reviewing your trust holdings in 2026 requires a focus on structural health rather than just looking at the share price chart. A healthy trust should be transparent about its debt and its efforts to manage its own valuation.

-

Check the Gearing Level: Ensure the trust isn’t over-leveraged (usually above 20%) if you are worried about market volatility.

-

Evaluate the Buyback History: Look at the RNS announcements to see if the board has actually been buying back shares during the recent period of wide discounts.

-

Review the Revenue Reserves: For income trusts, check how many years of dividends the trust has in the “bank” to ensure your payout is secure.

-

Look at the “Look-Through” Cost: Under the new CCI rules, verify the total cost of the trust including its management fee and transactional costs.

The following table can help you decide which trust type fits your current 2026 financial goals.

| Choose a “Dividend Hero” if… | Choose a “Private Equity” Trust if… |

| You are in or near retirement and need reliable cash. | You have a 10-year horizon and want max growth. |

| You want to avoid the “lumpiness” of market cycles. | You are comfortable with wide price swings. |

| You value a proven, conservative board of directors. | You want to own the “next big thing” before it IPs. |

The Final Trust Checklist

-

[ ] Verify the current discount to NAV using the AIC website (theaic.co.uk).

-

[ ] Check if the trust has adopted the optional CCI cost-disclosure format.

-

[ ] Review the last annual report for the “manager’s review” of the gearing strategy.

-

[ ] Ensure the trust is held within a tax-efficient wrapper like a Stocks & Shares ISA.

-

[ ] Compare the trust’s performance against its specific benchmark, not just the FTSE 100.

Capitalizing on the Closed-Ended Advantage

The UK investment trust market in 2026 offers one of the most compelling risk-reward profiles in recent memory. By utilizing Expert Tips for UK Investment Trusts, you are shifting from a passive observer to an active participant in a sector that is designed to protect and grow capital through structural superiority. Whether you are hunting for 10 percent yields in infrastructure or 30 percent discounts in private equity, the key to success is understanding that in the world of trusts, the share price is only half the story.

Frequently Asked Questions About UK Investment Trusts

Why do investment trusts trade at a discount?

Answer: This happens when there is more selling pressure on the shares than there is demand, causing the share price to fall below the value of the underlying assets.

What is the difference between an investment trust and a unit trust?

Answer: An investment trust is a public company with a fixed number of shares (closed-ended), whereas a unit trust creates or cancels units based on investor demand (open-ended).

Can I lose more than I invest if a trust is geared?

Answer: No, as a shareholder in a public company, your liability is limited to the amount you invested; you cannot be held responsible for the trust’s debts.

What happens to trusts when interest rates fall?

Answer: Generally, falling rates are positive for trusts as it reduces the cost of gearing and makes their yields more attractive compared to cash.

Answer: You buy them exactly like any other company share through an online broker, platform, or app using the trust’s unique ticker symbol.