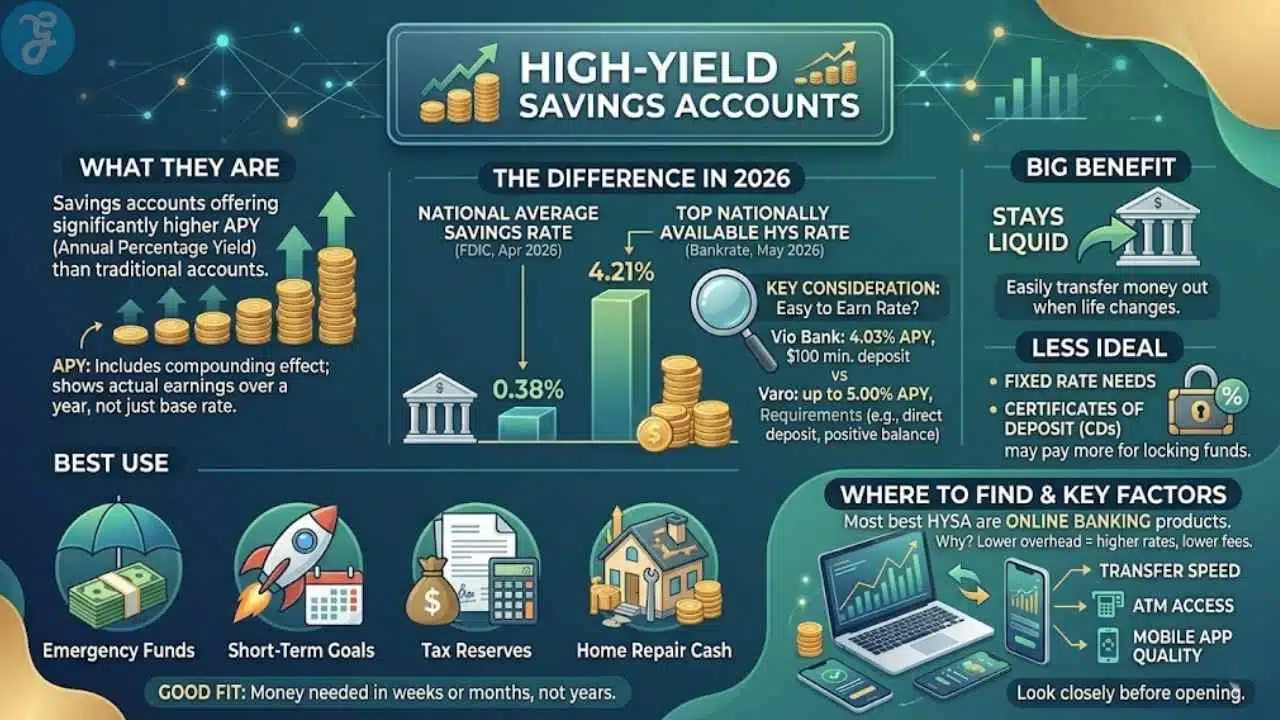

Are you still earning almost nothing while high-yield savings accounts keep paying real interest? If that sounds familiar, you are in the right place. FDIC data for April 2026 puts the national average savings rate at 0.38%, while the best nationally available online accounts are still paying well above that.

This guide breaks down the best picks, the tradeoffs that matter, and the account features that make daily banking easier.

What Are High-Yield Savings Accounts?

High-yield savings accounts give your cash a better APY without locking it away like a CD. A high-yield savings account is a savings account that pays a much stronger APY (annual percentage yield) than a traditional savings account. APY includes the effect of compounding, so it shows what you can actually earn over a year, not just the base interest rate.

That difference is not small in 2026. FDIC data for April 2026 shows the national average savings rate at 0.38%, while Bankrate’s May 2026 roundup put the top nationally available rate at 4.21%.

The key thing to watch is whether the headline rate is easy to earn. Vio Bank lists 4.03% APY with a $100 minimum opening deposit, while Varo advertises up to 5.00% APY only if you receive at least $1,000 in direct deposits and finish the month with a positive balance across your Varo accounts.

- Best use: emergency funds, short-term savings goals, tax reserves, and home repair cash.

- Good fit: money you may need in weeks or months, not years.

- Less ideal: money you want to lock at a fixed rate, where certificates of deposit may pay more.

- Big benefit: your balance stays liquid, so you can transfer money out when life changes.

Most of the best high-yield savings accounts are online banking products. That is usually why they can keep rates higher and fees lower, but it also means you need to look closely at transfer speed, ATM access, and mobile app quality before you open one.

How to Choose the Best High-Yield Savings Account

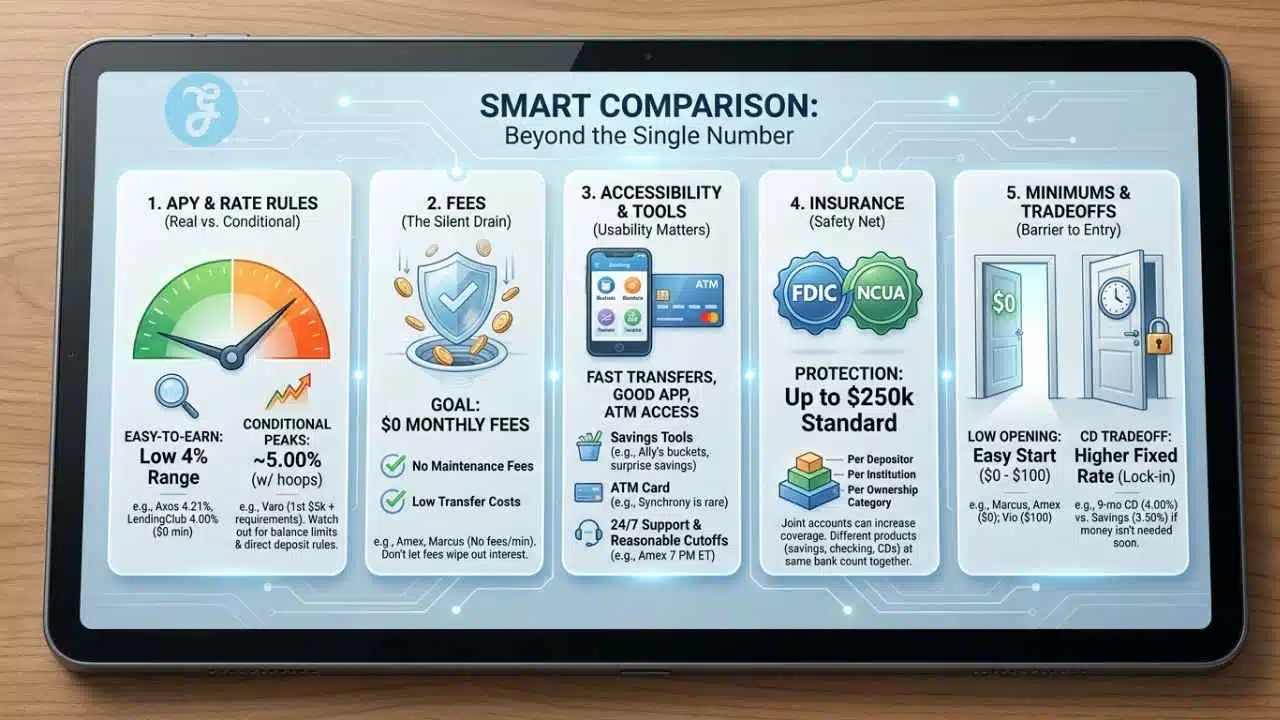

The smartest way to compare savings accounts is to stop chasing one number in isolation. A strong APY matters, but so do fees, transfer rules, customer support, and how easy it is to reach your money when you need it.

| What to compare | Why it matters | What stands out in 2026 |

|---|---|---|

| APY and rate rules | A high rate helps your cash grow faster, but only if it is easy to qualify for. | Top easy-to-earn rates are in the low 4% range, while some 5.00% offers come with direct deposit and balance conditions. |

| Fees | Monthly fees can wipe out a good chunk of your interest earnings. | The strongest picks on this list avoid monthly fees and keep transfer costs low. |

| Access | Fast transfers, a good app, and ATM access can matter more than a few tenths of a percent. | Ally leads on savings tools, and Synchrony is rare because it offers an ATM card for its HYSA. |

| Insurance | FDIC or NCUA coverage protects your deposits if the institution fails. | The standard protection is still up to $250,000 per depositor, per institution, per ownership category. |

| Minimums | A low opening requirement makes it easier to start now and add more later. | Many top accounts now open with $0, but a few strong APY leaders still ask for $100. |

Competitive APY rates

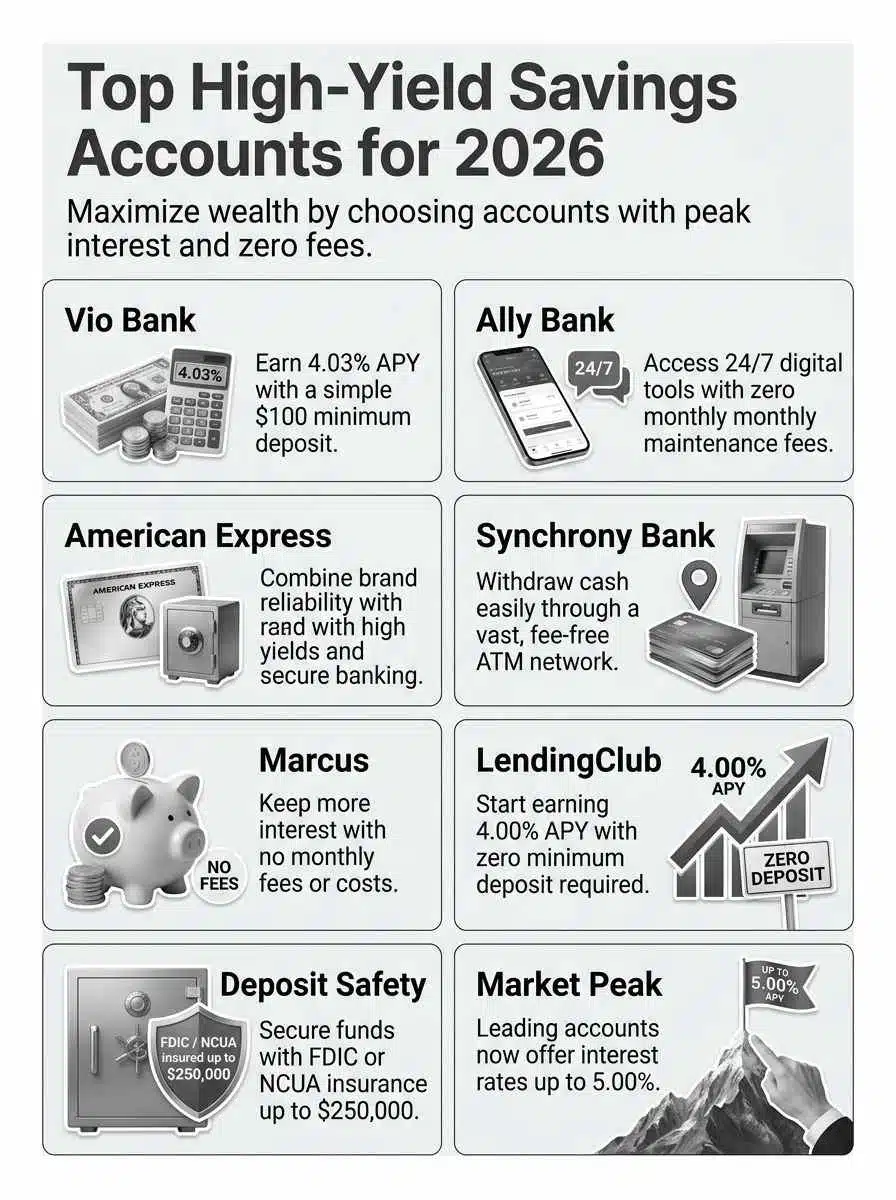

If your main goal is pure yield, look at the real, easy-to-earn rate first. Bankrate’s May 2026 roundup showed Axos Bank at 4.21% APY, Vio Bank at 4.03% APY with a $100 minimum deposit, and LendingClub Bank at 4.00% APY with no minimum deposit.

This is also where many readers get tripped up. Some banks advertise a great top-line number, but the best rate may apply only to a limited balance or after you meet direct deposit rules. Varo’s 5.00% APY is a good example, it applies only to the first $5,000 after you meet its monthly requirements.

Low or no fees

A high APY loses some of its shine if the account chips away at your balance every month. That is why no monthly fees matter so much for personal finance, especially if you are building an emergency fund or saving in smaller chunks.

American Express states that its High Yield Savings account has no fee to open, no minimum deposit, and no monthly fees. Marcus by Goldman Sachs is just as clean on this front, with no fees and no minimum deposit as of May 8, 2026.

Accessibility and ease of use

This is the part many rate tables miss. The best account on paper can still feel annoying if transfers take too long, the app is clunky, or you cannot get cash without jumping through hoops.

Ally is especially strong here because it gives you up to 10 savings buckets, automated boosters, 24/7 customer service, and up to 10 limited withdrawals or transfers per statement cycle. Its Surprise Savings tool can even sweep up to $25 at a time from a linked checking account on Mondays, Wednesdays, and Fridays.

American Express keeps the process simple too, but its cutoff matters. The bank says transfers started after 7:00 p.m. Eastern, or on non-business days, begin processing on the next business day.

FDIC or NCUA insurance

Insurance is the part you hope you never need, but you still want it right. FDIC coverage at banks and NCUA coverage at federally insured credit unions both protect deposits up to standard limits, and those limits depend on how your accounts are titled.

For most readers, the practical takeaway is simple: keep no more than $250,000 in the same ownership category at one bank unless you have confirmed how your coverage stacks. Joint accounts can increase protection because each owner gets separate coverage under the rules.

- Single account: up to $250,000 per depositor.

- Joint account: up to $250,000 per owner at the same institution.

- Different banks: coverage applies separately at each insured institution.

- Different products: savings, checking, and CDs at the same bank may count together within the same ownership category.

Minimum deposit and balance requirements

Low minimums make it easier to start, but they also tell you what kind of saver the bank is built for. Vio Bank asks for $100 to open, while Marcus by Goldman Sachs, American Express, and several other major picks let you start with $0.

If you are also comparing certificates of deposit (CDs), this is where the tradeoff gets real. Marcus listed its online savings account at 3.50% APY as of May 8, 2026, while its 9-month CD was at 4.00% APY, which is a better rate if you do not need the money soon.

Best for Overall APY: Vio Bank High-Yield Online Savings

Vio Bank is the cleanest pick here for readers who care most about earning a strong rate without a pile of conditions. It is built like a straightforward online savings account, and that simplicity is part of the appeal.

Features & Details (Vio Bank High-Yield Online Savings)

Vio Bank lists 4.03% APY on its Online Savings Account, with only $100 required to open. The bank also says the account has no monthly fee, interest compounds daily, and deposits are FDIC insured up to standard limits.

There is another practical detail I like here: Vio says new savings accounts can be opened with an initial deposit from $100 up to $250,000. If you are moving a larger cash reserve from a traditional savings account, that makes the switch much easier.

The tradeoff is access. Vio is an online-first bank, so this is best for money you mainly move by transfer, not for a savings account you expect to tap with an ATM card every week.

Pros & Cons (Vio Bank High-Yield Online Savings)

| Pros | Cons |

|---|---|

|

|

Best for Online Banking: Ally Online Savings Account

Ally works best for readers who want their savings account to actually help them save, not just sit there. If you like visual tools, auto-saving features, and a polished app, this is where Ally earns its place.

Features & Details (Ally Online Savings Account)

Ally charges no monthly maintenance fees and requires no minimum opening deposit. Its savings account also includes daily compounding, 24/7 customer service, and the Online & Mobile Security Guarantee.

The real differentiator is the built-in savings system. Each Ally savings account can have up to 10 buckets, and the account includes boosters like recurring transfers, round-ups, and Surprise Savings. That matters if you are working on multiple savings strategies at once, such as an emergency fund, travel money, and holiday spending.

Transfer timing is another thing worth knowing before you open the account. Ally says eligible next-day transfers generally arrive the next business day if you initiate them before 7:30 p.m. Eastern, while standard transfers can take until the third business day.

Pros & Cons (Ally Online Savings Account)

| Pros | Cons |

|---|---|

|

|

Best for Digital Banking Integration: American Express High-Yield Savings

American Express is a smart pick if you want a familiar brand, a simple setup, and one clean login for more of your financial services. It feels especially useful for readers who already use the American Express app and want savings inside the same digital routine.

Features & Details (American Express High-Yield Savings)

American Express says its High Yield Savings account has no fee to open, no minimum deposit, no monthly fees, and daily compounding with interest credited monthly. It also offers 24/7 customer support, which is still not a given in online banking.

The app experience is a real plus here. American Express notes that eligible customers can manage their personal Card and Bank accounts in the same app, which is handy if you do not want another separate banking dashboard to keep track of.

There are two practical rules to know. First, the bank’s High Yield Savings account has a $5 million maximum balance. Second, transfers initiated after 7:00 p.m. Eastern start processing the next business day, so late-night moves may not happen as fast as you expect.

Pros & Cons (American Express High-Yield Savings)

| Pros | Cons |

|---|---|

|

|

Best for ATM Access: Synchrony High-Yield Savings Account

Synchrony stands out because it solves a problem most high-yield savings accounts do not solve very well: getting to your money without waiting on a transfer. If you want a HYSA that still feels usable in a pinch, this one deserves a close look.

Features & Details (Synchrony High-Yield Savings Account)

Synchrony says its High Yield Savings account comes with no minimum deposit, no minimum balance, and no monthly fees. The bank also confirms that you can request an optional ATM card, which is rare for this category.

That ATM feature is more useful than it first sounds. Synchrony states that it does not charge a fee to use an ATM, and it will refund up to $5 in domestic ATM fees per statement cycle charged by other financial institutions. It also allows mobile check deposit, with a current $2,000 daily mobile deposit limit per account.

There is still a tradeoff. Synchrony’s account agreement limits certain transfers or withdrawals from the HYSA to six per statement cycle, and checks are not available with the High Yield Savings account.

Pros & Cons (Synchrony High-Yield Savings Account)

| Pros | Cons |

|---|---|

|

|

Best for Low Fees: Marcus by Goldman Sachs Online Savings

Marcus by Goldman Sachs is one of the easiest accounts here to say yes to if you hate friction. It keeps the fee structure simple, the minimums at zero, and the transfer experience surprisingly friendly for an online savings account.

Features & Details (Marcus by Goldman Sachs Online Savings)

Marcus lists its Online Savings Account at 3.50% APY as of May 8, 2026, with no fees and no minimum deposit. The account also includes daily compounding, FDIC insurance, and 24/7 customer support.

What makes Marcus especially good for low-fee savers is how it handles money movement. Marcus says it charges no ACH transfer fees, no wire transfer fees, and no minimum balance for the Online Savings Account.

There is also a small timing advantage here. Marcus says if you schedule a transfer into your Marcus account before 6:00 p.m. Eastern, you begin earning interest on the day you initiate the transfer, even before the money arrives.

Pros & Cons (Marcus by Goldman Sachs Online Savings)

| Pros | Cons |

|---|---|

|

|

Final Words

The best high-yield savings accounts in 2026 do more than flash a big number. The right one fits how you save, how often you move money, and whether you care more about APY, app quality, or easy cash access.

If you want the strongest easy-to-earn APY from this list, Vio Bank is a strong place to start. If you care more about online banking tools, Ally stands out. If ATM access matters, Synchrony is the practical choice.

Check the APY, read the fee rules, confirm FDIC or NCUA coverage, and move your money with purpose. A better savings account can make your cash work much harder without adding more risk.

Frequently Asked Questions (FAQs) About High-Yield Savings Accounts

1. What is a high-yield savings account, and how does apy (annual percentage yield) matter?

A high-yield savings account pays a higher apy than a regular savings account, so your money grows faster. Watch the APY, it tells you how much interest you earn each year, and keep an eye on the federal reserve for rate moves.

2. Which banks and apps offer the best high-yield savings accounts in 2026?

Look at offerings from bread savings, bask bank, greenfi, and morgan stanley private bank, plus online options like e*trade premium savings (brokerage savings), everbank performance savings (online bank), and cit bank platinum savings (platinum savings), each has different perks. Compare APY, fees, and access, and pick the one that fits your cash needs.

3. Are certificates of deposit (cds) better than high-yield savings accounts for extra interest?

Sometimes, yes, CDs can pay more, but they lock your money for a set term, so shop around before you commit.

4. Is my money safe in a high-yield account?

Most banks are backed by fdic (federal deposit insurance corporation), and credit unions are backed by ncua (national credit union administration), so deposits are insured up to limits. If you want fossil-fuel-free banking, greenfi and similar providers focus on that, so check their policies.

5. What can I use a high-yield savings account for, beyond simple saving?

You can build an emergency fund, save for a home down payment, pay down student loans, or stash cash for travel, wellness, food, or big bills like life insurance and car insurance. Use it as a safe place for money you might need soon, or as a buffer before taking business loans or making big purchases.

6. Where can I find trusted picks and coverage on the best accounts?

Read reviews on wsj, barron’s, marketwatch, fortune, and ibd, and look at reports from curinos; writers like kate ashford, tony armstrong, and margarette burnette often cover rates and trends, so follow their work when you shop.