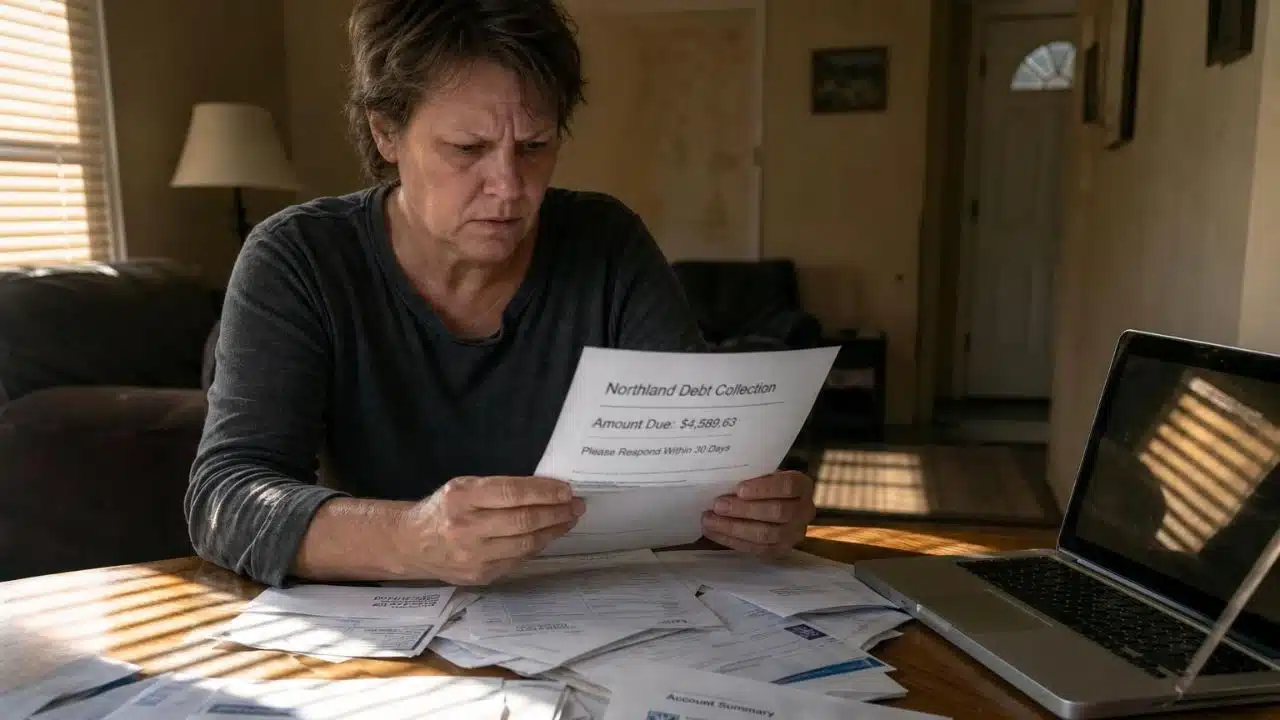

Seeing CSCRCT03 PO Box 1280 on an envelope can throw your whole day off. Most readers want the same plain answers: who sent it, what it means, and whether they really owe the debt listed on the notice.

We checked current company details and consumer protection rules so we could turn that stress into a simple plan. The short version is this: do not panic, do not ignore the letter, and do not pay until the account details make sense.

We will walk through what CSCRCT03 usually means, how to contact credit control, and how to dispute or verify a debt if anything looks wrong.

CSCRCT03 Credit Control Service Overview

If your letter lists cscrct03 PO Box 1280 or PO Box 1280 Oaks, PA 19456-1280, it is usually tied to Credit Control, LLC, a debt collector that works accounts for banks, lenders, and other businesses. The confusing part is that the letter may use the Oaks, PA post office box for mail even though the company’s main consumer contact pages list its office in Missouri.

That split matters because a post office box on a collection notice is often a mail-processing address, not the company’s headquarters. So if you see po box 1280 credit control on the letter, treat it as the address to use for that account unless the notice tells you otherwise.

In Credit Control’s 2026 company materials, the business says it has operated since 1989, has more than 500 employees nationwide, and is licensed in all 50 states, Puerto Rico, and Guam. That helps answer the “is this a real company?” question, but it still does not prove that the debt owed is accurate.

A proper notice should also help you identify the account fast. Look for the current creditor, any account number ending in a few digits, the current balance, and a clear deadline for a dispute.

| What to look for on the letter | Why it matters |

|---|---|

| Current creditor and original creditor | This tells you who says you owe the balance and whether the account was transferred. |

| Account number ending in a few digits | You can match it against old statements, emails, or bank records without sharing extra personal details. |

| Interest, fees, payments, or credits | These line items show whether the balance changed from the original debt amount. |

| 30-day dispute date | This date tells you how long you have to force the collector to pause collection while it verifies the debt. |

What is the purpose and function of CSCRCT03 Credit Control?

Credit Control acts as a third-party collection agency. In plain English, that means a creditor can hire it to collect a past-due account or place an account with it for recovery.

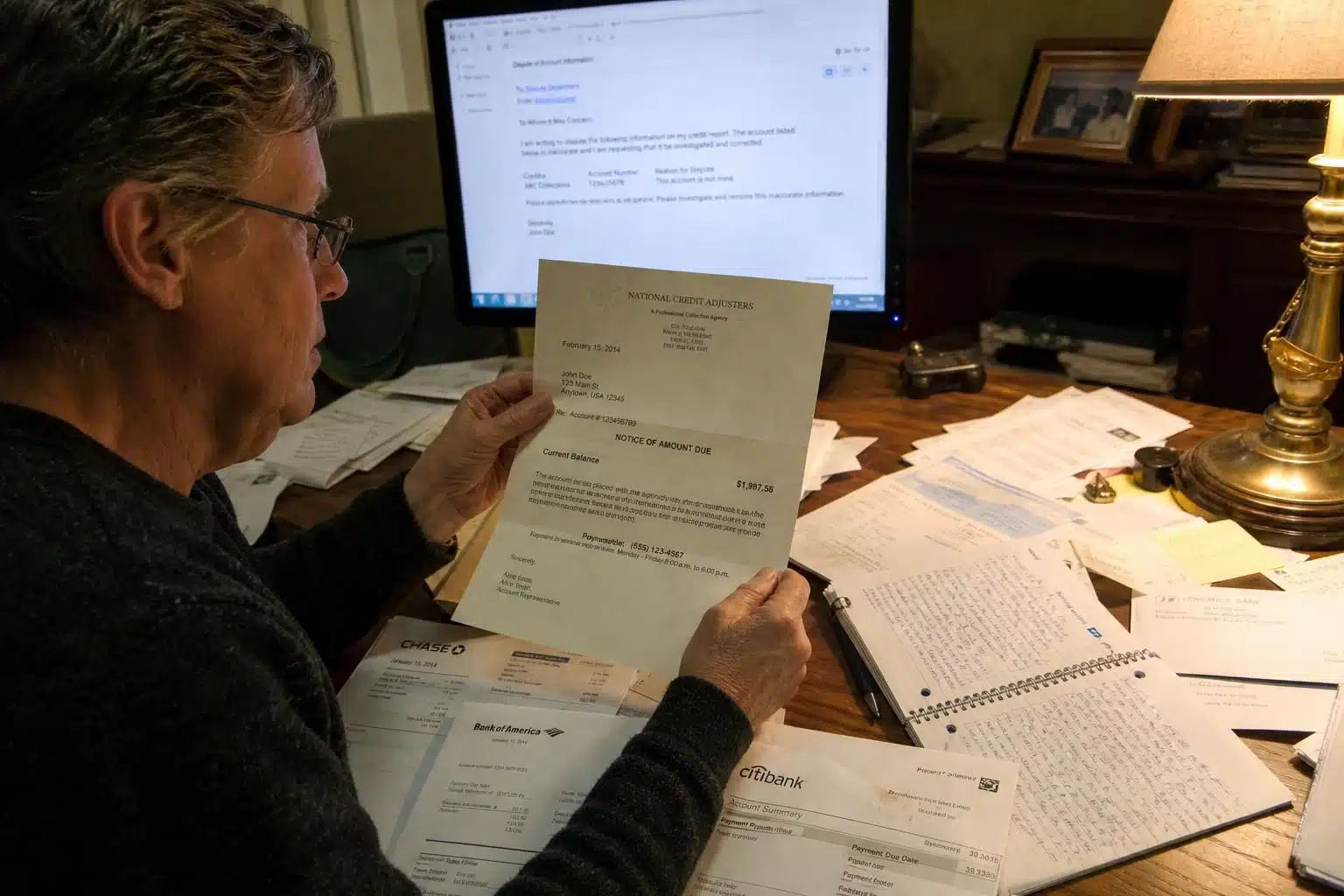

If your notice says they are trying to collect a debt owed to Bank of America or another lender, start by comparing the letter to your own records. Match the creditor name, the last digits of the account, and any payment or credit entries, including small line items such as a 99.00 credit or payment that could change the balance.

The company’s FAQ says the account number or reference number on its letter is the key detail you need for questions or login issues. That is useful because many online posts about PO Box 1280, Oaks, PA, point to different businesses, and the safest way to identify the right company is to match the full company name, creditor, and reference number shown on your own notice.

If the letter gives you a dispute deadline, work from the printed date on that notice. Waiting too long can shrink your leverage, even if you still plan to challenge the debt later.

How can I contact CSCRCT03 Credit Control and what are their hours?

The company’s consumer pages list a toll-free phone number, TTY support, a mailing address in Missouri, and an online message form for account questions. Your letter may still direct you to PO Box 1280, Oaks PA 19456-1280, and for a document like a dispute letter, we would use the exact address printed on the notice in front of us.

Some CSCRCT03 letters also tell you to call the phone for more information about credit questions or to scan them with your smartphone for more information. Those tools are fine for quick confirmation, but a written dispute is still the better move when the balance, dates, or creditor looks off.

| Contact method | Best use | Smart move |

|---|---|---|

| PO Box 1280, Oaks, PA | Written dispute or request for verification | Best for building a paper trail. |

| Toll-free phone line | Fast questions about your account number or mailing status | Take notes, but do not rely on a phone call alone for a dispute. |

| Online message form | Basic account questions | Save a screenshot of what you send. |

The CFPB’s debt collection rule says a validation notice must include the mailing address where the collector accepts disputes and requests for information about the original creditor. That is why the Oaks, PA, post office box can still be the right place to mail your letter even if the company’s main office is somewhere else.

Certified mail with return receipt is worth the small extra cost. It gives you a mailing date, delivery proof, and a cleaner timeline if you later need to show when your letter arrived.

What rights do consumers have under the Fair Debt Collection Practices Act (FDCPA)?

If Credit Control or any other debt collector contacts us, the FDCPA gives us a set of guardrails. Those rules do not erase a real debt, but they do control how the collector can communicate and what information on debt collection rights it must provide.

The first big protection is the validation notice. It should tell you the amount of the debt; the creditor; the account number ending on the account, if there is one; and how to dispute the balance or ask for information about the original creditor.

The CFPB says collectors generally cannot call before 8 a.m. or after 9 p.m., and the current rule also creates a presumption of a violation if they place more than seven calls about the same debt within seven days or call again within seven days after a phone conversation about that debt. If your call log shows that pattern, keep the dates and times.

- They cannot harass, threaten, or use abusive language.

- They cannot lie about who they are or how much you owe.

- They must provide validation information in the first communication or within five days.

- They must pause collection on the amount you dispute if you send a written dispute within 30 days.

- They must follow your written request to stop contacting you, with limited exceptions.

Another useful right is control over contact. If calls at work or late at night are a problem, you can tell the collector in writing not to contact you in those places or at those times.

If you want contact to stop completely, you can also send a written letter saying so. That does not make the debt disappear, but it can force future communication into a narrower lane and give you more breathing room.

A collection letter can ask for payment and still be legal. What it cannot do is pressure you in a way that hides your right to dispute the debt or ask for proof.

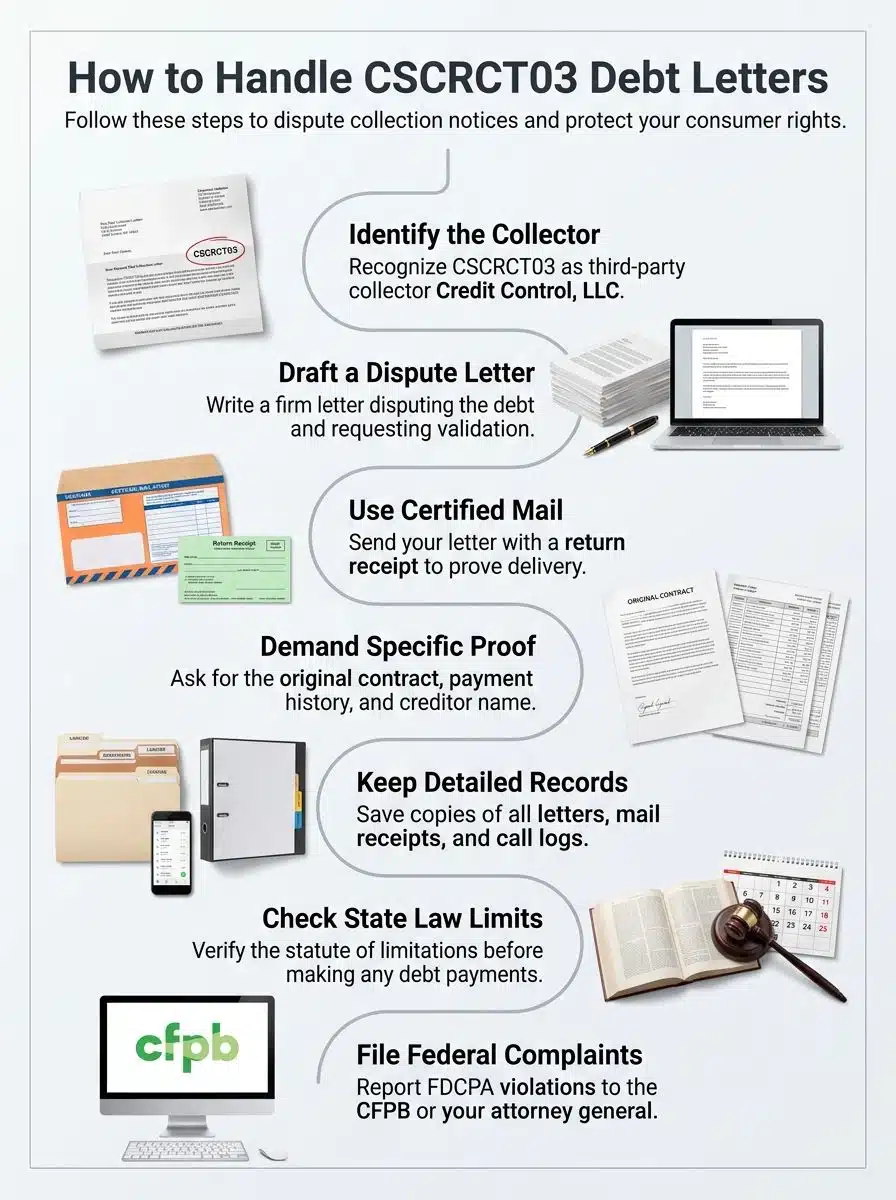

How can I dispute or verify a debt?

If you do not recognize the account, think the amount is wrong, or believe you already paid it, ask for verification in writing. This is the safest response to a CSCRCT03 notice because it slows the situation down and gives you a record.

Before you write, read the letter closely. A modern validation notice should show the creditor name, the current amount owed, itemized changes such as interest or fees and payments or credits, and the end date for the 30-day dispute window.

What steps should I take to request debt validation?

Keep the request short and firm. You do not need to tell your whole life story, and you do not need to admit the debt is yours.

The most effective letter simply identifies you, identifies the account, states the amount you dispute, and asks the collector to verify the debt. If your notice lists CSCRCT03, PO Box 1280, Oaks PA 19456-1280, use that exact address for your mailing unless the letter tells you to write somewhere else.

- Write your full name, mailing address, and the account or reference number from the letter.

- State clearly that you dispute the debt, or dispute only part of it if the amount looks wrong.

- Ask for the name and address of the original creditor if it is different from the current creditor.

- Ask for an itemization that explains the original debt amount, interest, fees, payments, and credits.

- Mail the letter by certified mail and keep copies of the letter, envelope, and receipt.

- Log every later call, voicemail, email, or letter so your timeline stays clean.

The CFPB says that if you send a written dispute or request for original-creditor information within 30 days, the collector must pause collection on the amount you dispute until it responds. That is why mailing the letter quickly matters so much.

| Ask for this | Why it helps |

|---|---|

| Name of the original creditor | Useful if the current creditor is unfamiliar or the debt changed hands. |

| Itemization of the balance | Shows whether fees, interest, or credits changed the number you see today. |

| Account number or reference number | Lets you match the debt to your own records. |

| Proof of the claimed balance | Helps you challenge a notice that only repeats a number without support. |

If the debt turns out to be valid and you want to resolve it, ask about payment options only after you understand the numbers. Credit Control’s FAQ says it does not charge a fee for payments made on its site or by phone, but it also notes that some clients do not allow credit card payments, so a rejected card does not automatically mean the account is fake.

How do I dispute inaccuracies on my debt record?

If the same debt appears on your credit reports and the details are wrong, send disputes to both the collector and the credit reporting companies. That gives you two paths to fix the same problem.

Be specific about the error. State whether the balance is wrong, the account does not belong to you, the dates are off, or the creditor name is incorrect.

- Attach copies of anything that proves your position, such as statements, payoff letters, bank records, or identity theft documents.

- Point to the exact line that is wrong instead of writing a general complaint.

- Ask for correction or deletion of the inaccurate information.

- Keep a complete file with every letter, receipt, and screenshot.

The CFPB says credit reporting companies generally must investigate a credit report dispute within 30 days, may extend to 45 days in some cases, and must notify you of the results within five business days after the investigation ends. That timeline is why it helps to send your strongest documents the first time.

If you think the account is fraud or identity theft, move fast. Credit Control’s FAQ says it may ask for an Identity Theft Report, a police or incident report, or a notarized affidavit of fraud or identity theft so it can review the claim.

If a reply only repeats the balance and skips the proof, write back and say the debt is still disputed. A weak response is not the same as a clear explanation.

If the collector does not verify the debt, keeps reporting wrong information, or contacts you in a way that breaks the law, file a complaint with the Consumer Financial Protection Bureau and your state attorney general. As of April 2026, the CFPB says most companies respond to complaints within 15 days, and some cases take up to 60 days for a final response.

Final Words

If you got a CSCRCT03 PO Box 1280 letter, start with the basics.

Match the creditor, the account number ending on the notice, and the balance before you pay anything. If the letter looks wrong, dispute the debt in writing and keep copies.

If the information checks out and you do owe it, you can then decide whether to ask about payment options. If it does not check out, make the collector prove it.

That one step, done within 30 days, often gives you the clearest path forward. It can also help protect your credit and your rights.

Frequently Asked Question (FAQs) on CSCRCT03

1. Who is CSCRCT03 Credit Control at PO Box 1280 Oaks PA 19456-1280?

They are a collections group tied to an LLC Oaks firm; they send mail to PO Box 1280, Oaks, PA. Check credit-control.com. What else do you find on their site for phone and account notes?

2. Why did I get a notice?

They may be trying to collect a debt, even if you do not think you owe it. Read the note, check dates, and keep your records.

3. How do I dispute the debt?

To dispute the debt? Send a short, written letter that says you dispute it within the time the law allows. Keep copies, mail by certified mail, and do not sign anything you do not understand.

4. Why does the paper list sunglasses and polarization (waves)?

They may list items linked to the charge, like eyewear, sunglasses, or a note about polarization (waves) on a receipt. Ask them for an itemized bill, and ask for proof if the item looks wrong.