Businesses rarely change payment methods because something sounds futuristic. They change when the current system wastes time, blocks customers, delays settlement, or gives the finance team another reason to hate Monday morning.

That is the real reason more companies are looking at accepting USDT payments. Not because every business suddenly wants to become a crypto company. Most do not. They are looking at USDT because international payments still create too much friction for too many businesses.

A client wants to pay from another country. A contractor wants faster settlement. A digital seller wants fewer chargeback headaches. A customer already holds stablecoins and does not want to move through three extra steps just to complete a simple payment.

That is where USDT starts to look less like a crypto headline and more like a payment operations tool.

It is not perfect. Far from it.

USDT brings regulatory questions, accounting work, wallet risk, refund complications, network confusion, and stablecoin transparency concerns. A business that adds it without a plan is not modern. It is just creating a new mess with better branding.

The useful question is more practical: where does USDT actually reduce payment friction, and where does it quietly create more work than it solves?

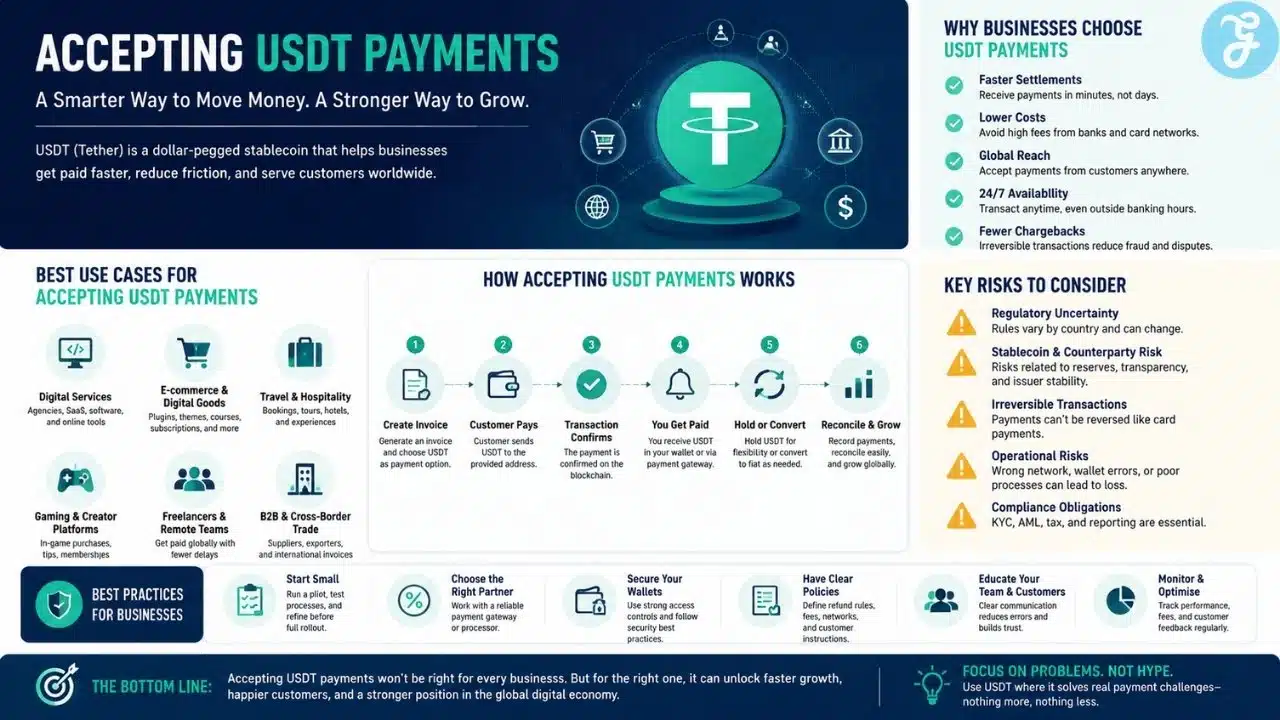

Why Accepting USDT Payments Is Becoming A Business Conversation

USDT is built to track the value of the U.S. dollar. That one detail explains much of its appeal.

A business can tolerate many things in payments. Random price swings are not one of them. If a company invoices someone for $2,000, it does not want to receive an asset that behaves like a roller coaster before the payment is even recorded. Stablecoins became useful because they made crypto payments easier to understand in normal business terms.

That does not make USDT the same as money sitting safely in a bank account. It is still a digital asset. It still depends on infrastructure, issuers, exchanges, wallets, processors, and regulation. But compared with volatile crypto assets, it is easier for businesses to price, invoice, and explain.

The demand usually appears in businesses that already deal with payment friction. A local service provider with smooth domestic card payments may not care. A software seller with buyers in several countries might. A freelancer platform, digital agency, gaming-related business, online service provider, exporter, or travel company may see the use case faster because their payment problems are already cross-border.

The appeal is not ideological. Most serious businesses do not have time for ideology when invoices are late.

The appeal is optionality.

The Real Use Case Is Not Always Checkout

People often talk about USDT as if it only belongs on a checkout page. That is too narrow.

Some businesses may accept USDT from customers. Others may use it to pay contractors. Some may use it for vendor settlement, international invoices, or moving dollar-linked value outside standard banking hours. A few may hold it briefly as working liquidity. Many should probably convert it quickly instead of treating it like a treasury strategy.

This is where businesses need to stop copying each other.

A payment method should match the business model. If customers are not asking for USDT, if finance cannot reconcile it cleanly, if legal has not checked the rules, and if support cannot explain what happens when a payment goes wrong, then adding it is not progress.

It is decoration.

USDT makes the most sense when three things meet:

- A real cross-border payment problem

- Customers, clients, vendors, or contractors who already understand stablecoins

- Internal systems that can handle records, refunds, wallets, and compliance

Without those, the benefit gets thin quickly.

The Setup Looks Simple Until Money Gets Stuck

On paper, accepting USDT is not complicated.

A business can use a direct wallet. The customer sends USDT to an address, the transaction confirms on-chain, and the business records the payment. Simple enough.

Except it is only simple when everything goes right.

Someone must manage the wallet. Someone must protect private keys. Someone must confirm the network. Someone must match the payment to an invoice. Someone must decide what happens if the customer sends the wrong amount. Someone must explain why a transaction cannot be reversed like a card payment.

That is why many businesses start with a crypto payment gateway rather than direct wallet acceptance. Providers such as NOWPayments and CoinGate offer merchant tools for crypto payment flows, invoices, confirmations, and settlement-related features depending on the market and setup.

A gateway does not remove every problem. It just moves some of the operational burden into a system built for payments.

The dangerous detail is network selection.

USDT can exist on several blockchain networks. If a customer sends USDT through the wrong network or to an unsupported address, the business may not be able to recover it easily. This is one of those boring operational details that sounds minor until it becomes a real support ticket with real money attached.

A proper payment flow should make the network painfully clear. Not slightly clear. Not hidden in small text. Clear enough that a tired customer paying at midnight does not make an expensive mistake.

What USDT Can Solve And What It Cannot

The decision becomes clearer when the payment problem is matched against the operational reality.

| Payment Problem | Where USDT Can Help | What Still Needs Control |

|---|---|---|

| Slow international settlement | Faster wallet-to-wallet movement | Legal checks, records, and reporting |

| Chargeback risk | Confirmed transactions are usually final | Clear refund policy and support process |

| Crypto-native customers | Familiar payment option for buyers who already hold USDT | Checkout clarity and network instructions |

| Contractor payments | Faster settlement in some cross-border cases | Tax records, wallet security, and approvals |

| Currency friction | Dollar-linked payment value | Stablecoin, exchange, and issuer risk |

| Limited payment access | Adds another rail where cards or banks are weak | Compliance and counterparty screening |

This is where the hype needs to calm down.

USDT can make some payment flows faster. It does not fix bad bookkeeping. It does not replace compliance. It does not remove customer support. It does not make a weak finance process suddenly organized.

If the business already struggles to match invoices with bank deposits, crypto payments may expose that weakness faster. If refunds are messy today, USDT will not magically make them elegant. If the company has no one responsible for payment operations, adding another rail will probably create more confusion.

Fast payments are useful.

Fast chaos is still chaos.

Where USDT Makes The Most Practical Sense

The strongest USDT use cases usually appear in businesses where borders matter.

A digital agency working with overseas clients may want to offer USDT as an additional payment option. Not for every client. Not as a replacement for bank transfers. Just as another route when the client already uses stablecoins and settlement delays are annoying.

Freelancers and remote teams may see similar value. Small international payments can get eaten by fees, delays, and platform restrictions. USDT can be useful when both sides understand the process and the paperwork is handled properly.

Digital goods sellers may also see the appeal. Software access, templates, plugins, subscriptions, online courses, and other instant-delivery products can be exposed to chargeback risk. USDT’s finality may help in some cases. It can also create support pressure when a customer sends the wrong amount or pays through the wrong network.

Travel and global booking platforms are another natural fit because customers come from different countries and payment preferences vary. A global audience makes alternative rails more relevant. Still, travel companies need reliable refund handling. Travel is not exactly known for having zero cancellations.

Gaming, creator platforms, and online communities may also find USDT easier to explain because some users already understand wallets and stablecoins. That does not remove the need for fraud controls, platform rules, age-related restrictions where relevant, and local compliance.

B2B trade is the serious end of the conversation. Exporters, suppliers, and international service businesses may look at USDT because banking rails are slow or inconsistent in some corridors. But higher payment value means higher responsibility. Counterparty checks, documentation, sanctions screening, and legal review matter more here, not less.

Accepting a fast payment from the wrong party is not operational efficiency.

It is a problem wearing a speed badge.

The Benefits Are Real, But Not Universal

USDT can help businesses that already have a payment problem.

It may reduce settlement delays. It may serve customers who already prefer stablecoins. It may lower chargeback exposure in selected business models. It may make contractor or vendor payments easier in some cross-border situations. It may offer payment access outside banking hours.

That is enough to make it worth studying.

But not enough to make it universally useful.

A business with domestic customers, reliable card approval, clean bank settlement, and no crypto demand may gain very little from accepting USDT payments. In that case, the company may be adding a new payment method mostly to look current.

That is a weak reason.

Payment methods should earn their place. If they do not reduce friction, increase successful payments, serve a real customer segment, or improve settlement, they are just another system to maintain.

The Risk Conversation Cannot Be Pushed To The Bottom

USDT is widely used, but wide usage is not the same as zero risk.

Tether says USDT is pegged 1:1 and backed by reserves, and it publishes transparency information. At the same time, USDT has faced scrutiny around reserves, transparency, regulatory treatment, and risk assessment.

A business does not need to turn that into panic. It does need to treat it as part of the decision.

The risk list is not small:

- Regulation can vary by country and region.

- Exchanges or processors may restrict certain services.

- Wallet security mistakes can be expensive.

- Wrong-network payments can be hard to recover.

- Transactions are usually irreversible.

- Accounting and tax treatment may require specialist help.

- Counterparty screening still matters.

- Stablecoin reserve concerns should not be ignored.

- Liquidity can become more important during market stress.

Europe is a useful warning sign here. MiCA has changed the regulatory environment for crypto assets and stablecoins in the European Economic Area, and some platforms have adjusted stablecoin availability because of those rules.

That does not mean USDT is unusable everywhere. It means businesses must stop assuming that a payment method available in one market is automatically practical in another.

Local rules matter. Provider rules matter. Business type matters.

The Rollout Should Start With An Audit, Not A Logo On Checkout

The worst way to adopt USDT is to add it because competitors are doing it.

Start with the payment workflow. Where are customers failing to pay? Which countries create settlement delays? How often do chargebacks happen? Do customers ask for stablecoin payments? Are contractors requesting USDT? Can finance reconcile digital asset payments without turning month-end into a crime scene?

If there is no real problem, stop there.

If there is a real problem, test carefully.

Do not launch it across every product and every market on day one. Start with one customer segment, one invoice type, or one controlled payment flow. Use a gateway unless the company already has proper crypto operations experience. Decide whether USDT will be held or converted. Set wallet controls. Write refund rules before the first customer pays. Train support and finance teams.

Then measure what happens.

Look at payment success rate, settlement time, support tickets, refund issues, reconciliation workload, customer confusion, and conversion problems. A payment method that looks impressive but creates more work may not be worth keeping.

This is the part too many businesses skip because the technology feels simple.

The operational layer is where the truth shows up.

USDT Belongs In The Payment Stack, Not On A Pedestal

USDT should not be treated as a replacement for every traditional payment method.

Cards are still better for many consumer transactions. Bank transfers are still necessary for many regulated business payments. Local wallets often win in domestic markets. Stablecoins are strongest where cross-border movement, dollar-linked value, and user familiarity overlap.

That is the practical view.

A good payment stack does not worship one rail. It uses the right rail for the right customer and the right risk level.

USDT can sit inside that stack as an additional option. It can help certain businesses move money faster, serve specific customers, and reduce friction in selected payment flows.

But if it is added without legal review, finance planning, support training, and operational controls, it can become another shiny tool that makes the back office miserable.

The Smarter Way To Think About Accepting USDT Payments

Before accepting USDT payments, a business should ask a blunt question: what exact payment problem is this solving?

If the answer is vague, wait.

If the answer is specific, test it with discipline. Use a reliable processor. Keep the rollout limited. Make network instructions clear. Avoid holding large balances without a treasury policy. Bring legal, tax, accounting, and finance into the setup early. Write refund rules before there is a refund dispute.

USDT adoption should not be about looking innovative. That is how businesses buy complexity and call it strategy.

The better case is practical.

For the right company, USDT can reduce cross-border friction, serve crypto-native customers, and make payment operations more flexible. For the wrong company, it can create accounting confusion, compliance pressure, and support problems that outweigh the benefit.

The technology is not the deciding factor.

Judgment is.