The United States is currently navigating a pivotal moment in healthcare history as the second quarter of 2026 begins. For decades, the rising price of medication has outpaced inflation, creating a systemic barrier to health that affects millions. However, the Prescription Drug Cost Crisis 2026 is being met with unprecedented regulatory and private-sector responses. From the first-ever Medicare price negotiations going live to the launch of federal discount portals, the tools available to patients have expanded significantly.

Yet, the burden remains heavy: recent data suggests that nearly 60% of adults still worry about their ability to afford essential treatments, forcing a new era of “medical consumerism” where patients must hunt for the best deal just to survive.

How We Selected Our 15 Best Prescription Drug Cost Crisis 2026 Facts

To assemble this guide, we analyzed the latest 2026 Medicare and You handbook, recent KFF health tracking polls from March 2026, and the implementation reports from the Centers for Medicare and Medicaid Services (CMS). Our selection criteria prioritized the “Day One” impacts of the Inflation Reduction Act’s 2026 provisions, such as the new out-of-pocket caps and negotiated drug prices. We also examined the role of market disruptors like direct-to-consumer pharmacy models and the new federal “TrumpRx” initiatives. These 15 points were chosen to offer a comprehensive view of the technical, legislative, and behavioral shifts defining how Americans manage their health expenses this year.

15 Essential Truths About the Prescription Drug Cost Crisis 2026

The following insights detail the new protections, the lingering hurdles, and the strategic workarounds Americans are using to lower their pharmacy bills today.

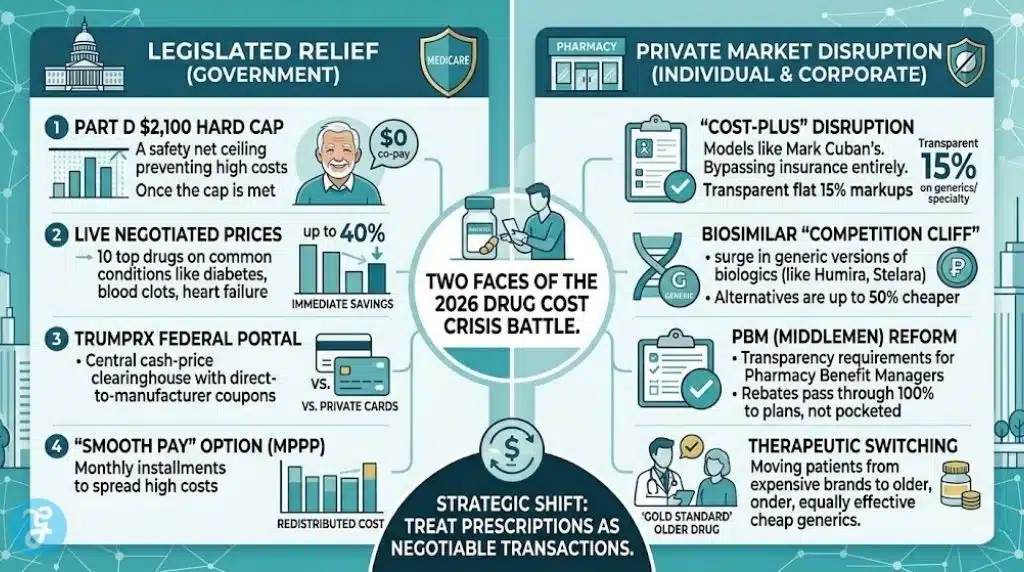

1. The $2,100 Medicare Out-of-Pocket Cap

Starting January 1, 2026, a hard cap on out-of-pocket costs for Medicare Part D beneficiaries has moved to $2,100. Once a patient hits this limit, their co-payments for covered drugs drop to zero for the remainder of the year. This is a critical safety net for those with chronic conditions like cancer or rheumatoid arthritis.

Best for: seniors and disabled individuals on Medicare with high-cost specialty medications.

Why We Chose It:

-

It provides an absolute financial ceiling that prevents medical bankruptcy for retirees.

-

It simplifies the “donut hole” confusion that plagued previous decades.

Things to consider:

-

This cap does not include monthly plan premiums or drugs not covered by your specific formulary.

2. Live Negotiated Prices for Top Drugs

As of today, April 2, 2026, the first set of 10 drugs negotiated directly by Medicare are available at their “Maximum Fair Prices.” These include common treatments for diabetes (Jardiance, Januvia), blood clots (Eliquis, Xarelto), and heart failure (Entresto). Beneficiaries are seeing immediate savings of up to 40% on these specific brands.

Best for: patients treating diabetes, heart disease, or autoimmune disorders.

Why We Chose It:

-

It marks the first time in history the U.S. government has used its bulk-buying power to lower costs.

-

It sets the precedent for an additional 15 drugs being added to the list later this year.

Things to consider:

-

Savings vary depending on your specific secondary insurance or Advantage plan.

3. The Launch of “TrumpRx”

Launched in early 2026, the federal TrumpRx website acts as a centralized clearinghouse for negotiated cash-price deals. The administration has sought “most favored nation” deals directly with manufacturers to offer discounted coupons for those without insurance or those whose plans don’t cover specific specialty drugs.

Best for: uninsured individuals or those in “coverage gaps” for high-cost medications.

Why We Chose It:

-

It represents a new federal attempt to use market competition to drive down cash prices.

-

it offers an alternative to private discount cards which sometimes harvest user data.

Things to consider:

-

Not all drugs are available on the portal; it focuses primarily on high-volume maintenance meds.

4. The “Smooth Pay” (MPPP) Option

The Medicare Prescription Payment Plan (MPPP) is now fully operational in 2026. This allows beneficiaries to spread their out-of-pocket costs across the entire year in monthly installments rather than paying a massive lump sum at the pharmacy counter in January.

Best for: patients who hit their deductible early in the year and struggle with cash flow.

Why We Chose It:

-

It fixes the “timing” problem of drug costs, making them as predictable as a utility bill.

-

It is a voluntary program that can be joined at any time during the year.

Things to consider:

-

You are still paying the same total amount (up to the $2,100 cap); it is simply re-distributed.

5. 40% “Medical Nonadherence” Rate

A sobering fact of 2026 is that roughly 43% of Americans report they have not taken medication as prescribed due to cost. This includes skipping doses, cutting pills in half, or leaving prescriptions unfilled at the pharmacy.

Best for: healthcare providers and policymakers tracking public health outcomes.

Why We Chose It:

-

It highlights the human cost of the crisis beyond simple dollar amounts.

-

It shows that high prices lead directly to worse long-term health and higher ER visits.

Things to consider:

-

Lower-income and uninsured adults are twice as likely to report these dangerous workarounds.

6. The Biosimilar “Competition Cliff”

In 2026, the market has seen a surge in “biosimilars”—lower-cost versions of expensive biologic drugs like Humira and Stelara. With Stelara exiting the Medicare negotiation program this year due to new competition, patients are finding that these alternatives are up to 50% cheaper than the original brand.

Best for: patients with Crohn’s disease, psoriasis, or rheumatoid arthritis.

Why We Chose It:

-

Competition is often more effective at lowering prices than legislation alone.

-

It provides a generic-like experience for the most expensive “specialty” tier drugs.

Things to consider:

-

You may need a new prescription from your doctor to switch to a biosimilar equivalent.

7. Inflation-Based Rebate Penalties

The federal government is now actively collecting rebates from drug companies that raise their prices faster than the rate of inflation. In 2026, these funds are being used to lower the premiums for Medicare beneficiaries and fund further price-containment initiatives.

Best for: all taxpayers concerned about runaway price gouging.

Why We Chose It:

-

It acts as a powerful deterrent against the “traditional” twice-a-year price hikes.

-

It aligns drug pricing with the broader economic reality of the American consumer.

Things to consider:

-

This rule applies to over 600 drugs that have seen excessive price increases since 2023.

8. The GLP-1 Weight-Loss Coverage Crisis

As of April 2026, many employers have begun dropping coverage for “blockbuster” weight-loss drugs like Wegovy and Zepbound due to high costs. This has created a massive direct-to-consumer market where patients are paying out-of-pocket for compound versions or seeking telehealth alternatives.

Best for: individuals managing obesity or metabolic health.

Why We Chose It:

-

It is the most volatile sector of the pharmaceutical market in 2026.

-

It illustrates the tension between medical innovation and corporate affordability.

Things to consider:

-

Always verify the source of “compounded” GLP-1s to ensure safety and purity.

9. PBM (Pharmacy Benefit Manager) Reform

Congress is currently debating a major overhaul of the “middlemen” in the drug supply chain. In 2026, new transparency requirements mean that PBMs must pass through 100% of the rebates they get from manufacturers directly to the plan sponsors or patients, rather than pocketing them.

Best for: employers and small business owners trying to lower their employee health costs.

Why We Chose It:

-

It targets the hidden “kickbacks” that have historically kept list prices artificially high.

-

It represents a rare area of bipartisan agreement in the 2026 political landscape.

Things to consider:

-

These changes may lead to a restructuring of how pharmacies are reimbursed for their work.

10. The Rise of “Cost-Plus” Pharmacies

Models like Mark Cuban’s Cost Plus Drugs have expanded their 2026 catalogs to include hundreds of specialty and generic medications with a flat 15% markup. Many Americans are now bypassing their insurance entirely, as the cash price at these pharmacies is often lower than their insurance co-pay.

Best for: patients on generic maintenance meds for high blood pressure, cholesterol, or mental health.

Why We Chose It:

-

It has permanently disrupted the traditional “black box” pricing of retail pharmacies.

-

It empowers patients to shop like consumers for the first time.

Things to consider:

-

These pharmacies typically do not accept insurance, so the cost won’t count toward your deductible.

11. Importation from Canada and Mexico

Despite legal hurdles, the “Personal Importation” of drugs remains a primary coping mechanism in 2026. Florida’s state-wide importation program, which began in 2024, has expanded this year to include a wider range of medications for chronic conditions, sourced from licensed Canadian wholesalers.

Best for: residents in states with active importation programs.

Why We Chose It:

-

It highlights the global disparity in drug pricing for the same brand-name products.

-

It provides a “pressure relief valve” for the U.S. market.

Things to consider:

-

Only use programs sanctioned by state or federal authorities to avoid counterfeit risks.

12. The “Therapeutic Switching” Trend

With high costs persisting, 2026 has seen a surge in “therapeutic switching”—where doctors move patients from an expensive brand-name drug to a different, older, but equally effective class of medication that is available as a cheap generic.

Best for: budget-conscious patients who are comfortable with “gold standard” older treatments.

Why We Chose It:

-

It is the most effective way for a patient to lower their bill by 90% or more.

-

It avoids the “newest is best” marketing trap often set by pharmaceutical companies.

Things to consider:

-

Discuss the potential side-effect differences with your physician before switching.

13. Patient Assistance Program (PAP) Scrutiny

Many drug manufacturers offer “Patient Assistance Programs” to provide free drugs to low-income earners. However, in 2026, these are under fire for “accumulator” rules, where insurance companies refuse to count these manufacturer-funded dollars toward the patient’s deductible.

Best for: lower-income households and the uninsured.

Why We Chose It:

-

It is a vital but complex resource that often feels like a “cat and mouse” game with insurers.

-

Understanding these rules can mean the difference between getting a drug for $0 or $1,000.

Things to consider:

-

Check if your state has passed “Accumulator Ban” legislation to protect these funds.

14. Discount Card “Data Harvesting” Awareness

In 2026, consumer advocacy groups are warning about the privacy trade-offs of using common discount cards. While they save you money at the counter, they often sell your prescription history to data brokers.

Best for: privacy-conscious patients.

Why We Chose It:

-

It identifies the “hidden cost” of “free” discount services.

-

It encourages the use of more secure federal portals like TrumpRx.

Things to consider:

-

Read the fine print of any discount app before entering your personal health data.

15. The Shift to “White Label” Generics

Hospitals and large health systems in 2026 are increasingly buying “white label” generics—medications produced directly for the hospital system to avoid the traditional supply chain markups. This is significantly lowering the cost of drugs administered during hospital stays.

Best for: patients undergoing surgery or inpatient treatment.

Why We Chose It:

-

It shows that the “crisis” is being fought at the institutional level as well as the individual level.

-

It helps reduce the “room and board” cost of hospital care.

Things to consider:

-

Ask your hospital if they use a direct-sourcing model for their pharmacy.

Strategic Summary of the Prescription Drug Market 2026

The current state of medication affordability is one of “Legislated Relief vs. Economic Pressure.” While the Inflation Reduction Act and new federal portals have created strong safety nets—particularly for seniors with the $2,100 cap—the private sector for working-age adults remains volatile. The Prescription Drug Cost Crisis 2026 has essentially split the American public into two groups: those protected by new federal caps and those forced to navigate a wild-west market of discount cards, cost-plus pharmacies, and therapeutic switching.

The key to financial health in this environment is a shift in mindset—treating every prescription as a negotiable transaction and utilizing every tool from TrumpRx to biosimilar alternatives to protect your household budget.

Visualizing the Drug Cost Crisis: Comparison and Savings

The tables below provide a breakdown of how different patient profiles are impacted by the 2026 changes and the potential savings available through different sourcing methods.

2026 Cost-Saving Comparison by Patient Type

The data below illustrates how the new 2026 protections apply differently across different demographics.

| Patient Category | Primary 2026 Protection | Expected Out-of-Pocket Change | Best Strategic Move |

| Medicare (Part D) | $2,100 Hard Cap | High Savings (for high-cost meds) | Enroll in “Smooth Pay” (MPPP) |

| Uninsured | TrumpRx Portal | Moderate Savings | Compare TrumpRx vs. Cost-Plus |

| Employer Insured | PBM Rebate Pass-Through | Neutral to Low Savings | Ask for “Therapeutic Switching” |

| Low-Income | Expanded LIS (Extra Help) | High Savings | Verify eligibility via SSA.gov |

| Weight-Loss (GLP-1) | Generic/Telehealth Market | Increased Costs (due to coverage loss) | Research validated compounders |

Our Top 3 Picks and Why?

-

The $2,100 Medicare Cap: This is our top pick because it is the single most effective “bankruptcy preventer” in modern healthcare. It provides a definitive end to the infinite out-of-pocket spending for our most vulnerable citizens.

-

Medicare Price Negotiations: We chose this because it tackles the root of the problem—the list price itself. By lowering the starting price, every subsequent layer of the system becomes more affordable.

-

The “Cost-Plus” Disruption: This is an essential pick because it has brought transparency to a previously opaque industry. It proves that medications can be affordable and profitable without the convoluted insurance middleman.

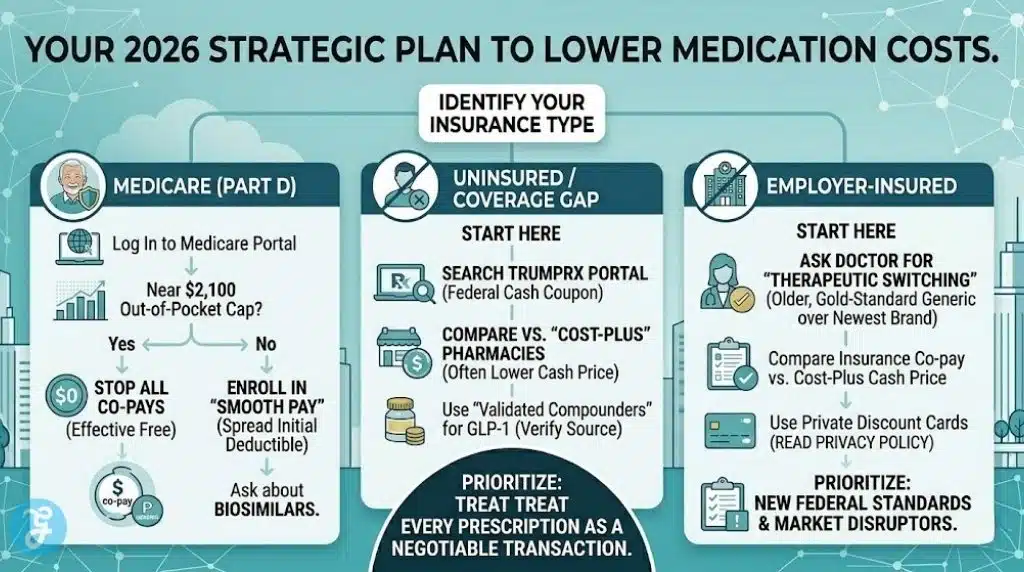

Strategic Implementation Guide: How to Lower Your Medication Costs?

Lowering your bills in 2026 requires a proactive “multi-channel” approach. Do not assume your insurance co-pay is the lowest price available.

The Selection Framework

-

Check the Federal Standard: Start by searching for your medication on the TrumpRx portal. If a negotiated “cash price” coupon is available, it may be lower than your insurance.

-

Audit Your Medicare “Pots”: If you are on Medicare, log into your portal to see how close you are to the $2,100 cap. If you have hit it, your drugs are effectively free for the rest of 2026.

-

Evaluate the “Generic Gap”: If your brand-name drug is too expensive, search for a biosimilar (for biologics) or ask your pharmacist if there is an “interchangeable” generic version.

-

Calculate the Installment Benefit: If you have a high bill in the first few months of the year, use the “Smooth Pay” option to spread that cost out, even if you are below the cap.

Use the decision matrix below to determine the best sourcing method for your specific situation.

Decision Matrix

| If your situation is… | Choose X if… | Choose Y if… |

| On High-Cost Brand Name | Check Medicare Negotiated List for immediate 40%+ savings. | Apply for a PAP directly from the manufacturer. |

| On Multiple Generics | Use Cost-Plus Drugs to bypass insurance co-pays. | Check your local pharmacy $4 list for “loss-leader” pricing. |

| Dealing with Coverage Denial | Appeal via your Doctor for “Medical Necessity.” | Use the TrumpRx Portal for a cash discount. |

| High Bill in January | Enroll in Smooth Pay to spread the cost to December. | Look for a Manufacturer Coupon to cover the deductible. |

The Final Checklist: 5-Point Drug Cost Health Plan

-

Verify your current out-of-pocket total for 2026; if you are near $2,100, do not pay another co-pay.

-

Search for your top three most expensive drugs on the new TrumpRx federal website.

-

Ask your doctor if there is a “biosimilar” or a “therapeutic alternative” that could save you 50% or more.

-

Compare your insurance co-pay against the cash price at a “Cost-Plus” or “Direct” pharmacy.

-

Review your “Explanation of Benefits” (EOB) to ensure your PBM is passing through rebates correctly.

The Prescription Drug Cost Crisis 2026 is being fought on multiple fronts, from the halls of Congress to the smartphone in your pocket. While systemic change is finally arriving in the form of price negotiations and hard caps, the individual responsibility to be a “savvy shopper” remains paramount. By 2026, the tools of the trade—TrumpRx, biosimilar competition, and monthly payment plans have matured into a robust framework that can significantly reduce the burden of illness. Your health should never be a choice between a pill and a meal; by using the roadmap above, you can take control of your pharmaceutical expenses and focus on what matters most: your recovery and your well-being.