No one likes to sit down and think about what happens after they pass away. I get it. It is a grim topic. But ignoring the inevitable is exactly how the taxman ends up taking a massive chunk of your life’s work. Over the last decade, sky-high property prices have pushed everyday families right into the danger zone of the 40% tax bracket.

What used to be a tax strictly for the ultra-wealthy is now a massive headache for regular people who just want to leave their home to their kids. If you do not take action, the government could wipe out nearly half of the wealth you spent decades building. The good news is that with smart UK inheritance tax planning, you can legally and safely shrink that bill. Sometimes, you can even wipe it out entirely. The rules are always shifting, especially with the massive pension and business tax shakeups kicking in between 2026 and 2027. You need to get your house in order today. Let’s look at exactly how the system works and how you can shield your hard-earned cash from the tax office.

| Factor | What it Means for Your Wallet |

| Rising House Prices | Pushes everyday middle-class families into the 40% tax bracket. |

| Frozen Allowances | The £325k threshold is stuck until 2030, acting as a stealth tax on your savings. |

| Upcoming Law Changes | Strict new rules on pensions and business assets hit in 2026 and 2027. |

| The Smart Move | Early action and strategic financial structuring save your family a fortune. |

What is Inheritance Tax in the UK?

Inheritance tax is basically a massive fee the government charges on the estate of someone who has died. Your estate is literally everything you own at the time of your death. We are talking about your house, your savings accounts, your stocks, your cars, and even payouts from life insurance if you have not set them up properly in a trust. Once your executor tallies up the total value of your assets, they deduct your outstanding debts and funeral costs.

If whatever is left over sits above the government’s set limit, HM Revenue and Customs (HMRC) steps in and takes 40% of everything above that line. It sounds harsh, and for many grieving families, it feels incredibly unfair. However, understanding the exact rules of the game is the first step to beating them and keeping your wealth in the family.

| Allowance Type | Current Limit | Who Can Use It |

| Basic Nil Rate Band | £325,000 | Everyone (frozen until 2030). |

| Residence Nil Rate Band | £175,000 | Parents passing a main home to direct descendants. |

| Combined Single Allowance | Up to £500,000 | Single homeowners passing property to kids. |

| Combined Married Allowance | Up to £1,000,000 | Married couples passing property to kids. |

Current Tax Thresholds and Allowances

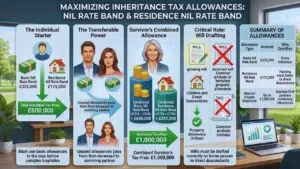

To figure out how to save cash, you first need to know your basic allowances inside and out. The standard nil rate band currently sits at £325,000. That means the first £325,000 of your estate is completely tax-free. The government locked this number back in 2009 and recently confirmed it will stay frozen until at least 2030. If you plan to leave your main home to your kids or grandkids, you get a bonus allowance called the residence nil rate band.

Right now, that gives you an extra £175,000 of tax-free space. Add those two together, and a single person can pass on £500,000 without paying a single penny. Married couples can double this to £1 million. Just be aware that if your total estate is worth over £2 million, you start losing this property allowance at a rate of £1 for every £2 you are over the limit.

13 Proven Tips to Reduce Your Inheritance Tax Bill

When it comes to UK inheritance tax planning, doing nothing is the most expensive mistake you can make. The tax code is packed with legal exemptions, allowances, and strategies designed to help you pass wealth down the generations efficiently. You just have to know where to look and how to apply them to your specific financial situation. I have broken down the 13 most effective, battle-tested strategies to help you protect your assets from HMRC.

Some of these are incredibly simple tricks you can start doing this afternoon with a quick bank transfer. Others require a bit of legal setup or a chat with a financial advisor to get right. Either way, implementing even a handful of these steps will save your family a small fortune when the time comes.

1. Maximize the Nil Rate Band and Residence Nil Rate Band

This is the absolute bedrock of good financial planning, and you must make sure you use your basic allowances to the max before looking at complex loopholes. As mentioned, a single person has a £325,000 allowance plus a £175,000 property allowance, bringing the total to £500,000. But married couples and civil partners hold the real power here. When one partner dies, they can pass any unused tax-free allowance to the survivor. That means a surviving spouse can hold a combined basic band of £650,000 and a combined property band of £350,000.

A married couple can pass on exactly £1 million completely tax-free to their children. You just need to ensure your wills are drafted correctly so that the home actually passes to direct descendants, otherwise, you forfeit that extra property allowance entirely. Failing to utilize this double allowance is one of the most common and expensive mistakes grieving families discover during probate.

| Allowance Type | Amount | Who Qualifies |

| Basic Nil Rate Band | £325,000 | Every individual |

| Residence Nil Rate Band | £175,000 | Passing main home to direct descendants |

| Married Couple Maximum | Up to £1,000,000 | Married/Civil partners combining allowances |

2. Transfer Assets Using the Spousal Exemption

You do not pay a dime in inheritance tax on anything you leave to your husband, wife, or registered civil partner. It is a 100% complete exemption under UK law. You could leave an estate worth £50 million to your spouse, and HMRC gets absolutely nothing when you die. This lets couples shuffle their money, property, and stock portfolios around while they are still alive without stressing about tax traps. Just remember, you must be legally married or in a civil partnership for this to work.

The law does not care if you have lived with your partner for 40 years and shared a bank account the whole time. If there is no ring or legal document, unmarried partners face a brutal 40% tax charge on anything over the standard £325,000 mark. Many long-term cohabiting couples end up getting married later in life purely to secure this massive financial shield for the surviving partner.

| Recipient | Tax Rate | Condition |

| Married Spouse | 0% | Must be legally married |

| Civil Partner | 0% | Must be legally registered |

| Unmarried Partner | 40% (above £325k) | Cohabiting without legal marriage/partnership |

3. Use Your Annual Gifting Exemption

Want to shrink your taxable estate quickly? Start giving your money away while you are still around to see your kids enjoy it. Every person in the UK gets an annual gifting exemption of £3,000. You can hand this cash to one person or chop it up among five people. Either way, it instantly vanishes from your taxable estate. If you forget to use it one year, the government lets you carry it forward to the next year, meaning you could give away £6,000 in one go.

A married couple who did not use their allowance last year could jointly dump £12,000 into their kids’ bank accounts right now, completely tax-free. Doing this consistently over 10 or 15 years removes a massive chunk of cash from the taxman’s reach without requiring any complicated legal paperwork or expensive advice. It is the easiest habit to build into your yearly financial routine.

| Exemption Feature | Details | Benefit |

| Annual Limit | £3,000 per tax year | Instantly leaves your taxable estate |

| Carry Forward | 1 year maximum | Can gift up to £6,000 in one go if unused prior year |

| Couples Potential | £6,000 combined per year | Massive reduction over a decade |

4. Give Gifts Out of Normal Expenditure

Financial advisors often call this the best-kept secret in British tax law. If you have extra income that you do not need to live your normal life, you can give it away tax-free. The best part is that there is absolutely zero upper limit on this rule. It is incredibly powerful if you have a massive pension, a high salary, or huge dividend payouts from investments. The catch is strict: the cash must come from your regular income, not your savings or capital gains.

You also have to prove that giving this money away does not ruin your standard of living or force you into debt. Common moves include paying your grandkids’ private school fees, covering a child’s mortgage payments, or paying someone’s life insurance premiums directly out of your monthly paycheck. Doing this bleeds cash out of your estate fast, but you must keep meticulous records to prove it was genuinely surplus income.

| Rule Requirement | Explanation | Common Examples |

| Source of Funds | Must come from regular income, not capital | Pensions, salary, dividend payouts |

| Lifestyle Impact | Cannot negatively impact standard of living | Grandkid’s school fees, monthly savings |

| Financial Limit | No upper limit | Removes excess cash from 40% tax |

5. Take Advantage of Small Gifts and Wedding Allowances

On top of your £3,000 main allowance, you can give as many “small gifts” of up to £250 per person as you want every single tax year. You could hand £250 to 20 different friends, nieces, or nephews, and it is all completely tax-free. The only rule is you cannot give this £250 to someone who already took a slice of your main £3,000 allowance. Weddings are another massive loophole you should exploit. If your child is getting married, you can gift them £5,000 tax-free.

Grandkids or great-grandkids tying the knot? You can give them £2,500. For literally anyone else getting married, like a friend or a cousin, you can give £1,000. These specific allowances stack up fast and help bleed money out of your estate legally. Timing these gifts around family milestones is a brilliant way to help the younger generation while simultaneously frustrating HMRC’s collection efforts.

| Gift Type | Maximum Amount | Who Can Receive It |

| Small Gift | £250 per person/year | Anyone (not using the £3,000 allowance) |

| Child’s Wedding | £5,000 | Your own child tying the knot |

| Grandchild’s Wedding | £2,500 | Grandchild or great-grandchild |

| Anyone Else’s | £1,000 | Friends, cousins, neighbors |

6. Understand the 7-Year Rule for Larger Gifts

If you want to give away massive chunks of cash, like a £50,000 house deposit for your son, you step into the zone of “Potentially Exempt Transfers” (PETs). The rule is simple: you can give away as much money or property as you want while you are alive. If you live for seven full years after handing it over, it drops completely out of your estate, and HMRC cannot touch it. If you die before those seven years are up, the gift gets dragged back into your estate for the final tax math.

But if you survive at least three years, a sliding scale called “taper relief” kicks in. The 40% tax rate slowly drops down to 32%, then 24%, then 16%, and finally 8% the closer you get to the seven-year finish line. Give early to maximize this benefit. Waiting until you are seriously ill to hand out large sums of money guarantees the government will take their 40% cut.

| Years Since Gift | Tax Rate Paid (Taper Relief) | Outcome |

| 0 – 3 Years | 40% | Full tax applies if estate is over threshold |

| 3 – 4 Years | 32% | 20% reduction on the tax bill |

| 4 – 5 Years | 24% | 40% reduction on the tax bill |

| 7+ Years | 0% | Completely free from inheritance tax |

7. Prepare for the 2027 Pension Rule Changes

For decades, pensions were the ultimate bulletproof vest against estate taxes in the UK. Money left in a defined contribution pension passed to the kids completely tax-free. Well, the party is officially over. The government is changing the rules dramatically. Starting in April 2027, unused pension pots and death benefits will be dragged directly into your estate value for tax purposes. This flips retirement planning completely upside down for millions of people. People used to drain their normal savings and leave their pensions untouched to dodge tax.

Now, that strategy is a massive trap. You need to talk to a financial advisor right away. It might actually make more sense to drain your pension earlier, gift the cash, or move the money into different tax-efficient wrappers before 2027 hits. Ignoring this upcoming change could cost your family hundreds of thousands of pounds in completely avoidable taxes.

| Timeframe | Pension Tax Rule | Impact on Estate |

| Current Rule | Generally tax-free upon death | Used to shelter wealth from inheritance tax |

| April 2027 Onwards | Added to taxable estate value | Unused pots face up to 40% inheritance tax |

| Action Needed | Review drawdown strategy | May need to spend pension sooner |

8. Adapt to New Limits on Business and Agricultural Relief

Owning a farm or a trading business used to be a golden ticket for estate planning. It offered 100% relief from inheritance tax, meaning you could hand the family farm or the family firm down to the kids without them having to sell it to pay the taxman. The recent budgets completely crushed this benefit. From April 2026, that 100% relief is strictly capped at £1 million combined for business and agricultural assets.

Anything over that £1 million mark only gets 50% relief, which creates an effective 20% tax rate on the excess value. If you own a successful company or a large farm, you have to rewrite your succession plan today. If you do not prepare liquidity to pay this new tax, your kids will be forced to liquidate the business or sell off acreage just to settle the massive bill with HMRC.

| Asset Value | Old Rule (Pre-April 2026) | New Rule (From April 2026) |

| Up to £1 Million | 100% Tax Relief | 100% Tax Relief |

| Over £1 Million | 100% Tax Relief | 50% Tax Relief (Effective 20% tax rate) |

| The Big Risk | Keeping business intact | Heirs forced to sell assets to pay the tax |

9. Set Up a Trust to Protect Family Assets

Trusts sound like something only billionaires and politicians use, but they are incredibly useful for normal, middle-class families too. A trust is simply a legal setup where you hand your money or property over to a group of people, called trustees, to manage for someone else, called beneficiaries. Dumping cash into a trust pulls it out of your taxable estate, assuming you survive the standard seven years after making the transfer.

Trusts are absolutely perfect if you want to leave money to grandkids who are way too young or irresponsible to handle a massive lump sum at 18. They are also brilliant for keeping your cash strictly in your bloodline, protecting it if your child ends up getting a nasty divorce down the road and their ex-spouse tries to claim half. Setting them up requires a solicitor, but the long-term protection and tax savings make the initial legal fees completely worth it.

| Trust Benefit | How It Works | Best Used For |

| Estate Reduction | Assets leave estate after 7 years | Moving large sums of wealth |

| Control | Trustees manage the money | Young or irresponsible beneficiaries |

| Bloodline Protection | Shields cash from divorces/creditors | Keeping wealth strictly in the family |

10. Lower Your Tax Rate by Donating to Charity

Anything you give to a registered charity in the UK is 100% exempt from inheritance tax. If you leave a specific pile of cash, an art collection, or even a house to charity in your will, that value is wiped off your estate before HMRC does their math. But the government goes a step further to reward generosity. If you leave at least 10% of your net estate to a qualifying charity, the tax rate on the rest of your taxable wealth drops from 40% down to 36%.

For families hovering just over the tax threshold, this math sometimes works out brilliantly. The tax savings can mean the kids get roughly the same amount of money they would have anyway, but a charity gets a massive, life-changing payout instead of the government. It is a fantastic way to build a personal legacy while legally stripping HMRC of their revenue.

| Donation Type | Tax Benefit | Financial Impact |

| Any Charity Gift | 100% tax-free | Reduces overall estate value |

| 10% of Net Estate | Cuts remaining tax rate to 36% | Leaves more for heirs and charity, less for HMRC |

| Community Good | Funds local or national causes | Creates a lasting legacy while saving money |

11. Use Life Insurance to Cover the Bill

Sometimes, dodging the tax is mathematically impossible. If your wealth is locked up in a huge London house or a family business you refuse to sell, your kids are going to face a massive tax bill with absolutely no liquid cash to pay it. The smartest fix is buying a specific product called a “whole of life” insurance policy. You pay a premium every month, and when you die, the policy drops a massive lump sum exactly big enough to cover the estimated tax bill.

But here is the critical part: you absolutely must write this policy in trust. If you don’t, the payout just gets added to your estate, inflating your tax bill even more. Written in trust, the cash bypasses your estate and goes straight to the kids so they can hand it straight to HMRC without having to mortgage their own homes.

| Policy Setup | How It Works | Tax Consequence |

| Standard Policy | Pays lump sum on death | Added to estate, inflates tax bill |

| Written in Trust | Bypasses the estate entirely | 100% tax-free payout to family |

| Primary Use | Covers the final HMRC bill | Prevents fire-sale of the family home |

12. Spend Your Wealth While You Can

It sounds crazy to put this on a list about financial planning, but it is entirely true. You spent 40 years grinding for this money, and you have every right to spend it on yourself. Go on a luxury cruise, buy the sports car you always wanted, renovate the kitchen, or fly first class. Every single pound you spend on yourself is a pound that naturally shrinks your taxable estate. I constantly see older folks living incredibly frugal lives out of sheer habit, hoarding cash in a low-interest bank account.

When they pass, the government just walks in and takes 40% of it. The easiest and most enjoyable strategy for UK inheritance tax planning is simply enjoying the fruits of your labor while you still have your health and mobility. You cannot take it with you, so you might as well spend it rather than leaving it for the taxman to squander.

| Action | Result on Estate | Lifestyle Benefit |

| Hoarding Cash | 40% goes to the government | Frugal, restrictive retirement |

| Home Upgrades | Increases comfort, naturally drains cash | Better daily living environment |

| Travel & Hobbies | Shrinks taxable liquid assets | You enjoy the money you earned |

13. Keep Excellent Records of All Financial Gifts

When you die, your executors have the miserable, stressful job of digging through your bank statements and proving your financial history to the government. If they cannot prove that the £3,000 you gave your daughter was your annual allowance, or that the £500 a month to your grandson came out of your surplus income, HMRC will ruthlessly classify it as a taxable gift. Go to the store, buy a cheap notebook, or open an Excel spreadsheet, and write down every single financial gift you make.

Log the exact date, the exact amount, who got it, and which legal exemption you are using. If you are using the “normal expenditure” rule, keep a spreadsheet of your monthly income and bills to prove you could afford it. This 5-minute habit saves your grieving family months of agony and thousands in legal fees trying to fight HMRC during probate.

| Record Type | Why You Need It | HMRC Consequence if Missing |

| Gift Log | Proves date and amount given | Treat as a taxable Potentially Exempt Transfer |

| Income/Expense Sheet | Proves “normal expenditure” affordability | HMRC claims it was from capital, taxing it 40% |

| Will & Trust Docs | Shows legal routing of assets | Delays probate, causes massive family stress |

Why You Need to Start Planning Now?

The days of setting up a simple will and forgetting about your finances are over. The British tax landscape is getting aggressive, and the government is actively looking for ways to boost tax revenue. They are using frozen thresholds to quietly drag more people into the tax net through inflation. Add in the looming April 2026 business relief caps and the April 2027 pension tax changes, and the message is clear: the rules are rigged against those who wait until the last minute.

Proper estate structuring takes real time and effort. You cannot wait out a seven-year rule if you are already severely ill, and you cannot restructure a massive family business overnight. Grab a coffee, sit down with your spouse, and start mapping out where your money is going right now. Booking a meeting with a qualified financial advisor today is the smartest investment you will ever make to protect your family’s future.

| Action Step | Timeline | Why You Must Do It |

| Audit Your Estate | This Month | You cannot fix a problem if you do not know exactly what you are worth today. |

| Review Pension Rules | Before April 2027 | Prevent your hard-earned pension from becoming a sudden 40% tax trap. |

| Start Annual Gifting | By April 5th | Max out your £3,000 allowance before the current tax year resets. |

| Update Your Will | Within 6 Months | Ensure your assets are legally routed in the most tax-efficient way possible. |

Final Thoughts

Watching the government slice 40% off the wealth you spent a lifetime accumulating is a bitter pill to swallow for anyone. But as we have covered today, it is largely an optional tax for those who prepare early and act decisively. Effective UK inheritance tax planning is not about dodging your legal duties or hiding money in offshore accounts; it is about using the exact rules, thresholds, and allowances the government gave you to protect your family. Start with the quick wins.

Use your annual £3,000 gifting allowance today and start keeping a tight record of your surplus income gifts. Most importantly, do not ignore the massive pension and business changes rolling out in 2026 and 2027. Speak to an expert, get your paperwork in order, and go enjoy the wealth you worked so hard to build.