As we approach the final days of the 2025/26 financial year, the window for optimizing your tax position is rapidly closing. With the current economic landscape and frozen thresholds, effective 2025 UK tax planning is no longer just for the wealthy; it is a necessity for anyone looking to shield their hard-earned income from “fiscal drag.” By taking strategic steps now, you can fully utilize your legal allowances and ensure you aren’t paying a penny more to HMRC than is absolutely required.

Our Selection Methodology

To compile this comprehensive list of pro tips, we reviewed the 2025/26 HMRC tax tables, current legislation regarding capital gains, and the latest pension annual allowance rules. We prioritized strategies that offer the highest immediate impact on tax liability for a broad range of taxpayers, from basic-rate employees to high-net-worth business owners. Each tip was assessed based on its feasibility in the final ten days of the tax year and its ability to provide long-term fiscal benefits under the 2026 economic conditions.

Smart Strategies for 2025 UK tax planning

Navigating the complexities of the UK tax code requires a proactive approach. The following 15 tips represent the most effective ways to manage your liabilities before the new tax year begins on April 6th.

1. Maximize Your £20,000 ISA Allowance

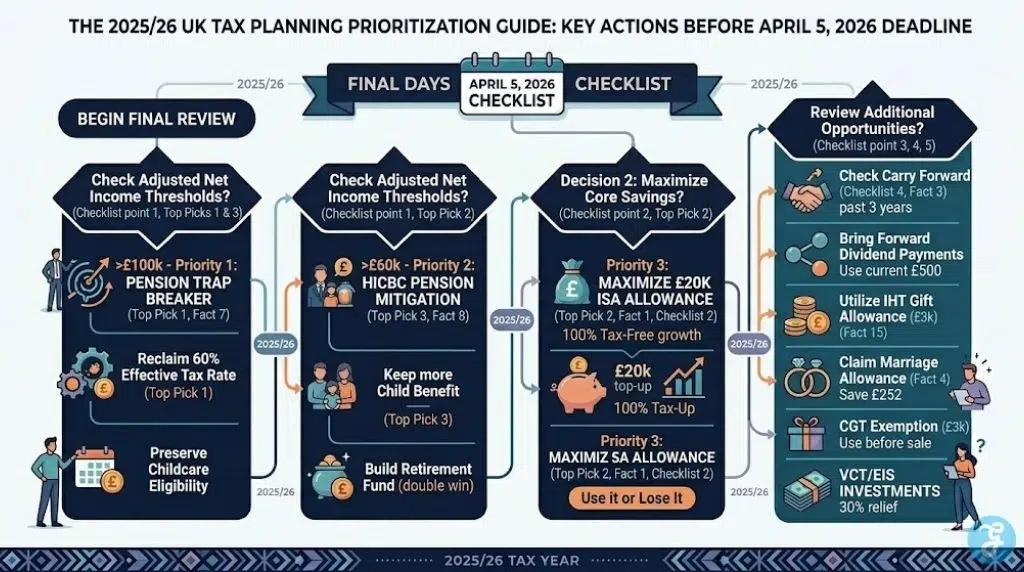

The Individual Savings Account (ISA) remains one of the most powerful tools in your arsenal, allowing you to save or invest up to £20,000 each year completely tax-free. Whether you choose Cash, Stocks & Shares, or an Innovative Finance ISA, the returns are shielded from both Income Tax and Capital Gains Tax.

Best for: Savers and investors looking for a long-term, tax-efficient home for their surplus cash.

Things to consider: The £20,000 limit is “use it or lose it,” meaning any unused portion cannot be carried forward to the 2026/27 tax year.

While the ISA is perfect for general savings, your pension offers even more significant upfront tax relief.

2. Utilize the £60,000 Pension Annual Allowance

For most taxpayers, you can contribute up to £60,000 (or 100% of your relevant UK earnings, whichever is lower) into your pension and receive tax relief at your highest marginal rate. This effectively means a £10,000 contribution only costs a basic-rate taxpayer £8,000, or just £6,000 for a higher-rate taxpayer.

Best for: Individuals aiming to build a retirement nest egg while significantly reducing their current year’s income tax bill.

Things to consider: Ensure your total contributions across all pension pots do not exceed the allowance, as excess contributions are subject to a tax charge.

If you have already hit this year’s limit, you may be able to look back at previous years.

3. Leverage Pension “Carry Forward” Rules

If you haven’t used your full annual allowance in the previous three tax years, you can “carry forward” the unused portions to the current 2025/26 year. This can allow for a much larger tax-relievable contribution if you have had a sudden spike in income.

Best for: High earners or business owners who had lower pension contributions in 2022, 2023, or 2024.

Things to consider: You must have been a member of a registered pension scheme during those previous years to be eligible for carry forward.

Managing your allowances is also a family affair, especially when it comes to shared benefits.

4. Claim the Marriage Allowance Transfer

If one spouse or civil partner earns less than the personal allowance (£12,570) and the other is a basic-rate taxpayer, you can transfer £1,260 of the unused allowance. This can reduce the higher-earning partner’s tax bill by up to £252 for the year.

Best for: Couples where one partner works part-time, is a stay-at-home parent, or is retired with a low pension.

Things to consider: This is only available if the higher-earning partner does not pay tax at the higher (40%) or additional (45%) rates.

Investment income also has its own set of dedicated allowances that shouldn’t be ignored.

5. Exhaust the £500 Dividend Allowance

In the 2025/26 tax year, the first £500 of dividend income is tax-free. If you own a limited company or hold shares outside of an ISA, ensuring you utilize this small but helpful threshold is a key part of 2025 UK tax planning.

Best for: Small business directors and retail investors with significant shareholdings in taxable accounts.

Things to consider: Any dividends above this £500 limit are taxed at 8.75% for basic rate, 33.75% for higher rate, and 39.35% for additional rate taxpayers.

Similarly, selling assets requires careful timing to stay within the exempt amounts.

6. Use Your £3,000 Capital Gains Tax (CGT) Exemption

The CGT annual exempt amount currently stands at £3,000. If you are planning to sell second homes, stocks (outside an ISA), or other valuable assets, doing so before April 5th allows you to realize gains up to this amount without paying tax.

Best for: Investors looking to “rebalance” their portfolios or sell off assets to fund other ventures.

Things to consider: If you are married, you can transfer assets to your spouse before the sale to utilize two sets of allowances, effectively doubling your tax-free gain to £6,000.

Beyond simple allowances, some strategies involve shifting your taxable income entirely.

7. Avoid the “Personal Allowance Trap” at £100,000

For every £2 you earn above £100,000, you lose £1 of your personal allowance. This creates an “effective” tax rate of 60% on income between £100,000 and £125,140. Making a pension contribution or a charitable donation to bring your “adjusted net income” back down to £100,000 is one of the smartest moves you can make.

Best for: Professionals earning between £100,000 and £130,000 who want to avoid a massive spike in their tax bill.

Things to consider: This strategy also helps preserve your eligibility for tax-free childcare and 30 hours of free childcare.

Child-related benefits are another area where income thresholds are strictly enforced.

8. Mitigate the High Income Child Benefit Charge (HICBC)

In 2026, the HICBC starts to apply when one partner earns over £60,000 and is fully repayable once income hits £80,000. Just like the personal allowance trap, pension contributions can be used to lower your income and keep more of your Child Benefit.

Best for: Families where the highest earner is approaching or slightly over the £60,000 threshold.

Things to consider: The charge is tapered, meaning for every £200 of income over £60,000, you lose 1% of the benefit.

Saving for the next generation can also provide immediate tax-efficient homes for your capital.

9. Fund a Junior ISA (JISA) for Your Children

The JISA allowance is £9,000 per child for the 2025/26 tax year. While this doesn’t offer immediate income tax relief for the parent, all growth and interest within the account are tax-free for the child.

Best for: Parents and grandparents who want to build a long-term fund that the child can access at age 18.

Things to consider: Once the money is in a JISA, it belongs to the child and cannot be withdrawn by the parent for other purposes.

If you have spare space in your own home, you can also generate tax-free income directly.

10. Utilize the Rent-a-Room Relief

If you rent out a furnished room in your main home, you can earn up to £7,500 per year completely tax-free. This is an automatic relief, meaning if your rental income is below this, you don’t even need to report it to HMRC.

Best for: Homeowners with a spare bedroom who are looking for a simple way to supplement their income.

Things to consider: If you share the income with a partner, the limit is halved to £3,750 each.

Smaller “side hustles” also benefit from specific exemptions.

11. Claim the £1,000 Trading and Property Allowances

HMRC provides two separate £1,000 allowances: one for “trading” (like selling on eBay or freelance work) and one for “property” (like renting out a parking space). If your gross income from these sources is under £1,000 each, it is tax-free.

Best for: Casual sellers, micro-influencers, and those with very small-scale rental income.

Things to consider: You cannot use these allowances if you are already deducting actual expenses from your income for tax purposes.

Generosity can also be a strategic part of your end-of-year planning.

12. Use Gift Aid to Extend Your Tax Bands

When you donate to charity via Gift Aid, the charity gets an extra 25%. However, higher-rate and additional-rate taxpayers can also claim back the difference between the basic rate and their highest rate via their tax return, effectively extending their basic rate tax band.

Best for: Philanthropic individuals who pay tax at 40% or 45%.

Things to consider: You must keep records of your donations to ensure you claim the correct amount on your Self Assessment.

For those willing to take on more risk, specialist investment schemes offer substantial rewards.

13. Invest in VCTs or EIS for 30% Tax Relief

Venture Capital Trusts (VCTs) and the Enterprise Investment Scheme (EIS) offer a massive 30% upfront income tax relief on investments up to £200,000 (VCT) or £1 million (EIS). This means a £10,000 investment could reduce your tax bill by £3,000.

Best for: Sophisticated investors with high tax bills who are comfortable with the risks of investing in smaller, unquoted companies.

Things to consider: You must hold VCT shares for at least five years and EIS shares for three years to keep the tax relief.

Even family members who don’t work can still benefit from pension planning.

14. Contribute to a Pension for a Non-Earning Spouse

You can contribute up to £2,880 into a pension for a spouse or child who has no income. The government will automatically add 20% tax relief, bringing the total contribution to £3,600.

Best for: Providing a financial head start for children or ensuring a non-working partner has their own retirement fund.

Things to consider: This is a highly efficient way to move money out of your taxable estate for inheritance tax purposes as well.

Finally, don’t forget the annual limits for passing on wealth.

15. Make Use of the £3,000 IHT Annual Gift Allowance

You can give away up to £3,000 worth of gifts each tax year without them being added to the value of your estate for Inheritance Tax (IHT). Like the ISA, if you didn’t use last year’s allowance, you can carry it forward for one year only.

Best for: Older individuals looking to gradually reduce their estate’s IHT liability.

Things to consider: Small gifts of up to £250 per person are also exempt, provided they are not to the same person who received your £3,000 gift.

Strategic Analysis

To help you prioritize your actions in these final days, the following table compares the most common 2025 UK tax planning tools based on their immediate tax-saving potential and ease of implementation.

| Tool / Allowance | Max Limit | Primary Benefit | Ease of Setup |

| ISA Contribution | £20,000 | 100% Tax-Free Growth | Very High |

| Pension Relief | £60,000 | Up to 45% Income Tax Relief | High |

| VCT / EIS | £200k / £1m | 30% Upfront Tax Credit | Moderate |

| Marriage Allowance | £1,260 | £252 Direct Tax Saving | High |

| CGT Exemption | £3,000 | Tax-Free Asset Disposal | Moderate |

Our Top 3 Picks And Why?

-

Pension Contribution (The Trap Breaker): This is our top pick because it offers the unique ability to reclaim the 60% effective tax rate for those in the £100k-£125k bracket, providing the single highest “bang for your buck.”

-

ISA Allowance: This is the most essential “foundation” tip. It is easy to set up, and the cumulative benefit of years of tax-free growth is life-changing for long-term wealth.

-

HICBC Pension Mitigation: For families, this is a “double win” as it keeps more cash in the household via Child Benefit while simultaneously building a retirement fund.

Preparation Checklist

Ensure you have completed these steps before midnight on April 5th to lock in your 2025/26 benefits:

-

Check your “adjusted net income” to see if you are approaching the £100k or £60k thresholds.

-

Log into your ISA provider and ensure you have utilized as much of the £20,000 limit as possible.

-

Contact your pension provider to confirm the total contributions made this year (including employer contributions).

-

Review any unused pension allowance from 2022/23, as this will expire forever on April 6th.

-

If you are a business owner, consider bringing forward dividend payments to utilize the current year’s £500 allowance.

Taking Control of Your 2026 Fiscal Outlook

Mastering your 2025 UK tax planning is about more than just numbers; it’s about ensuring that your financial strategy aligns with your life goals. By utilizing the 15 tips outlined above, you can turn the complexities of the HMRC system into a series of advantages that protect your income and accelerate your path to financial independence. As the April 5th deadline looms, the most important step is to act now—once the clock strikes midnight, these specific 2025/26 opportunities are gone for good.

FAQs

When is the absolute deadline for 2025/26 tax planning?

The tax year ends at midnight on April 5, 2026. However, many banks and investment platforms have earlier internal cut-off times for processing payments.

Can I still use my 2024/25 ISA allowance?

No, once the tax year ends, any unused ISA allowance for that year is lost. You cannot carry it forward to the 2025/26 or 2026/27 years.

How much can I put into my pension if I don’t work?

If you have no relevant UK earnings, you can still contribute up to £2,880 net (£3,600 gross) into a pension and receive 20% tax relief.

Do I need to report my ISA on my tax return?

No, income and gains generated within an ISA are completely tax-free and do not need to be declared on your Self Assessment tax return.