When you take out a personal loan, the interest rate doesn’t just shape your monthly EMI — it decides the real price tag for your loan. Even a small difference, say 1–2%, can mean thousands of rupees more on a ₹5 lakh loan. So, comparing rates is absolutely necessary.

Luckily, checking out different lenders and their offers isn’t as complicated as it sounds, as long as you know what to pay attention to.

What Decides Your Personal Loan Interest Rate

Right now in India, personal loan interest rate run anywhere from about 9.60% all the way up to 35%, depending on who you borrow from and what your financial profile looks like.

Here’s what really matters:

- Your credit score: If it’s credit score 750 or higher, you’re usually looking at better rates.

- Your monthly income and how steady your job is: Financial Institutions trust borrowers with stable, higher incomes.

- Your relationship with the bank: Existing customers or pre-approved folks often get special deals.

- Loan amount and tenure: Sometimes, lenders treat short-term and long-term loans differently.

- Your job profile: Salaried employees at bigger, well-known companies usually get more attractive rates than self-employed people.

- Knowing where you stand on these points helps you figure out if the offer you’ve got actually makes sense for you.

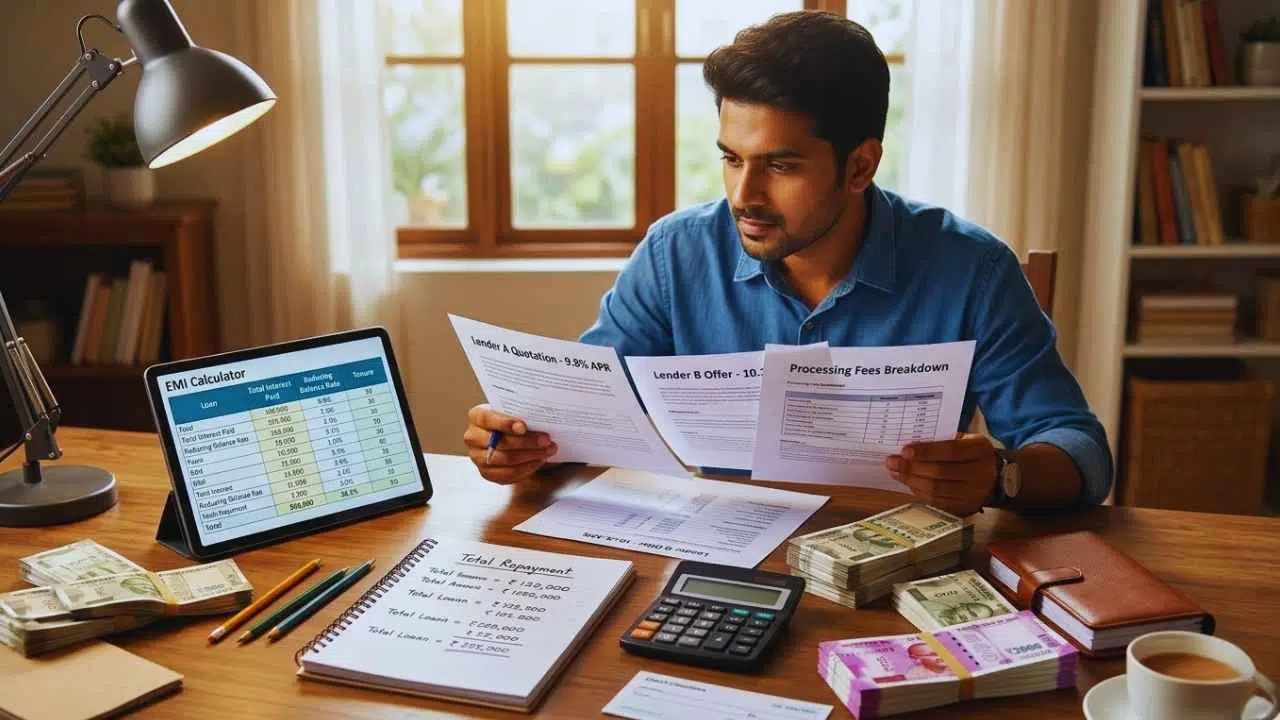

How to Really Compare Personal Loan Interest Rates

Don’t Get Fooled by Headline Rates

That eye-catching rate in the ad? It’s usually reserved for people with flawless credit. Instead of falling for that, ask each lender for a rate quote that’s based on your own details — your income, your credit score, and how much you want to borrow. The real rate you get might be very different from the one splashed across their website.

Check the Total Cost, Not Just the EMI

Lower EMI doesn’t always mean a cheaper loan. Stretching out your tenure drops your monthly payment, but you’ll end up paying more interest over time. Use a personal loan calculator to see exactly how much you’ll repay — principal plus interest — with each lender, for the same loan amount and tenure. That’s the number that really matters.

Don’t Ignore Processing Fees and Charges

Processing fees usually run from 0.5% to 5% of the loan amount. On a ₹10 lakh loan, a 3% processing fee is ₹30,000 right off the bat. Always include these fees when you’re looking at the total cost, not just the rate. Sometimes financial institutions offer deals with lower or even zero processing fees, especially during promotions, and that can tip the scales when rates are otherwise similar.

Make Sure You’re Comparing Apples to Apples

Always convert everything to an annualized reducing balance rate so you’re comparing the same thing. For example, a flat rate of 8% costs a lot more than a reducing balance rate of 8%, because with flat rates, you pay interest on the original loan amount the entire time, no matter how much you’ve paid back.

Wrapping Up

Taking the time to compare personal loan interest rates pays off — it saves you more money than you’d think, and it doesn’t eat up nearly as much time as people assume. Check the real rate for your profile, add up the total repayment (fees included), and make sure you compare the offers fairly. A little effort upfront means you won’t end up paying more for your loan than you have to.