Bad credit can feel like a heavy burden, making it harder to get approved for a Credit Card With Bad Credit. Frequent rejections and high interest rates only add to the frustration. Many people face this challenge after setbacks like job loss or medical expenses. Just when it’s time to rebuild, lenders often seem out of reach.

Credit scores range from 300 to 850, and anything below 580 is considered poor—leading to lower approval chances and higher APRs.

This guide simplifies the process with practical steps, including checking your credit report at AnnualCreditReport.com, choosing secured options like the Capital One Platinum Secured Credit Card, and using prequalification tools to avoid hard inquiries.

It also covers key factors like payment history and credit utilization to help improve your FICO score and increase approval odds.

What Does It Mean to Have Bad Credit?

People often face bad credit after a string of missed payments or tough times repaying debts. This situation drags down your credit score, and lenders see you as a higher risk. FICO labels a score below 580 as poor, way under the U.S. average of 715 as of April 2025.

Scores in the poor range sit between 300 and 579, while fair credit runs from 580 to 669, and good credit hits 670 to 739. Think of bad credit like a bumpy road in your credit history; it shows up through reports from credit bureaus like Equifax and TransUnion.

Folks with this issue struggle to snag loans or cards, but hey, it’s not the end of the world, you can start rebuilding credit with smart financial habits.

Bad credit stems from patterns like high credit utilization ratios or ignored bills, making approval for new credit tricky. Credit management tools, such as Experian Boost, can help lift your score by adding positive payments.

Lenders check your credit report for these red flags during the application process. You might feel stuck, like trying to climb a slippery hill, but options exist for fair credit or no credit folks.

Secured cards often require a security deposit, yet they pave the way for better terms later. Tools like CreditWise let you monitor progress without a hard inquiry, keeping things smooth as you work on that credit history.

Types of Credit Cards for Bad Credit

Bad credit feels like a roadblock, huh, but special cards can pave the way forward, with features like credit limits that match your deposit. Stick with me, and you’ll see how options such as unsecured cards, often from issuers like Capital One, offer a fresh start despite higher annual percentage rates.

Secured Credit Cards

You put down a refundable security deposit with secured credit cards, and that sets your credit limit. Lenders see less risk this way, so they approve folks with bad credit more often.

Think of it like a safety net; your cash backs up the card. Deposits usually run from $200 to $500. Pick secured cards from big names; they fit your personal finance needs best. The Capital One Platinum Secured Credit Card asks for just $49 up front for a $200 credit line at minimum.

First Progress Prestige Secured Mastercard needs a $200 deposit. OpenSky Plus Secured Visa Credit Card offers another choice, with no credit check required.

Use the card wisely for 12 to 18 months, and you might upgrade to unsecured credit cards. Pay on time, keep balances low, and watch your score climb. Issuers report to bureaus like the Consumer Financial Protection Bureau tracks.

Get cash back rewards on some, or aim for lower APR options. Your deposit comes back if you close the account in good standing. Compare offers on sites like Bankrate or CreditCards.com.

Navy Federal online has tools for members too. Chase, Citi, American Express, and Bank of America provide alternatives, but start here to rebuild.

Unsecured Credit Cards

Unsecured credit cards skip the security deposit, which makes them appealing if you hate tying up cash. Lenders base approval on your credit history, so expect higher APR and lower limits with bad credit.

Take the FIT Platinum Mastercard; it starts you at a $400 credit limit without any deposit. Folks often apply through a simple credit card application process, and some get instant approval after a soft credit inquiry.

Rebuilding credit without upfront money, like getting a second chance at bat.

The Reflex Platinum Mastercard offers up to $1,000 initial limit, no deposit needed, perfect for steady progress. Milestone Mastercard and Indigo Mastercard guarantee that $1,000 limit right away, easing the sting of past mistakes.

Aspire Cash Back Rewards Mastercard and Fortiva Cash Back Rewards Mastercard push limits to $1,000 too, subject to your approval odds. These cards charge higher interest rates, so pay on time to avoid extra fees.

Think of them as tools to fix your score, one swipe at a time, without the hassle of secured options.

Credit-Builder Cards

Credit-builder cards help you improve your credit profile. They report your payments to big agencies like Experian, Equifax, and TransUnion. Take the PREMIER Bankcard Mastercard Credit Card, for example.

It builds credit with monthly reports to consumer reporting agencies. You make payments, and that positive history boosts your score. Institutions offer savings-linked options too.

These programs aim to lift your credit step by step. Rebuilding your credit like fixing a leaky roof, one shingle at a time. The Perpay Credit Card suits folks with bad credit.

It gives access to a credit line up to $1,500. Plus, no hard credit check hits your score. You shop with it like a virtual credit card. Perpay reports to all three major bureaus. That builds your history across the board.

Credit-builder cards act like training wheels for your finances, they steady you until you ride solo with better credit, says Holly D. Johnson, a credit expert.

Steps to Get Approved for a Credit Card with Bad Credit

If your credit score feels like a flat tire on the road to financial freedom, don’t sweat it—we’ll walk you through simple moves, like pulling your Experian report to spot mistakes or proving steady paychecks with bank statements, that boost your odds with issuers such as Capital One, so keep reading for the full scoop on turning that “no” into a “yes.

Check Your Credit Report and Score

You face hurdles with bad credit, but checking your report and score starts the fix. This step reveals issues blocking card approvals, like errors or low scores in the 300 to 850 range.

- Head to AnnualCreditReport.com for free copies of your credit reports from all three major bureaus: Experian, Equifax, and TransUnion; you get these weekly, no strings attached, to spot mistakes that drag down your score.

- Pull your credit score through CreditWise from Capital One, a tool that gives free access without dinging your score at all; it tracks changes in your report, like new debts, and even simulates how decisions, say paying off a loan, might boost your number.

- Understand that scores run from 300 to 850, so a low one signals bad credit to lenders like Citi® or Premier Bankcard®; fix this by reviewing reports for errors, then dispute them directly with the bureaus to lift your standing fast.

- Think of your credit report as a financial diary, full of payment history and debts; use CreditWise to mimic outcomes, like how adding an authorized user could help, or what happens if you apply for student cards with high APR, that annual percentage rate on balances.

- Spot old addresses or wrong income details that scream instability to card issuers; correct these on your reports from Experian or others, and watch your approval odds climb, especially for options like the Perpay™ Credit Card aimed at rebuilders.

- Chatting with a friend like Madison Hoehn, who shares her tale of finding report glitches; she disputed errors via TransUnion, saw her score jump, and snagged a card despite past slips, proving this step packs real power for folks in your shoes.

Fix Errors on Your Credit Report

Bad credit can feel like a heavy backpack, weighing you down when you apply for new cards. Fix those errors on your credit report, and watch your approval odds soar, maybe even snagging a lower apr down the line.

- Pull your free credit reports from all three major bureaus, Equifax, TransUnion, and Experian, because some lenders only report to one or two, so you catch every mistake across the board.

- Spot common slip-ups like wrong personal info, old debts marked as new, or accounts that aren’t yours, and identifying these mistakes can potentially uplift your credit scores and boost your approval chances for that shiny new credit card.

- File a dispute online or by mail with each bureau that shows the error, include proof like bills or statements, and hey, disputing incorrect information can result in an improved credit score, turning your frown upside down.

- Wait for the bureaus to investigate, they usually take 30 days, and if they side with you, poof, the error vanishes, which fixes credit report errors and can improve approval chances for credit cards, like unlocking a secret door.

- Check back after the dispute to confirm changes, and if one bureau updates but another doesn’t, dispute again, since corrections should be made across all relevant bureaus to keep your score consistent and strong.

- Think of it as cleaning house before a big party, fixing those errors polishes your credit and could lead to better terms, like a reduced apr on future cards, making lenders see you in a whole new light.

Show Proof of Stable Income and Housing

Lenders value steady employment and a fixed address. These traits signal reliability to them. You might need to submit proof of income during the application process. Think pay stubs or tax returns; they work well.

Stable residency matters too, so gather utility bills or a lease agreement. This documentation verifies your housing stability.

Got a reliable job? It proves you can handle new credit wisely, even with higher APR rates on cards for bad credit. Share these details upfront. They boost your approval odds a lot.

Lenders seeing you as a safe bet, like a steady ship in rough waters. Just pull together those papers, and watch doors open.

Pay Down Existing Debt

Pay down your existing debt to boost your chances of credit card approval. You improve the debt-to-income ratio by reducing credit card balances and revolving debt. This shows lenders you handle money well.

Think it like lightening a heavy backpack; suddenly, you move faster toward your goals. Lower balances lead to a better credit utilization ratio, too. That simple step demonstrates financial responsibility to potential lenders.

Reducing outstanding debt directly influences your approval odds for new credit cards. Lenders see you as less risky when you tackle those balances. Keep an eye on apr, or annual percentage rate, as paying down debt cuts interest costs over time.

I get it, debt feels like a mountain sometimes, but chipping away builds momentum. You gain control, and approvals follow.

Explore Prequalification Offers

You want a credit card, but bad credit makes you nervous about applying. Many issuers let you check prequalification status. This step does not hurt your credit score. It helps you make smart choices.

Think of it like testing the water before you jump in. Aspire, Fortiva, and Reflex Platinum Mastercard provide this option. They keep your score safe. Perpay’s approval check works the same way, with zero impact on your score.

These offers show if you meet basic rules. You focus on cards that might say yes. Skip the ones that lead to hard inquiries, which can ding your score more.

Prequalification acts as your secret weapon. It avoids rejection surprises. Cards like these often come with details on apr, or annual percentage rate, so you know costs upfront. Talking with a friend who gives you the inside scoop.

You apply with confidence. Lenders see your effort. This builds a path to better credit. Grab those offers online or by phone. Start small, and watch approvals roll in.

Research Credit Card Options for Bad Credit

Start your search for credit cards by focusing on those that fit bad credit scores. Pick options that report to major credit bureaus, like Equifax or TransUnion, to help rebuild your history.

Grab online comparison tools to check annual fees, interest rates, and apr details side by side. These tools make it easy, almost like shopping for the best deal at a flea market, and they boost your odds of approval.

Dig into cards that match your credit level, such as the Capital One Platinum Secured Credit Card, which lets you check approval status in seconds. Compare reporting policies to see how they track your payments.

This step feels like detective work, but it pays off with smarter choices and fewer rejections.

Additional Tips for Approval

You know, sometimes the path to approval feels like climbing a hill with a backpack full of rocks, but a few smart moves can lighten that load and get you there faster. Team up with a trusted pal on their account, or hunt for options that grow with you, like a seedling turning into a sturdy tree—stick around to uncover these gems and boost your chances.

Consider Becoming an Authorized User

Struggling with bad credit feels like climbing a steep hill, but here’s a smart shortcut. Become an authorized user on a family member’s or trusted friend’s credit card account with good credit.

This boosts your credit score without you even needing to use the card. You gain from the primary cardholder’s positive payment history, and issuers add no credit check for you. Folks with no or poor credit find this builds their history fast, like borrowing a ladder to reach higher ground.

Your credit report getting a free upgrade, all while avoiding high apr charges on your own. Family or friends with solid accounts let you ride their good habits. They stay in charge, and you reap the rewards.

This path opens doors if solo applications fail, giving your score a gentle push upward.

Look for Cards with an Upgrade Path

Pick a credit card that offers an upgrade path, like shifting from a secured option to an unsecured one after you handle your account well over time. This move feels like leveling up in a game, where your good habits unlock better perks without starting over.

Cards with these paths let you keep your account history intact, so you move to options with stronger benefits, such as lower APR or higher limits, all without a fresh application.

Take the Capital One Platinum Secured Credit Card, for example; it gives automatic checks for a bigger credit line in as little as six months, and you won’t need extra cash deposits.

The Discover it Secured Credit Card runs automatic reviews for upgrades after seven months, making the process smooth and rewarding. With a friend who says, Stick with this, and soon you’ll ditch the security deposit for real freedom.” These upgrades build your credit story steadily, turning a basic card into something more powerful.

Apply for a Store Credit Card

Store credit cards offer a smart path for folks with bad credit. They prove easier to snag than regular cards, and you can grab one from places like department stores or big retailers.

You walk into your favorite shop, apply right there, and bam, approval might come quick if you show steady shopping habits. These cards come with lower credit limits, sure, but they pack higher APRs, so watch those interest charges like a hawk.

Use them wisely, pay on time, and they add glowing payment history to your credit report.

Folks rebuild credit this way all the time, turning a simple store card into a stepping stone. Say you charge a small purchase, pay it off monthly, and voila, your score starts climbing.

They help establish fresh credit habits too, especially when other doors slam shut. Keep balances low to dodge that high APR bite, and soon enough, better options appear on the horizon.

Best Credit Cards for Bad Credit

If bad credit feels like a heavy backpack slowing you down, these top picks act as your trusty sidekick to lighten the load and boost your score over time.You grab a secured card with low fees and rewards, turning everyday buys into steps up the credit ladder, so keep reading for the details that fit your wallet.

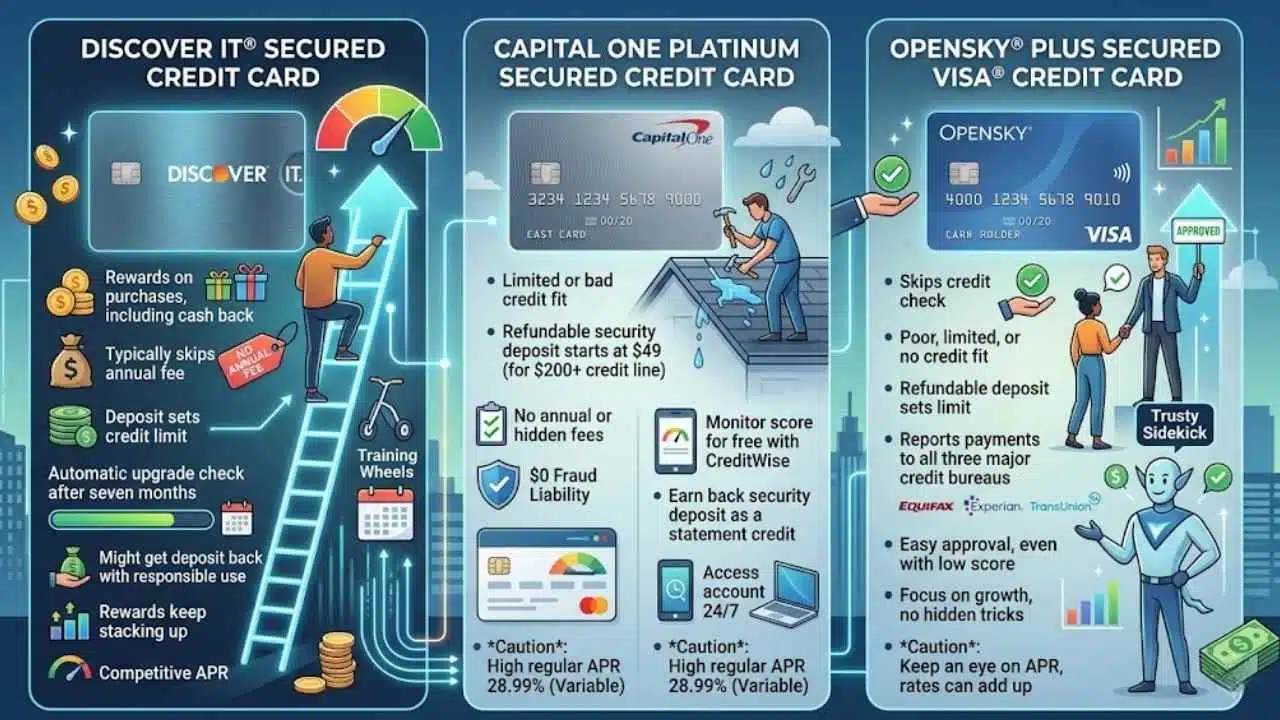

Discover it® Secured Credit Card

Discover it Secured Credit Card shines for folks rebuilding their credit. This card offers rewards on purchases, like cash back, which feels like a nice pat on the back when you’re starting over.

It typically skips the annual fee, so you keep more money in your pocket. Folks with poor, limited, or no credit find it a solid fit. You put down a deposit that sets your credit limit, acting like training wheels for better habits.

The card checks your account automatically after seven months for a possible upgrade to unsecured status. That means you might get your deposit back if you play your cards right. Rewards keep stacking up, and the APR stays competitive for a secured option.

Think of it as a ladder out of the credit pit, one responsible payment at a time. Many call it a top pick for building credit from scratch.

Capital One Platinum Secured Credit Card

Capital One Platinum Secured Credit Card suits people with limited or bad credit. You put down a refundable security deposit that starts at $49. This gives you at least a $200 credit line.

Rebuilding your credit like fixing a leaky roof, one solid payment at a time. The card has no annual or hidden fees, which keeps things simple and stress-free. It offers $0 Fraud Liability for unauthorized charges, so you stay protected if something goes wrong.

Monitor your credit score for free with CreditWise from Capital One. Earn back your security deposit as a statement credit through responsible use and timely payments. Access your account 24/7 via online banking and the mobile app.

The regular APR stands at 28.99% (Variable), so watch those interest rates. Think of it as a trusty sidekick in your credit journey, helping you climb back up without extra baggage.

OpenSky® Plus Secured Visa® Credit Card

OpenSky® Plus Secured Visa® Credit Card fits folks with poor, limited, or no credit like a glove. You put down a refundable security deposit, which sets your credit limit. This card skips the credit check, so approval comes easy, even if your score sits low.

It reports payments to all three major credit bureaus, helping you build that credit history step by step.

Think of this card as your trusty sidekick in the credit rebuild game. Cardholders love how it focuses on growth, with no hidden tricks. Keep an eye on that APR, though, as rates can add up if you carry a balance.

Approval feels accessible, and it opens doors for better options down the road.

Benefits of Using a Credit Card to Rebuild Credit

You can turn your credit story around with a card that builds solid payment records, cuts down on how much credit you use, and opens up chances for bigger limits over time, like a phoenix rising from the ashes.

Eager for tips on the best cards? Keep scrolling!

Helps Build Payment History

Payment history makes up 35% of your FICO score, so it packs a big punch in rebuilding credit. Pay your credit card bills on time, and you add positive marks to your credit reports.

Think of it like watering a plant; consistent care helps it grow strong. Set up reminders or automatic payments to stay on track, even if life gets busy. This habit boosts your score and keeps high APR from biting harder with late fees.

Consistently paying on time contributes 35% to your credit score, turning small wins into major progress. Imagine chatting with a friend who says, I nailed my bills this month,” and you reply, “Me too, it’s paying off.” On-time payments account for 35% of that FICO boost, so grab this chance with a credit card.

Tools like auto-pay apps make it simple, helping you avoid slips while managing APR costs.

Lower Credit Utilization Ratio

Lower credit utilization boosts your FICO Score, since it makes up 30% of that total. Lenders see it as a sign of smart money habits, like handling cash without going overboard. Think of it as keeping your plate light at a buffet, you avoid the heavy regret later.

Keep your balance under 30% of your credit limit, say $150 on a $500 card, and watch your score climb.

Pay your balance in full each month to dodge interest from the apr, or annual percentage rate. This habit cuts debt fast and shows lenders you’re on top of things. Folks who do this often get credit limit hikes, which drops utilization even more.

Your card as a trusty sidekick, helping you rebuild without the drama of extra fees.

Access to Potential Credit Limit Increases

Credit cards can boost your limit over time, and that feels like a win when you’re rebuilding. Take Capital One, for example. They check you for a higher credit line in as little as 6 months, no extra deposit needed.

Perpay does it even faster, in just 3 months with good habits. PREMIER Bankcard waits 12 months, but rewards steady payments. Some cards let you earn back your security deposit too, or unlock bigger limits.

Your card growing with you, like a plant that thrives on care.

This access helps in real ways, folks. Higher limits mean better credit use ratios, which can lead to lower apr over time. You pay on time, and the card company notices. It’s like training a pet; consistent effort brings rewards.

Cards from these issuers make it simple to climb up. Stick with responsible use, and watch those increases roll in.

Final Thoughts

You’ve learned how to check your credit report, fix errors, and pick secured cards that match your needs, like those from Capital One or Discover. These steps feel simple, right, because they build habits that boost your score without much hassle.

So, why not grab your free report from AnnualCreditReport.com today and start applying? With on-time payments and low utilization under 30 percent, you’ll rebuild your history fast and unlock better rates.

Take that first step now; your future self will thank you for turning bad credit into a comeback story.

Frequently Asked Questions (FAQs) About Credit Cards for Bad Credit

1. I’ve got bad credit, can I still snag a credit card approval?

You bet, start by applying for secured cards, they often work like a charm when your score’s in the dumps. Just put down a deposit, and you’re building credit faster than you think. Watch that apr (annual percentage rate) though, it can bite if you’re not careful.

2. What’s the deal with apr (annual percentage rate) on cards for folks with bad credit?

It’s the interest you’ll pay on balances, and with bad credit, it often skyrockets like a rocket. Shop around to find lower ones.

3. How do I boost my odds of getting approved, even with lousy credit?

Pay bills on time, it’s like giving your credit score a high-five. Cut down on debt, and consider a co-signer, that can open doors. Don’t forget to check the apr (annual percentage rate) before you commit, nobody likes nasty surprises.

4. Are there tricks to avoid high fees when applying with bad credit?

Go for cards with no annual fees first, they’re like hidden gems. Read the fine print on apr (annual percentage rate) to dodge extra costs.