Imagine living in a bustling town in Africa or South Asia, where you run a small shop but can’t get a loan from a bank. You feel stuck, right? Bills pile up, and growth seems out of reach for folks in emerging markets.

This hits hard for millions in the informal economy, where traditional financial services often ignore underserved groups. It’s like trying to climb a ladder with missing rungs, frustrating and unfair.

Over 1 billion people lack access to basic financial services, especially in places like Latin America and Indonesia. But fintech steps in with digital payments and mobile-first solutions to boost financial inclusion.

This blog explores how innovations like Nubank and Alipay drive economic growth through digital transformation. You’ll learn about expanding access for MSMEs and tackling challenges like regulatory frameworks.

Stick around for the ride.

The Rise of Fintech in Emerging Markets

Picture fintech bursting onto the scene in places like Kazakhstan and Mexico, much like a sudden storm that waters dry lands, sparking access to banking for folks who never had it.

Smartphone growth, paired with tools like WeChat Pay and digital money systems, drives this change, pulling in groups long ignored by old banks.

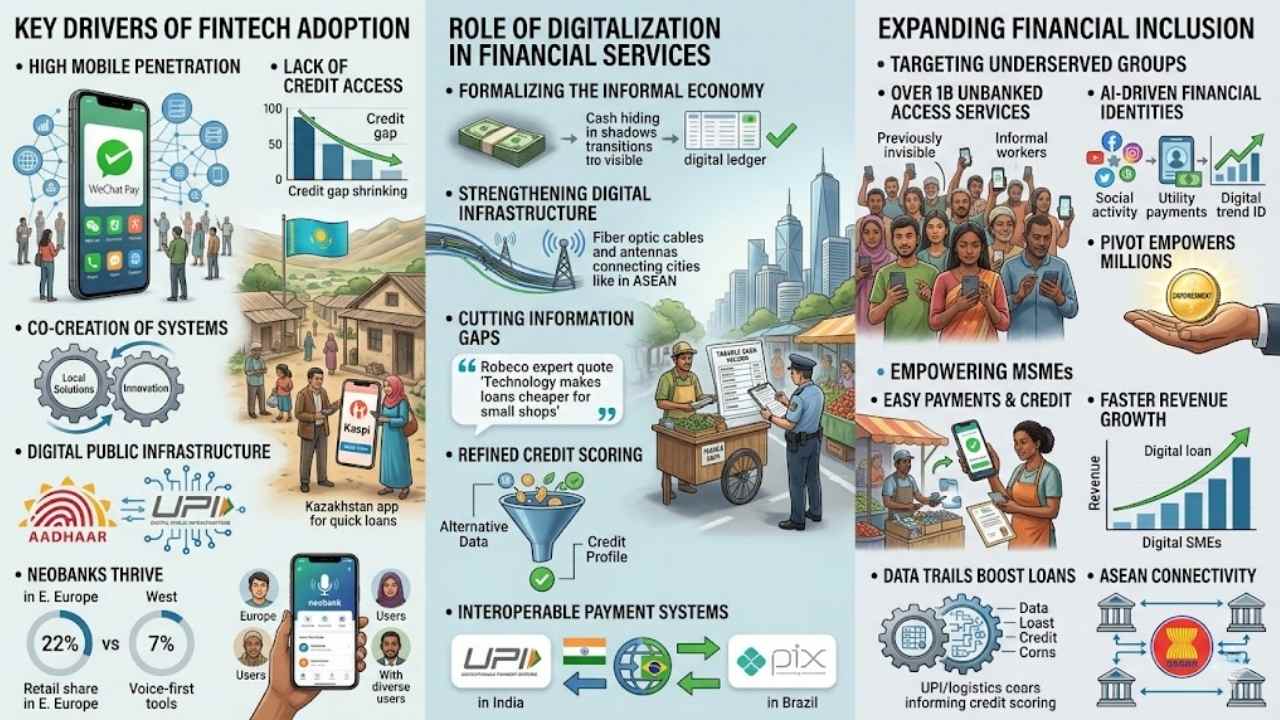

Key drivers of fintech adoption

High mobile penetration fuels fintech growth in emerging markets. People grab smartphones, yet they lack credit access. This mix sparks rapid digital tech adoption. Think of it as a spark igniting a fire, folks in places like China and Mexico jump on board.

The World Bank noted this trend back in January 2019 with their “Global Economic Prospects: Darkening Skies” report. Emerging economies co-create financial systems, not just borrow ideas.

They build digital public infrastructure, like India’s Aadhaar system, to bridge gaps. Smartphone adoption drives this, especially during the covid-19 pandemic. Digitalisation in financial services opens doors wide.

Intent to build inclusive systems breaks the biggest barriers, forget old limits like geography. AI-driven ecosystems fit mobile-first users perfectly. They scale up, stay accessible, and make real money.

Neobanks shine here, grabbing 22% retail market share in Eastern Europe versus just 7% in the West. These setups focus on underserved groups with multilingual, voice-first tools. Picture entrepreneurs in Kazakhstan using apps like Kaspi for quick loans.

Emerging markets and developing economies lead with innovations in mobile payments and digital banking. They emphasize consumer protection amid regulation and supervision.

The role of digitalization in financial services

Digitalization changes financial services in emerging markets, like a quiet revolution sweeping through dusty street markets. It tackles the huge informal economy, where cash hides in shadows and deals slip under the radar.

This shift builds stronger digital infrastructure, key for growth in places like ASEAN countries. Think of it as turning invisible ink into bold print; suddenly, governments see taxable cash flows from once-hidden businesses.

The World Economic Forum highlights how this formalization boosts tax revenue, helping nations fund better roads and schools. Robeco experts, such as Nina Petry, point out that digital technology cuts information gaps, making loans cheaper for small shops.

Fintech firms use this data goldmine to refine credit scoring, especially for SMEs through platforms like online lending. Digital payment systems, take UPI in India or Pix in Brazil, stay open and interoperable, letting users pile on extras like credit or invoicing.

The Cambridge Centre for Alternative Finance notes how these tools create verifiable cash flow records from informal spots, improving financial sector oversight. Giulia Ajmone Marsan and Adelia Rahmawati discuss in reports how such innovation and technology empower micro enterprises, weaving them into the formal financial and monetary systems.

It’s like giving a street vendor a digital passport to the big leagues, enhancing productivity across the board.

Expanding Financial Inclusion

Fintech opens doors for folks in remote villages, who once struggled to get bank accounts, by letting them use simple mobile apps for daily transactions. Imagine a street vendor in Kenya growing her business with quick loans from digital platforms, that’s the real magic sparking hope across emerging markets.

Targeting underserved groups

Over a billion people lack access to basic financial services in emerging markets. These folks, often called the unbanked, have always handled money in their own ways. Traditional banks just overlooked them, like hidden gems in a crowded market.

Most live in places where formal banking falls short. Mobile-first solutions step in to fill that gap. They target underbanked groups and informal workers with ease.

Artificial intelligence shifts views on these people, turning “risky” labels into chances for the future of finance. It uses alternative data from daily digital habits to build new financial identities.

No more relying on old credit scores, which felt like outdated maps. This pivot empowers folks, making them key players in the financial ecosystem. Think of it as giving everyone a fair shot at the game, with tools that fit their lives.

Empowering micro, small, and medium enterprises (MSMEs)

Small and medium-sized enterprises, once ignored by big banks and markets, now grab new chances through tech advances. They get easy access to payments, logistics, and credit. Picture a street vendor in a bustling market suddenly handling deals with a quick app tap.

SMEs that embrace digital tools see faster revenue growth. These firms also earn more cash per worker than those stuck in old ways. Digital deals create rich data trails. This info sharpens credit scoring for better loans.

Banks use this smart scoring to offer more sme finance without big risks. Credit fuels growth in emerging spots, it lifts output like a rising tide. Take India’s UPI, it powers 75% of digital retail trades since 2016.

Open banking lets MSMEs link up fast. Tools like insurtech guard their risks, while wealthtech builds their savings. ASEAN regional payment connectivity ties markets together. The digital economy framework agreement smooths cross-border flows.

MSMEs thrive with these boosts, they dodge old hurdles.

Innovations Transforming Financial Services

![]()

Imagine your phone turning into a super-fast bank teller, zipping money across borders with apps like M-Pesa in Kenya, making cash feel old-school. Then picture quick loans popping up on screens for small shops in India through platforms like Lendingkart, or folks in Brazil trading digital coins on blockchain setups that skip the middleman and cut fees.

Mobile payment platforms

Mobile payment platforms are changing how people handle money in emerging markets. Take Brazil’s Pix, for example. The central bank launched it as a fast digital payment system. It now boasts 168 million daily users after just three years.

That’s a huge chunk of Brazil’s 220 million people. Folks send cash with a quick tap on their phones. No need for old-school banks. India’s Unified Payments Interface, or UPI, started in 2016.

It lets users transfer funds through mobile devices. Today, it handles 75% of the nation’s digital retail deals. Imagine: you’re at a street market, and zap, payment done in seconds.

Platforms like M-Pesa in South Africa, Dana in Indonesia, and PicPay in Brazil make life easier too. They allow transactions right from your phone, skipping traditional accounts. In Brazil, apps blend Pix with artificial intelligence and messaging tools.

This speeds up buys for everyone. Think of it as a digital wallet that fits in your pocket, offering e-disc perks on the go. Small vendors thrive with these, reaching more customers without hefty fees.

It’s like giving money wings to fly across borders, safely and swiftly.

Digital lending solutions

Fintech firms tap alternative data and AI to check credit scores. They boost loan access for folks and small shops via online lending. Imagine: a street vendor in a bustling market gets quick cash without piles of paperwork.

Nubank, a no-branch bank in Brazil, shakes up old credit rules. It opens doors for millions who banks ignored before.

MoniePoint in Nigeria backs small businesses with smart tools. Their models prove inclusion pays off and lasts. India’s Aadhaar system uses fingerprints to speed up accounts for the unbanked.

Folks now grab loans they never dreamed of, like finding hidden treasure in their pockets. These tweaks fuel dreams and spark growth in tough spots.

Blockchain and cryptocurrency adoption

Emerging markets skip old payment steps. They jump from cash straight to mobile apps. Take Kazakhstan’s Kaspi, for example. It shows how folks ditch credit cards for quick online transfers.

China’s Alipay and WeChat Pay lead this charge too. These tools make money move fast, like a shortcut in a busy city. Public-private partnerships build bridges here. They create systems that work across borders, smooth as silk.

Digital setups like UPI in India and Pix in Brazil open doors wide. They link up easily with blockchain tech. This sparks cryptocurrency use in daily life. AI systems fit mobile users perfectly.

They scale up, stay cheap, and make real money. The UAE shines as a hotspot for this innovation. Leaders at the Centre for Financial and Monetary Systems gather to boost sustainability and resilience.

Cryptos add strength, like hidden armor in tough times.

The Impact on Economic Growth

Fintech sparks faster business growth in emerging markets, like a farmer in Kenya using mobile loans to buy better seeds and double his crop yield. This tech builds stronger economies too, helping families weather tough times with quick access to savings apps during floods or job losses.

Boosting productivity

Informal businesses in emerging markets produce just 25% of the output per worker that formal ones do. This gap drags down productivity and stalls growth, like a car stuck in mud. Digitalization steps in to fix that mess.

It tackles challenges from the informal sector and sparks real improvements in the business world. Picture a small shop owner switching to digital tools; suddenly, tasks speed up and efficiency soars.

This shift to digital ways lets emerging markets ramp up productivity fast. They even leap ahead of developed nations in some spots. The spread of digitalization keeps reshaping the business scene for the better.

Take mobile banking apps as an example; they cut paperwork and free up time for real work. Entrepreneurs gain tools like quick loans through fintech platforms, turning ideas into action without endless waits.

Enhancing financial resilience

Fintech opens doors to savings accounts and insurance for folks in emerging markets. People build stronger buffers against tough times this way. Households weather economic storms better with these tools at hand.

Businesses stay afloat during shocks, too. Picture a small shop owner in Kenya using a mobile app to stash cash for rainy days; it keeps dreams alive.

Access grows, and so do credit ratings for countries and companies over time. The gap in bond yields shrank after Covid ended, showing real progress. Folks smooth out spending with wealth services, easing policy moves for central banks.

Think of it as a safety net that catches everyone, turning vulnerability into strength.

Challenges and Risks

Fintech firms in emerging markets face tough rules that slow down their growth, like strict laws on data privacy that make operations tricky. Cyber threats loom large too, with hackers eyeing weak spots in mobile apps, so companies must beef up their defenses to keep users safe and build trust.

Regulatory hurdles

Governments play a big role in fintech growth. They push for better financial know-how among people. Think of it like a coach guiding a team to play fair and smart. Regulatory bodies focus on keeping consumers safe and ensuring loans stay responsible.

This setup helps fintech companies build trust, even in tricky spots. The UAE stands out with its welcoming vibe for new financial tools. Its mix of people from everywhere fuels this progress.

Progressive rules, such as those for stored value facilities and retail payment services, make it easier for fintech to thrive. These regulations act like guardrails on a winding road, keeping things steady without slowing down innovation.

The Digital Cooperation Organization backs digital shifts in its member nations. It fosters teamwork to tackle regulatory bumps. Picture countries linking arms to jump over hurdles together.

Such groups help smooth out differences in laws across borders. They promote safe cyber practices too, vital for fintech’s future. Still, challenges pop up with varying rules in emerging spots.

Firms must adapt to local demands while eyeing global standards. Partnerships with regulators can turn potential roadblocks into stepping stones for growth.

Addressing cybersecurity concerns

Fintech brings amazing perks to emerging markets, but those digital literacy gaps sure amp up risks like fraud and scams in financial services. Imagine, you’re swiping on your phone for a quick loan, and bam, a sneaky scam slips through because not everyone knows the red flags.

Advancements zoom ahead, yet if they outpace boosts in digital literacy and public trust, folks in certain groups stay left out or face exploitation. We feel that pinch, right? AI steps in to read those tricky human behaviors and spot financial moves that old systems miss, but it drags in fresh risks too.

Those AI-powered setups for mobile users scale up fast, stay easy to use, and make solid business sense, yet data security screams for attention. Fintech cuts costs on transactions, pumps up small business growth, and builds economic strength, but strong cybersecurity keeps it all safe.

AI lets people build their financial profiles with every deal, which sparks worries over privacy and data protection. This shift in finance hits both the big structures and our everyday lives, so secure systems become the real hero here.

The Future of Fintech in Emerging Markets

Imagine AI spotting fraud in seconds, while machine learning tailors loans to fit everyday folks in bustling villages. Partnerships between banks and startups will spark fresh ideas, teaming up to build secure apps that connect farmers to global markets, so keep reading to see how these changes unfold.

AI and machine learning in financial services

AI drives big changes in finance across places like Brazil and Nigeria. Entrepreneurs in bustling spots, you know, Lagos, Jakarta, Cairo, and Dubai, lead this shift with smart tech.

They use it to skip old banking setups, like jumping over a rusty fence to reach fresh ground. This redefines who gets access to money matters, pulling in folks left out before.

Astra Tech shows how this works through its app, Botim. It boasts over 150 million users who chat and connect daily. Picture sending money home, and bam, a quick loan offer pops up in the talk.

Or listen to voice notes in your local dialect, and AI dishes out savings advice, like a wise friend whispering tips. These tools make finance feel personal, almost like a chat over coffee.

Strengthening partnerships and collaborations

Public-private partnerships spark real change in fintech. They build interoperable systems that cross borders with ease. Leaders at the Centre for Financial and Monetary Systems gather often.

These folks tackle big shifts in global finance. Their focus hits sustainability, resilience, innovation, and digitalization spot on. The UAE steps up as a key spot for fresh ideas in money matters.

It draws in folks hungry for inclusion. The Digital Cooperation Organization backs digital shifts in its member lands. Picture it like a team huddle, where everyone shares plays to win big.

Fintech stars like Nubank shine bright in places such as Mexico. Spin by Oxxo joins the fun too. These outfits promise better access to cash for everyday people. Recent studies back this push for teamwork.

The World Bank’s “Global Economic Prospects: Darkening Skies” lays out the scene. Folks at the Bank for International Settlements explore “Digital Payments, Informality and Economic Growth.” The Center for Financial Inclusion chimes in with “Small Firms, Big Impact.” All point to joint efforts driving fintech forward.

Final Words

Fintech sparks big changes in emerging markets, from mobile payments like India’s UPI to digital lending that boosts small businesses. These tools make finance simple and fast, cutting out old hurdles for folks without bank accounts.

Imagine turning your phone into a powerhouse wallet, empowering millions to join the economy. What if you explored Nubank’s model in Brazil to see real growth in action? Examine reports on blockchain for more insights, or check partnerships driving AI in finance.

Grab this wave, folks, and watch emerging economies soar to new heights.

FAQs

1. What exactly is fintech, and how is it shaking up emerging market economies?

Fintech, you know, those clever tech tools for finance, is like a fresh breeze in places like Kenya and India, opening doors to banking for folks who never had it before. It boosts money flow, cuts costs, and sparks growth where it matters most. Picture your grandma in a remote village sending cash via her phone, that’s the magic happening right now.

2. How does fintech help everyday people in developing countries?

Fintech steps in like a trusty sidekick, offering mobile wallets and quick loans to folks skipped by big banks. It builds financial inclusion, turning dreams into reality for small business owners.

3. Are there any bumps in the road for fintech in emerging markets?

Oh, sure, regulations can feel like navigating a maze blindfolded in spots with spotty internet. Yet, with smart tweaks, it overcomes hurdles like cyber threats and builds trust. All in all, it’s a game-changer worth the effort.

4. Can fintech really speed up economic growth in these areas?

Absolutely, by streamlining payments and credit, fintech fuels jobs and innovation across emerging economies.