The American financial landscape crossed a historic threshold yesterday, April 1, 2026, as the first compliance deadlines for the Consumer Financial Protection Bureau’s (CFPB) “Open Banking” rule officially took effect for the nation’s largest financial institutions. This regulation, rooted in Section 1033 of the Dodd-Frank Act, represents the most significant shift in consumer financial power in a generation. By mandating that banks provide a secure, standardized way for customers to share their own data with third-party apps, the bureau is attempting to end the era of “financial lock-in.” The Impact of Open Banking on US Consumers is already being felt as the first wave of “Pay-by-Bank” services and instant loan switching tools hit the market this week.

How We Selected Our 7 Best Impact of Open Banking on US Consumers Facts

To build this 2026 framework, we analyzed the final Section 1033 rule text alongside the April 2026 compliance reports from the “Tier 1” banks (those with over $250 billion in assets). Our selection criteria prioritized the “Day One” shifts that directly affect a user’s ability to switch accounts and lower their borrowing costs. We also examined the 2026 “standard-setting” updates that have replaced old-fashioned screen scraping with modern APIs. These 7 points were chosen to provide a 360-degree view of how the CFPB’s new rules are transforming the American wallet from a closed system into a portable, competitive asset.

7 Essential Truths About the Impact of Open Banking on US Consumers

The following insights break down the technical, fiscal, and behavioral nuances of the U.S. financial landscape under the new 2026 rules.

1. The “Number Portability” for Bank Accounts

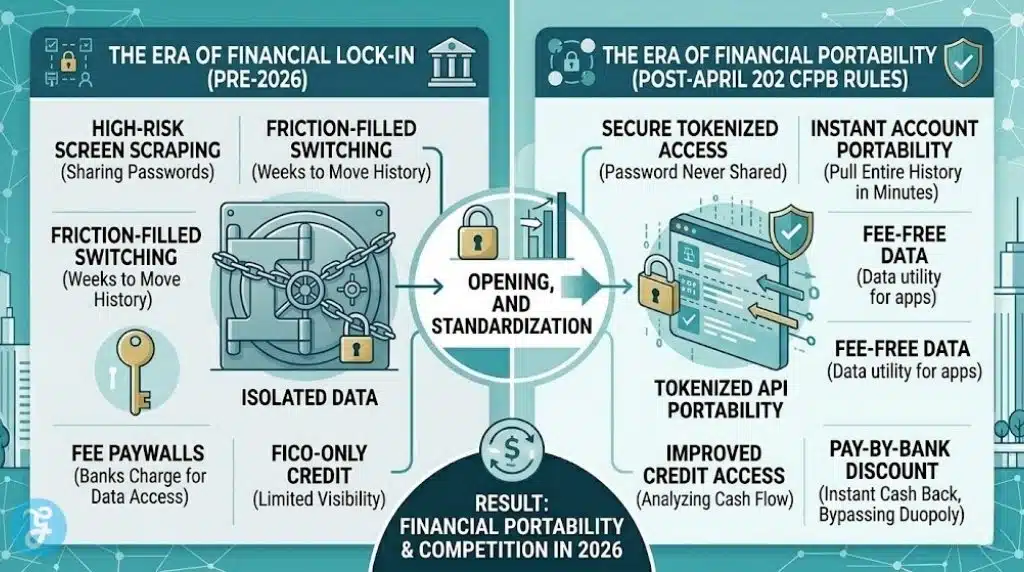

The most visible effect of the 2026 rule is that bank accounts have become “portable,” similar to how mobile phone numbers were freed up in the early 2000s. Under the new rules, your transaction history, bill-pay settings, and direct deposit details are no longer “trapped” at your original bank. You can now authorize a new bank to “pull” your entire history instantly, making it possible to switch to a higher-interest savings account in minutes rather than weeks.

Best for: consumers stuck in “Big Bank” accounts with near-zero interest rates.

Why We Chose It:

-

It removes the single biggest friction point that prevented Americans from switching banks.

-

It forces banks to compete on rates rather than relying on customer inertia.

Things to consider:

-

While the data moves instantly, some manual verification of complex recurring bills may still be required.

2. The End of “Screen Scraping” Risks

Prior to April 2026, most budgeting apps used “screen scraping,” a process where you gave the app your actual bank password. The new CFPB rules have effectively killed this practice for large institutions. Instead, banks must now provide a “Developer Interface” (API) that allows apps to access your data without ever seeing your login credentials. This move significantly reduces the risk of massive data breaches and identity theft.

Best for: privacy-conscious users of apps like Rocket Money, YNAB, or Mint successors.

Why We Chose It:

- It elevates the security baseline for the entire American fintech ecosystem.

- It eliminates the “cat and mouse” game where banks would block apps to “protect” data.

Things to consider:

-

You will now see a standardized “Authorization Disclosure” screen whenever you connect a new app.

3. Mandatory “Fee-Free” Data Access

A critical “Day One” win for the 2026 cycle is the total ban on data access fees. The CFPB has ruled that banks cannot charge you—or the apps you use—to access your own financial information. This prevents “Big Banks” from creating a paywall around your transaction history, ensuring that open banking remains a free public utility for every account holder.

Best for: users of free budgeting, credit-building, and savings-automation apps.

Why We Chose It:

-

It ensures that low-income consumers aren’t priced out of financial optimization tools.

-

It stops banks from “taxing” innovation in the fintech sector.

Things to consider:

-

Banks are still pushing for “reasonable infrastructure fees” in the 2026 legislative reform cycle.

4. The One-Year “Authorization Sunset”

To prevent “zombie” apps from tracking your spending forever, the 2026 rules introduce a mandatory one-year sunset. Any third-party app you authorize will lose access to your bank data exactly one year after you sign up, unless you explicitly re-authorize it. This forces a yearly “digital spring cleaning” of who has access to your financial life.

Best for: people who frequently try out new apps and then forget to delete their accounts.

Why We Chose It:

-

It provides a built-in privacy guardrail that doesn’t require user maintenance.

-

It ensures that data collection remains “reasonably necessary” for the service provided.

Things to consider:

-

You will likely receive a flurry of “Re-authorize your app” emails every 12 months.

5. “Pay-by-Bank” as a Credit Card Alternative

Open banking has cleared the way for “Pay-by-Bank” at major retailers. Because third-party apps can now securely initiate payments directly from your checking account with your permission, you can bypass the 3% credit card processing fees. In 2026, many merchants are offering “instant 2% discounts” if you pay via a secure open-banking link instead of a Visa or Mastercard.

Best for: debit-card-heavy shoppers looking for the same “rewards” or discounts as credit users.

Why We Chose It:

-

It creates the first real competition for the “credit card duopoly” in decades.

-

It provides immediate cash-back-style savings at the point of sale.

Things to consider:

-

Pay-by-bank transactions do not typically offer the same “chargeback” protections as credit cards.

6. Improved Credit Access for “Thin File” Borrowers

The 2026 rules have fundamentally changed how lenders evaluate risk. Instead of relying solely on a FICO score, lenders can now (with your permission) analyze your actual cash flow and rent payment history via open banking. This has enabled millions of “thin file” consumers—particularly young people and immigrants—to qualify for competitive loans based on their real-world habits.

Best for: young adults, immigrants, and those with limited traditional credit history.

Why We Chose It:

-

It makes the credit market more meritocratic and inclusive.

-

It uses “ground truth” data (income/expenses) rather than opaque credit algorithms.

Things to consider:

-

Lenders will have a much more granular view of your spending habits, including “discretionary” leaks.

7. The 2026 “Reform” Uncertainty

While the large-bank deadline has passed, the “Section 1033” landscape is currently in a state of political flux. As of mid-2026, new leadership at the CFPB and in Congress is proposing “refinements” to the rule. These potential changes include allowing banks to charge fees for “premium” data and redefining which small banks are exempt, meaning the “final” shape of open banking is still being negotiated.

Best for: strategic planners and fintech founders watching the regulatory horizon.

Why We Chose It:

-

It acknowledges that the current April 1 rules are a “First Wave,” not the final destination.

-

It highlights the ongoing tension between consumer rights and bank infrastructure costs.

Things to consider:

-

Small banks (under $850 million in assets) are currently exempt until at least 2030.

Strategic Summary of the Open Banking Transition

The Impact of Open Banking on US Consumers is a shift from “Financial Feudalism” to “Financial Portability.” By April 2026, the biggest hurdles to leaving a bad bank—the loss of data and the risk of screen scraping—have been legally dismantled for the top-tier institutions. While the political climate in Washington suggests that “Section 1033” will see further revisions this year, the core principle remains: your data belongs to you, not the bank. To succeed in this new era, consumers must move from being “account holders” to “data owners,” proactively using secure APIs to hunt for the best interest rates and lowest loan costs in a newly transparent market.

Visualizing the Open Banking Shift: Security & Portability

The tables below provide a comparative look at how your financial interactions change before and after the 2026 compliance era.

2026 Financial Data Access Comparison

This data illustrates the structural security and cost differences between the “Old Way” and the new 2026 standard.

| Feature | Pre-2026 “Screen Scraping” | Post-April 2026 CFPB Rule | Optimization Goal |

| Credential Safety | High Risk (User shares password) | Secure (Tokenized API) | Never share your bank password |

| Data Access Fee | Hidden in bank terms | Mandatory $0 | Ensure apps are free to connect |

| Data Recency | Intermittent (Refresh delays) | Real-Time (99.5% uptime) | Use for “Pay-by-Bank” timing |

| Access Duration | Indefinite until disconnected | 1-Year Sunset | Review app list every April |

| Portability | Hard (Manual history download) | Easy (Digital transfer) | Switch banks for better rates |

Our Top 3 Picks and Why?

-

The End of Screen Scraping: This is our top pick because it fixes a massive security hole in the American internet. Moving to tokenized APIs is the single biggest upgrade to financial privacy in the last 20 years.

-

Bank Account Portability: We chose this because it is the “Big Stick” for consumers. The ability to move your entire financial life to a competitor in minutes is the only thing that will truly force big banks to raise their interest rates.

-

Pay-by-Bank Discounts: This is an essential pick because it puts cash back in your pocket immediately. In an inflationary 2026, a 2% “direct-pay” discount at the grocery store or gas station adds up to thousands of dollars in annual savings.

Investor’s Framework: How to Optimize Your Financial Data?

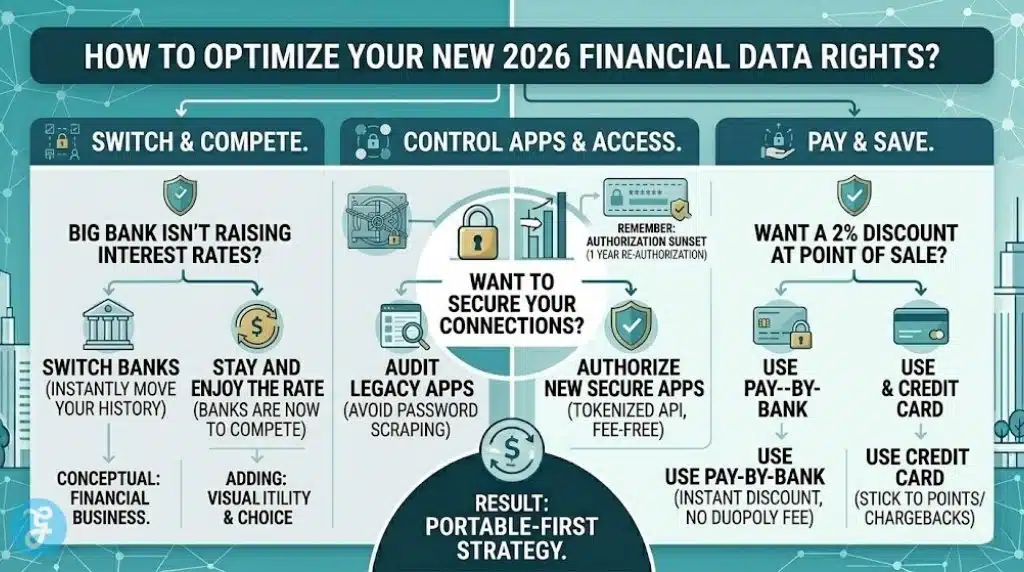

Optimizing your 2026 banking experience requires a “Portable-First” strategy. Do not let your data sit idle in a low-yield account.

The Selection Framework

-

Audit Your Connections: Log into your primary bank’s “Security” dashboard. Under the new 2026 rules, they must provide a single screen showing every app currently accessing your data.

-

Test “Pay-by-Bank”: Look for “Instant Transfer” or “Pay-by-Bank” options at major retailers. If they offer a discount for bypassing credit cards, use it for large purchases to maximize the margin.

-

Request a “Portability Quote”: If you are applying for a loan, ask the lender if they support “Section 1033 data sharing.” If they do, provide your 12-month history via API to potentially lower your APR.

-

Monitor the “Sunset”: Mark your calendar for one year from today. Your apps will stop working unless you re-authorize them—be ready to “cull” the apps that didn’t provide enough value.

Use the decision matrix below to determine the best way to handle your data sharing in the current environment.

Decision Matrix

| If your priority is… | Choose X if… | Choose Y if… |

| Absolute Security | Only connect apps that use the new “CFPB Standard” API. | Avoid legacy apps that still ask for your bank password. |

| Highest Interest Rates | Switch Banks using the portability tools to a high-yield online bank. | Stay at Big Bank only if they match the competitive rate. |

| Lowering Borrowing Costs | Share 12-Month History to prove your cash flow to lenders. | Stick to FICO if your transaction history is “messy.” |

| Consumer Privacy | Let the “Sunset” occur for apps you don’t use daily. | Re-authorize only the core “financial health” tools. |

The Final Checklist: 5-Point Open Banking Readiness Plan

-

Log into your main bank account and locate the “Third-Party Access” portal mandated by the 1033 rule.

-

Verify that your budgeting app has transitioned from “Screen Scraping” to a “Secure API” connection.

-

Identify at least one recurring “Pay-by-Bank” opportunity (like a utility or rent) to avoid credit card surcharges.

-

Check if your “Tier 1” bank (if applicable) has met the April 1 compliance deadline; if not, you may have grounds for a CFPB complaint.

-

Set a recurring reminder to review your “Data Permissions” every 12 months to ensure your “Authorization Sunset” is working for you.

The Future of Finance: From Gatekeepers to Enablers

America’s open banking future is no longer a theoretical concept; as of April 2026, it is a regulated reality. The CFPB’s decision to mandate data portability has effectively turned every bank from a “gatekeeper” of your history into a “service provider” that must earn your business every day. While the 2026 “Reform” debates in Washington may shift the technical details, the era of bank-driven inertia is over. By treating your financial data as a portable asset and utilizing the new secure API infrastructure, you can reclaim the thousands of dollars previously lost to “lousy rates” and “opaque fees.” In 2026, the most powerful tool in your wallet isn’t your credit card—it’s your right to move your data.