Ireland’s healthcare landscape in 2026 is defined by a significant push toward universal care under Sláintecare, yet the structural gap between the Health Service Executive (HSE) and private medical insurance (PMI) remains a primary concern for residents. While the public budget has reached a record €29 billion, private premiums continue to rise as families seek to bypass systemic bottlenecks. Navigating the differences between public and private healthcare Ireland requires a clear understanding of how these two tracks operate independently and where they overlap. This guide highlights the six fundamental divergences that dictate the speed, cost, and quality of your medical journey this year.

Our Selection Methodology

To define these six critical differences, we reviewed the 2026 HSE National Service Plan, the Waiting Time Action Plan (WTAP) 2026, and the latest premium data from the Health Insurance Authority (HIA). We focused on the changes effective as of April 2026, including the new regionalized HSE Health Regions and the impact of recent 5.9% premium hikes across major insurers. Our selection prioritizes the practical “point-of-care” experience to ensure users can make informed financial decisions in the current economic climate.

6 Key Differences Between Public and Private Healthcare Ireland

Understanding these differences is essential for balancing your household budget against your long-term health requirements.

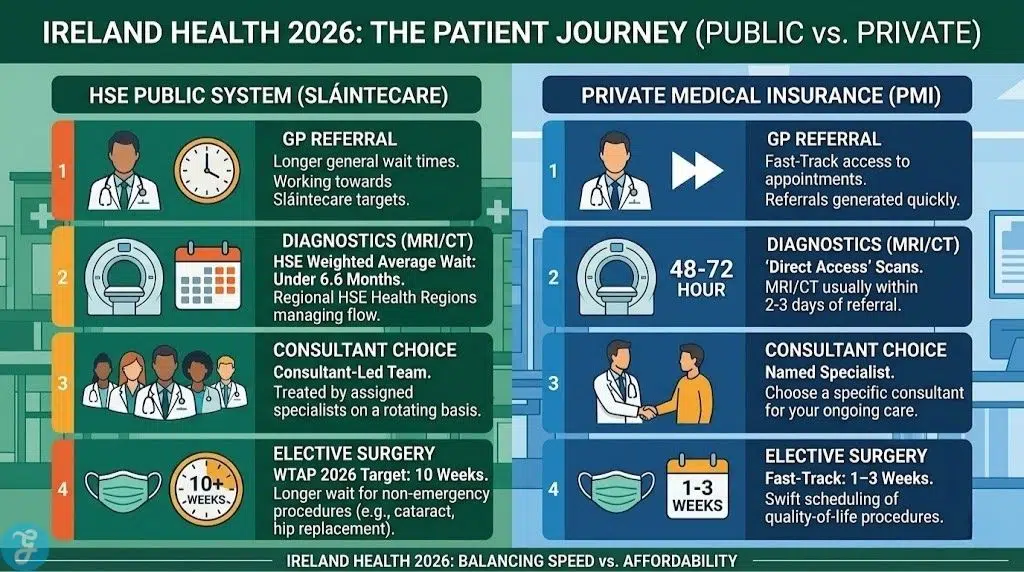

1. Access Speed: The Sláintecare Target vs. The Private Fast-Track

The most significant motivator for private insurance in 2026 remains the speed of elective care. While the HSE is aggressively working toward the Sláintecare targets, a gap in delivery still exists.

-

Best for: Individuals requiring “quality of life” procedures like hip replacements or cataract surgery.

-

Why We Chose It: The WTAP 2026 targets a 10-week wait for outpatients, but private insurance often secures these appointments in under 14 days.

-

Things to consider: For life-threatening emergencies, the HSE is the primary responder; private insurance is strictly for scheduled, elective care.

2. Consultant Choice: Clinical Teams vs. Named Specialists

Under the new Public-Only Consultant Contract (POCC), the way patients interact with senior doctors is shifting.

-

Best for: Patients who prefer a long-term, one-on-one relationship with a specific surgeon or specialist.

-

Why We Chose It: Public patients are treated by a “Consultant-led team,” meaning you may see different doctors on each visit, whereas private patients choose their specific consultant by name.

-

Things to consider: The 2026 HSE model ensures more senior expertise is available 24/7 for public patients, narrowing the “experience gap” even if you don’t choose the name.

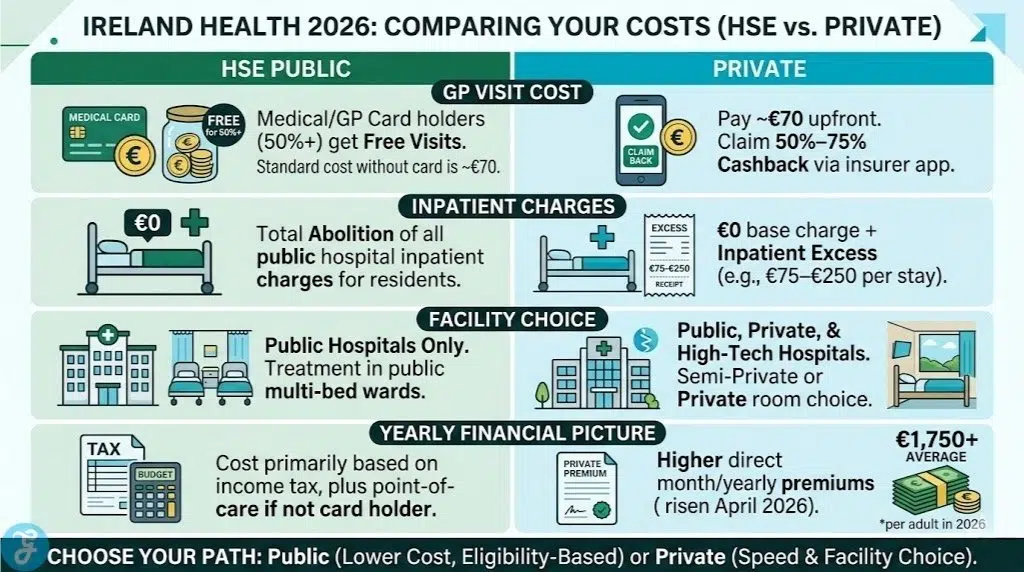

3. Inpatient Costs: €0 Public Abolition vs. The Private “Excess”

A major milestone for 2026 is the total abolition of all public inpatient charges for residents in Ireland.

-

Best for: Budget-conscious families who want to eliminate the financial risk of a long-term hospital stay.

-

Why We Chose It: Staying in a public hospital as a public patient now costs €0. In contrast, private patients often pay an “excess” (typically €75–€250) per stay.

-

Things to consider: While the public stay is free, you have no choice of room type and will likely be in a multi-bed ward.

4. Facilities: Public Wards vs. High-Tech Hospitals

The physical environment of care differs greatly, with private insurance offering access to exclusive “High-Tech” facilities.

-

Best for: Patients prioritizing privacy, comfort, and access to specific advanced surgical robotics.

-

Why We Chose It: Private insurance is the only gateway to hospitals like the Blackrock Clinic or the Beacon without paying massive out-of-pocket fees.

-

Things to consider: Public hospitals are the only locations equipped for major trauma and complex emergency neurosurgery in many regions.

5. Diagnostics: National Lists vs. Direct Access Scans

Getting an MRI or CT scan is often the “bottleneck” in a medical diagnosis, and the two systems handle this very differently.

-

Best for: Quick diagnosis of sports injuries or non-urgent persistent pains.

-

Why We Chose It: Most private plans in 2026 offer “Direct Access” to scan centers, where you can get an MRI within 48–72 hours of a GP referral.

-

Things to consider: The HSE has reduced its weighted average wait time for diagnostics to under 6.6 months, but it remains significantly slower than private alternatives.

6. Day-to-Day Benefits: Medical Cards vs. Insurance Cashback

The way you pay for your local GP or physiotherapist depends heavily on your eligibility status.

-

Best for: Working professionals who do not qualify for a Medical Card but visit the doctor frequently.

-

Why We Chose It: Over 50% of the population now has a Medical or GP Visit Card for free public GP care. Private insurance bridges the gap for others by offering 50%–75% cashback on everyday fees.

-

Things to consider: You must pay the GP upfront (€60–€75) and claim the money back through your insurer’s app.

2026 Comparative Summary

To help you decide which path is right for your household, we have summarized the current 2026 costs and service levels in the table below. Note that average private premiums have risen to approximately €1,750 per adult following the April 2026 price adjustments.

| Feature | HSE Public Patient (2026) | Private Health Insurance Member |

| Outpatient Wait Target | 10 Weeks (WTAP 2026) | 1–3 Weeks |

| Consultant Choice | No (Assigned Team) | Yes (Named Specialist) |

| Inpatient Charge | €0 (Abolished) | €0 + Inpatient Excess (€75-€250) |

| Hospital Type | Public Only | Public, Private, & High-Tech |

| GP Visit Cost | €0 (If Eligible) / €70 (Standard) | €70 (Upfront) – 75% Cashback |

The Healthcare Verdict: Choosing Your 2026 Path

The differences between public and private healthcare Ireland in 2026 reflect a system in transition. For many, the abolition of public hospital charges and the expansion of GP Visit Cards have made the HSE a more viable primary option than ever before. However, the private sector remains the only reliable way to secure “certainty of time” for elective procedures and diagnostics. As premiums continue to rise due to medical inflation, the decision often comes down to whether you are paying for the quality of the medicine—which is high in both sectors—or the quality of the convenience.