Navigating the legal landscape of digital assets in Aotearoa has become significantly more complex as of March 2026. With the Inland Revenue Department (IRD) and the Financial Markets Authority (FMA) tightening their oversight, staying compliant requires more than just basic record-keeping—it requires an understanding of the specific “triggers” that now define taxable events in the eyes of New Zealand authorities.

How We Selected Our 9 NZ Crypto Regulation Updates

To provide these insider tips, we analysed the February 2026 IRD issues paper (IRRUIP18) on DeFi, the March 2026 FMA Designation Notice regarding stablecoins, and the newly implemented CARF reporting requirements. Our selection prioritises the most recent 2026 legislative shifts that move crypto from a “grey zone” into a highly transparent, standardised financial reporting environment.

The 9 Most Critical NZ Crypto Regulation Updates for 2026

The following points break down the essential regulatory changes that every New Zealand-based trader and business must navigate this year.

1. The 1 April 2026 CARF Reporting Deadline

From 1 April 2026, New Zealand officially implements the OECD’s Crypto-Asset Reporting Framework (CARF). This means that New Zealand-based exchanges and service providers are now legally mandated to collect and report your transaction data directly to the IRD. The days of “invisible” trading are over, as this data is also shared with 48 other international jurisdictions.

Best for: Active traders using local exchanges who want to avoid automated IRD audits.

Why We Chose It:

-

It marks the biggest shift in NZ crypto transparency in a decade.

-

It turns “reporting” from a voluntary act into a systematic, automated process.

-

It ensures that offshore activity is eventually visible to the IRD through global data exchange.

Things to consider: The first reporting period ends in March 2027, but your data collection begins the moment the clock strikes midnight on 1 April 2026.

2. DeFi “Disposal” Triggers for Wrapping and Bridging

The IRD’s February 2026 guidance clarified a contentious point: wrapping tokens (e.g., ETH to wETH) or bridging assets to another chain is now considered a taxable disposal. If you transfer crypto to a smart contract or pool where you no longer hold the unique private key for those specific units, the IRD views this as a sale and a subsequent acquisition of a new asset.

Best for: DeFi users, yield farmers, and cross-chain power users.

Why We Chose It:

-

It eliminates the “bridge and hide” strategy many used to defer taxes.

-

It highlights that even if the economic value stays the same, the legal right changes.

-

It aligns NZ with the strict “realisation” views held by the UK’s HMRC.

Things to consider: This can trigger a tax bill even if you haven’t “cashed out” to NZD, meaning you may need a cash reserve to cover taxes on paper gains.

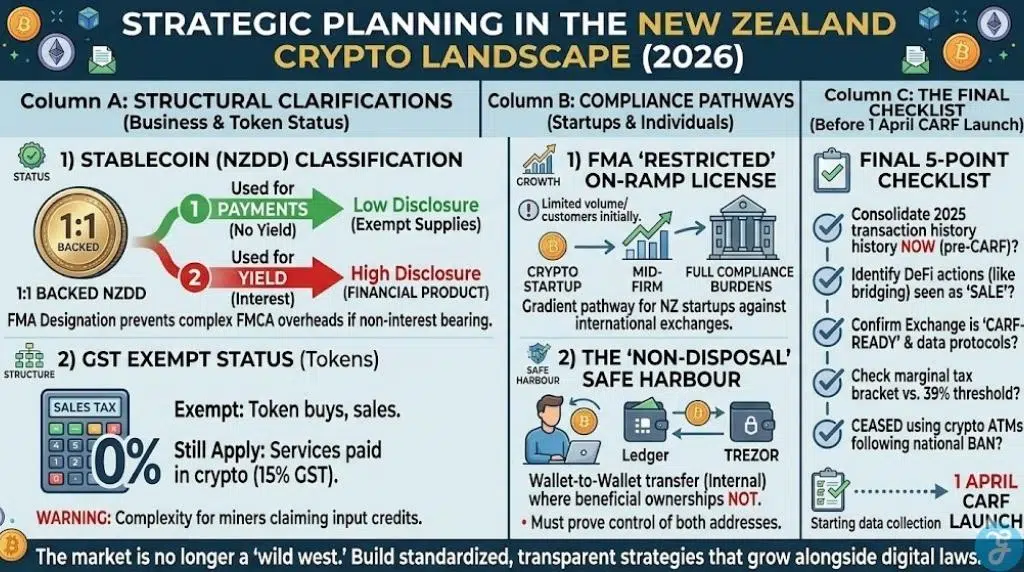

3. Stablecoin Classification and the NZDD Ruling

On 11 March 2026, the FMA issued a first-of-its-kind designation declaring the NZDD stablecoin (and similar 1:1 backed tokens) as a payment mechanism rather than a “financial product” or debt security. This prevents stablecoins from being bogged down by the heavy disclosure requirements of the Financial Markets Conduct Act, provided they pay no interest or yield.

Best for: Businesses looking to integrate NZD-pegged stablecoins into their payment rails.

Why We Chose It:

-

It provides much-needed legal clarity for the local fintech sector.

-

It reduces the “compliance friction” for merchants accepting digital payments.

-

It encourages the development of a domestic, regulated stablecoin ecosystem.

Things to consider: If a stablecoin begins offering “yield” or “interest,” it will likely be reclassified as a debt security, triggering massive compliance overheads.

4. The Enforcement of the Crypto ATM Ban

To combat money laundering and the “cash-to-crypto” pipeline, New Zealand authorities have completed the rollout of a ban on cryptocurrency ATMs. Officials cited the high risk of these machines being used for illicit finance and the lack of robust KYC (Know Your Customer) protections at physical kiosks.

Best for: Understanding why New Zealand is taking a harder stance on “anonymous” entry points.

Why We Chose It:

-

It signals a shift toward a “safe and simple” but highly regulated environment.

-

It removes a high-fee, high-risk entry point for vulnerable consumers.

-

It forces all crypto transactions back into the transparent, bank-linked ecosystem.

Things to consider: Investors must now use registered online exchanges that comply with the full Anti-Money Laundering (AML) reform.

5. The FMA’s New “Restricted” On-Ramp License

Recognising the need for innovation, FMA CEO Samantha Barrass introduced a restricted or “on-ramp” license in early 2026. This allows smaller fintechs and crypto startups to enter the market with lighter compliance burdens initially, with the restrictions being lifted as the firm grows in volume and maturity.

Best for: Local entrepreneurs and startup founders in the Web3 space.

Why We Chose It:

-

It prevents “compliance-killing” costs from stifling small New Zealand startups.

-

It provides a clear, graduated pathway to full financial service provider status.

-

It fosters a competitive environment against large international exchanges.

Things to consider: These licenses are “controlled,” meaning the FMA can place strict limits on the number of customers or the volume of trades allowed.

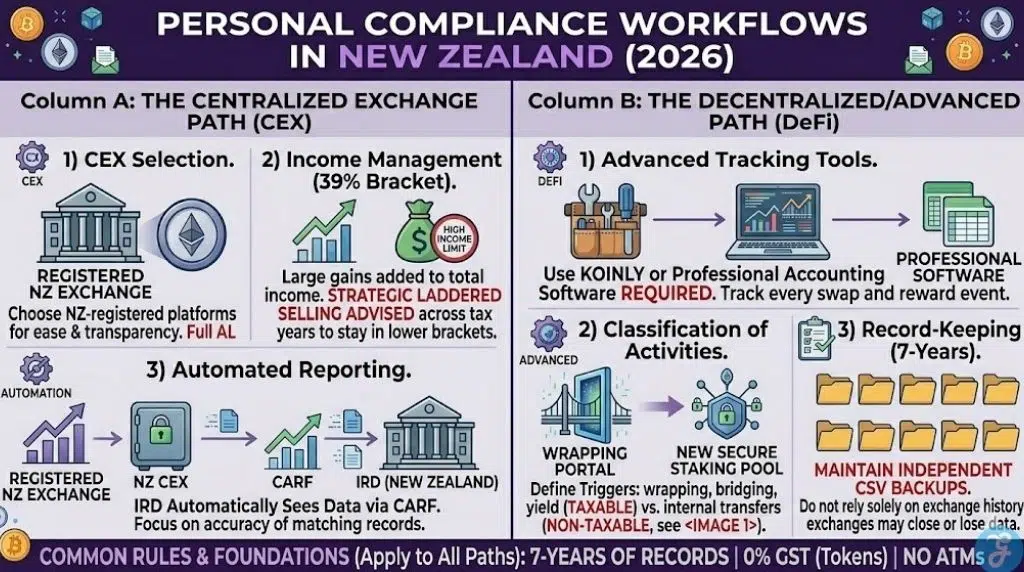

6. The 7-Year Standardised Record-Keeping Mandate

The IRD has reinforced that crypto records must be kept for seven years. Given the new visibility provided by CARF, “missing data” is no longer a valid excuse for non-compliance. Investors are now expected to maintain a standardised digital trail of every transaction hash and timestamp.

Best for: Long-term investors who want to protect themselves against retrospective audits.

Why We Chose It:

-

It is a non-negotiable requirement for any IRD enquiry.

-

It protects the investor by proving the “cost basis” of their assets.

-

It encourages the use of professional crypto accounting software that standardises data.

Things to consider: Relying on exchange download history is risky, as exchanges can close or lose data; always maintain an independent backup of your CSV files.

7. GST Exemption for Crypto-Asset Supplies

A vital piece of the puzzle that remains stable in 2026 is the GST-exempt status of crypto-assets. Digital assets are treated as “financial services” or “exempt supplies,” meaning you don’t pay 15% GST when buying or selling tokens. However, services paid for in crypto (like consulting) are still subject to standard GST rules.

Best for: Self-employed contractors and businesses using crypto for operational costs.

Why We Chose It:

-

It maintains New Zealand’s competitiveness as a crypto-friendly jurisdiction.

-

It prevents the “double taxation” problem that would exist if GST and Income Tax overlapped.

-

It simplifies the bookkeeping for most individual traders.

Things to consider: If you are “mining” crypto and are GST-registered, the rules for claiming input credits on your hardware can be extremely complex.

8. The “Non-Disposal” Rule for Wallet-to-Wallet Transfers

A common point of confusion cleared up in the IRRUIP18 issues paper is the status of internal transfers. Simply moving your Bitcoin from a Ledger to a Trezor, or from one exchange to another where you retain beneficial ownership, is not a taxable event.

Best for: Security-conscious investors who frequently move assets between storage solutions.

Why We Chose It:

-

It provides a “safe harbour” for those prioritising self-custody.

-

It distinguishes between a “technical move” and a “legal disposal.”

-

It ensures that improving your security doesn’t trigger a surprise tax bill.

Things to consider: You must be able to prove that you control both the “from” and “to” addresses if the IRD queries the transaction.

9. Strategic Planning for the 39% Top Tax Bracket

With New Zealand’s top marginal tax rate at 39% for income over $180,000, 2026 is the year of strategic timing. Large crypto gains are added to your other income, meaning a single well-timed sale can push your entire portfolio’s profit into the highest tax bracket.

Best for: High-income earners and “whales” planning their exit strategy.

Why We Chose It:

-

It highlights the “hidden cost” of impulsive selling.

-

It encourages “laddered selling” across multiple tax years to stay in lower brackets.

-

It reflects the reality of how crypto is integrated into the broader NZ income tax system.

Things to consider: Using a “Look-Through Company” (LTC) or a Trust can sometimes help manage this tax load, but only if the structure is set up before the profit is made.

Comparing the 2026 NZ Crypto Landscape

To effectively manage your NZ Crypto Regulation Updates, it is helpful to see how these rules vary depending on the type of activity you are performing. The table below provides a quick reference for the current 2026 tax and legal status.

NZ Crypto Activity Status Table (2026)

| Activity Type | Taxable Event? | GST Status | Disclosure Level |

| Buy & Hold | No (Until Sale) | Exempt | High (via CARF) |

| Staking Rewards | Yes (On Receipt) | Exempt | High (via IRRUIP18) |

| DeFi Wrapping | Yes (Disposal) | Exempt | High (New in 2026) |

| Wallet Transfer | No | Exempt | Minimal |

| Accepting as Payment | Yes (Business Income) | 15% (on service) | High (Required) |

Our Top 3 Picks and Why?

Of the nine points discussed, the CARF Deadline, DeFi Disposal Triggers, and Stablecoin Classification are the most critical. These three form the “compliance foundation” for 2026: they establish who sees your data, what specific actions will cost you in tax, and how the assets themselves are legally defined. Mastering these three ensures you are prepared for almost any regulatory hurdle in New Zealand.

Strategic Guide: How to Stay Compliant by Yourself?

Staying on the right side of the law in New Zealand doesn’t require a law degree, but it does require a proactive approach to your digital finances.

The Selection Framework:

-

Centralised vs Decentralised: If you use Centralised Exchanges (CEXs), assume the IRD already has your data via CARF. If you use DeFi, assume your “wrapping” and “staking” are taxable events.

-

Long-Term vs Short-Term: If your dominant purpose is selling for profit, you are taxable. If you are a “true” collector (rare in crypto), you might have an argument for non-taxable gains, but the IRD’s default position is that crypto is acquired for disposal.

-

Stablecoin Utility: Use NZD-pegged stablecoins for payments to simplify your accounting, as their “non-financial product” status makes them easier to handle for small business owners.

Decision Matrix (Table):

| Strategy A: High Compliance (CEX-focused) | Strategy B: Advanced Compliance (DeFi-focused) |

| Use NZ-registered exchanges. | Use Koinly or similar to track every swap. |

| Export CARF-compliant CSVs monthly. | Document “wrapped” vs “unwrapped” events. |

| Pay tax on 31 March each year. | Account for “rewards” the moment they hit your wallet. |

The Final Checklist: 5-point Checklist Before the 1 April CARF Launch

-

Have you consolidated your 2025 transaction history before the new rules kick in?

-

Are you aware which of your DeFi activities (like bridging) will now be seen as a “sale”?

-

Have you checked if your exchange is “CARF-ready” and what data they will be sharing?

-

Is your current marginal tax bracket close to the 39% threshold?

-

Have you stopped using crypto ATMs following the national ban?

The Future of Digital Finance in Wellington

The New Zealand crypto market in 2026 is no longer a “wild west.” By embracing international standards like CARF and providing specific guidance on DeFi and stablecoins, the FMA and IRD have created a framework that balances enforcement with innovation. For the “insider,” the key to success is no longer about finding loopholes, but about building a standardised, transparent strategy that grows alongside these new digital laws.