In the Australian property market, few terms ignite as much debate as negative gearing. As the nation grapples with housing affordability in 2026, understanding the intersection of tax policy and real estate investment is crucial for both seasoned investors and first-time buyers navigating the current economic climate.

How We Selected Our 7 Best Negative Gearing Australia Facts

To assemble this list, we analysed recent Australian Taxation Office (ATO) data, the latest federal budget papers, and independent economic modelling from the Grattan Institute. Our selection was based on three primary factors: the direct impact on personal income tax, the relationship between interest rates and investor cash flow, and the most recent 2026 legislative proposals regarding property tax reform.

The Most Significant 7 Facts About Negative Gearing Australia in 2026

The following points break down the essential mechanics and the political reality of this tax strategy within the Australian economy.

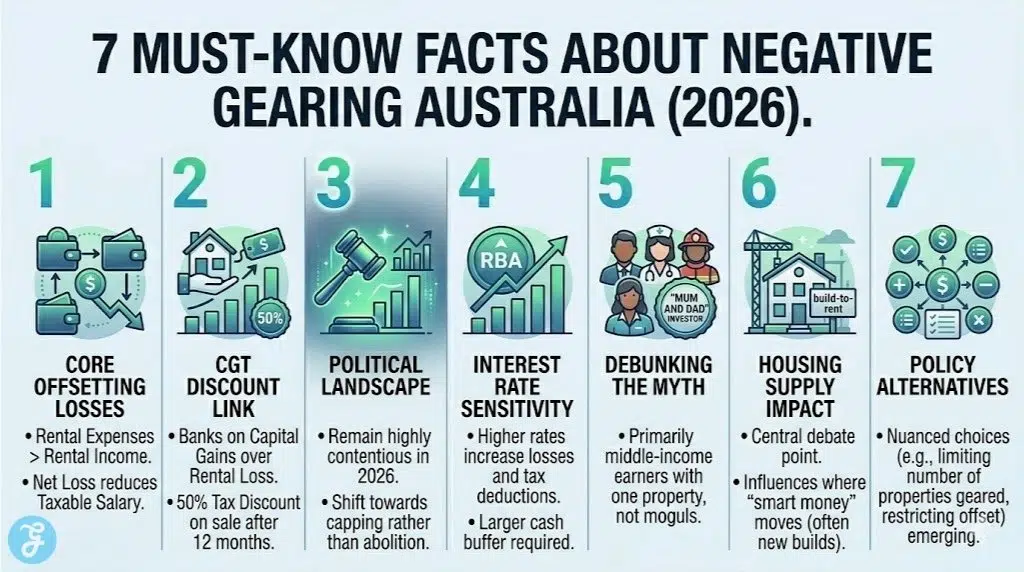

1. The Core Mechanism of Tax Offsetting

Negative gearing occurs when the annual cost of owning an investment property—including mortgage interest, maintenance, and rates—exceeds the rental income it generates. Under current Australian law, this “net rental loss” can be deducted from your other taxable income, such as your salary.

Best for: High-income earners looking to reduce their total income tax liability.

Why We Chose It:

- It is the fundamental pillar of Australian property investment strategy.

- It provides an immediate tax benefit that offsets holding costs.

- It allows investors to manage expensive assets that would otherwise be unaffordable.

Things to consider: You are still technically losing money out-of-pocket each month; the tax return only recovers a portion of that loss.

2. The Interplay with the Capital Gains Tax (CGT) Discount

Negative gearing is rarely used in isolation. Most investors accept a short-term income loss with the expectation of a long-term capital gain. When the property is eventually sold, the 50% CGT discount (for assets held over 12 months) ensures that only half of the profit is taxed.

Best for: Long-term “buy and hold” investors focusing on wealth creation.

Why We Chose It:

- It explains why investors are willing to lose money on rent—they are banking on the untaxed growth.

- It creates a “tax arbitrage” where losses are deducted at full marginal rates, but gains are taxed at half.

Things to consider: If property prices stagnate or fall, the strategy fails because there is no gain to offset the accumulated losses.

3. The 2026 Political and Reform Landscape

As of early 2026, negative gearing remains a “third rail” of Australian politics. While various minor parties have called for its total abolition to improve housing affordability, the major parties have shifted toward “capping” the number of properties an individual can gear rather than removing the perk entirely.

Best for: Staying informed on potential legislative risks to your portfolio.

Why We Chose It:

- High housing prices in 2026 have made tax reform a primary election issue.

- Any change to these rules could trigger a significant shift in market liquidity.

Things to consider: Grandfathering clauses are almost certain to be included in any reform, protecting existing investors.

4. Interest Rate Sensitivity and the “Cash Flow” Reality

With the Reserve Bank of Australia (RBA) maintaining a “higher for longer” stance on interest rates through 2025 and into 2026, the volume of negatively geared properties has hit record highs. Higher interest payments mean larger tax deductions, but also tighter monthly budgets for investors.

Best for: Investors managing mortgage stress in a high-rate environment.

Why We Chose It:

- It highlights the “double-edged sword” of high interest rates for property owners.

-

It underscores the importance of having a “cash buffer” to survive between tax returns.

Things to consider: A drop in interest rates could turn a “negatively geared” property into a “positively geared” one, increasing your tax bill.

5. The Demographic Profile of Gearing Investors

Despite the popular image of “property moguls,” ATO data reveals that the vast majority of people using Negative Gearing Australia are middle-income earners. This includes teachers, nurses, and emergency service workers who own a single investment property.

Best for: Debunking common myths about who benefits from property tax breaks.

Why We Chose It:

- It explains why total abolition is politically difficult—it affects a large portion of the voting middle class.

- It shows that property is a common vehicle for retirement savings in Australia.

Things to consider: While many investors are middle-class, the largest financial benefits still accrue to those in the highest tax brackets.

6. Impact on Housing Supply and New Construction

A major point of contention in 2026 is whether negative gearing encourages new home builds. Critics argue it mostly drives up prices for existing homes, while proponents argue that without it, the private rental market would collapse due to a lack of investor interest.

Best for: Understanding the broader societal impact of your investment choices.

Why We Chose It:

- It is the central argument used by both sides of the tax reform debate.

- It influences where “smart money” is moving—often toward new “build-to-rent” projects.

Things to consider: Some proposed reforms would only allow negative gearing for new properties to stimulate supply.

7. Proposed “Caps” and Policy Alternatives

Rather than a “yes/no” debate, 2026 has seen the rise of nuanced alternatives. These include limiting deductions to the amount of investment income earned (preventing offsets against salary) or capping the total number of geared properties at two per person.

Best for: Planning a diversified portfolio that isn’t reliant on a single tax rule.

Why We Chose It:

- These “middle-ground” policies are the most likely to be legislated in the next three years.

- They represent a move toward “revenue neutral” housing policy.

Things to consider: Investors with more than two properties may need to restructure their holdings into trusts or companies.

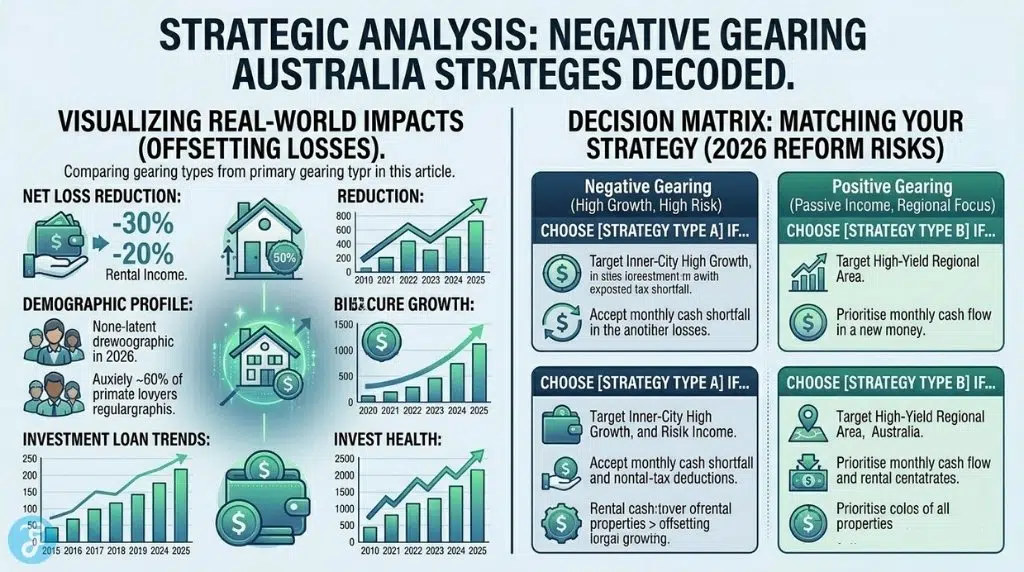

An Overview Of Negative Gearing Australia and Economic Trends

The property market in 2026 is defined by a delicate balance between high holding costs and robust capital growth in key metropolitan areas. As tax rules evolve, the “passive” investor is being replaced by the “strategic” investor who prioritises location and yield.

Overview Comparison Table

| Investor Type | Primary Goal | Tax Impact | Market Risk |

| Negative Gearing | Capital Growth | High Tax Deduction | Interest Rate Hikes |

| Positive Gearing | Monthly Income | Increased Tax Bill | Low Growth |

| Neutral Gearing | Break-Even | Minimal Tax Impact | Vacancy Rates |

Our Top 3 Picks and Why?

Of the seven facts discussed, the Core Mechanism of Tax Offsetting, the CGT Link, and Interest Rate Sensitivity are the most critical. These three pillars form the “holy trinity” of the Australian property strategy: they provide the immediate tax relief, the long-term wealth incentive, and the primary variable risk (interest rates) that determines if an investment is sustainable.

Buyer’s Guide: How to Choose the Right Negative Gearing Australia Strategy by Yourself?

Before jumping into a property purchase for tax reasons, you must ensure the underlying asset is sound. Never buy a “bad” property just for a “good” tax deduction.

The Selection Framework:

Marginal Tax Rate: If you are in the 19% or 32% bracket, the benefits of negative gearing are significantly lower than for those in the 45% bracket.

Rental Yield: Look for a “balanced” yield that doesn’t leave you with an unmanageable monthly shortfall.

Growth History: Ensure the area has a proven track record of capital growth to justify the 50% CGT strategy later.

Decision Matrix (Table):

| Choose Strategy A (Negative) if… | Choose Strategy B (Positive) if… |

| You are in the highest tax bracket. | You are nearing retirement and need cash flow. |

| You have a high, stable salary. | You want to pay down your mortgage quickly. |

| You are targeting high-growth inner-city areas. | You are investing in high-yield regional areas. |

The Final Checklist: 5-point Checklist Before Committing to a Gearing Strategy

Have you calculated your “after-tax” cash flow, including all hidden costs like property management fees?

Is your employment stable enough to cover the “net loss” for at least 12–24 months?

Have you spoken to an accountant about the impact of the 2026 “Stage 3” tax adjustments on your deductions?

Does the property have the potential for capital growth that exceeds your total out-of-pocket losses?

Are you prepared for the possibility of a “cap” on the number of geared properties you can hold?

The Future of Australian Property and Tax Efficiency

Negative gearing is not a “magic bullet” for wealth, but a sophisticated financial tool that requires active management. As the Australian political landscape shifts toward a more supply-focused housing model, the investors who succeed will be those who adapt their strategies to align with both tax efficiency and broader economic goals.