Tired of low savings rates and high fees cutting into hard-earned money? Many people struggle to choose the right bank in today’s digital world, unsure whether to stick with traditional branches or switch to modern online options.

It’s like choosing between a cozy neighborhood diner and a fast drive-thru—both serve a purpose, but in different ways.

In the Online Banks vs Traditional Banks debate, online banks often offer higher savings interest rates by avoiding the costs of physical branches and large staff. This guide highlights key differences, including accessibility, customer service, fees, and security, to help match banking needs with the best option.

Use this as a clear roadmap to make smarter financial decisions and find the right fit.

What Are Traditional Banks?

Walking into a brick-and-mortar spot like Bank of America or Chase, where tellers greet you face-to-face for deposits or loans. These spots, often called physical banks, offer services from checking accounts to credit cards, making everyday money moves feel personal and hands-on.

Definition and Overview (Traditional Banks)

Traditional banks stand as the classic pillars of finance, with physical branches you can walk into for face-to-face help. These brick-and-mortar banks, like Bank of America or Chase, serve as financial institutions that handle your money needs right in your neighborhood.

They offer a wide range of financial services, from checking accounts to certificates of deposit, or CDs, and even credit cards for everyday personal finance. Customers visit these spots for cash deposits, quick chats with tellers, or complex financial transactions that feel more secure in person.

Think of them as the reliable old friend who always has a door open, blending tradition with modern touches.

Many traditional banks now mix in extensive online capabilities, so you get the best of both worlds without missing out. They provide personal service and in-person convenience for tasks like cash deposits at their ATM network.

This setup suits folks who value that human touch in their banking experience, especially when dealing with Huntington or Citi for broader options. Traditional banking tends to offer a wider range of services in total, covering everything from loans to investment products.

You know, it’s like having a sturdy toolbox ready for any money fix, complete with federal deposit insurance corporation protection through the FDIC.

Traditional banks give you that warm handshake feel, making finance less like a cold app and more like a trusted chat over coffee. – Emmanuel Nyame, financial expert at Investopedia

Services Provided by Traditional Banks

Traditional banks serve as your go-to spots for hands-on money matters. They mix old-school charm with modern twists to keep your finances in check.

- Checking and savings accounts form the backbone, letting you deposit cash right at the counter, and many spots like Capital One throw in high-yield savings accounts for extra growth.

- Loans and mortgages come with personal chats from bankers who guide you through options, often tying into services like CareCredit for health-related financing.

- Credit cards, such as the Synchrony Mastercard, offer rewards and easy applications in branch, plus tools for building credit history.

- Investment products, including certificates of deposit (CDs), get explained face-to-face, helping you pick ones with solid interest rates from places like American Express.

- ATM access shines bright, with networks that let you withdraw fee-free, and some banks link to Zelle for quick peer-to-peer transfers.

- Customer support happens in person or via phone, providing that human touch for tricky issues, unlike purely digital banking setups.

- Safe deposit boxes protect your valuables on-site, a perk not always found in online-only banks.

- Business banking services cover everything from payroll to merchant accounts, with advisors who meet you to tailor financial products.

- Notary and wire transfer services add convenience, often free or low-cost at brick-and-mortar locations insured by the Federal Deposit Insurance Corporation (FDIC).

- Online and mobile banking features blend in seamlessly now, giving you digital wallet options while still offering those in-person visits for peace of mind.

What Are Online Banks?

Online banks run everything through the web, no brick-and-mortar spots in sight, making them a fresh take on banking basics like your everyday bank account. They handle tasks with apps and sites, often teaming up with ATMs for cash needs, and folks love how direct banks cut out the middleman for quicker moves.

Definition and Overview (Online Banks)

Ditching long lines at the bank for quick taps on your phone. Banks that operate fully online, like direct banks such as Synchrony Bank or Discover, give you access to banking products mainly through mobile apps and websites.

They skip physical branches to cut costs, which lets them offer higher interest rates on savings accounts. Customers enjoy fewer fees too, thanks to those low overhead expenses. Think of it as banking that fits in your pocket, prioritizing digital convenience and easy access for everyone.

Online banks redefine convenience by putting powerful tools like two-factor authentication right at your fingertips, says Libby Wells, a banking expert.

These institutions, including pioneers like Security First Network Bank, focus on cybersecurity to keep your bank account safe. They provide competitive annual percentage yields, often beating traditional options, as noted by Bankrate data.

Mobile banking here means you handle everything from deposits to transfers without stepping outside. Bain and Company studies show how such banks emphasize user accessibility, making everyday tasks a breeze.

How Online Banks Operate

Online banks run everything through digital channels, no physical branches in sight. They cut costs by skipping rent and staff for buildings, which lets them pass savings to you in big ways.

You grab your phone and handle deposits or transfers anytime, day or night, with apps that feel like a chat with a friend. These banks prioritize digital convenience and user accessibility, making online banking a breeze for quick tasks.

They offer higher interest rates due to their lower overhead costs, and yes, that means more competitive rates for savings accounts or investment products. Pippin Wilbers, an expert in finance, often highlights how these setups maintain editorial integrity by focusing on clear, honest info for users.

Customers access banking products mainly through mobile and online platforms, ditching lines at tellers for speedy logins. Online banks charge fewer fees than traditional brick-and-mortar counterparts, keeping your money where it belongs, in your pocket.

They typically provide higher annual percentage yields on savings products compared to brick-and-mortar banks, a real win if you save often. Some even include pay later options for flexible spending, adding to the mix.

While today’s traditional banks boast extensive online capabilities, pure online banks stay completely digital or online-only, emphasizing that seamless vibe.

Key Differences Between Traditional and Online Banks

Ever wonder why picking a bank feels like choosing between a cozy old diner, and a sleek food truck on wheels? Traditional spots offer that face-to-face chat over coffee, while online ones let you handle cash from your couch at midnight, but watch out for those hidden fees that can sneak up like a bad surprise party.

Accessibility and Convenience

Traditional banks shine with their brick-and-mortar locations. You walk in, chat face-to-face, and handle cash deposits on the spot. You dash to a local branch during lunch, grab some advice from a teller who knows your name.

That personal touch feels like a warm handshake in a digital world. Online banks flip the script. They deliver services through mobile apps and websites, anytime, anywhere. No lines, no closing hours – just tap your phone at midnight for a quick transfer.

Think of it as banking in your pajamas, super handy for busy folks.

Sure, traditional spots offer that in-person convenience for complex needs, like notary services. Yet online options prioritize digital ease, letting you manage accounts from your couch.

Many traditional banks now blend in extensive online tools too. Some go fully digital, ditching branches altogether. This mix gives you choices that fit your lifestyle, whether you crave human interaction or lightning-fast access.

Fees and Costs

Let’s compare fees and costs between online banks and traditional ones, since this can hit your wallet hard.

| Aspect | Traditional Banks | Online Banks |

|---|---|---|

| Typical Fees | They often charge more for monthly maintenance, ATM use outside networks, and overdrafts, adding up fast like a leaky faucet. | Online banks charge fewer fees than brick-and-mortar counterparts, keeping your money safe from sneaky deductions. |

| Overhead Impact | High costs from physical branches lead to lower interest rates on savings, so you earn less over time. | Lower overhead costs let them offer higher interest rates, putting more cash back in your pocket. |

| Savings Yields | Brick-and-mortar spots give lower annual percentage yields on savings products, which feels like settling for crumbs. | They typically offer higher annual percentage yields on savings, thanks to slim operations without fancy lobbies. |

| Other Cost Factors | In-person services might include extra charges for things like wire transfers or paper statements. | Competitive rates extend to investment products, with digital access cutting out middleman expenses for you. |

Interest Rates and Savings Options

Online banks and traditional banks show big differences in interest rates and savings options, often tipping the scale based on your money goals.

| Aspect | Traditional Banks | Online Banks |

|---|---|---|

| Interest Rates | They give lower rates on savings. Brick-and-mortar spots mean higher costs, so your money grows slow. Stashing cash in a sleepy vault, it barely buds up. | They push higher interest rates, thanks to low overhead. Online spots cut costs, so you earn more. Online banks offer higher annual percentage yields on savings products than brick-and-mortar banks do. They provide more competitive rates for savings accounts or investment products. Think of it as your money sprinting ahead, not just strolling. |

| Savings Options | They serve up a wider range of services, like easy cash deposits at branches. You get in-person help for complex needs, but rates lag. Traditional banks offer brick-and-mortar locations that customers can visit in person. | They focus on digital perks with higher yields. You access products through mobile and online platforms, often with fewer fees. Online banks charge fewer fees than their traditional brick-and-mortar counterparts. Imagine ditching lines for app taps, your savings bloom faster here. |

Personal Interaction and Customer Service

Traditional banks shine with face-to-face chats, you know, like when you walk into a branch and talk to a teller about your account. They offer personal service right there in brick-and-mortar locations, perfect for folks who need help with cash deposits or complex issues.

You’re stuck on a loan question, so you pop in and sort it out over coffee, almost like catching up with an old friend. Customers love that human touch, it builds trust in ways a screen can’t match.

Online banks flip the script by focusing on digital tools, think apps and chats that let you handle everything from your couch. They prioritize mobile and online platforms for quick access, no lines or drive time involved.

Sure, you might miss the in-person vibe, but hey, their extensive online capabilities keep things smooth, even if traditional spots now mix in digital options too. Troubleshooting a transfer at midnight, the app guides you like a trusty sidekick, saving you a trip.

Pros and Cons of Traditional Banks

Walking into a cozy branch where friendly tellers know your name and handle everything from quick cash deposits to complex loans right on the spot, offering rock-solid security with vaults and in-person advice that feels like chatting with a trusted neighbor, yet these spots can hit your wallet with sneaky monthly charges, long lines during lunch rushes, and branches that close just when you need them most—hey, if you’re weighing whether this old-school vibe suits your daily grind, dive deeper into our full breakdown ahead to pick the perfect fit for your money moves.

Advantages of Traditional Banks

Traditional banks bring that classic touch to your money matters, like a reliable old friend who’s always there. They shine in ways that make banking feel personal and secure, drawing on their long history to meet diverse needs.

- Personal service stands out as a big plus with traditional banks; you get face-to-face help from tellers who know your name, and this builds trust, especially when you need advice on loans or complex transactions. Walking in, chatting about your financial goals over coffee, and leaving with customized solutions that feel just right.

- In-person convenience for cash deposits makes life easier; drop off your money at a branch without fuss, perfect for folks who handle lots of cash from jobs or small businesses. Envision this: you finish a garage sale, head to the bank, and deposit everything on the spot, no mailing checks or waiting for apps to process.

- Brick-and-mortar locations offer that tangible presence; visit anytime for services like safe deposit boxes or notary help, giving peace of mind in a digital landscape. It’s like having a home base for your finances, where you can sort issues right away, face to face.

- A wider range of services comes standard with traditional banking; from wealth management to international wire transfers, they cover more ground than many online options. Think of it as a full toolbox, ready for everything from everyday checking to big life events like buying a house.

- Extensive online capabilities blend the best of both worlds in today’s traditional banks; log in from home for quick transfers or bill pay, even as you enjoy those physical branches. This setup lets you bank your way, mixing digital speed with the option for a real conversation when it counts.

Disadvantages of Traditional Banks

Traditional banks come with some downsides that might make you think twice. They often lag behind in areas where online options shine, like costs and digital ease.

- Higher fees eat into your money, since traditional banks charge more for things like account maintenance and overdrafts compared to online banks, which keep fees low due to their slim operations.

- Lower interest rates on savings hurt your growth, as brick-and-mortar spots offer smaller annual percentage yields than online banks, thanks to those high overhead costs from physical branches.

- Limited hours tie you down, because you can’t always pop in for cash deposits or personal service outside business times, unlike the round-the-clock access from mobile and online platforms.

- Less competitive savings options slow your earnings, with traditional banks trailing behind on rates for accounts and investments, while online banks push higher yields to attract digital users.

- Wider services sound great, but they come with extra complexity, forcing you to deal with in-person visits for some tasks that online banks handle smoothly through apps and websites.

- Personal interaction helps, sure, but it means waiting in lines at brick-and-mortar locations, a hassle when online banks prioritize quick digital convenience without the face-to-face wait.

Pros and Cons of Online Banks

Ever wondered if ditching that old brick-and-mortar spot for a sleek digital banking app, like those from Ally or Chime, could save you cash on fees while offering higher yields on your checking or high-yield savings accounts, but maybe leave you missing face-to-face chats during a glitch? Stick around to weigh these ups and downs for your wallet.

Advantages of Online Banks

Online banks bring a fresh twist to managing your money, often making it easier and more rewarding than you might expect. They cut out the middleman of physical branches, passing those savings right back to you in smart ways.

- These banks shine with higher annual percentage yields on savings products, beating out brick-and-mortar spots because they skip the costly overhead, like rent for buildings.

- Fees stay low here, folks, way fewer than what traditional banks charge, so your hard-earned cash doesn’t vanish into thin air on silly extras.

- Expect competitive interest rates on savings accounts or investment options, thanks to those slim operating costs that let online banks reward you more.

- Digital convenience rules the day with online and mobile banking, putting everything at your fingertips through apps and websites, no lines or drives needed.

- Customers get easy access to all banking products mainly via mobile and online platforms, Checking your balance during a coffee break, simple as that.

- Some banks run completely digital or online-only, prioritizing user accessibility that fits your on-the-go life, while even traditional ones add online features, but these pure players lead the pack.

Disadvantages of Online Banks

Online banks sound great for tech-savvy folks, but they come with some real drawbacks that might make you pause. You could miss out on that face-to-face help, especially if you love chatting with a teller over coffee.

- Limited personal interaction hits hard when you crave a human touch; traditional banks shine here with their in-person service, letting you walk into brick-and-mortar locations for quick chats about your accounts, while online setups force you to rely on chatbots or phone calls that feel cold and impersonal.

- Cash deposits turn into a hassle without physical branches; sure, online banks grant access through mobile and online platforms, but you often need to hunt for partner ATMs or mail checks, unlike traditional banks that offer in-person convenience for dropping off your money right away.

- Customer service can feel distant and slow; Waiting on hold during a glitch, with no local spot to visit, as online and mobile banking prioritize digital convenience over the warm, hands-on support you get from traditional banks’ wider range of services.

- Security worries loom larger in a fully digital world; hackers love targeting online platforms, and without brick-and-mortar backups, you might sweat over potential breaches, even though today’s traditional banks offer extensive online capabilities too.

- Fewer total services leave gaps for complex needs; online banks may skimp on things like notary help or safe deposit boxes, forcing you to look elsewhere, while traditional banking tends to provide that broader lineup in one spot.

How to Choose Between Online and Traditional Banks

Picking the right bank feels like choosing between a cozy neighborhood diner and a speedy drive-thru, you know, so start by figuring out if you crave face-to-face chats at a local branch or quick taps on a mobile app for your checking account and ATM access.

Think about your daily habits, like how often you deposit cash or need help with loans, and weigh if higher interest rates on savings beat out those pesky fees from brick-and-mortar spots.

Don’t forget security, folks—online options use strong encryption and fraud alerts, while traditional ones offer that personal touch with tellers who know your name, but always check FDIC insurance for peace of mind.

If this sparks your curiosity about ditching your old bank for something fresh, keep scrolling to dive deeper into making the switch that suits your wallet and lifestyle.

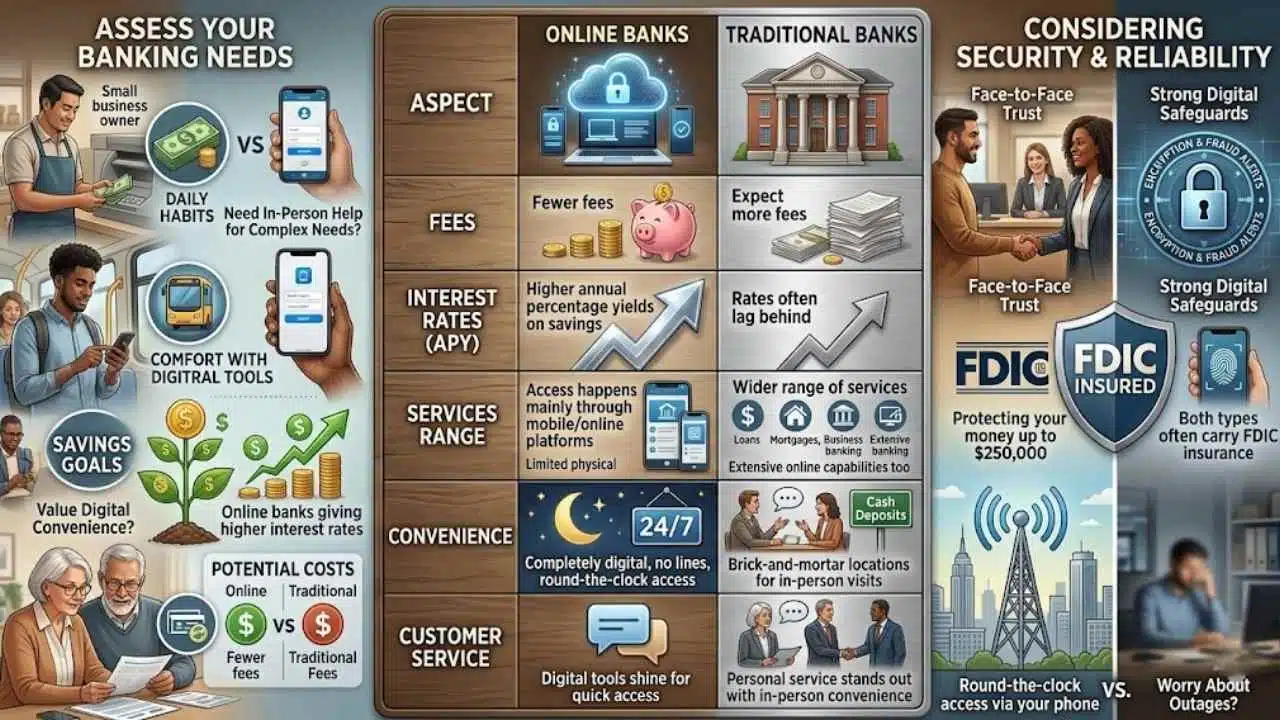

Assessing Your Banking Needs

You face choices between online banks and traditional banks every day. Pick based on your daily habits and financial goals.

- Think about how often you need in-person help, like cash deposits at brick-and-mortar locations that traditional banks offer. You might prefer this if you handle lots of cash. Traditional banks provide personal service and in-person convenience for such tasks. They tend to offer a wider range of services in general, which suits complex needs.

- Check your comfort with digital tools, since online banks grant customers access to banking products primarily through mobile and online platforms. If you love apps and quick logins, this fits. Online and mobile banking typically prioritize digital convenience and user accessibility, like a smooth ride on a highway.

- Look at your savings goals, because online banks typically offer higher annual percentage yields on savings products compared to brick-and-mortar banks. They give higher interest rates due to their lower overhead costs. Online banks may offer more competitive interest rates for savings accounts or investment products, boosting your money faster.

- Count up potential costs, as online banks charge fewer fees than their traditional brick-and-mortar counterparts. Traditional banks might hit you with more charges. This matters if you hate surprise fees eating into your budget, like unwelcome guests at a party.

- Consider if you value face-to-face chats, since traditional banks offer brick-and-mortar locations that customers can visit in person. Online banks focus on digital chats instead. Today’s traditional banks offer extensive online capabilities, while some banks are completely digital or online-only, so blend them if you want both worlds.

- Weigh your need for broad options, given that traditional banking tends to offer a wider range of services in general. Online banks shine in specific areas like high-yield savings. Pick what matches your life, perhaps like choosing shoes that fit just right for a long walk.

Comparing Costs and Benefits

Let’s weigh the costs and benefits of online banks against traditional ones, like sizing up two old friends to see who fits your wallet best.

| Aspect | Online Banks | Traditional Banks |

|---|---|---|

| Fees | They charge fewer fees than brick-and-mortar spots. Dodging those pesky charges, like a pro at a game of tag. | Expect more fees here. They cover costs for all those physical branches, you know. |

| Interest Rates | Online banks offer higher annual percentage yields on savings products. They also give competitive rates for savings accounts or investment products, thanks to low overhead costs. | Rates often lag behind. Brick-and-mortar banks spend big on buildings, so your savings grow slower. |

| Services Range | Access happens mainly through mobile and online platforms. They prioritize digital convenience and user accessibility, but options might feel limited. | They provide a wider range of services in general. Plus, many now boast extensive online capabilities, blending old and new. |

| Convenience | Some banks run completely digital or online-only. Banking from your couch at midnight, no lines or drives needed. | They offer brick-and-mortar locations for in-person visits. Great for cash deposits and that face-to-face chat, like catching up with a neighbor. |

| Customer Service | Digital tools shine for quick access. Yet, you might miss the human touch during tricky spots, feeling a bit like talking to a robot pal. | Personal service stands out with in-person convenience. Staff help right there, making complex issues easier to sort. |

Considering Security and Reliability

Security matters a lot when you pick a bank. Traditional banks offer brick-and-mortar locations that customers can visit in person, which adds a layer of trust for some folks. You walk in, talk to a teller, and handle things face-to-face.

Online banks grant customers access to banking products primarily through mobile and online platforms, so they focus on strong digital safeguards like encryption and fraud alerts. Both types often carry FDIC insurance, protecting your money up to $250,000.

Think about your comfort with tech; if you worry about hacks, traditional spots might feel safer, even though online ones use top-notch tools to keep data secure.

Reliability ties into how you access your funds. Today’s traditional banks offer extensive online capabilities, blending in-person service with apps for quick checks. Some banks run completely digital or online-only, which means no branches but round-the-clock access via your phone.

Imagine needing cash late at night; traditional banking tends to offer a wider range of services in general, including easy deposits at ATMs. Online and mobile banking typically prioritize digital convenience and user accessibility, but what if the internet goes down? Weigh these points against your daily habits, like if you travel often or prefer human help during outages.

Final Words

You’ve weighed the perks of traditional banks, like face-to-face chats and easy cash drops, against online banks’ high interest rates and low fees. Pick what fits your life, since both types keep your money safe with solid tech and rules.

These choices boost your savings without much hassle, thanks to simple apps or quick branch visits. Check out sites like Bankrate for rate comparisons, or talk to a financial advisor for personalized tips.

Switched to an online bank and watched my savings grow faster than expected, what a relief. Now go ahead, grab the bank that sparks your financial joy and watch your future brighten.

Frequently Asked Questions (FAQs): About Online Banks vs Traditional Banks

1. What’s the big difference between online banks and traditional banks?

Online banks operate without physical branches, so you handle everything through apps or websites, which often means lower fees and higher interest rates. Traditional banks have actual locations you can visit for face-to-face help, like chatting with a teller about your savings. Think of it as choosing between a speedy drive-thru and a sit-down diner, both get the job done but in their own way.

2. Are online banks safer than traditional ones?

People worry about security with online banks, but they use top-notch encryption just like traditional banks do. In fact, both follow strict rules to protect your money.

3. Why might I pick a traditional bank over an online one?

If you like personal touches, traditional banks offer in-person customer service that feels like talking to an old friend. They also let you deposit cash easily at branches, which online banks can’t match without extra steps.

4. How do I choose between online and traditional banks for my needs?

Start by thinking about your daily habits, if you hate lines and love convenience, go online. But if you need quick cash access or prefer human advice, stick with traditional. It’s like picking shoes, comfort wins every time.