As we move through 2026, the prospect of a “Britcoin” has shifted from a theoretical concept to a detailed technical ambition. The Bank of England and HM Treasury are currently navigating the final stages of the design phase, preparing the groundwork for a financial infrastructure that could redefine how every household in the United Kingdom interacts with money.

How We Selected Our 10 Best Digital Pound Progress Updates

To curate these facts, we analysed the March 2026 progress reports from the Bank of England and the latest “National Payments Vision” published by HM Treasury. Our selection criteria focused on three pillars: technical feasibility demonstrated in the Digital Pound Lab, the legislative protections currently being drafted for Parliament, and the economic impact of holding limits on the traditional banking sector. We prioritised updates that offer concrete evidence of how the system will function in daily life rather than broad policy statements.

10 Critical Facts about the Digital Pound and Future UK Payments

The following developments represent the most significant milestones in the UK’s journey toward a retail Central Bank Digital Currency (CBDC) as of mid-2026.

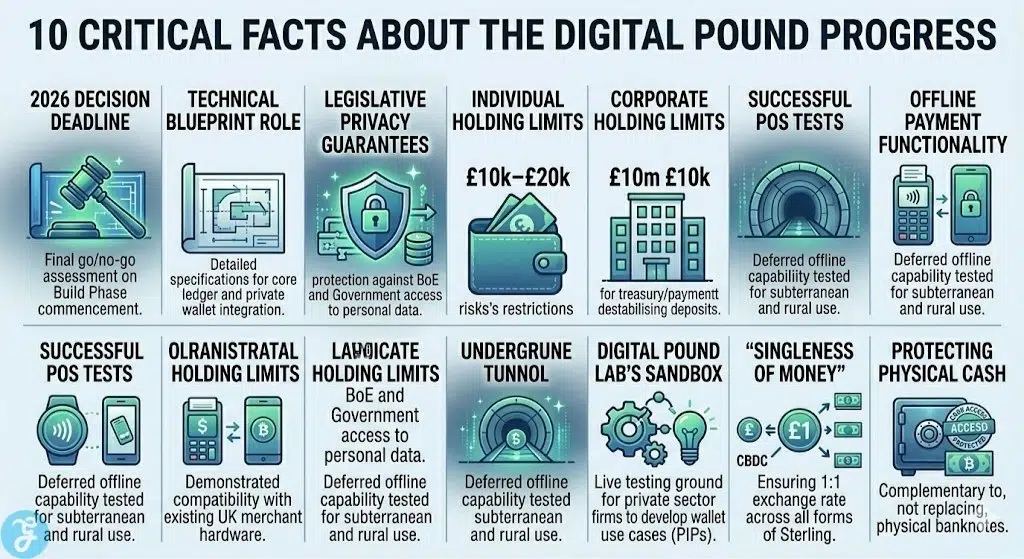

1. The 2026 Decision Deadline

The Bank of England and HM Treasury have confirmed that a final decision on whether to proceed to the “Build Phase” will be made in late 2026. This decision follows a multi-year design period and will be based on a comprehensive joint assessment of the technical blueprint and the overall economic case for issuance.

-

Best for: Stakeholders awaiting a definitive “go/no-go” signal for UK digital currency.

-

Why We Chose It: * It sets a clear timeline for the end of the experimental phase.

-

It triggers the potential commencement of primary legislation.

-

It allows the private sector to align their long-term investment strategies.

-

-

Things to consider: Even if the decision is “yes,” a public launch is not expected until the late 2020s.

2. The Role of the Digital Pound Blueprint

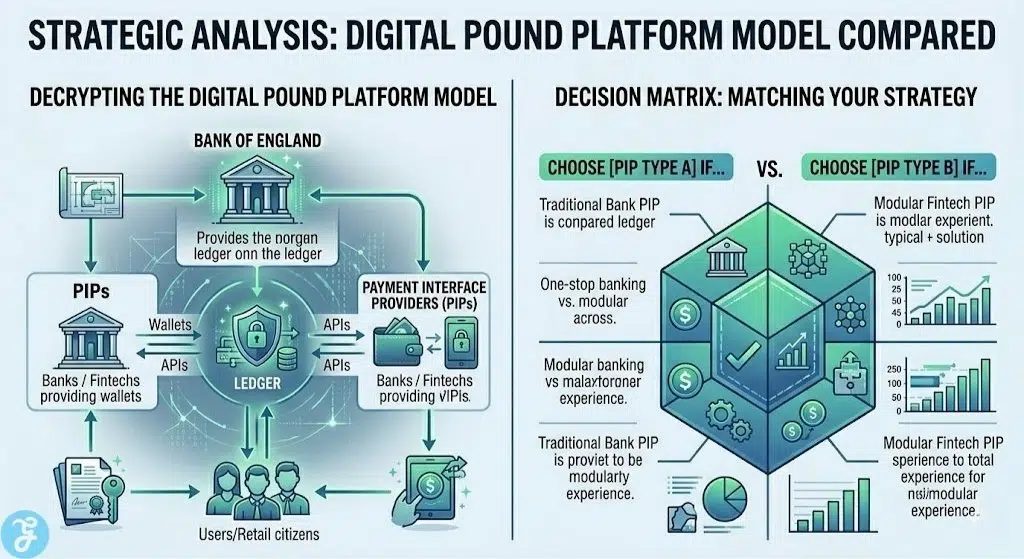

A detailed “Digital Pound Blueprint” is scheduled for publication later this year to explain the full technical and functional proposition. This document will serve as the master plan for the infrastructure, detailing how the core ledger will interact with private-sector wallet providers.

-

Best for: Developers and fintech firms looking to build compatible services.

-

Why We Chose It: * It provides the technical specifications needed for system interoperability.

-

It clarifies the “platform model” where the Bank provides the rails and the private sector provides the interface.

-

It outlines the standards for resilience and security.

-

-

Things to consider: The blueprint remains subject to change based on the final results of ongoing lab experiments.

3. Legislative Privacy Guarantees

A central fact of the 2026 plans is the commitment to primary legislation that will guarantee user privacy by law. This legislation will explicitly prevent both the Bank of England and the Government from accessing personal spending data or using the currency to control how individuals spend their money.

-

Best for: Citizens concerned about government surveillance and data privacy.

-

Why We Chose It: * It addresses the single largest point of public concern regarding CBDCs.

-

It ensures that privacy is “baked in” by design rather than just promised.

-

It separates the role of law enforcement from the day-to-day operation of the ledger.

-

-

Things to consider: While the Bank cannot see your data, your private wallet provider (like a bank) will still perform standard KYC checks.

4. Individual Holding Limits of £10,000 to £20,000

To protect the stability of the traditional banking system, the proposed holding limit for individuals remains between £10,000 and £20,000. This cap is designed to prevent a rapid “bank run” where depositors move all their savings from commercial banks into the safer central bank digital currency during a crisis.

-

Best for: Maintaining the balance between innovation and financial stability.

-

Why We Chose It: * It is a high enough limit to cover most monthly salaries and everyday spending.

-

It limits the “disintermediation” of commercial banks.

-

It is significantly higher than the limits proposed for the Digital Euro.

-

-

Things to consider: These limits are intended to be transitional and could be raised as the market matures.

5. Corporate Holding Limits in the Millions

While individual limits are well-publicised, the Bank is also finalising plans for corporate holding limits, which are expected to be set in the millions. These caps, potentially around £10 million, will allow businesses to use the Digital Pound for treasury management and B2B payments without destabilising bank funding.

-

Best for: Small-to-medium enterprises and large corporate treasurers.

-

Why We Chose It: * It enables the currency to be used for high-value wholesale and commercial trade.

-

It prevents massive corporate deposit flight from the banking sector.

-

It includes potential exemptions for systemically important financial institutions.

-

-

Things to consider: The complexity of managing these limits for multi-subsidiary companies is still being debated.

6. Successful POS Technical Feasibility Tests

Recent proofs-of-concept have demonstrated that the Digital Pound can work seamlessly with existing Point of Sale (POS) hardware found in UK shops. This ensures that merchants will not need to purchase expensive new equipment to accept digital currency payments in person.

-

Best for: Retailers and high-street businesses looking for low-cost implementation.

-

Why We Chose It: * It removes a major barrier to adoption for small businesses.

-

It proves that the technology can integrate with current payment terminals and Android devices.

-

It supports the goal of making the digital currency as easy to use as a contactless card.

-

-

Things to consider: Software updates for thousands of terminals will still be required before a full rollout.

7. Advancements in Offline Payment Functionality

The Bank has successfully tested “deferred offline payments,” which allow users to pay in environments without an active internet connection, such as on the London Underground. This feature is critical for ensuring the digital currency is as resilient and reliable as physical cash.

-

Best for: Commuters and residents in rural areas with poor connectivity.

-

Why We Chose It: * It replicates the “always-works” nature of physical banknotes.

-

It enhances the overall resilience of the UK’s payment infrastructure.

-

It uses “secure elements” in smartphones and smartcards to prevent double-spending.

-

-

Things to consider: Device-to-device offline payments (without any POS terminal) are a longer-term goal and may not be available on “day one.”

8. The Digital Pound Lab’s Industry Sandbox

The “Digital Pound Lab,” which launched in August 2025, is currently serving as a live testing ground for private sector firms to experiment with wallet use cases. This collaborative environment allows banks and fintechs to build and test their own “Payment Interface Provider” (PIP) services before any formal launch.

-

Best for: Fintech startups and traditional banks developing new financial products.

-

Why We Chose It: * It fosters a competitive ecosystem of private-sector wallet providers.

-

It identifies technical friction points before they reach the public.

-

It allows for the testing of “programmable money” features like automated payments.

-

-

Things to consider: Participation in the lab does not guarantee a future licence to operate a digital wallet.

9. Commitment to the “Singleness of Money”

A core principle of the project is ensuring the “singleness of money,” meaning one Digital Pound will always be worth exactly one pound in cash or bank deposits. This ensures that the UK’s money system remains unified and that different forms of currency do not trade at different values.

-

Best for: Maintaining public trust in the stability of the national currency.

-

Why We Chose It: * It prevents the fragmentation of the UK payment landscape.

-

It ensures a 1:1 exchange rate with physical banknotes at all times.

-

It distinguishes the digital currency from volatile cryptocurrencies.

-

-

Things to consider: Maintaining this singleness becomes more complex if private stablecoins become a dominant form of payment.

10. Protecting the Future of Physical Cash

The Bank of England has reiterated that the Digital Pound is intended to complement, not replace, physical cash. Legislation has already been enacted to protect the public’s right to access and use banknotes for as long as they are needed.

-

Best for: Vulnerable groups and those who prefer the anonymity of physical money.

-

Why We Chose It: * It ensures that no one is “forced” into a purely digital economy.

-

It maintains a fallback option during major power or network outages.

-

It reflects the government’s dual-track approach to payment innovation.

-

-

Things to consider: While cash is protected, its use is still expected to decline as digital alternatives become more convenient.

An Overview Of the Digital Pound and Its Strategic Future

The current design phase is about more than just technology; it is about ensuring that the UK remains at the forefront of global financial innovation. By building a secure, state-backed digital currency, the Bank of England aims to provide a stable foundation for the private sector to innovate.

Overview Comparison Table

Understanding how the digital currency sits between traditional money and private assets is key to following its progress.

| Feature | Physical Cash | Digital Pound | Commercial Bank Deposit |

| Issuer | Bank of England | Bank of England | Commercial Banks |

| Anonymity | Full | Private but not Anonymous | Private but not Anonymous |

| Interest | No | No (Proposed) | Yes |

| Holding Limit | None | £10k–£20k (Proposed) | None |

Our Top 3 Picks and Why?

Of the ten facts, the Legislative Privacy Guarantees, the Individual Holding Limits, and the Offline Functionality are the most impactful. These three pillars directly address the public’s concerns about surveillance, protect the banking system from collapse, and ensure that the currency is as dependable as the cash in your pocket.

Buyer’s Guide: How to Prepare for the Digital Pound by Yourself?

While you cannot yet open a digital pound wallet, you can take several steps to ensure you are ready for the transition later this decade.

The Selection Framework:

-

Provider Research: Keep an eye on which traditional banks and fintechs are participating in the Digital Pound Lab.

-

Digital Literacy: Familiarise yourself with mobile-first banking and digital identity verification (KYC) processes.

-

Security Awareness: Start using hardware security features on your devices, such as biometrics, to prepare for future wallet security.

Decision Matrix (Table):

| Prepare for Digital Pound if… | Stick to Traditional Banking if… |

| You want the security of money held directly at the central bank. | You prioritise earning interest on your liquid savings. |

| You want to use programmable payments for automated budgeting. | You are uncomfortable with any digital-only financial records. |

| You frequently use digital-only shops and services. | You rely primarily on physical cash for your daily privacy. |

The Final Checklist: 5-point Checklist for the 2026 Milestone

-

Follow the Bank of England’s “Decision Update” expected in late 2026.

-

Review the upcoming “Digital Pound Blueprint” for technical features.

-

Check if your current bank plans to offer a “Payment Interface Provider” (PIP) wallet.

-

Ensure your mobile devices are compatible with the latest biometric security standards.

-

Monitor Parliament for the introduction of the primary legislation regarding CBDC privacy.

A New Era for the Sterling Monetary System

The journey toward a Digital Pound represents the most significant update to the UK’s monetary plumbing in a generation. By focusing on privacy, stability, and ease of use, the Bank of England is attempting to build a system that combines the safety of central bank money with the convenience of modern digital finance.