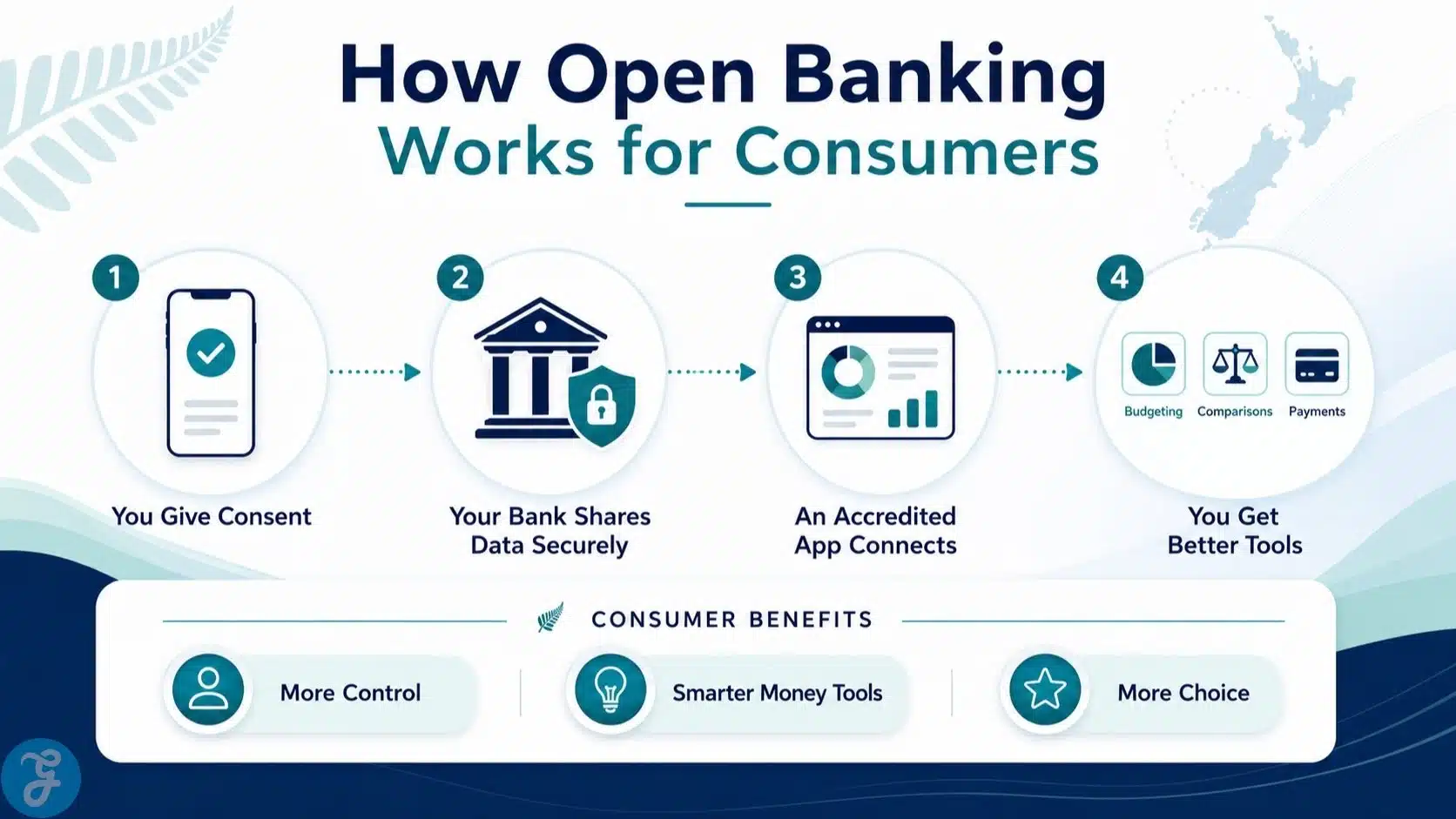

New Zealand’s banking system has often been criticised for being too concentrated, too comfortable, and not exactly famous for making consumers feel powerful. So, the country’s Open Banking Initiative matters because it could slowly change the balance of power. Instead of banks holding customer data behind closed doors, consumers can authorise trusted third parties to access their banking data or initiate payments on their behalf.

The progress is now real, not just policy theatre. New Zealand’s Customer and Product Data Act 2025 created the legal foundation for a Consumer Data Right, and banking became the first designated sector from 1 December 2025. MBIE says the banking regulations explain how the Consumer Data Right applies to banking to deliver regulated open banking, while Payments NZ says the Act creates a legal right for customers to access and share their data or authorise payments.

Our Selection Criteria

To keep this guide consumer-focused, the facts below are not just about technical APIs or regulatory acronyms. The aim is to explain what is actually changing for everyday New Zealanders.

Here is the selection logic used for this guide.

| Selection Factor | Why It Matters |

|---|---|

| Consumer Control | Open banking only matters if customers can control their own data |

| Bank Readiness | Consumers need major banks connected before services become useful |

| Payment Use Cases | Payments are one of the most practical early benefits |

| Data Sharing | Secure account data access can power budgeting, lending, and comparison tools |

| Regulation | Legal backing gives consumers and fintechs more confidence |

| Competition | Open banking may pressure banks to improve pricing and services |

| Security | Consent, accreditation, and standards are essential |

| Fintech Participation | Consumers benefit only when useful third-party apps enter the market |

This is especially important because New Zealand’s open banking rollout has moved from voluntary industry work into a regulated framework. The difference matters. Voluntary progress can be slow. Regulation gives the system teeth.

10 Things Every Reader Must Know About New Zealand’s Open Banking Initiative

New Zealand’s open banking journey is no longer just about future promise. The foundations are now in place, but consumer benefits will depend on adoption, bank readiness, fintech participation, and trust.

1. Open Banking Officially Entered Its Regulated Phase In December 2025

The biggest progress point is that open banking is no longer only an industry-led experiment. MBIE announced that open banking regulations came into force on 1 December 2025, setting out which banks are designated and how open banking will be phased in.

This matters because consumers need legal rights, not vague promises. The regulated framework sits under New Zealand’s Consumer Data Right, which is designed to let customers securely share data and authorise actions such as payments.

Best For:

- Consumers who want more control over their banking data

- Readers trying to understand why December 2025 was a major milestone

Why We Chose It:

- It marks the shift from voluntary progress to formal regulation

- It gives consumers a legal foundation for data sharing

- It creates clearer responsibilities for banks and third parties

- It starts New Zealand’s broader Consumer Data Right journey

Things To Consider:

- Regulation has started, but consumer-facing products will still develop over time

- The benefits depend on banks, fintechs, and accredited requestors actually connecting well

2. The Four Largest Banks Were First In Line

The first banks required to have open banking systems ready from 1 December 2025 were ANZ, ASB, BNZ, and Westpac. MBIE’s implementation timeline says these four banks were required from that date, while Kiwibank has a later phased schedule.

This is practical because the largest banks cover a major share of consumer banking relationships in New Zealand. If open banking had launched only with small providers, the average customer might barely notice. Starting with the big four makes the system more relevant from day one.

Best For:

- Customers of ANZ, ASB, BNZ, and Westpac

- Consumers waiting for real open banking coverage

Why We Chose It:

- The largest banks have the biggest consumer reach

- Early big-bank participation makes the ecosystem more useful

- It gives fintechs access to a larger potential customer base

- It supports competition by opening data from dominant players

Things To Consider:

- Readiness does not automatically mean every app works perfectly immediately

- Consumers still need approved third-party services to make use of the infrastructure

3. Kiwibank Is Following On A Separate Timeline

Kiwibank is not on the exact same timeline as the big four. MBIE says Kiwibank is required to have open banking systems ready from June 2026 for payment services and from December 2026 for other open banking services.

That matters because Kiwibank is often discussed in New Zealand’s banking competition debate. If open banking is meant to increase competition and consumer choice, Kiwibank’s participation will be important, even if it arrives in stages.

Best For:

- Kiwibank customers

- Readers tracking phased open banking rollout

Why We Chose It:

- It clarifies that not all banks entered at the same time

- Kiwibank’s participation broadens consumer coverage

- The phased approach separates payment services from other data services

- It shows that open banking is still a rollout, not a one-day switch

Things To Consider:

- Kiwibank customers may need to wait longer for full functionality

- Other banks and deposit-takers can voluntarily opt in, but coverage may vary

New Zealand’s open banking model is not only about viewing account data in another app. Payments NZ says the Customer and Product Data Act creates a legal right for customers to access and share their data or authorise payments.

That is a major distinction. Data sharing can support budgeting apps, loan applications, financial dashboards, and product comparison tools. Payment initiation can support faster, account-to-account payments without relying only on cards. For consumers and businesses, that could mean more choice in how money moves.

Best For:

- Consumers using budgeting or personal finance apps

- Small businesses looking for alternative payment methods

Why We Chose It:

- It explains the two main consumer functions: data and payments

- Payment initiation can create practical everyday use cases

- Data access can improve financial insights and product comparison

- It moves banking from closed systems toward consumer-directed access

Things To Consider:

- Consumers must understand what they are authorising

- Payment and data-sharing services should only be used through trusted, accredited providers

5. Payments NZ’s API Centre Is The Technical Backbone

The Payments NZ API Centre has been central to building the standards and protocols for open banking in Aotearoa New Zealand. The API Centre says it is working with banks and the tech community to create open banking standards and protocols that enable fast, secure, user-friendly data sharing.

This is important because open banking cannot run on good intentions and vibes. Banks and fintechs need common technical standards, security profiles, testing, and implementation rules. Without standards, every fintech would need a different connection to every bank, which would be expensive, slow, and messy.

Best For:

- Fintech builders and banking technology readers

- Consumers wondering how apps connect securely

Why We Chose It:

- Shared standards reduce integration complexity

- The API Centre helps align banks and third parties

- Standardisation supports better security and reliability

- It creates a foundation for more consumer-facing innovation

Things To Consider:

- Standards still need adoption by banks and third parties

- Technical readiness is only one part of the consumer experience

6. The Implementation Plan Has Concrete Bank Deadlines

Payments NZ’s updated Minimum Open Banking Implementation Plan gave specific readiness deadlines for major banks. Under the updated plan, ANZ, ASB, BNZ, and Westpac needed to be ready by 30 May 2025 with the API Centre’s v2.3 Payment Initiation standard and by 28 November 2025 with the v2.3 Account Information standard.

This matters because deadlines create pressure. Without them, open banking can become one of those projects everyone supports in principle while moving at the speed of a sleepy glacier.

Best For:

- Readers tracking real rollout progress

- Fintechs planning integrations with major banks

Why We Chose It:

- It shows the rollout had concrete technical milestones

- Payment initiation and account information were both prioritised

- The plan focused on the largest banks first

- Deadlines help turn policy into infrastructure

Things To Consider:

- Readiness dates do not guarantee instant mass consumer adoption

- Product quality depends on both bank APIs and third-party implementation

7. Open Banking Is Part Of A Bigger Consumer Data Right

The banking rollout is only the first step. MBIE says banking is the first sector included in New Zealand’s Consumer Data Right, enabling open banking from 1 December 2025. The banking regulations include customer data and allow payments as designated actions.

This means the Open Banking Initiative is part of a wider data-rights model. Over time, the same concept could extend into other sectors, letting consumers move and use their data more easily across the economy.

Best For:

- Readers interested in consumer rights and digital regulation

- Businesses watching future data-sharing rules

Why We Chose It:

- It places open banking inside a broader policy framework

- Banking is the first use case, not necessarily the last

- Consumer data rights can support innovation across sectors

- It shows New Zealand is building a long-term data-sharing system

Things To Consider:

- Expansion into other sectors will take time

- Consumer education will be essential as data sharing becomes more common

8. The Main Consumer Promise Is More Competition

New Zealand’s banking sector has faced criticism for limited competition. Reuters reported in 2024 that the government promised a banking shake-up after the Commerce Commission found the personal banking sector lacked competition, with the four largest banks dominating the market. The same report noted that open banking was seen as having strong potential to promote disruptive competition over the medium to long term.

For consumers, this is the big prize. Open banking could make it easier for fintechs to offer budgeting tools, smarter lending assessments, account comparisons, payment alternatives, and switching support. In theory, banks may have to compete harder when customers can move their data more easily.

Best For:

- Consumers are frustrated by limited banking competition

- Readers studying fintech and market reform

Why We Chose It:

- Competition is one of the strongest policy reasons for open banking

- Data portability can reduce bank lock-in

- Fintechs can build services on top of bank data

- Better comparison and payment tools may pressure incumbents

Things To Consider:

- Competition gains will not appear overnight

- Consumers need easy, trusted products before open banking changes behaviour at scale

9. Consumer Trust Will Decide Adoption

Open banking only works if people trust it. Consumers are being asked to let approved third parties access sensitive financial data or initiate payments. Even with regulation and standards, many people will naturally ask: “Is this safe?” That is not paranoia. That is adulthood.

MBIE’s framework includes accreditation, standards, and regulated roles, while industry updates from legal firms noted that applications to become an Accredited Requestor opened from 1 December 2025. Consumer-facing guidance was expected to follow during 2026 as the framework became more established.

Best For:

- Consumers worried about privacy and security

- Fintechs building trust-based products

Why We Chose It:

- Trust is essential for adoption

- Accreditation helps separate legitimate participants from risky actors

- Clear consent flows will matter for consumer confidence

- Security messaging must be simple, not buried in legal fog

Things To Consider:

- Consumers should understand permissions before approving access

- Poorly designed consent screens could damage trust in the whole system

10. The Real Test Is Whether Consumers See Useful Products

Regulation and APIs are important, but consumers will judge open banking by usefulness. Can it help them budget better? Switch banks more easily? Get a better loan? Pay a merchant without card fees? See all accounts in one place? Avoid overdraft surprises? Compare offers without manually uploading bank statements?

Payments NZ lists participating API providers and third parties in the secure open banking ecosystem, showing that the market is building beyond banks alone. Some third parties already have API services agreements with providers and apps or services in market or near market.

Best For:

- Consumers waiting for practical open banking tools

- Fintech companies building consumer-facing services

Why We Chose It:

- Open banking succeeds only when services become useful

- Third-party participation drives innovation

- Consumers need clear benefits, not technical explanations

- Real adoption will depend on simple, trustworthy experiences

Things To Consider:

- Early services may feel limited while the ecosystem matures

- Consumers should compare fees, permissions, and support before using third-party apps

An Overview Of 10 Facts About New Zealand’s Open Banking Initiative

New Zealand’s open banking system has moved from planning into regulated rollout. The foundations are in place, but consumer impact will build gradually as banks connect, fintechs launch better tools, and customers become comfortable with secure data sharing.

Overview Comparison

Here is a quick way to understand the most important moving parts.

| Fact | What It Means For Consumers | Status |

|---|---|---|

| 1 | Open banking is now regulated | Started 1 December 2025 |

| 2 | Big four banks came first | ANZ, ASB, BNZ, Westpac required from launch |

| 3 | Kiwibank follows later | Payments from June 2026, wider services from December 2026 |

| 4 | Data and payments are included | Customers can share data and authorise payments |

| 5 | API Centre sets standards | Common technical rules support secure connections |

| 6 | Deadlines were set | Major bank readiness milestones in 2025 |

| 7 | It sits inside Consumer Data Right | Banking is the first designated sector |

| 8 | Competition is the policy goal | More fintech choice and less bank lock-in |

| 9 | Trust is the adoption test | Accreditation, consent, and security matter |

| 10 | Useful apps will decide success | Consumers need practical benefits |

Our Top 3 Picks And Why?

Three points matter most for ordinary consumers.

| Key Point | Why It Stands Out |

|---|---|

| Consumer Control | Open banking gives customers more say over how their banking data is used |

| Payment Initiation | It could create cheaper, easier account-to-account payment options |

| Competition | It may push banks and fintechs to offer better products and services |

These three explain why open banking is not just a technical reform. It is a consumer-power reform.

How To Understand The Open Banking Initiative By Yourself

The easiest way to understand open banking is to think of it as permission-based banking access. Your bank still holds your account, but you can authorise another approved service to access your data or initiate certain actions.

The Selection Framework:

- Check Whether Your Bank Is Covered: ANZ, ASB, BNZ, and Westpac were first; Kiwibank follows in stages.

- Understand What You Are Sharing: Know whether you are sharing account information, transaction data, or payment permission.

- Use Trusted Providers: Look for accredited or recognised third-party services.

- Focus On Real Benefits: Budgeting, payments, lending, comparisons, and switching tools should make life easier.

The Final Checklist

Before using an open banking service, consumers should ask five questions.

- Is this provider accredited or clearly authorised?

- What data am I giving access to?

- Can the provider initiate payments or only view data?

- How do I withdraw consent?

- What benefit am I getting in return?

The Bigger Consumer Lesson From New Zealand’s Open Banking Rollout

New Zealand’s open banking progress is meaningful because it gives consumers something banks do not always rush to hand over: control. For years, customer data has helped banks understand, price, and retain customers. Open banking gives consumers a way to use that same data for their own benefit.

Still, the uncomfortable truth is that the Open Banking Initiative will not magically fix banking competition by itself. APIs do not automatically create better products. Regulation does not automatically create trust. A legal right does not automatically make consumers change behaviour. The system still needs clear apps, safe consent flows, visible value, strong enforcement, and enough fintech competition to make banks nervous in a productive way.

The future looks promising, but gradual. The first phase is about infrastructure. The second phase is about useful services. The third phase, if New Zealand gets it right, is about consumers finally having more leverage in a banking market that has needed stronger competition for a long time.

Frequently Asked Questions (FAQs) About The Open Banking Initiative

What Is New Zealand’s Open Banking Initiative?

New Zealand’s Open Banking Initiative lets customers securely share banking data or authorise payments through approved third parties under the Consumer Data Right framework. Banking became the first designated sector from 1 December 2025.

Which Banks Are Included First?

ANZ, ASB, BNZ, and Westpac were required to have open banking systems ready from 1 December 2025. Kiwibank follows in stages, with payment services from June 2026 and other services from December 2026.

How Does Open Banking Help Consumers?

It can help consumers use budgeting apps, compare financial products, share data for lending, make account-to-account payments, and access more personalised financial services. The real benefits depend on the quality of third-party apps.

Is Open Banking Safe?

It is designed to be safer than screen scraping because it uses regulated access, standards, and consent-based data sharing. Consumers should still use only trusted providers and check exactly what permissions they approve.

Will Open Banking Make Banks Cheaper?

Not immediately, but it could increase competition over time. If fintechs and banks use consumer-permissioned data to offer better comparisons, payments, lending, and