Splitting purchases into four smaller installments makes checkout feel effortless. This convenience explains the explosive popularity of Buy Now Pay Later Services. While these short-term loans temporarily ease cash flow, missed payments quickly escalate into late fees, overdrafts, or collections.

Understanding the mechanics behind these financial tools is critical for consumers in the United States. Federal oversight by the Consumer Financial Protection Bureau aims to establish clearer industry standards, but borrowers must always remain cautious. Utilizing these payment plans can directly impact credit scores, making it essential to fully weigh the risks. In many situations, relying on traditional credit cards or establishing a dedicated savings plan offers a safer, more sustainable alternative for managing purchases without facing unexpected financial penalties.

What Is Buy Now, Pay Later (BNPL)?

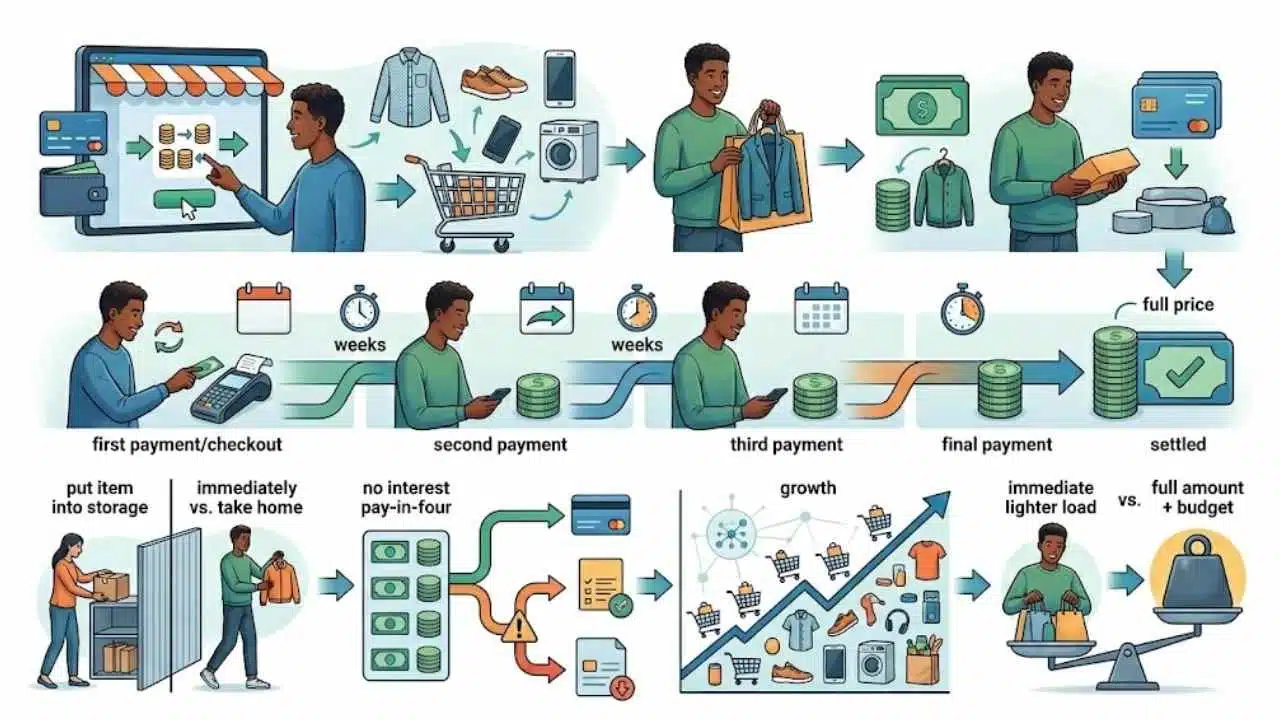

Buy Now, Pay Later (BNPL) is a type of short-term installment loan that allows consumers to make immediate purchases and divide the cost into smaller, scheduled payments. Integrated directly at the point of sale, these services offer a frictionless alternative to traditional credit cards by breaking larger expenses into manageable pieces.

Buy now, pay later is a short-term loan at checkout

Buy now, pay later plans let you take the item home right away and split the cost into installments. In the most common pay-in-four setup, you pay about 25% up front and then make three more payments every two weeks, which usually means the balance is gone in about six weeks.

In its January 2025 report, the Consumer Financial Protection Bureau said 21% of consumers with a credit record used BNPL at least once in 2022 across six large providers, and the median purchase amount was $108. That matters because it shows BNPL is often used for everyday retail spending, not just one big emergency purchase.

- It is not layaway: you get the product now, and the debt starts now.

- It is not always a credit card: many pay-in-four loans have no interest, but they can still charge late fees or send debt to collections.

- It is not always private forever: most pay-in-four plans have stayed off traditional credit files, but reporting rules are changing.

BNPL feels small at checkout, but your budget still has to absorb the full price.

BNPL also grew fast during and after the COVID-19 pandemic, when online checkout tools became more common and merchants pushed faster payment options. That convenience is real, but it works best when you already know exactly how the full balance will be covered.

How Does Buy Now, Pay Later Work?

At checkout, you choose a BNPL option instead of paying the whole bill at once. The provider reviews basic information, often gives a decision in seconds, takes the first payment, and schedules the rest automatically.

- You pick the plan at online checkout or in store.

- The provider reviews your application, usually with a soft credit check for pay-in-four plans.

- You make the first payment right away.

- The remaining payments are auto-debited from your card or bank account on the dates in the agreement.

A practical tip: always check whether you are choosing a true pay-in-four plan or a longer monthly financing offer. Many providers now show both, and the longer version can bring interest, hard credit checks, or a very different refund process.

Popular BNPL platforms

The big names often look similar on the surface, but the small details can change what the plan costs you and how it affects your credit.

| Provider | Common setup | What matters most |

|---|---|---|

| Affirm | Pay in 4 with four interest-free payments every two weeks | Affirm says its Pay in 4 option has no late or hidden fees, which makes it easier to budget if you pay on time. |

| Cash App Afterpay | Four payments over six weeks | U.S. shoppers can be charged up to $8 per missed installment, and total late fees on one order are capped at 25% of the order value. |

| Klarna | Pay in 4 with automatic biweekly payments | Klarna markets pay-in-four as interest-free, but you still need to confirm whether checkout is offering pay in 4, pay later, or a longer monthly loan. |

| PayPal Pay in 4 | Four interest-free payments | PayPal lists Pay in 4 for purchases from $30 to $1,500, with the first payment due at purchase and no late fees. |

| Splitit | Installments charged against your existing credit card | Splitit does not add its own fees in the standard setup, but it uses your available credit limit, so your regular credit card terms still matter. |

| Sezzle | Standard split-pay plans, plus optional longer financing in some cases | Sezzle can charge fees for late, failed, or rescheduled payments, and its Sezzle Up feature can report payment history if you enroll. |

If you use more than one app, make your own master list of due dates. Each provider makes its own dashboard look simple, but your checking account sees the combined total.

The Benefits of Buy Now, Pay Later Services

BNPL is popular for a reason. When the plan is short, clear, and already fits your budget, it can be a useful payment tool.

Interest-free payments

The biggest draw is simple: many pay-in-four plans charge no interest if you stay on schedule. That can be cheaper than carrying the same purchase on a credit card, especially because the Federal Reserve reported that credit card accounts assessed interest averaged 21.52% APR in February 2026.

The CFPB’s December 2025 market update found the average BNPL loan size was $135 in 2023. For a small retail purchase that you could pay off within six weeks anyway, splitting it up can ease timing pressure without adding interest.

Flexible repayment terms

Flexibility is the other big benefit. The CFPB reported that the six large firms in its 2025 market review served a combined 53.6 million users in 2023, and the average user took 6.3 BNPL loans per lender during the year, which shows how easy it is to reuse the tool.

That is helpful only if you stay deliberate. A good use case is a planned purchase that lands a few days before payday, not a cart full of things you would not buy if full payment were required today.

- Good fit for a planned, one-time purchase with a short payoff window

- Good fit when the total cost is already in your monthly budget

- Bad fit for routine bills, groceries, or anything that depends on next month being easier

Convenience for online and in-store shopping

BNPL is built for speed. You can often use it online, in an app, or at the register without filling out a long loan application.

That convenience can help with cash flow, but it also removes friction that used to stop impulse spending. The best way to keep the convenience and cut the risk is to check one thing before you tap pay: do the due dates line up with your paycheck dates?

The Risks of Buy Now, Pay Later Services

BNPL can solve a timing problem, but it can also hide a budget problem. That is why the risks deserve just as much attention as the perks.

Overspending and poor budgeting

In a January 2025 report, the CFPB found that 63% of BNPL borrowers had multiple simultaneous loans at some point in 2022, and 33% had simultaneous loans across multiple firms. That is the clearest warning sign in this market: the danger is rarely one plan, it is stacking several at once.

A 2024 Federal Reserve Bank of Boston paper by Joanna Stavins found BNPL users were much more likely to revolve credit card balances, had lower checking account balances, and were more likely to report a recent bankruptcy filing. If BNPL is becoming your regular fix for a tight month, that is a cue to step back before short-term debt turns into real financial fragility.

Missed payments and late fees

The Federal Reserve’s 2025 household survey found that 26% of BNPL users were late on a payment in the prior 12 months. Of those who paid late, 64% said they were charged extra.

The same survey found that 11% of BNPL users had a payment trigger an overdraft or non-sufficient funds fee from their bank. So the true cost of a missed payment is often bigger than the late fee shown in the app.

- Set payments for the day after payday, not the day before rent is due

- Use one bank account for BNPL payments so you can watch the cash flow clearly

- Turn off the plan if the next payment depends on overtime, a tax refund, or wishful thinking

Limited consumer protections

BNPL protections have improved, but they are still uneven. In May 2024, the Consumer Financial Protection Bureau said many BNPL lenders must provide key credit-card-like rights, including the right to dispute charges and seek refunds after a return.

That helps, but it does not make every BNPL plan equal to a credit card. Return windows, billing disputes, buyer protection, and reporting practices still vary by lender and by product, so keep your receipts, return confirmations, and payment screenshots until the account shows a zero balance.

If the return is messy, the paper trail matters more than the checkout promise.

How BNPL Affects Your Credit

For years, one of the odd things about BNPL was that it could be easy to get, easy to miss, and hard to see on a traditional credit report. That is starting to change, but it is still inconsistent.

Impact on credit scores

The CFPB says most pay-in-four BNPL products do not report payment history to the major credit bureaus. That means on-time payments often do not help your credit score in the same way a well-managed credit card or installment loan can.

But missed payments can still hurt you if the debt goes to collections. TransUnion also says BNPL information it receives is currently visible to you on your credit file, though scoring providers, lenders, and insurers generally cannot use that data yet.

FICO added BNPL-specific versions of FICO Score 10 and FICO Score 10 T in June 2025, which means BNPL data can matter more as lenders adopt newer scoring models. So the old rule, that BNPL never affects credit, is no longer safe to assume.

Reporting inconsistencies across providers

Provider rules now differ enough that you should check them before every purchase, even if you have used the same app before. A pay-in-four offer and a longer monthly financing offer from the same brand may be treated very differently.

| Question to check | Why it matters |

|---|---|

| Will this loan be reported to a credit bureau? | On-time payments may help build history in some cases, and late payments may become more visible over time. |

| Is approval based on a soft or hard inquiry? | A soft inquiry usually does not affect your score, while a hard inquiry can. |

| Could missed debt be sent to collections? | That is where a short-term checkout decision can become a real credit problem. |

| Is this pay in four or longer monthly financing? | Longer plans are more likely to carry APR, formal underwriting, and regular credit reporting. |

As of April 1, 2025, Affirm says it reports all of its pay-over-time loan products issued from that date to Experian, including Pay in 4. Afterpay says its U.S. Pay in 4 product does not currently report to credit bureaus, while Sezzle Up reports only if you choose to enroll.

Tips for Using BNPL Responsibly

If you decide to use BNPL, a few simple habits can do most of the heavy lifting. The goal is to make the plan boring, predictable, and easy to finish.

Set a budget before using BNPL

Run one test before every purchase: if the store removed BNPL at checkout, would you still buy the item this month? If the answer is no, wait.

The Federal Reserve’s 2025 survey found that 31% of BNPL users said their main reason was to spread out payments, while 29% said it was the only way they could afford the purchase. If it is the only way you can afford it, that is a warning, not a green light.

Limit the number of active BNPL loans

Keep active plans to one or two at most. That single rule solves a lot of the confusion that leads to late payments.

The CFPB’s loan-stacking data shows why this matters. Once you juggle several plans across apps, it becomes easy to forget a debit date, underestimate what is still owed, or think a new purchase is manageable because each installment looks small by itself.

Always read the terms and conditions

Do not skim the fine print. Read the payment dates, late fee policy, return rules, and credit reporting language before you approve the plan.

- Check the exact due dates

- Check whether autopay pulls from a card or bank account

- Check the late fee amount and any grace period

- Check whether the provider may report to credit bureaus or collections

- Check how refunds and disputes are handled

If any of those answers are hard to find, stop and pay another way. A loan that is easy to take should also be easy to understand.

Alternatives to Buy Now, Pay Later Services

You do not have to choose between paying everything today and using BNPL. In many cases, a regular credit card or a savings plan gives you more control.

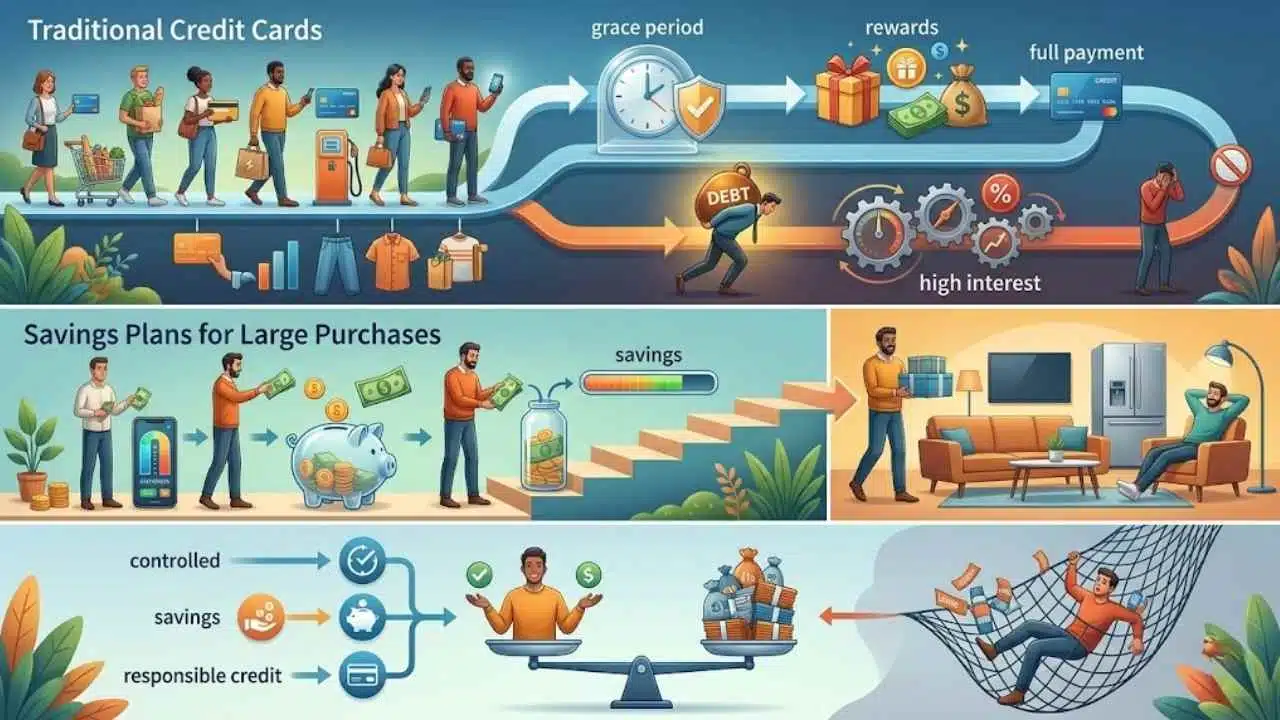

Traditional credit cards

A credit card can be cheaper than BNPL if you pay the statement balance in full by the due date, because the grace period can mean zero interest. You also usually get stronger chargeback rights, clearer billing rules, and in some cases rewards.

The catch is what happens if you carry the balance. The Federal Reserve’s February 2026 data shows average APR on credit card accounts assessed interest at 21.52%, so a card is a solid tool for convenience and consumer protection, but a very expensive tool for long-running debt.

Savings plans for large purchases

A savings plan is slower, but it is the cleanest option for a big purchase you can see coming. You avoid late fees, avoid credit surprises, and buy only when the money is truly there.

As of May 18, 2026, the FDIC listed the national average savings rate at 0.38%, which is a good reminder to shop for a better savings account if you go this route. Even then, the real win is not the interest, it is that saving first keeps a future purchase from becoming future stress.

| Option | Best use | Main upside | Main trade-off |

|---|---|---|---|

| BNPL pay in four | Small planned purchase you can clear in six weeks | Often 0% interest if paid on time | Late fees, overdraft risk, and easy loan stacking |

| Credit card paid in full | Everyday spending with discipline | Grace period, rewards, and stronger consumer protection | Gets expensive fast if you carry the balance |

| Credit card with carried balance | Short emergency only | Flexible repayment | High APR can outcost BNPL in a hurry |

| Savings plan | Large purchase you can delay | No debt and no late fees | You have to wait |

Final Thoughts

Buy now, pay later can be useful when the purchase is modest, the payoff window is short, and the full amount already fits inside your budget. Used that way, it is a timing tool, not a rescue plan.

The trouble starts when several payment plans overlap, due dates sneak up on you, or the purchase only works if next month is somehow better. That is where late fees, overdrafts, credit issues, and real stress begin to pile up.

Before you tap pay, compare the BNPL offer with a credit card you can pay off in full or a simple savings plan. Read the terms, track the dates, and keep buy now, pay later as an occasional tool, not a habit.

Frequently Asked Questions (FAQs) About Buy Now, Pay Later Services

1. What is buy now pay later?

Buy now pay later, or BNPL, splits a purchase into small installments. Shops offer it at checkout, so you pay over weeks or months.

2. Are there fees or interest?

Many BNPL plans charge no interest if you pay on time, but some add fees or interest for longer terms. Late fees can hit your wallet, so watch the repayment dates.

3. Will BNPL hurt my credit score?

Usually, on-time payments do not hurt your credit score, but missed payments can lower it. Some providers run a soft approval check, and some report to credit bureaus, so read the terms.

4. Is BNPL right for me?

It can help with budgeting for a big buy, but treat it like cash you owe. Read the fine print on fees, repayment, and consumer protection, and pick a plan that fits your personal finance goals.