The transition into the 2025 tax year represents one of the most significant shifts in how the United States government monitors digital asset transactions. With the introduction of new reporting forms and refined definitions of “broker,” taxpayers must adopt a more rigorous approach to record-keeping to remain compliant.

How We Selected Our 9 Best IRS Crypto Reporting Rules Tips

To compile these essential tips, we reviewed the latest IRS publications, including the instructions for the draft Form 1099-DA and recent revenue rulings regarding digital asset custody. Our selection criteria focused on the changes with the highest impact on individual filers, specifically targeting areas where new automated reporting might conflict with traditional manual tracking methods.

The Most Critical 9 IRS Crypto Reporting Rules for the 2025 Tax Year

Staying ahead of federal requirements is the only way to avoid unnecessary audits and penalties. The following tips cover the essential updates every digital asset holder should understand before the next filing season.

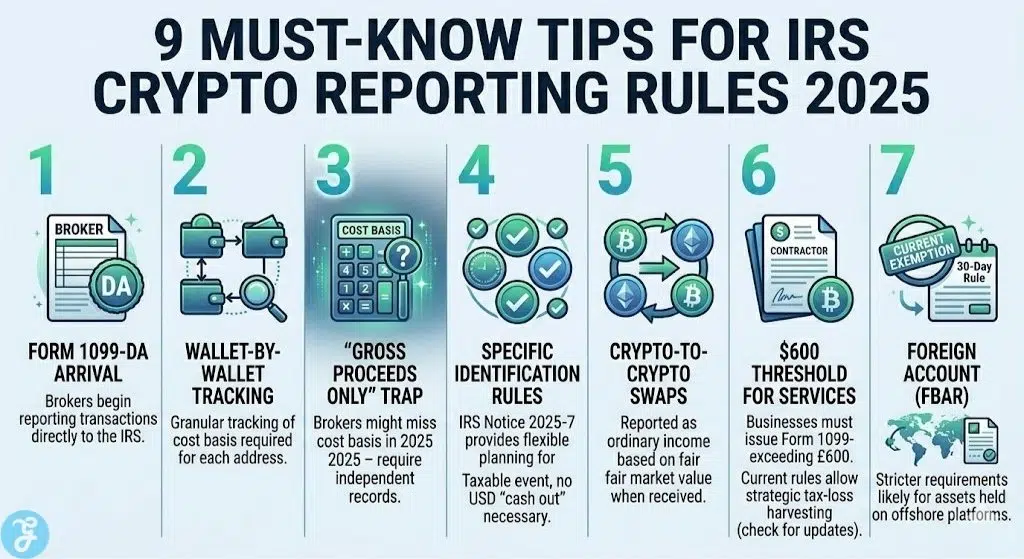

1. The Arrival of Form 1099-DA

Starting in 2025, centralized exchanges and certain hosted wallet providers will begin issuing Form 1099-DA. This dedicated form will report gross proceeds from sales and exchanges directly to the IRS, marking the end of the “self-reporting only” era for many users.

-

Best for: Simplifying the initial data entry for high-volume traders.

-

Why We Chose It:

-

It creates a formal paper trail that matches IRS records.

-

It reduces the likelihood of “missing” transactions on your return.

-

It forces a higher level of accountability for major US-based exchanges.

-

-

Things to consider: Not all international or decentralised platforms will issue this form, leading to potential reporting gaps.

2. Wallet-by-Wallet Cost Basis

The IRS has moved toward a more granular approach to cost basis tracking. Instead of averaging your purchase price across all your holdings, the IRS Crypto Reporting Rules now lean toward tracking the specific basis within each individual wallet or account.

-

Best for: Investors with complex portfolios across multiple hardware and software wallets.

-

Why We Chose It:

-

It prevents “basis bleeding” between long-term and short-term holdings.

-

It aligns with the technical reality of how tokens are stored on-chain.

-

It provides more accurate data during a potential manual audit.

-

-

Things to consider: This requires significantly more detailed record-keeping compared to simple aggregate tracking.

3. The “Gross Proceeds Only” Trap

A major point of confusion for 2025 is that while brokers must report gross proceeds, they are not yet strictly required to report the cost basis for all assets. This means your 1099-DA might show a massive “sale” without showing what you originally paid for the asset.

-

Best for: Avoiding overpayment of taxes on transactions where the basis is unknown to the broker.

-

Why We Chose It:

-

It highlights the need for independent tax software or manual spreadsheets.

-

It protects taxpayers from being taxed on the full sale price as pure profit.

-

It underscores the transitionary nature of the 2025 reporting cycle.

-

-

Things to consider: You will be responsible for proving your cost basis if the broker reports it as “zero” or “unknown.”

4. Specific Identification Relief (Notice 2025-7)

The IRS has provided temporary relief regarding how you identify which specific coins were sold. Under Notice 2025-7, taxpayers have more flexibility in choosing which “lots” to sell, provided they can provide a reasonable technical trail of the transaction.

-

Best for: Strategic tax planning and minimizing capital gains hits.

-

Why We Chose It:

-

It allows for more efficient tax-loss harvesting within a single year.

-

It acknowledges the technical difficulty of identifying specific “UTXOs” or tokens.

-

It provides a “safe harbour” for those making a good-faith effort to report correctly.

-

-

Things to consider: This relief is temporary and may be tightened in future tax years.

5. Reporting Crypto-to-Crypto Swaps

Many users still believe that taxes are only due when they “cash out” to a bank account. However, the IRS Crypto Reporting Rules clearly state that swapping one token for another (e.g., BTC to ETH) is a taxable event based on the fair market value at the time of the swap.

-

Best for: Day traders and DeFi participants who frequently rotate their positions.

-

Why We Chose It:

-

It is one of the most common areas where taxpayers inadvertently trigger a penalty.

-

It ensures that gains are captured even if they remain within the “crypto ecosystem.”

-

It aligns crypto trading with traditional “like-kind” exchange rules for securities.

-

-

Things to consider: Calculating the USD value for thousands of micro-swaps on DeFi can be incredibly difficult without automated tools.

6. Reporting Staking and Airdrop Income

Income generated through staking or received via an airdrop must be reported as ordinary income. The value is determined by the token’s price at the exact moment you have “dominion and control” over the funds.

-

Best for: Passive income seekers and early adopters of new protocols.

-

Why We Chose It:

-

It differentiates between capital gains (growth) and ordinary income (earnings).

-

It clarifies the timing of when the tax liability is actually triggered.

-

It mirrors how interest or dividends are treated in traditional banking.

-

-

Things to consider: If the token price crashes after you receive it, you may still owe tax based on its initial higher value.

7. The $600 Threshold for Services

If you are a freelancer or business owner paying for services in cryptocurrency, the $600 threshold applies just as it does with USD. You are required to collect a W-9 and issue a Form 1099-NEC if the total value of the crypto sent exceeds this limit in a calendar year.

-

Best for: Small business owners and independent contractors.

-

Why We Chose It:

-

It integrates digital assets into the broader “gig economy” tax framework.

-

It provides the IRS with a way to track non-wage business expenses.

-

It protects businesses from losing their tax deductions for labour costs.

-

-

Things to consider: You must track the USD value of the payment at the time of transfer, not at the end of the year.

8. Wash Sale Rule Exemptions (For Now)

Currently, the “Wash Sale Rule”—which prevents investors from claiming a loss if they buy the same asset back within 30 days—does not technically apply to digital assets because they are classified as property, not securities.

-

Best for: Investors looking to lower their tax bill during a market downturn.

-

Why We Chose It:

-

It allows for “aggressive” tax-loss harvesting that isn’t possible with stocks.

-

It provides a significant strategic advantage during volatile market periods.

-

It represents a rare “loophole” that hasn’t been closed by Congress yet.

-

-

Things to consider: This could change at any moment through new legislation, so keep a close watch on late-year updates.

9. Foreign Account Reporting (FBAR/FATCA)

If you hold more than $10,000 across foreign crypto exchanges at any point in the year, you may be required to file an FBAR (FinCEN Form 114). While the rules are still being refined for digital assets, the IRS has signalled increased interest in offshore holdings.

-

Best for: Users of major international exchanges like Binance or Bybit.

-

Why We Chose It:

-

The penalties for non-disclosure of foreign accounts are exceptionally high.

-

It reflects the global nature of the digital asset market.

-

It prepares users for the eventual “full disclosure” requirements.

-

-

Things to consider: Determining if a decentralised protocol counts as “foreign” is still a legal grey area.

An Overview Of X IRS Crypto Reporting Rules And Compliance Trends

The complexity of these rules underscores the importance of staying organised throughout the year. As the IRS gains better data from exchanges, the margin for error for individual filers continues to shrink.

Overview Comparison Table

Before filing, it is vital to understand which events trigger different types of tax liability.

| Transaction Type | Tax Classification | Reporting Requirement |

| Selling Crypto for USD | Capital Gain/Loss | Form 8949 / 1099-DA |

| Swapping BTC for ETH | Capital Gain/Loss | Form 8949 |

| Receiving Staking Rewards | Ordinary Income | Schedule 1 |

| Mining New Coins | Ordinary Income | Schedule C |

Our Top 3 Picks and Why?

Of the nine tips, the Arrival of Form 1099-DA, Reporting Crypto-to-Crypto Swaps, and Wallet-by-Wallet Cost Basis are the most critical. These three represent the biggest “pain points” for the 2025 season and are the most likely to cause filing errors if overlooked.

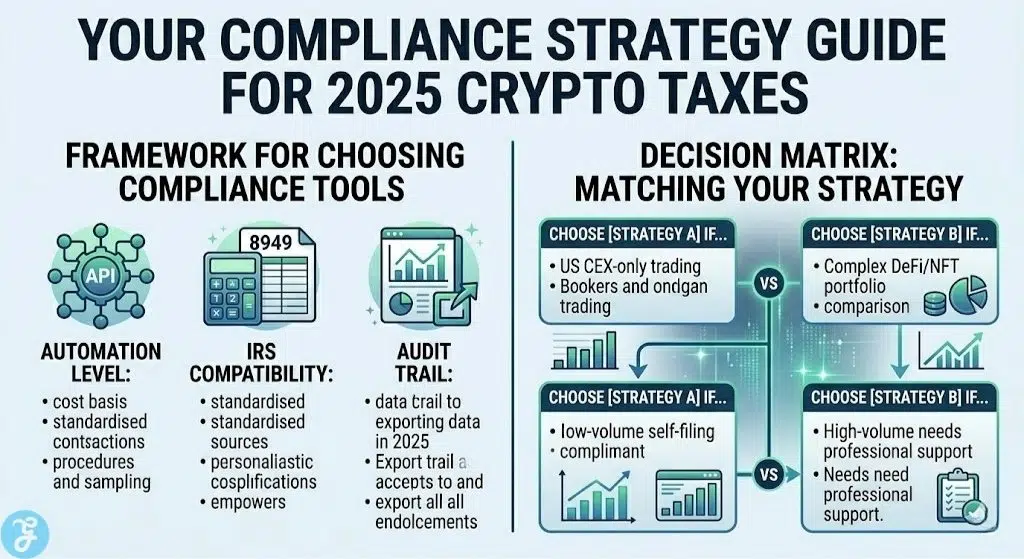

Buyer’s Guide: How to Choose the Right IRS Crypto Reporting Rules Strategy by Yourself?

Developing a personal compliance framework is the only way to manage a large volume of transactions without burning out. Use the following criteria to evaluate your current setup.

The Selection Framework:

-

Automation Level: Does your chosen software connect via API to all your wallets and exchanges?

-

IRS Compatibility: Does the tool generate a ready-to-file Form 8949?

-

Audit Trail: Can you export a line-by-line history of every transaction’s cost basis?

Decision Matrix (Table):

| Choose Software A if… | Choose Software B if… |

| You only trade on US centralised exchanges. | You interact with DeFi, bridges, and NFTs. |

| You want a free tier for low volume. | You need professional tax pro support. |

| You use a single wallet. | You manage dozens of self-custody addresses. |

The Final Checklist: 5-point Checklist Before Filing Your 2025 Taxes

-

Have you collected all your 1099-DA forms from exchanges?

-

Have you reconciled your self-custody wallet transfers to avoid “phantom” gains?

-

Have you identified any “lost” or “hacked” assets for potential casualty loss claims?

-

Did you remember to include staking rewards and airdrops as ordinary income?

-

Have you double-checked that your “cost basis” isn’t being reported as zero?

Mastering the Future of Digital Asset Taxation

The 2025 tax year is a turning point for transparency in the digital asset space. While the new IRS Crypto Reporting Rules may seem daunting, they are part of a larger movement toward legitimising cryptocurrency as a permanent fixture of the global financial system.