South Africa is not the easiest place to prove a neobank model. The country has sophisticated banks, deep income inequality, high mobile usage, cash-heavy habits, trust issues around financial services, and millions of people who still need affordable, practical banking. So when TymeBank launched in 2019 and later crossed 10 million South African customers, reached monthly profitability in December 2023, and helped Tyme Group achieve unicorn status after a $250 million Series D round in 2024, it did more than build another banking app. It proved that Neobanks In South Africa can work if they are built for the real market, not for a fintech fantasy boardroom.

The important word here is “real.” South African banking is not just about downloading an app and feeling modern. People need low fees, easy onboarding, cash-in and cash-out access, grocery-store convenience, trust, savings tools, credit options, and help when something goes wrong. TymeBank’s lesson is simple but powerful: digital banking succeeds when it stops pretending physical life does not exist.

Our Selection Criteria

To understand why TymeBank worked, we need to look beyond customer numbers. A neobank can acquire users quickly and still fail if those customers do not transact, save, borrow, trust the platform, or stay active.

Here is the practical filter used for this guide.

| Selection Factor | Why It Matters |

|---|---|

| Customer Growth | Scale proves market demand and distribution strength |

| Profitability | Most neobanks globally struggle to become profitable |

| Local Market Fit | South Africa needs hybrid access, not app-only theory |

| Retail Partnerships | Physical touchpoints reduce onboarding and trust barriers |

| Low-Fee Banking | Price matters in a cost-sensitive market |

| Financial Inclusion | The model must serve underbanked users, not only affluent digital users |

| Product Expansion | Savings, credit, insurance, and payments build deeper relationships |

| Regulatory Trust | Banking licences and compliance matter in financial services |

| Global Validation | Investor backing shows the model can travel beyond one market |

This list is written for fintech founders, banking professionals, startup investors, digital transformation teams, and readers trying to understand why TymeBank became one of the most important examples of digital banking in Africa.

Now let’s break down the 13 facts that explain why TymeBank’s rise matters.

13 Essential Facts About Neobanks In South Africa And TymeBank’s Market Proof

TymeBank did not prove that every neobank will work in South Africa. It proved something more useful: the right digital model can work when it is designed around local realities.

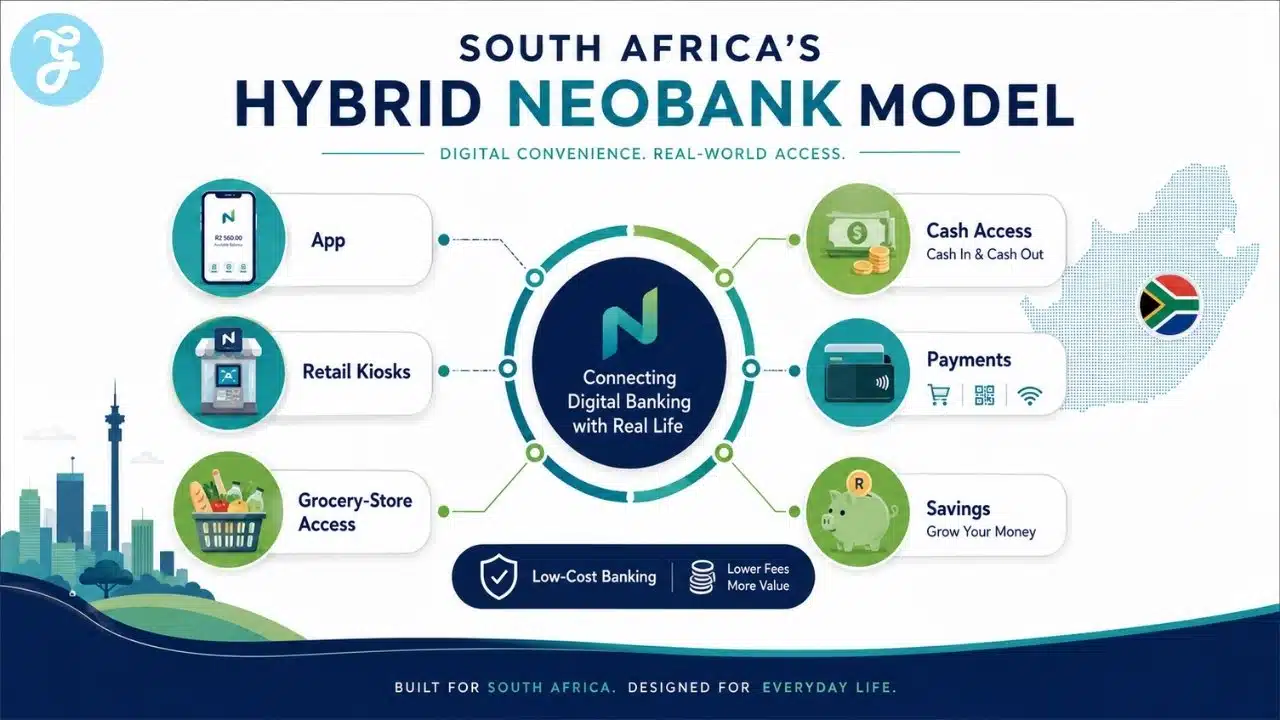

1. TymeBank Proved That Digital Banking Needed Physical Access Points

Most neobank stories begin with an app. TymeBank’s South African story began with a more practical insight: many customers still need real-world access points. The bank used kiosks in retail environments, especially through Pick n Pay and Boxer, to let customers open accounts quickly where they already shop. In 2021, TymeBank said customers could open accounts in under five minutes online, in-app, or at Pick n Pay and Boxer kiosks.

That mattered because South Africa is not a purely digital market. People may own smartphones, but they also shop in physical stores, use cash, and trust brands they encounter in daily life. The retail-kiosk model made digital banking feel less invisible and more accessible.

Best for:

- Understanding why app-only banking was not enough

- Readers studying hybrid fintech distribution

Why We Chose It:

- It explains TymeBank’s strongest early-market insight

- Retail kiosks reduced customer onboarding friction

- Physical presence helped build trust in a digital product

- The model matched how many South Africans actually live and bank

Things to consider:

- Retail partnerships can change over time

- Physical touchpoints add operational complexity compared with pure app-only models

2. The Bank Turned Grocery Stores Into Banking Infrastructure

TymeBank’s early growth was closely tied to the idea that banking should happen where people already spend time. Instead of building a traditional branch network, the bank used retail partnerships as a distribution engine. Early reporting noted that its partnership with Pick n Pay and Boxer gave it access to hundreds of physical stores across the country.

This was clever because grocery stores have frequent foot traffic, geographic spread, and consumer trust. In a market where branch access can be expensive and uneven, using retail stores as banking infrastructure gave TymeBank a cheaper and more scalable route to customers.

Best for:

- Fintech founders thinking about offline distribution

- Banks trying to lower acquisition costs

Why We Chose It:

- It shows how TymeBank avoided traditional branch economics

- Retail presence helped customers onboard in familiar spaces

- It created a practical bridge between digital banking and cash-based behavior

- It made banking part of everyday errands

Things to consider:

- Retail dependency can create strategic risk

- Neobanks still need strong digital engagement after customers sign up

3. Low Fees Were Not A Marketing Trick, They Were The Product

In South Africa, fees matter. A bank account is not attractive if it quietly eats small balances with monthly charges and transaction costs. TymeBank leaned heavily into low-fee banking, and its current GoTyme Bank site promotes a free bank account, while its Google Play listing says “No paperwork. No monthly fees. No stress.”

The bank also said in 2021 that more than 80% of its customers paid zero bank fees and that customers had completed more than 100 million free transactions since launch. That gave the model a clear value promise for cost-sensitive consumers.

Best for:

- Price-sensitive customers

- Understanding why low-cost banking matters in emerging markets

Why We Chose It:

- Low fees addressed a real customer pain point

- The offer was easy to understand

- It helped the bank stand apart from traditional fee-heavy perceptions

- It supported financial inclusion by lowering the cost of participation

Things to consider:

- Low fees require a very efficient operating model

- Banks still need revenue through transactions, lending, partnerships, or value-added services

4. TymeBank Solved Onboarding Before Chasing Fancy Features

One underrated reason TymeBank worked is that it made account opening simple. In 2021, the bank said accounts could be opened in under five minutes through online channels, the app, or retail kiosks. That is not a glamorous feature, but it is essential.

For many users, the first barrier to banking is not advanced wealth management. It is paperwork, time, branch visits, and uncertainty. TymeBank reduced that friction, which made the first step into digital banking easier.

Best for:

- First-time digital banking users

- Fintech teams designing customer onboarding

Why We Chose It:

- Fast onboarding supported rapid customer growth

- It helped reduce intimidation around banking

- It made digital banking accessible to people outside affluent urban segments

- It showed that simplicity can be a competitive advantage

Things to consider:

- Fast onboarding must still meet compliance requirements

- Easy signup does not guarantee long-term customer activity

5. Profitability Made TymeBank Different From Most Neobank Stories

Many neobanks are excellent at raising money and less excellent at making money. TymeBank stood out because it reached its first profitable month in December 2023, less than five years after launching in February 2019. The Asian Banker reported this milestone, and Reuters later noted Tyme Group’s unicorn valuation after its $250 million Series D round.

This matters because profitability changes the story. Customer growth is exciting, but profitability suggests the model can become sustainable. For neobanks in emerging markets, that is a much stronger proof point than download numbers alone.

Best for:

- Investors studying neobank business models

- Readers comparing hype with financial durability

Why We Chose It:

- Profitability is rare and important in neobanking

- It proved the model was not only growth-funded experimentation

- It strengthened TymeBank’s credibility with investors

- It supported the idea that digital banking can scale efficiently in South Africa

Things to consider:

- One profitable month is not the same as permanent profitability

- Sustained profitability depends on active users, lending quality, deposit growth, and operating discipline

6. TymeBank’s Growth Was Fast Enough To Change The Conversation

TymeBank moved from launch in 2019 to millions of customers within a few years. The bank announced 3 million customers in 2021, with between 3,000 and 5,000 new customers joining daily at that stage. Reuters reported that Tyme Group had 10 million South African customers by late 2024, while later industry reporting said the South African operation had moved beyond that level.

This kind of growth matters because banking is usually slow to disrupt. Customers are cautious with money. They do not switch just because an app looks pretty. TymeBank’s growth showed that a low-cost, convenient, trusted model could win mass-market adoption.

Best for:

- Understanding digital banking adoption in South Africa

- Readers studying fintech scale

Why We Chose It:

- Customer growth proved real market demand

- It showed that digital banking could move beyond early adopters

- It validated the hybrid retail-plus-app model

- It created pressure on traditional banks to keep improving digital services

Things to consider:

- Customer count should be separated from active usage

- Growth must be matched with service quality and product depth

7. Financial Inclusion Was A Business Strategy, Not A Charity Slogan

TymeBank did not only target affluent digital banking users. Its model was built around affordability and underserved customers. British International Investment said its investment helped TymeBank deliver affordable financial services to 10 million underserved customers.

This matters because financial inclusion often gets treated like a social-impact footnote. TymeBank showed that underserved customers can also be a scalable commercial market when the product is designed around their needs. Low fees, fast onboarding, retail access, savings pockets, and simple digital tools created a model that was both inclusive and commercially serious.

Best for:

- Understanding inclusive fintech models

- Readers studying banking for underserved markets

Why We Chose It:

- It links financial inclusion with business model design

- It shows that underserved does not mean unprofitable

- It explains why TymeBank’s market fit was different from premium neobanks

- It gives the story social and commercial relevance

Things to consider:

- Inclusion must be measured through active use, not account openings alone

- Products still need strong consumer protection and responsible lending practices

8. Savings Tools Helped Turn A Basic Account Into A Money Habit

A neobank cannot rely only on account opening. It needs customers to keep using the product. TymeBank’s GoalSave feature helped by giving customers savings pockets and a visible reason to keep money inside the ecosystem. The bank’s current site promotes GoalSave with a 10% interest rate, while earlier company material described GoalSave as a free savings tool with multiple savings pockets.

This is important because savings tools create emotional and practical attachment. People do not only want somewhere to receive money. They want a way to separate goals, build discipline, and feel progress.

Best for:

- Customers building savings habits

- Neobanks trying to deepen engagement

Why We Chose It:

- Savings pockets create repeated app usage

- Strong savings messaging makes the account more attractive

- It helps move customers from sign-up to habit formation

- It gives low-cost banking a stronger value proposition

Things to consider:

- Interest rates can change

- Customers should always check the latest terms, limits, and qualifying conditions

9. TymeBank Used Partnerships To Expand Beyond Basic Banking

TymeBank’s model was not only a bank account. It expanded through partnerships and additional financial services. African Rainbow Capital reported in 2021 that TymeBank partnered with The Foschini Group to target TFG’s 26 million customers, with plans for products including insurance and term loans. More recent coverage of GoTyme Bank has highlighted partnerships across Sanlam, Boxer, Takealot, Kazang, and business lending channels.

This is where the neobank model becomes more interesting. The account is the entry point. The business becomes stronger when customers use savings, credit, insurance, payments, merchant services, or embedded finance.

Best for:

- Understanding neobank ecosystem strategy

- Readers studying partnership-led growth

Why We Chose It:

- Partnerships helped TymeBank expand reach and product depth

- Retail and enterprise relationships supported customer acquisition

- Embedded finance creates new revenue pathways

- The model showed how neobanks can grow beyond basic accounts

Things to consider:

- Partnerships must be managed carefully to avoid brand confusion

- More products can create complexity if customer experience is not clear

10. The Rebrand To GoTyme Bank Shows The Model Became Global

TymeBank officially transitioned toward the GoTyme Bank brand in 2026. Fintech News Singapore reported that the new GoTyme Bank app went live on January 22, 2026, with the rebrand aligning South African operations with the wider Tyme Group brand. Financial Afrik later reported that the South African Reserve Bank notice confirmed the name change to GoTyme Bank Limited in April 2026.

This matters because the South African model did not stay local. Tyme Group expanded into the Philippines and prepared for further Asian expansion. The rebrand shows that TymeBank’s South African success became part of a broader global digital-banking platform story.

Best for:

- Understanding Tyme’s global strategy

- Readers following African fintech expansion

Why We Chose It:

- The rebrand reflects alignment with a multi-country banking group

- It shows South Africa was a proof market, not the final destination

- Global branding supports investor and customer recognition

- It helps explain why Nubank’s investment mattered

Things to consider:

- Rebrands can create customer confusion if not communicated clearly

- Local trust must be preserved even when the brand becomes more global

11. Nubank’s Investment Was A Major Global Validation Signal

In December 2024, Reuters reported that Brazil’s Nubank invested $150 million in Tyme Group as part of a $250 million Series D round, valuing the group at $1.5 billion and giving it unicorn status. The round also included M&G Catalyst and existing shareholders.

That is not just a funding headline. Nubank is one of the world’s most important digital banking companies, so its investment suggested that Tyme’s model had global relevance. Investors were not only buying a South African bank. They were backing a digital banking model that could work across emerging markets.

Best for:

- Investors and fintech founders

- Readers studying global digital banking models

Why We Chose It:

- Nubank’s involvement increased credibility

- The $1.5 billion valuation made Tyme Group a major African fintech story

- The investment supported expansion into Southeast Asia

- It showed that emerging-market neobank models can travel across regions

Things to consider:

- High valuation creates high expectations

- Expansion into new markets brings regulatory, cultural, and execution risks

12. TymeBank Proved That Neobanks Must Respect Cash, Not Pretend It Disappeared

One reason neobank models sometimes fail in emerging markets is that they behave as if cash has already vanished. South Africa has strong digital banking adoption, but cash still matters for many households, informal workers, and lower-income consumers. TymeBank’s retail model gave customers a bridge between physical money habits and digital accounts.

This is why the South African neobank lesson is not “build an app and wait.” It is “build an app, then connect it to how people actually earn, spend, shop, save, and withdraw.” That is a much harder job, but it is also why the model worked.

Best for:

- Emerging-market fintech teams

- Understanding cash-to-digital transition models

Why We Chose It:

- It explains why physical access remained important

- It recognizes that cash habits do not disappear overnight

- It shows why hybrid banking can outperform pure app models

- It captures one of South Africa’s most important market realities

Things to consider:

- Cash handling adds cost and operational requirements

- Over time, digital usage must increase for the economics to keep improving

13. TymeBank’s Story Shows That Neobanks Need Trust As Much As Technology

Banking is not only a technology product. It is a trust product. South Africans needed to believe that a branchless bank was safe, legitimate, useful, and worth using. TymeBank built trust through regulation, partnerships, visible retail presence, low fees, and service simplicity.

This is the biggest lesson for Neobanks In South Africa. Winning the market is not about being the most futuristic. It is about being trusted enough to hold someone’s salary, grant payment, savings, or everyday spending money. TymeBank’s success came from making digital banking practical, affordable, and familiar.

Best for:

- Fintech founders building mass-market products

- Readers studying consumer trust in financial services

Why We Chose It:

- Trust is essential in banking adoption

- Technology alone does not solve financial exclusion

- Retail partnerships and low fees helped reduce skepticism

- It explains why TymeBank’s model felt local rather than imported

Things to consider:

- Trust can be damaged quickly by outages, fraud, poor support, or confusing fees

- Neobanks need long-term reliability, not only fast growth

An Overview Of 13 Facts About Neobanks In South Africa And TymeBank’s Rise

TymeBank’s story is not just a startup success story. It is a case study in how digital banking must adapt to local behavior, income realities, retail habits, and trust barriers.

Overview Comparison Table

Here is a quick comparison to help readers connect each fact with the broader lesson.

| Fact | Core Lesson | Why It Matters |

|---|---|---|

| 1 | Physical access still mattered | Digital banking needed real-world touchpoints |

| 2 | Grocery stores became banking infrastructure | Retail partnerships lowered acquisition friction |

| 3 | Low fees were central | Affordability drove adoption |

| 4 | Onboarding came first | Simple signup reduced barriers |

| 5 | Profitability changed the story | The model showed financial discipline |

| 6 | Growth proved demand | Millions of customers validated the market |

| 7 | Inclusion became strategy | Underserved customers could support scale |

| 8 | Savings tools built habits | GoalSave deepened engagement |

| 9 | Partnerships expanded the model | Ecosystem growth created more value |

| 10 | Rebranding showed global ambition | GoTyme aligned South Africa with the group |

| 11 | Nubank validated the model | Global investors saw emerging-market potential |

| 12 | Cash still had to be respected | Hybrid access matched local behavior |

| 13 | Trust mattered most | Banking adoption depends on credibility |

Our Top 3 Picks And Why?

Three lessons stand out because they explain why TymeBank worked where many digital banking ideas struggle.

| Key Lesson | Why It Stands Out |

|---|---|

| Hybrid Distribution | TymeBank combined digital banking with retail access points |

| Low-Cost Design | The model directly addressed South Africa’s price-sensitive market |

| Trust Through Familiarity | Retail partnerships and simple products made digital banking feel safer |

These three ideas explain why TymeBank was not just another app. It was a locally adapted banking model.

How To Chose the Best Neobanks In South Africa By Yourself

To evaluate any neobank in South Africa, do not start with the app design. Start with market fit. Ask whether the bank solves real customer problems around cost, access, trust, cash, savings, credit, and support.

The Selection Framework:

- Look At Active Usage, Not Just Signups: A large customer number matters more when customers transact regularly.

- Check The Fee Model: Low fees are powerful, but the bank still needs sustainable revenue.

- Study Distribution: South African neobanks need to bridge digital and physical behavior.

- Evaluate Product Depth: Savings, lending, insurance, and payments help the bank become more than a free account.

The Final Checklist

Before judging whether a South African neobank is truly working, use this five-point checklist.

- Does it solve a real affordability problem?

- Can customers onboard easily without branch friction?

- Does it support cash-in, cash-out, or retail-based access where needed?

- Are customers using it beyond sign-up?

- Is there a credible path to sustainable revenue and trust?

The Bigger Lesson From TymeBank’s South African Experiment

TymeBank’s rise proves that digital banking can work in South Africa, but only when the model respects the country’s realities. South Africa is digitally advanced, but it is not frictionless. It has strong banks, but many consumers still want cheaper and simpler alternatives. It has smartphone adoption, but cash and physical retail still matter.

That is why TymeBank’s achievement is bigger than one company. It showed that Neobanks in South Africa can scale when they combine low fees, fast onboarding, retail access, savings tools, partnerships, regulatory trust, and disciplined economics. The model was not purely digital. It was digital where digital helped, and physical where physical still mattered.

The uncomfortable truth is that many neobanks fail because they copy models from wealthier markets and assume users will adapt. TymeBank did the opposite. It adapted the model to users. That is the lesson every challenger bank, fintech founder, and digital banking investor should take seriously.

Frequently Asked Questions (FAQs) About Neobanks In South Africa

What Are Neobanks In South Africa?

Neobanks in South Africa are digital-first banks or banking platforms that offer app-based financial services, often with lower fees and simpler onboarding than traditional banks. Some, like TymeBank, also use retail partnerships and physical access points to support customers.

Why Did TymeBank Work In South Africa?

TymeBank worked because it combined low fees, fast onboarding, retail kiosks, savings tools, and a model designed for underserved and cost-sensitive customers. It did not rely only on an app.

Is TymeBank Still Called TymeBank?

TymeBank began transitioning to the GoTyme Bank brand in South Africa in 2026. Reports said the new GoTyme Bank app went live in January 2026, and the South African Reserve Bank notice confirmed the name change to GoTyme Bank Limited in April 2026.

Is TymeBank Profitable?

TymeBank reached its first profitable month in December 2023, less than five years after launching in February 2019. Sustained profitability depends on continued customer activity, product growth, credit quality, and operating discipline.

What Is The Biggest Lesson From TymeBank’s Success?

The biggest lesson is that neobanks must fit local behavior. In South Africa, that meant combining digital banking with low fees, retail access, trust-building, cash awareness, and simple products that solve everyday financial problems.