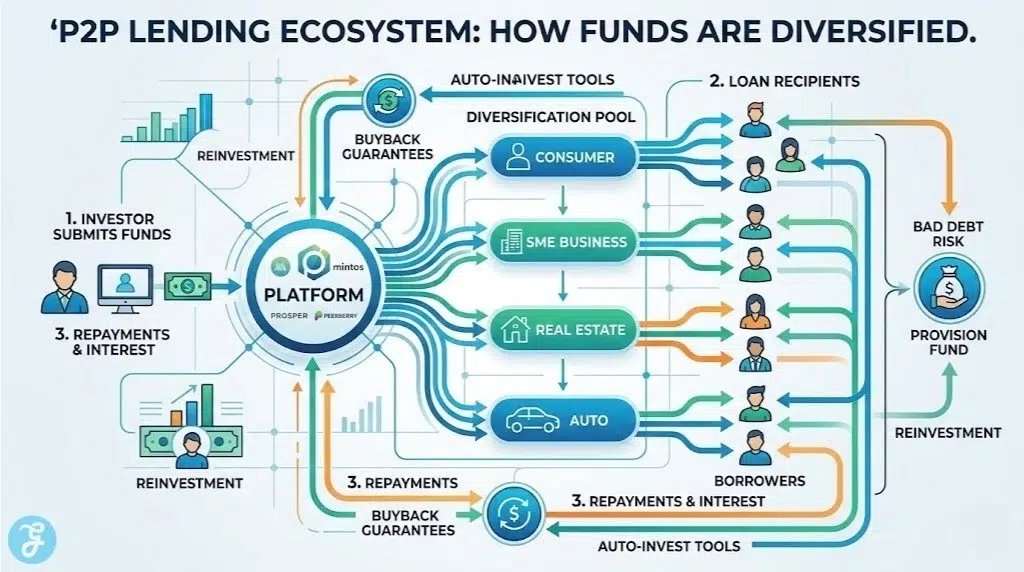

Finding the best peer-to-peer lending platforms in 2026 offers investors a unique opportunity to diversify their portfolios outside of traditional stock and bond markets. P2P lending connects individual investors directly with borrowers—whether they are consumers consolidating debt, small businesses expanding operations, or real estate developers funding new projects. By cutting out the traditional banking middleman, borrowers often receive more favorable terms, while investors can capture higher yield returns.

However, the industry has shifted significantly over the last few years, with a stronger emphasis on platform regulation, buyback guarantees, and automated investing tools. The following platforms represent the most reliable and lucrative global options for both novice and experienced P2P investors today.

How We Selected Our 10 Best Peer-to-Peer Lending Platforms

Our 2026 selection process prioritized platforms that have demonstrated resilience through recent economic fluctuations. We focused on transparency, historical default rates, and the tools provided to help retail investors manage risk. Below are the key metrics and criteria we used to evaluate the top lending networks.

| Criteria | Evaluation Metric | Why It Matters |

| Historical Yield | Average Annual Return (Net of bad debt) | Determines the actual profitability of the platform for the investor. |

| Risk Mitigation | Presence of Buyback Guarantees or Provision Funds | Protects the investor’s principal if a borrower defaults on their loan. |

| Market Liquidity | Availability of a Secondary Market | Allows investors to sell their loans and cash out before the loan term ends. |

| Platform Transparency | Audited financial reports and public loan books | Ensures the platform operates legally and transparently within its jurisdiction. |

| Automation Tools | Auto-Invest functionality and portfolio diversification algorithms | Saves time and automatically reinvests returns to compound interest efficiently. |

The 10 Best Peer-to-Peer (P2P) Lending Platforms

Whether you are looking for high-yield European consumer loans, US-based personal credit, or socially conscious micro-investing, these 10 platforms are the best in the business for 2026.

1. Mintos

Mintos is widely considered the powerhouse of European P2P lending. Rather than originating loans itself, it acts as a massive marketplace, connecting investors with dozens of different loan originators from around the world. This structure allows for unparalleled geographical and loan-type diversification. In 2026, Mintos operates as a fully regulated investment firm, offering “Mintos Core” automated portfolios that make it incredibly easy for beginners to start earning passive income with built-in diversification.

-

Best features: Massive loan volume and highly customizable Auto-Invest tools.

-

Pros: Unmatched diversification across countries and loan types; highly regulated.

-

Things to consider: Because it relies on external loan originators, investors must monitor the health of those third-party companies, not just Mintos.

2. Prosper

Prosper was the first peer-to-peer lending platform in the United States and remains one of the few platforms still open to retail investors in the American market. It focuses primarily on unsecured personal loans used for debt consolidation, home improvement, or medical expenses. Investors can browse individual loan listings and fund portions of them (as little as $25 per note). It is an excellent choice for US-based investors looking for a regulated, domestic P2P experience.

-

Best features: Custom automated investing and a very long, proven historical track record.

-

Pros: Highly transparent grading system for borrowers (AA to HR) to assess risk.

-

Things to consider: Unlike many European platforms, Prosper does not offer a buyback guarantee if a borrower defaults.

3. PeerBerry

PeerBerry has established itself as one of the most reliable and resilient platforms in the P2P space. It focuses heavily on short-term consumer loans issued by the Aventus Group and Gofingo. What sets PeerBerry apart is its flawless track record regarding its buyback guarantee; to date, no investor has lost capital due to a loan default on the platform. The interface is exceptionally clean, making it a favorite for investors who want a “set it and forget it” high-yield experience.

-

Best features: Ironclad buyback guarantee and a loyalty program for large investors.

-

Pros: Excellent track record during economic downturns and no cash drag (funds are quickly invested).

-

Things to consider: The platform lacks a secondary market, meaning you must wait for the short-term loans to finish to withdraw capital.

4. Funding Circle

Funding Circle is a premier platform for investors who want to support small and medium-sized enterprises (SMEs) rather than individual consumers. Operating primarily in the UK and the US, it connects accredited and institutional investors with established businesses looking for growth capital. It offers a more conservative risk profile compared to consumer payday loans, as the businesses undergo rigorous financial underwriting before being listed on the platform.

-

Best features: High-quality commercial underwriting and support for local economies.

-

Pros: Lower default rates than high-yield consumer loans and excellent corporate transparency.

-

Things to consider: Often requires a higher minimum investment and is largely restricted to accredited investors in the US.

5. Kiva

Kiva operates differently than every other platform on this list because it is entirely focused on social impact rather than financial return. It allows you to lend as little as $25 to entrepreneurs and students in developing nations across the globe. You do not earn interest on your loans; instead, as borrowers repay the principal, you can reinvest that money into new causes. It is the best platform for philanthropists who want to empower communities through microfinance rather than traditional charity.

-

Best features: Unmatched global social impact and connection to borrowers’ personal stories.

-

Pros: Empowers individuals in developing nations and has an incredibly high repayment rate (over 96%).

-

Things to consider: There is zero financial return on investment; it is a philanthropic platform.

6. Swaper

Swaper is a boutique P2P platform based in Estonia that focuses strictly on short-term consumer loans originating from its parent company, Wandoo Finance. It is famous in the P2P community for offering one of the highest fixed return rates on the market (up to 14%, and 16% for VIP investors). It operates almost entirely through its Auto-Invest tool, making it an aggressive, high-yield, hands-off addition to an investment portfolio.

-

Best features: Exceptionally high fixed interest rates and a reliable buyback guarantee.

-

Pros: Very simple auto-invest setup and an intuitive mobile app for tracking returns.

-

Things to consider: Low diversification, as all loans come from a single parent company.

7. CrowdProperty

For investors looking to back tangible assets, CrowdProperty is the leading UK platform for peer-to-peer real estate development lending. Investors fund loans given to property professionals for developments, bridging, and refurbishments. All loans are secured by a first charge on the underlying property, providing a significant layer of physical security. It bridges the gap between traditional P2P lending and real estate investing.

-

Best features: First-charge security on physical real estate assets.

-

Pros: Excellent historical returns with zero capital losses to date; backs physical assets.

-

Things to consider: Property development projects can be delayed, meaning capital might be tied up longer than expected.

8. LenDenClub

LenDenClub is currently one of the fastest-growing and most prominent P2P platforms in India. Regulated by the Reserve Bank of India (RBI) as an NBFC-P2P, it offers Indian investors access to highly vetted consumer loans. Its flagship “InstaMoney” product generates high volumes of short-term loans, and the platform utilizes an AI-driven credit assessment algorithm to keep default rates low. It is the premier choice for domestic investors in the Indian financial market.

-

Best features: Advanced AI credit scoring and deep integration with the Indian financial market.

-

Pros: Offers hyper-diversification (investing as little as ₹1 per loan) to minimize risk.

-

Things to consider: Only available to Indian residents and taxpayers.

9. Esketit

Esketit was founded by the creators of Creamfinance, a massive European alternative lender. The platform allows investors to fund loans originated by the founders’ own companies across Spain, Poland, and Jordan. Because the platform and the loan originators share the same ownership, there is a strong alignment of interests, and the buyback guarantees are backed by a highly profitable corporate group.

-

Best features: “Skin in the game” from founders and a highly liquid secondary market.

-

Pros: Very stable returns, strong corporate backing, and reliable auto-invest algorithms.

-

Things to consider: As a newer platform compared to Mintos, its long-term track record is still being built.

10. GoPeer

GoPeer is Canada’s first regulated consumer peer-to-peer lending platform. It connects creditworthy Canadians looking for personal loans with investors looking for fixed-income yields. It is highly praised for its strict underwriting—approving only a small percentage of borrowers who apply—which keeps the quality of the loan book very high. It fills a massive gap in the North American market, offering Canadians a transparent alternative to traditional bank investments.

-

Best features: Strict Canadian regulatory compliance and rigorous borrower vetting.

-

Pros: Excellent user interface and access to a previously untapped Canadian P2P market.

-

Things to consider: Available only to Canadian residents.

Quick Overview

The following table summarizes the core features of these top platforms to help you choose the right network for your investment strategy.

Comparison Table

| Platform Name | Primary Loan Type | Target Yield | Buyback Guarantee |

| Mintos | Multi-Originator Marketplace | 9% – 12% | Yes (Varies by Originator) |

| Prosper | US Personal Loans | 5% – 9% | No |

| PeerBerry | Short-Term Consumer | 9% – 11% | Yes (Strictly Enforced) |

| Funding Circle | SME Business Loans | 5% – 7% | No |

| Kiva | Social Microloans | 0% | No |

| Swaper | High-Yield Consumer | 14% – 16% | Yes |

| CrowdProperty | UK Real Estate | 7% – 9% | No (Secured by Property) |

| LenDenClub | Indian Consumer Loans | 10% – 12% | Varies |

| Esketit | European Consumer | 10% – 12% | Yes |

| GoPeer | Canadian Personal Loans | 7% – 9% | No |

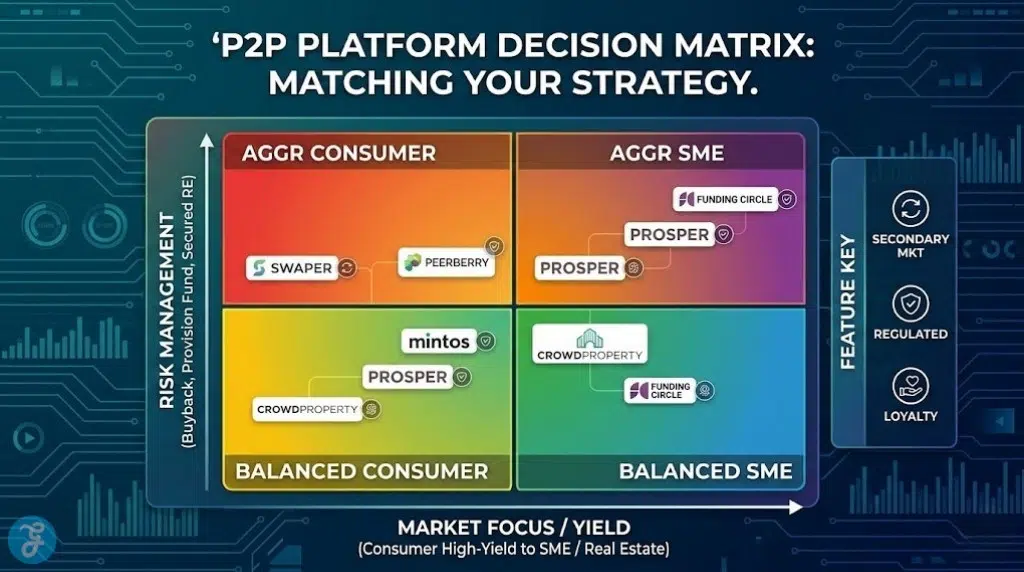

Quick Picks

If you need a fast recommendation based on your specific investor profile:

-

Best for European Diversification: Mintos

-

Best for US Retail Investors: Prosper

-

Best for Maximum Passive Yield: Swaper

-

Best for Social Impact & Philanthropy: Kiva

Final Thoughts On Peer-to-Peer Lending

Investing in the best peer-to-peer lending platforms can be an excellent way to boost your portfolio’s overall yield, especially in a low-interest-rate environment. However, it is crucial to remember that P2P lending is not without risk. Unlike a traditional savings account, your capital is at risk if borrowers default and the platform does not offer a robust provision fund. We highly recommend starting with platforms that offer Buyback Guarantees and utilizing Auto-Invest tools to spread your capital across hundreds of micro-loans, rather than putting all your money into a single borrower.