For Canadian professionals and business owners, the year 2026 has brought a unique set of fiscal challenges and opportunities. With the recent adjustments to federal tax brackets and the ongoing complexities of corporate investment rules, the traditional “Holding Company” (HoldCo) has evolved from a simple savings bucket into a sophisticated engine for tax efficiency for Canadian high earners.

While the headlines often focus on personal tax rates, the real wealth-building magic—and the most dangerous pitfalls—happens within the private corporate structure where capital can be sheltered, grown, and distributed with surgical precision.

Our Selection Methodology

To develop this guide, we analyzed the 2026 federal tax rate schedules, current Canada Revenue Agency (CRA) interpretations of the “passive income grind-down” rules, and recent 2026 updates to the capital gains inclusion thresholds. We consulted with financial planning models that compare immediate personal taxation against the long-term benefits of corporate deferral. Our criteria for this list prioritized “high-impact” strategies—those that provide the greatest net-worth lift for individuals earning above $250,000 while ensuring strict adherence to current anti-avoidance legislation.

10 Things Every Reader Must Know About How Canadian High-Earners Use Holding Companies for Tax Efficiency

Strategic corporate planning is no longer just for the ultra-wealthy; it is now an essential requirement for anyone looking to protect their hard-earned capital from the “tax drag” of high personal marginal rates.

1. The Power of the 40% Deferral Gap

In 2026, the gap between the top personal marginal tax rate (often exceeding 50% in many provinces) and the Small Business Deduction (SBD) rate (approximately 9-12%) remains the most significant driver for incorporating.

-

Best for: Business owners and incorporated professionals earning significantly more than their annual lifestyle costs.

-

Things to consider: This deferral is only a “loan” from the government; you eventually pay the remainder when you pull the money out as a personal dividend.

By keeping excess profits in a HoldCo, earners can reinvest nearly double the capital compared to what they would have left after personal taxes.

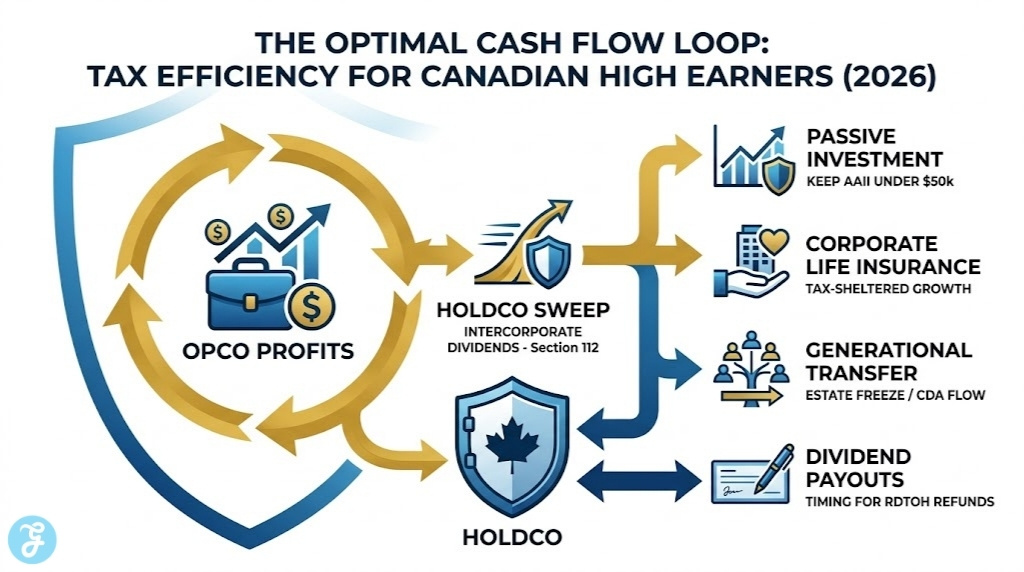

2. Tax-Free Intercorporate Dividends (Section 112)

High earners often use a HoldCo to “sweep” profits out of an active Operating Company (OpCo) without triggering an immediate tax bill.

-

Best for: Protecting retained earnings from potential lawsuits or business risks associated with the OpCo.

-

Things to consider: Strict “Safe Income” rules (Section 55) must be followed to ensure these dividends aren’t re-characterized as taxable capital gains by the CRA.

This mechanism allows wealth to be legally separated from operational risks while maintaining its tax-deferred status for future investments.

3. The Capital Dividend Account (CDA) Loophole

The CDA is a “notional” account that tracks the non-taxable portion of capital gains, allowing shareholders to extract cash completely tax-free.

-

Best for: Owners who have realized significant gains on stocks or real estate held within their corporation.

-

Things to consider: You must file a specific election (Form T2054) before paying the dividend, or you face stiff penalties for “excess” distributions.

Mastering the timing of CDA payouts is one of the most effective ways to get large sums of money out of a company without increasing your personal taxable income.

4. Managing the $50,000 Passive Income “Grind-Down”

The 2026 rules continue to penalize corporations that earn more than $50,000 in “passive” investment income (interest, dividends, rent) by reducing their access to the low 9% small business tax rate.

-

Best for: Corporations with large investment portfolios that still have active business operations.

-

Things to consider: For every $1 of passive income over $50,000, your business limit for the low tax rate is reduced by $5, disappearing entirely at $150,000.

Strategic earners often use “corporate class” funds or life insurance products to keep their taxable passive income below this critical threshold.

5. The Estate Freeze as a Generational Wealth Lock

A HoldCo allows high earners to “freeze” the value of their shares at current prices and issue new “growth” shares to their children or a family trust.

-

Best for: Parents looking to pass a family business or significant portfolio to the next generation without a massive tax bill at death.

-

Things to consider: You lose the ability to benefit from future growth personally, as that value is now legally owned by the next generation.

This strategy effectively shifts the future tax liability of business growth to heirs, often saving millions in eventual probate and terminal taxes.

6. Using Corporate-Owned Life Insurance for Liquidity

In 2026, permanent life insurance remains one of the few ways to grow wealth within a corporation without triggering the passive income grind-down.

-

Best for: Funding future estate taxes or providing a tax-free “buy-out” for a surviving business partner.

-

Things to consider: Premiums are generally not tax-deductible, but the eventual death benefit flows through the CDA to shareholders tax-free.

This creates a high-yield, tax-sheltered environment that traditional GICs or bonds simply cannot match inside a corporate structure.

7. The TOSI “Anti-Split” Wall

The 2018 “Tax on Split Income” (TOSI) rules were designed to stop high earners from paying out dividends to family members in lower tax brackets.

-

Best for: Owners whose family members are actively involved in the business (at least 20 hours per week).

-

Things to consider: Unless the family member meets specific “reasonableness” or “excluded business” tests, their dividends will be taxed at the highest possible rate.

Consulting with a specialist to document a spouse’s or child’s “meaningful contribution” is vital before attempting to split income in 2026.

8. RDTOH: The Government’s Refundable Security Deposit

When a corporation earns investment income, it pays a very high tax rate (~50.2%), but a large portion of this (Refundable Dividend Tax on Hand) is paid back to the company when it pays dividends to shareholders.

-

Best for: Maintaining the “integration” of the tax system, ensuring you don’t pay more tax through a company than you would personally.

-

Things to consider: You must actually pay out a dividend to “trigger” the refund, which might not always align with your personal cash flow needs.

Understanding your RDTOH balance helps ensure you aren’t leaving “pre-paid” tax sitting with the CRA longer than necessary.

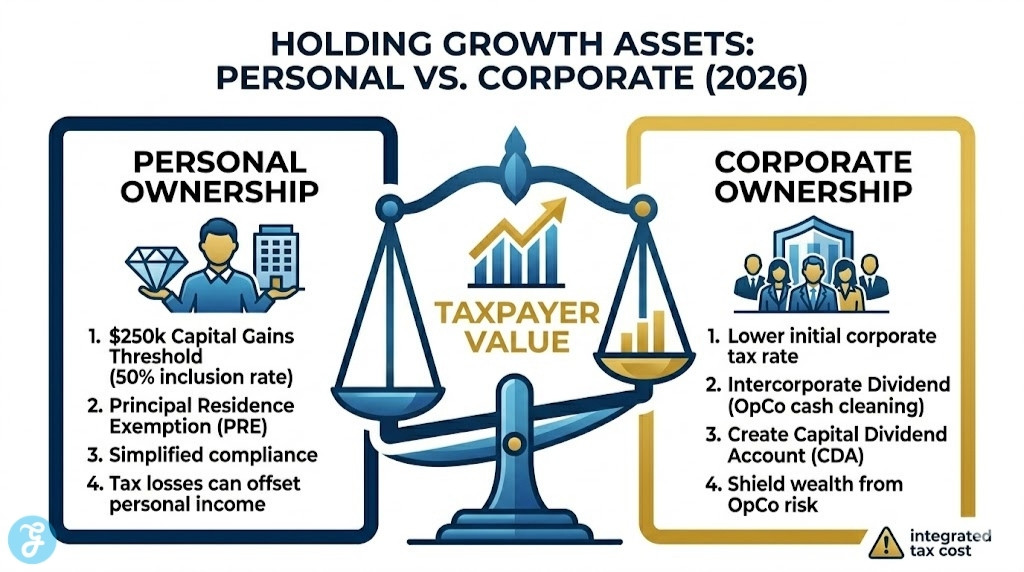

9. The Impact of the 2026 Capital Gains Pivot

While the proposed 2/3 inclusion rate was a major headline in previous years, 2026 has seen a stabilization where the first $250,000 of personal gains benefit from a 50% rate, while corporate gains face higher scrutiny.

-

Best for: High earners deciding whether to hold real estate personally or inside a corporation.

-

Things to consider: Corporations do not get the $250,000 threshold that individuals do, making personal ownership of certain assets more attractive in specific scenarios.

The decision of “where” to hold an appreciating asset has become the most debated topic in 2026 Canadian tax planning.

10. The Scientific Research and Experimental Development (SR&ED) Boost

For 2026, the expenditure limit for the enhanced 35% SR&ED tax credit has been adjusted, providing a massive incentive for tech-focused CCPCs.

-

Best for: High-earning entrepreneurs in the software, biotech, or engineering sectors.

-

Things to consider: The “taxable capital” threshold for this credit has been increased, meaning larger companies can now access these lucrative refunds.

This credit is often the difference between a startup’s failure and its ability to scale without seeking external venture capital.

Strategic Analysis

The choice between personal and corporate income management often comes down to the intended “use” of the funds. The table below highlights how different income types are treated in 2026.

| Income Type | Personal (Top Bracket) | Corporate (SBD Rate) | Retention Advantage |

| Active Business | ~53.5% Tax | ~12.2% Tax | 41.3% More to Reinvest |

| Capital Gains | 26.7% – 35.6% | ~25.1% – 33.3% | Minor (varies by province) |

| Interest Income | ~53.5% Tax | ~50.2% Tax (RDTOH eligible) | Neutral (Integration focus) |

Our Top 3 Picks And Why?

-

The Capital Dividend Account (CDA): This is the single most powerful tool for “cleaning” corporate cash. It allows the extraction of realized gains with zero personal tax, making it the ultimate goal of any investment-focused HoldCo.

-

The Estate Freeze: In an era of rising asset values, locking in the tax liability today while passing the “problem” of future growth to a family trust is the gold standard of succession planning.

-

Small Business Deduction (SBD) Retention: Protecting that 9-12% tax rate is the “daily win” of corporate tax efficiency. By carefully managing passive income, owners keep their primary wealth engine running at peak performance.

Preparation Checklist

-

[ ] Review your “Adjusted Aggregate Investment Income” (AAII) to stay below the $50,000 passive income threshold.

-

[ ] Confirm that your “Safe Income” on hand is sufficient for any planned intercorporate dividends.

-

[ ] Audit your Capital Dividend Account (CDA) balance before the end of the fiscal year.

-

[ ] Document all family member contributions to the business to satisfy TOSI “Reasonableness” requirements.

-

[ ] Evaluate if an “Estate Freeze” is appropriate given your current net worth and the age of your heirs.

Future-Proofing Your Corporate Wealth Structure

The Canadian tax landscape of 2026 is no longer a place for “set and forget” strategies. As high earners, the primary goal of using a holding company is to achieve tax efficiency for Canadian high earners by decoupling the earning of income from its ultimate taxation. By navigating the complex interplay between intercorporate dividends, refundable taxes, and generational freezes, you aren’t just saving money—you are building a resilient financial fortress that can withstand policy shifts and economic volatility for decades to come.

FAQs

-

Can I still use a Holding Company to split income with my retired parents? Only if they are over 65 and the dividends are paid from a “private corporation,” or if they meet the specific hours-worked criteria.

-

Is it better to pay myself a salary or a dividend in 2026? Salary is usually preferred if you want to generate RRSP room and pay into CPP; dividends are often simpler but don’t provide a corporate deduction.

-

Does a Holding Company protect my personal assets from business debt? Generally, yes. It provides a legal “firewall” between your active business operations and your accumulated savings.