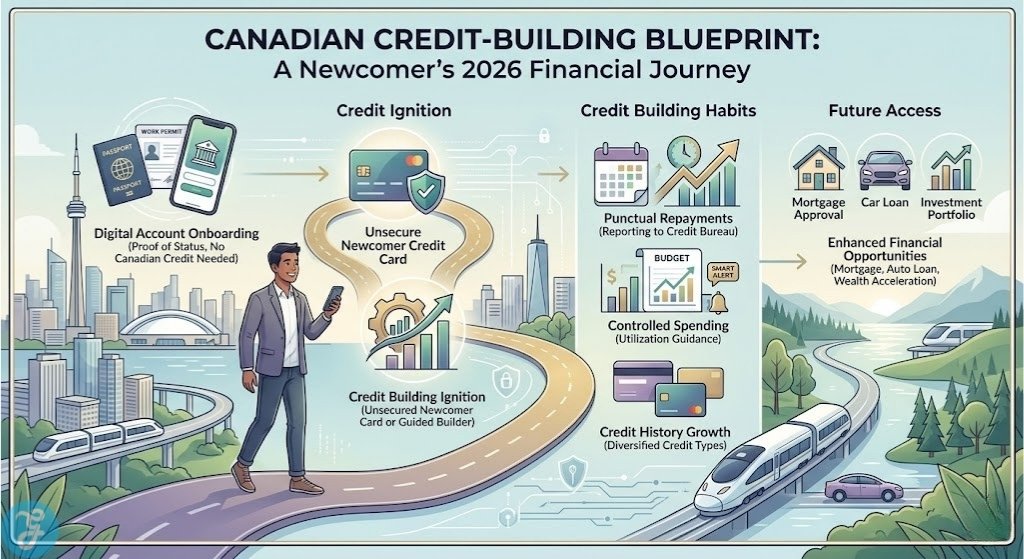

Starting your life in Canada involves a steep learning curve, especially when it comes to managing your money in a new currency. In 2026, the traditional path of visiting a physical branch to open an account is no longer the most efficient or rewarding choice. Digital banks and neobanks have transformed the landscape by offering high-interest rates, low fees, and specialized tools designed specifically for people with no domestic credit history. This guide details the top options available to help you hit the ground running as you settle into your new home.

How We Selected Our 9 Best Digital Banks for Newcomers

To provide you with the most effective banking options for 2026, we evaluated dozens of platforms based on their accessibility for those with zero Canadian credit. Our selection process prioritized digital-first institutions that offer immediate value through welcome bonuses, credit-building features, and intuitive mobile experiences. We focused on banks that allow you to start your financial journey without the typical hurdles found at older institutions.

The following criteria were used to rank the top contenders in the current market.

-

Credit Accessibility: Prioritizing banks that offer credit cards or building tools without requiring a prior Canadian credit score.

-

Fee Structure: Selecting accounts with no monthly maintenance fees to help you save money during your initial transition.

-

Welcome Value: Evaluating the quality of current 2026 bonuses, such as cash rewards or high-interest promotional periods.

-

Digital Infrastructure: Ensuring each bank provides a modern app that supports features like Interac e-Transfer and remote cheque deposits.

By analyzing these metrics, we have identified the nine banks that offer the best balance of utility and affordability for new residents.

| Selection Metric | Importance Level | Primary Benefit |

| Credit Builder Tools | Very High | Faster path to loans and mortgages |

| Zero Monthly Fees | High | Immediate cost savings on daily banking |

| No History Credit | High | Access to purchasing power immediately |

| High-Yield Savings | Medium | Growing your initial resettlement funds |

The following list explores the specific features and benefits of each selected institution to help you choose the best partner for your needs.

The 2026 Canadian market is highly competitive, meaning you can often secure a significant cash bonus just for opening your first account. These nine options provide a mix of traditional banking services delivered through a digital lens and modern fintech platforms that specialize in rapid credit establishment.

1. Simplii Financial

As the digital brand of CIBC, Simplii Financial offers a complete banking experience without the brick-and-mortar overhead. In 2026, they have refined their newcomer package to include a high-value cash bonus and an unsecured credit card specifically for those without a credit score. Their mobile app is consistently ranked as one of the best for ease of use and reliability.

Best for: Individuals who want a full-service bank with a massive ATM network and high welcome bonuses.

Why We Chose It:

-

It provides a dedicated newcomer credit card with a high approval rate for new residents.

-

The current 2026 welcome offer includes $300 in cash plus a bonus gift card for daily essentials.

-

You get access to over 3,400 CIBC ATMs across Canada without paying any withdrawal fees.

Things to consider: You cannot deposit cash directly at a branch, so you must use a CIBC machine for all physical transactions.

While Simplii is a great all-around choice, other digital banks focus more on the aesthetic and reward-based side of your spending.

2. Tangerine Bank

Tangerine is the digital subsidiary of Scotiabank and is widely recognized for its simplicity and transparency. They offer a no-fee daily chequing account and a highly customizable cash-back credit card that lets you choose your reward categories. This flexibility is perfect for newcomers who are still figuring out where their largest monthly expenses will be.

Best for: People who prioritize simple, transparent banking with no monthly fees and high-yield savings options.

Why We Chose It:

-

Their “Money-Back” credit card allows you to earn 2% cash back on three categories of your choice.

-

The sign-up process is entirely digital and can be completed in minutes using your smartphone.

-

Users can withdraw cash for free from any Scotiabank ATM, providing nationwide accessibility.

Things to consider: Their standard interest rates are often lower than neobank competitors once the initial promotional period ends.

If your primary goal is to improve your credit score as quickly as possible, a fintech platform might be more suitable.

3. Neo Financial

Neo Financial has become a leader in the 2026 credit-building space with its specialized “Build” membership. For a small monthly fee, this platform provides a path to a higher credit limit and clear milestones to help you improve your score in as little as three months. It is an excellent choice if you plan on applying for a car loan or a mortgage in the near future.

Best for: Newcomers who need an active, guided path to building a high Canadian credit score quickly.

Why We Chose It:

-

The credit builder tool offers transparent steps and smart tips to improve your financial habits.

-

You can earn instant cash back at thousands of local and national partners across Canada.

-

Keeping a balance of $5,000 across your accounts allows you to access the premium features for free.

Things to consider: The “Build” membership costs $7.99 per month if you do not meet the minimum balance requirements.

Another platform that excels at integrating spending and saving tools is currently a favorite among younger immigrants.

4. KOHO

KOHO is not a traditional bank but a financial platform that offers a prepaid Mastercard with deep credit-building capabilities. In 2026, their app includes features like rent reporting, which allows your monthly housing payments to count toward your credit score. This is one of the most innovative ways to build a history using expenses you are already paying.

Best for: Budget-conscious individuals who want to build credit using their rent payments and daily spending.

Why We Chose It:

-

The rent-reporting feature is a unique way to establish credit without taking on traditional debt.

-

You can earn up to 3.5% interest on your account balance, which is higher than most traditional banks.

-

Their “Everything” tier offers 2% cash back on all spending and no foreign exchange fees for travel.

Things to consider: Because it uses a prepaid card, you cannot deposit cash at a traditional bank machine.

While KOHO focuses on daily management, others are designed to help you grow your wealth through investing.

5. Wealthsimple

Wealthsimple has expanded from an investment platform into a comprehensive digital financial hub for 2026. Their “Cash” account functions like a high-interest chequing account, and their new credit card offers a 5% cash-back welcome bonus for the first thirty days. It is the perfect choice for those who want to manage their spending and their investments in a single, sleek app.

Best for: Tech-savvy newcomers who want to combine high-interest daily banking with easy access to stock and crypto trading.

Why We Chose It:

-

The app offers a seamless transition between spending, saving, and investing your money.

-

You get a 3% cash-back boost on the new Wealthsimple Visa during the initial welcome period.

-

There are no fees for international spending, making it ideal for those who travel frequently or send money abroad.

Things to consider: You must maintain a significant balance or set up direct deposit to unlock the highest interest rates.

For those who want a pure banking experience with the highest possible daily interest, a different digital-only bank is the current standard.

6. EQ Bank

EQ Bank is a digital-only institution that consistently offers some of the best everyday interest rates in Canada. In 2026, their Personal Account earns a total interest rate of 2.75% if you set up an automatic deposit for your paycheque. They also offer a unique card that reimburses you for any ATM fees charged by other banks, ensuring you never pay to access your own money.

Best for: Savers who want a completely fee-free experience and the highest available interest on their daily balance.

Why We Chose It:

-

They reimburse up to five ATM fees per month, meaning any cash machine in Canada becomes a free ATM.

-

The account includes free Interac e-Transfers and zero fees for everyday bill payments or transfers.

-

You can open multiple separate accounts for different savings goals within the same app.

Things to consider: This bank does not offer physical cheques, which might be a problem for some landlords or specific bill payments.

If you are looking for rewards that help with your daily living costs, a retail-linked digital bank could be the answer.

7. PC Financial

PC Financial is the digital bank for the Loblaws grocery network and Shoppers Drug Mart. Their “Money” account and Mastercard are perfect for newcomers because they allow you to earn PC Optimum points on every dollar you spend. These points can then be used for free groceries and household items, providing a direct benefit to your monthly budget.

Best for: Families and individuals who want to earn significant rewards on their grocery and pharmacy spending.

Why We Chose It:

-

You earn points at a high rate when shopping at any store within the Loblaws network.

-

The Mastercard is often available to newcomers with no credit history as part of their initial onboarding.

-

There are no monthly fees for the basic account, and you get free unlimited daily transactions.

Things to consider: The rewards are most valuable if you do the majority of your shopping at Loblaws-affiliated stores.

Some digital banks offer a more balanced approach by providing competitive rates on both savings and lending products.

8. Motusbank

Motusbank is a full-service digital bank that offers everything from high-interest savings to competitive mortgage rates. They are owned by a large credit union, which gives them a sense of stability while maintaining the low-fee structure of a digital institution. Their app is simple and functional, making it easy to manage your entire financial life in one place.

Best for: Newcomers who are planning on staying in Canada long-term and want to eventually apply for a mortgage.

Why We Chose It:

-

They offer some of the most competitive mortgage and loan rates in the digital banking sector.

-

You get access to over 3,500 free ATMs across Canada through the Exchange Network.

-

Their savings accounts consistently provide high interest without any hidden monthly maintenance fees.

Things to consider: The mobile app is more basic and lacks some of the advanced budgeting tools found in neobanks.

Finally, for those who want a highly automated and optimized banking system, there is one more innovative option to consider.

9. Manulife Bank

Manulife Bank offers a unique “All-in-One” account that combines your chequing, savings, and even your future mortgage into a single high-interest balance. For newcomers, their digital experience is streamlined and focused on helping you reach your financial goals through automation. It is a sophisticated choice for those who want their money to work as hard as possible.

Best for: High-income professionals who want an automated, sophisticated system to manage their total net worth.

Why We Chose It:

-

The All-in-One account automatically uses your idle cash to reduce the interest you pay on any debt.

-

Their mobile app provides deep insights into your spending patterns and your overall financial health.

-

It offers a very stable and secure digital environment backed by one of Canada’s largest insurance companies.

Things to consider: Some of their premium account structures have monthly fees if you do not maintain a high balance.

Setting Your Canadian Financial Foundation

The choice of a digital bank is one of the most important decisions you will make during your first year in Canada. By opting for an institution that understands the needs of new residents, you can avoid the frustration of high fees and slow credit growth. The banks listed here provide a powerful starting point for anyone looking to build a secure and prosperous future in their new home.

The information below summarizes the primary strengths and entry points for the top three categories of digital banking for newcomers.

| Bank Category | Primary Goal | Recommended Option | 2026 Feature |

| Big Bank Digital | Full Service/Welcome Bonus | Simplii Financial | $300 + $50 Bonus |

| Credit Builder | Fast Credit Establishment | Neo Financial | Guided Progress Tips |

| All-in-One Fintech | Investing & High Interest | Wealthsimple | 5% Cash Back Boost |

Our Top 3 Picks and Why?

While all nine banks have their merits, these three represent the most balanced and rewarding choices for a newcomer with no credit history.

-

Simplii Financial: It offers the best combination of a massive ATM network and a guaranteed path to an unsecured credit card.

-

Neo Financial: This is the most effective platform for actively learning how the Canadian credit system works while you build your score.

-

KOHO: The ability to report your rent payments to the credit bureaus is a game-changing feature for those who are just starting out.

How to Find the Right Digital Bank for Your Needs?

Selecting a bank requires you to be honest about your spending habits and your long-term financial goals. By using a structured approach to your decision, you can ensure that you are not paying for features you do not need while maximizing the rewards you are entitled to receive.

-

Audit Your Spending: Look at where you spend the most money to see if a grocery-linked or a cash-back card offers better value.

-

Determine Your Tech Level: Choose a neobank like Neo or Wealthsimple if you want the most advanced digital tools and automation.

-

Check ATM Proximity: If you frequently use cash, ensure your chosen bank is part of a large network like CIBC or Scotiabank.

-

Verify Credit Features: If your goal is to buy a house soon, prioritize banks that offer active credit building and rent reporting.

The following table can help you narrow down your choice based on your primary financial objective for the next year.

| Choose a Neobank (Neo/KOHO) if… | Choose a Traditional Digital Bank if… |

| You want to build your credit score as fast as possible. | You want a massive network of physical ATMs. |

| You prefer a modern, highly automated app experience. | You want a traditional bank’s stability and support. |

| You value innovative features like rent reporting. | You want a high-value cash welcome bonus. |

The Final Checklist

-

[ ] Download the Simplii and Tangerine apps to compare their current 2026 welcome offers.

-

[ ] Check your rental agreement to see if you can use KOHO’s rent-reporting feature.

-

[ ] Verify that you have your Social Insurance Number (SIN) and work permit ready for the sign-up process.

-

[ ] Review the ATM locations near your home to ensure you can access cash without fees.

-

[ ] Decide if you want to keep your spending and investing in the same app or separate them.

Building a Prosperous Life in Canada

Taking the first step toward financial independence in a new country is a major milestone. By choosing a digital bank that supports your unique situation, you are setting yourself up for long-term success. Whether you prioritize cash-back rewards, high interest, or rapid credit building, the Canadian market in 2026 has an option that will fit your lifestyle perfectly.

Frequently Asked Questions About Best Digital Banks for Newcomers

Do I need a credit score to open a digital bank account?

Answer: No, you do not need a credit score to open a basic chequing or savings account at any of these digital banks. However, a credit check is usually required if you apply for a credit card.

Is my money safe in a digital-only bank?

Answer: Yes, all the banks on this list are either members of the Canada Deposit Insurance Corporation (CDIC) or have their funds held in trust with CDIC-insured partners.

Can I use my work permit to open an account?

Answer: Yes, most digital banks accept a valid work permit or study permit along with government-issued photo identification as part of their newcomer onboarding process.

What is the fastest way to build credit with these banks?

Answer: The fastest ways are using a credit builder program like Neo’s, reporting your rent through KOHO, or obtaining an unsecured newcomer credit card from a bank like Simplii.

Answer: While there are no monthly maintenance fees, you may still be charged for specific actions like using an out-of-network ATM or requesting a printed bank statement.