If you have ever wondered how the ultra wealthy manage to give away millions to charity while simultaneously shrinking their tax bills to a fraction of what you might expect the secret usually lies in a specific financial tool. It is not an offshore account or a shady loophole. It is a completely legal highly encouraged vehicle called a donor advised fund.

Over the last decade these accounts have exploded in popularity. Financial advisors and tax professionals routinely recommend them as the ultimate bridge between philanthropy and wealth management. While the average person might write a check to their favorite charity at the end of the year wealthy individuals are using these specialized accounts to execute complex financial maneuvers. They are erasing capital gains resetting their portfolio metrics and shielding their estates from the government. The beauty of this tool is that you do not actually need to be a billionaire to use it. Proper donor advised funds tax strategies can often be applied by anyone looking to be smarter about their money.

What Exactly is a Donor Advised Fund?

Think of a donor advised fund as a personal charitable savings account. You open the account with a sponsoring organization which is usually the charitable arm of a major financial institution or a local community foundation. When you put cash stock or other assets into this account you are making an irrevocable donation to that sponsoring charity. Because of this you get an immediate tax deduction for the exact year you make the contribution. However the money does not have to go to an end charity right away.

The funds sit in your account where they can be invested and grow over time. You then act as the advisor to the fund telling the sponsor exactly which charities should receive the money and when. You get the tax break today but you retain the fun part of philanthropy which is deciding who gets the money tomorrow next year or even a decade from now.

| Account Feature | Operational Detail |

| Account Type | Personal charitable savings vehicle |

| Tax Deduction | Immediate deduction in the year of contribution |

| Investment Growth | Potential for tax free expansion |

17 Hidden Tax Strategies Wealthy Individuals Leverage Using DAFs

1. Taking an Immediate Deduction While Delaying the Grant

The most fundamental advantage of a donor advised fund is the timing. Let us say you have an unusually high income year and you desperately need a tax deduction by the end of December to avoid a massive tax bill. The problem is you have no idea which charities you actually want to support. You do not want to rush a large donation to an organization you have not researched. By dropping the money into a donor advised fund you lock in your tax deduction for the current year.

You can then take your time and wait until July of the following year to thoughtfully distribute the funds. This approach allows you to make more deliberate choices about your giving. Donor advised funds tax strategies make this separation of timing incredibly effective for wealthy individuals.

| Strategy Focus | Primary Benefit |

| Immediate Deduction | Lower your current year tax bill |

| Delayed Granting | Take time to research charities |

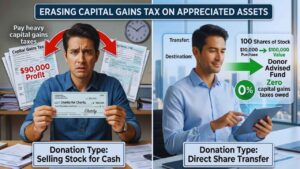

2. Erasing Capital Gains Tax on Appreciated Assets

Writing a check to charity is actually one of the least efficient ways to give if you hold investments. Wealthy individuals rarely give cash because they understand the power of donating highly appreciated assets. Imagine you bought stock for ten thousand dollars a decade ago and today it is worth one hundred thousand dollars. If you sell the stock to give the cash to charity you have to pay capital gains tax on the ninety thousand dollars of profit.

But if you transfer those shares directly into a donor advised fund the tax completely disappears. You pay zero capital gains tax and you still get to claim a charitable deduction for the full one hundred thousand dollar fair market value. This specific move is one of the most powerful wealth protection maneuvers available today.

| Donation Type | Tax Consequence |

| Selling Stock for Cash | Pay heavy capital gains taxes |

| Direct Share Transfer | Zero capital gains taxes owed |

3. Donating Complex and Illiquid Assets Before a Sale

Most local charities simply do not have the infrastructure to accept anything other than a credit card payment or a check. If you try to give a local animal shelter a ten percent stake in your private startup company they will not know what to do with it. Donor advised funds are fully equipped to handle complex assets. Wealthy investors frequently donate private equity shares real estate cryptocurrency and closely held business stock to their funds just before a major liquidity event.

The fund liquidates the asset tax free and the donor gets a massive deduction to offset the income from the rest of the sale. This lets you turn illiquid wealth into a flexible giving account effortlessly.

| Asset Class | Handling Capability |

| Real Estate and Equity | Fully supported by major sponsors |

| Immediate Liquidation | Asset is sold without tax penalties |

4. Using the Deduction Bunching Strategy

The standard deduction is quite high right now meaning many Americans no longer itemize their taxes. If you do not itemize your charitable gifts do not actually lower your tax bill. High earners bypass this math problem by using a strategy called bunching. Instead of giving twenty thousand dollars a year for five years and taking the standard deduction every time they will put one hundred thousand dollars into a donor advised fund in year one.

This massive contribution forces them well over the itemization threshold generating a huge tax refund. For the next four years they take the standard deduction on their taxes while slowly granting the money out of the fund. It maximizes the financial benefit of every dollar given.

| Tax Year | Deduction Strategy |

| Year One Contribution | Itemize for a massive tax refund |

| Subsequent Years | Claim standard deduction while giving |

5. Enjoying Tax Free Compound Growth

When you put money into a normal brokerage account you pay taxes on the dividends and taxes on the trades. When you put money into a donor advised fund it does not just sit in cash. It is invested in the market. Because the fund is technically owned by a tax exempt charity all of the growth happens completely tax free. If you deposit fifty thousand dollars and the market doubles over the next decade you now have one hundred thousand dollars to give away.

You generated fifty thousand dollars of charitable impact out of thin air and the internal revenue service cannot touch a single penny of the growth. Your giving capacity multiplies without any extra out of pocket costs.

| Investment Vehicle | Growth Taxation |

| Personal Brokerage | Taxes on dividends and trades |

| Charitable Account | Zero taxes on compound growth |

6. Softening the Blow of High Income Windfall Years

Financial windfalls are exciting until tax season arrives. Whether it is selling a medical practice receiving a massive corporate bonus or cashing out stock options a sudden spike in income can push a taxpayer into the absolute highest federal and state tax brackets. Wealthy individuals use donor advised funds as a shock absorber for these windfall years. By funneling a large portion of their windfall directly into the fund they artificially lower their adjusted gross income.

This keeps them out of the top tax brackets and preserves more of their wealth while simultaneously funding their philanthropy for the next decade. Implementing donor advised funds tax strategies during these peak earning years is incredibly smart planning.

| Income Event | Mitigation Action |

| Massive Bonus | Direct chunk of bonus to charity fund |

| Business Sale | Offset taxes with immediate deduction |

7. Shielding Wealth from the Estate Tax

For the ultra wealthy the federal estate tax is a looming threat that can swallow a massive percentage of their life work when they pass away. Any money left in a standard bank account or brokerage account is considered part of the taxable estate. However the moment an asset is transferred into a donor advised fund it is legally removed from the donor estate.

Families use these accounts to strategically trim down their net worth while they are still alive. This ensures that their wealth goes to causes they are passionate about rather than being absorbed by the federal government during probate. It gives you total control over the final destination of your lifetime earnings.

| Asset Location | Estate Tax Status |

| Personal Checking | Fully subject to estate taxes |

| Philanthropic Fund | Legally removed from taxable estate |

8. Bypassing Annual Distribution Minimums

Historically very wealthy families set up private foundations to manage their giving. One of the biggest drawbacks of a private foundation is the legal requirement to distribute at least five percent of the foundation net investment assets every single year regardless of market conditions. If the market crashes forcing a sale to meet the quota is painful.

Donor advised funds do not currently have a legally mandated annual payout requirement. Donors have the ultimate flexibility to let the account grow during lean years and make massive grants during strong economic times without the government breathing down their necks. You get to dictate the pace of your philanthropy based on your own timeline.

| Giving Vehicle | Distribution Requirement |

| Private Foundation | Mandatory five percent annually |

| Modern Giving Fund | No mandatory annual distribution |

9. Maintaining Complete Financial Privacy

When you operate a private foundation your tax returns are public record. Anyone with an internet connection can look up exactly how much money is in the foundation who the board members are and exactly which charities received grants. This often leads to an overwhelming flood of solicitation mail from organizations begging for money. Donor advised funds offer a shield of absolute anonymity.

Because the grants are officially distributed by the sponsoring organization the donor can choose to have the check sent completely anonymously. The receiving charity gets a check from the sponsor with no identifying information attached to the original donor keeping your wealth private.

| Privacy Factor | Level of Visibility |

| Foundation Returns | Completely open to public search |

| Sponsoring Organization | Complete anonymity is available |

10. Converting Burdensome Private Foundations

Many people who inherited or started private foundations eventually realize they are a complete administrative nightmare. The legal fees the accounting costs the tax filings and the board meetings become a second full time job. A massive trend right now is the legal conversion of private foundations into donor advised funds. The family works with a lawyer to dissolve the foundation and roll all the assets into a fund.

They retain all the fun parts of giving away the money but they completely eliminate the legal headaches the staff costs and the public scrutiny. It is a massive upgrade in efficiency for families who just want to help people without the red tape.

| Operational Aspect | Burden Level |

| Foundation Management | High costs and heavy compliance |

| Converted Fund | Zero compliance headaches |

11. Resetting the Cost Basis on Winning Stocks

This is one of the most brilliant and underutilized maneuvers in modern finance. Let us assume a wealthy investor wants to donate fifty thousand dollars to charity but they also own a specific tech stock that has skyrocketed in value and they want to keep it in their portfolio. Instead of giving cash they donate fifty thousand dollars worth of the highly appreciated stock to their fund avoiding the capital gains tax entirely.

Then they take the fifty thousand dollars in cash they were originally going to donate and buy the exact same stock on the open market. Their portfolio looks exactly the same but the stock now has a brand new higher cost basis which will save them a fortune in taxes later.

| Action Taken | Portfolio Impact |

| Donating Old Stock | Eliminates existing capital gains |

| Buying New Stock | Establishes a higher cost basis |

12. Eliminating Heavy Administrative Overhead

Running any kind of formalized charitable giving strategy usually requires a team of professionals. You need accountants to track the receipts and lawyers to ensure compliance with tax codes. With a donor advised fund the sponsoring organization handles everything for you. They do the due diligence to ensure the receiving charities are legitimate registered nonprofits.

They handle the tax reporting provide a single consolidated tax document at the end of the year and manage the investment platform. The donor simply logs into an app or a website clicks a few buttons and the money is sent. The sheer reduction in billable hours from accountants and lawyers pays for the minor fee the sponsor charges.

| Administrative Task | Responsible Party |

| Charity Vetting | Sponsoring organization |

| Tax Documentation | Handled seamlessly by the sponsor |

13. Establishing Seamless Legacy Planning

Estate planning is notoriously complicated especially when charitable intentions are involved. Writing complex trusts to dictate how money should be given away after death requires constant updating and expensive legal fees. A donor advised fund simplifies this entirely. A donor can easily name their children or trusted friends as successor advisors on the account.

When the original donor passes away the account seamlessly transitions to the successors outside of the probate process. The children simply log in and continue the family legacy of giving without ever needing to hire an estate lawyer to interpret a complex will. It is the easiest way to pass down your charitable values.

| Legacy Mechanism | Succession Process |

| Traditional Trust | Requires heavy legal interpretation |

| Successor Advisors | Instant access for named children |

14. Rebalancing Portfolios Without the Tax Sting

Financial advisors constantly preach the importance of diversifying a portfolio. If one stock performs incredibly well it might grow to represent too large a percentage of an investor total wealth. The standard move is to sell some of that stock to buy other assets but selling triggers capital gains taxes. Wealthy investors use their charitable funds as a rebalancing tool.

Instead of selling the overweight stock and paying the government they donate the excess shares directly to their fund. The portfolio is instantly brought back into balance the tax hit is completely avoided and they secure a massive charitable deduction in the process. It is a brilliant way to manage risk.

| Portfolio Status | Rebalancing Action |

| Overweight Stock | Donate excess shares directly |

| Risk Management | Balance restored without tax hit |

15. Sidestepping Complex IRS Reporting

If you are a generous person who gives to twenty different charities throughout the year tax season is incredibly frustrating. You have to hunt down twenty different receipt letters ensure they all have the proper legal language and list every single one on your tax return. If you lose a receipt you lose the deduction. A donor advised fund completely eliminates this paperwork nightmare.

You make one lump sum contribution to the fund and get one single tax receipt for the year. You can then distribute fifty different grants to fifty different charities from the fund and you never have to worry about tracking down another receipt for the government again.

| Giving Method | Paperwork Required |

| Direct Giving | Collect dozens of individual receipts |

| Consolidated Giving | One single tax receipt per year |

16. Outsmarting the 2026 Tax Law Changes

With the looming expiration of major tax code adjustments scheduled for the near future the landscape for charitable deductions is expected to shift dramatically. Certain limits on itemized deductions are expected to tighten and new floors may be introduced that will reduce the value of charitable gifts for high earners. Wealthy individuals and their advisors are acutely aware of this ticking clock.

They are aggressively front loading their funds right now pouring capital into these accounts to lock in the current highly favorable deduction rules. Proper donor advised funds tax strategies help them secure these benefits before the legislative window closes and the math works against them.

| Legislative Threat | Protective Action |

| Expiring Tax Cuts | Front loading charitable accounts |

| Lower Deduction Values | Securing current favorable rules |

17. Building a Multigenerational Culture of Giving

Beyond the spreadsheets the tax codes and the financial acrobatics a donor advised fund serves a deeply human purpose for wealthy families. It acts as a private family giving bank. Many high net worth parents use the account as a hands on training ground to teach their children about financial responsibility privilege and empathy.

Around the holidays the family will gather look at the balance of the fund and let the children research and pitch the charities they want to support. It forces the next generation to think critically about world issues and money management fostering a deeply rooted family tradition of philanthropy without the pressure of running a formal legal entity.

| Family Benefit | Educational Outcome |

| Group Discussions | Teaches children empathy and research |

| Shared Responsibility | Builds a lasting philanthropic legacy |

Final Thoughts

In the world of wealth management and estate planning using the right tools can make a massive difference in your financial security. Implementing donor advised funds tax strategies is not just about saving money it is about giving your wealth a distinct purpose. Wealthy Americans have figured out how to use these accounts to completely avoid capital gains taxes simplify their reporting and make a positive impact on the world on their own terms.

Whether you are trying to manage a sudden windfall reduce your taxable estate or just make your annual giving easier these accounts offer incredible flexibility. Speaking with your financial advisor about opening one of these accounts is a brilliant first step toward maximizing your philanthropic footprint while keeping more of your hard earned money out of the hands of the government.