Debt can be both a tool and a burden, depending on how it’s managed. For many, the road to financial stability is hindered by avoidable mistakes.

Understanding these pitfalls can make all the difference in achieving financial freedom. This article explores the common debt management mistakes that often derail progress and offers actionable advice to avoid them, making debt payments more effortless and stress-free.

Why Effective Debt Management Is Essential?

Managing debt isn’t just about paying off balances; it’s about maintaining financial health and reducing long-term stress. Poor debt management can lead to mounting interest rates, damaged credit scores, and a cycle of borrowing that’s hard to escape.

On the flip side, proactive debt management enables you to control your finances, reduce interest costs, and build a stable financial future.

Consequences of Poor Debt Management:

- High-interest payments eat into your income.

- Missed payments negatively impact your credit score.

- Increased reliance on loans or credit cards creates a vicious cycle.

Current Trend: According to a 2024 survey by the National Foundation for Credit Counseling, over 60% of Americans report struggling with at least one form of debt, underscoring the need for effective management strategies.

The 7 Common Debt Management Mistakes

Effectively managing debt starts with identifying the pitfalls that can hinder financial stability. These common debt management mistakes often stem from a lack of planning or understanding, but they can be avoided with the right strategies.

Mistake 1: Ignoring the Importance of Budgeting

A budget is the cornerstone of financial stability. Without one, it’s easy to overspend and lose track of your debt obligations. Studies show that households without a budget are twice as likely to fall into unmanageable debt.

Why This Happens:

- Lack of financial literacy.

- Misunderstanding of income versus expenses.

How to Avoid It:

- Create a monthly budget that tracks income, expenses, and debt payments.

- Use budgeting apps like Mint or YNAB to simplify the process.

- Regularly review and adjust your budget to account for changes in expenses.

Example: A young professional earning $3,500 monthly who spends $1,000 on unnecessary expenses like dining out and subscriptions can reduce discretionary spending to allocate $500 toward debt repayment.

Table: Budgeting Tips

| Step | Action | Benefit |

| Track Expenses | Use apps or spreadsheets to list spending. | Identify areas to cut back. |

| Set Spending Limits | Cap discretionary spending at 30% of income. | Avoid overspending. |

| Automate Savings | Direct a portion of income to savings. | Build financial resilience. |

Additional Tip: Break down fixed and variable expenses to gain better insights into areas where adjustments are possible.

Mistake 2: Only Paying the Minimum on Credit Cards

Minimum payments might seem like an easy solution, but they come with significant downsides, including prolonged debt repayment and higher overall costs due to interest.

Impact of Minimum Payments:

- A $5,000 credit card balance with 18% interest can take over 20 years to pay off with minimum payments.

- Prolonged payment periods increase overall financial stress.

How to Avoid It:

- Pay more than the minimum whenever possible.

- Prioritize paying off high-interest credit cards first using the avalanche method.

- Consider transferring balances to a lower-interest credit card.

Example: Sarah has $10,000 in credit card debt spread across three cards. By switching from paying the minimum to applying $1,000 monthly toward her highest-interest card, she reduces her repayment period by years and saves thousands in interest.

Table: Comparison of Debt Repayment Methods

| Method | How It Works | Best For |

| Snowball Method | Pay off smallest debts first. | Building momentum and morale. |

| Avalanche Method | Pay off highest interest first. | Saving money on interest. |

| Debt Consolidation | Combine debts into one loan. | Simplifying payments. |

Advanced Tip: If you’re struggling with high-interest debts, explore zero-interest balance transfer offers, but read the fine print for fees or timelines.

Mistake 3: Over-Reliance on Credit

Using credit for everyday expenses might seem convenient, but it can quickly lead to unmanageable debt. Studies suggest that 40% of credit card users carry a balance each month, leading to compounding interest.

Why It Happens:

- Lack of an emergency fund.

- Impulse spending habits.

- Misjudging repayment capacity.

How to Avoid It:

- Use cash or debit cards for daily purchases.

- Limit credit card use to planned expenses you can pay off immediately.

- Set spending alerts to monitor your credit usage in real time.

Example: A family that relies on credit cards for groceries can save by switching to a prepaid grocery budget. This reduces reliance on revolving credit.

Table: Strategies to Reduce Credit Reliance

| Strategy | Actionable Tip | Outcome |

| Build an Emergency Fund | Save 3-6 months of expenses. | Reduce dependency on credit. |

| Track Credit Utilization | Keep usage below 30% of limit. | Maintain a healthy credit score. |

| Pay Bills Automatically | Use automated payments. | Avoid late fees. |

Pro Insight: Credit reliance often stems from lifestyle inflation. Reassessing needs versus wants can significantly lower unnecessary credit usage.

Mistake 4: Not Having an Emergency Fund

Emergencies like medical bills or car repairs can force you to rely on loans or credit cards if you don’t have a financial cushion. An emergency fund is a financial safety net that helps you stay debt-free during unexpected crises.

How It Impacts Debt:

- Forces reliance on high-interest credit options.

- Prevents long-term savings growth.

How to Avoid It:

- Start with a goal of saving $1,000, then build up to 3-6 months’ worth of expenses.

- Automate savings to ensure consistency.

- Identify areas to cut back and redirect savings into your fund.

Quick List: Emergency Fund Strategies

- Cut unnecessary expenses.

- Save tax refunds or bonuses.

- Use savings apps like Acorns or Digit.

Case Study: John, a freelance designer, avoided $2,000 in credit card debt by using his emergency fund to cover unexpected dental surgery costs.

Table: Emergency Fund Building Tips

| Step | Action | Benefit |

| Start Small | Save $500-$1,000 initially. | Cover minor emergencies. |

| Automate Deposits | Schedule weekly transfers. | Build consistency. |

| Reassess Monthly | Adjust savings goals. | Stay on track. |

Pro Tip: Consider keeping your emergency fund in a high-yield savings account to earn interest while keeping the funds accessible.

Mistake 5: Ignoring High-Interest Debt

High-interest debt grows quickly and can snowball out of control if not addressed promptly. Data from Experian shows that the average credit card APR in 2024 was 20.4%, making it crucial to prioritize repayment.

Why It’s Harmful:

- Increases the total amount you owe over time.

- Limits your ability to focus on other financial goals.

How to Avoid It:

- Use the avalanche method to prioritize high-interest debts.

- Negotiate lower interest rates with lenders.

- Consolidate debts to reduce interest rates where possible.

Example: Maria consolidated her $15,000 debt with a 25% APR into a personal loan with a 12% APR, saving her $4,500 over three years.

Table: Impact of High-Interest Debt

| Debt Type | Interest Rate | Impact |

| Credit Cards | 18%-25% | Rapid growth of debt. |

| Personal Loans | 10%-15% | Moderate interest accumulation. |

| Payday Loans | 200%-400% | Extreme financial strain. |

Expert Insight: Lenders are often open to interest rate negotiations, especially if you have a strong payment history. Always ask!

Mistake 6: Failing to Seek Professional Help When Needed

Sometimes, managing debt on your own can feel overwhelming. Professional advice can provide clarity and options.

Signs You Need Help:

- Consistently missed payments.

- Feeling overwhelmed by the number of debts.

- Receiving collection notices or calls.

Where to Seek Help:

- Credit counseling agencies.

- Financial advisors.

- Nonprofit organizations specializing in debt relief.

Case Study: Lisa, a single mother with $30,000 in debt, reduced her payments by 40% with the help of a nonprofit credit counselor.

Quick List: Reputable Credit Counseling Agencies

- National Foundation for Credit Counseling (NFCC).

- Money Management International (MMI).

- InCharge Debt Solutions.

Pro Tip: Before hiring any debt relief service, verify its legitimacy through reviews and accreditation bodies like the Better Business Bureau.

Mistake 7: Taking on New Debt While Struggling to Pay Existing Debt

Borrowing more while struggling with existing obligations only compounds the problem. Research shows that nearly 50% of borrowers who consolidate debts take on new loans within a year, worsening their situation.

Why It Happens:

- Desire for quick financial relief.

- Misjudgment of repayment capabilities.

How to Avoid It:

- Calculate your debt-to-income (DTI) ratio to assess financial health.

- Focus on paying off existing debts before considering new loans.

- Seek financial counseling for personalized advice.

Interactive Suggestion: Use a debt-to-income ratio calculator to determine if you’re overleveraged.

Table: Signs of Financial Overextension

| Indicator | What It Means | Next Step |

| High DTI Ratio (>40%) | Too much income goes to debt. | Focus on paying off debt. |

| Missed Payments | Struggling to keep up with bills. | Seek professional assistance. |

| Overdrawn Bank Accounts | Living paycheck to paycheck. | Create a realistic budget. |

Additional Insight: Behavioral economists suggest creating a financial timeline to visualize debt-free milestones, helping prevent the urge to take on new debt.

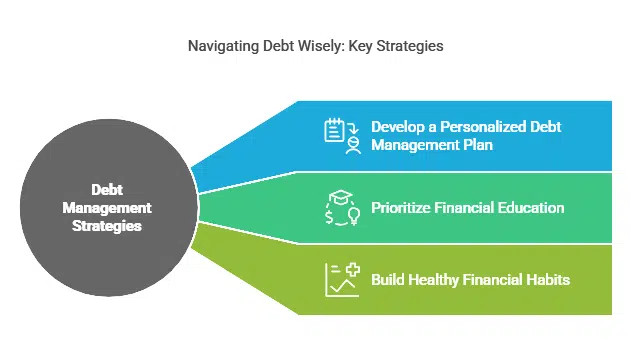

How to Avoid These Common Debt Management Mistakes?

Develop a Personalized Debt Management Plan

- Outline your financial goals and prioritize them.

- Break debts into manageable chunks and assign a timeline for repayment.

- Use tools like Excel templates or debt tracking apps.

Prioritize Financial Education

- Learn the basics of personal finance through books, courses, or online resources.

- Follow blogs or podcasts dedicated to debt management.

Build Healthy Financial Habits

- Regularly monitor your credit score and report.

- Set up automatic bill payments to avoid late fees.

- Practice delayed gratification for big purchases.

Wrap Up

Managing debt doesn’t have to be overwhelming. By avoiding these common debt management mistakes, you can create a pathway to financial freedom. Start with small changes, seek help when needed, and remain consistent in your efforts.

Take control of your financial future today and share this guide to help others do the same.