This is not just a technology upgrade; it is the bifurcation of the global monetary system. As the European Central Bank (ECB) finalizes legislation for the Digital Euro and China’s mBridge platform processes billions in non-dollar trade, the 2026 Crypto Pivot marks the end of the experimentation phase and the beginning of an infrastructure war. The pivot is no longer about if money goes digital, but who controls the rails it runs on.

Key Takeaways

- The “Western Rail” Strategy: Washington has solidified its stance with the implementation of the GENIUS Act (July 2025), effectively deputizing private stablecoin issuers like Circle and PayPal to distribute the digital dollar, eschewing a government-run FedCoin.

- The “Eastern Rail” Challenge: Project mBridge has graduated from a BIS experiment to a live geopolitical tool, enabling the BRICS bloc to settle oil and commodity trades in digital national currencies, completely bypassing the SWIFT network.

- Europe’s Legislative Showdown: 2026 is the “Year of Law” for the Digital Euro. With the technical preparation phase concluded in late 2025, the European Central Bank (ECB) is locked in a high-stakes negotiation with the EU Parliament over privacy limits and holding caps.

- The Rise of Tokenized Deposits: Commercial banks have launched a counter-offensive against stablecoins. Led by institutions like JPMorgan (via its Kinexys platform), banks are tokenizing standard deposits to offer 24/7 programmable settlements without leaving the regulated banking perimeter.

From Sandbox to Sovereignty: How We Got Here

To understand the gravity of the 2026 Pivot, one must look at the trajectory of the preceding two years. Between 2020 and 2024, Central Bank Digital Currencies (CBDCs) were largely academic exercises—isolated “sandboxes” where central bankers tested transaction speeds in safe, closed environments.

That changed radically in 2025. The geopolitical fractures widened, transforming these technical pilots into instruments of statecraft. The turning point came when the Bank for International Settlements (BIS) effectively handed over Project mBridge to its central bank partners in Asia and the Middle East, signaling that the platform was ready for real-world commercial traffic. Simultaneously, the United States, facing fierce political opposition to a surveillance-heavy “FedCoin,” made a decisive pivot. Instead of building a competitor to the Digital Yuan, Washington chose to regulate the private market, passing the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act in July 2025.

We are now living through the consequences of those decisions. The global financial system is no longer a monolith anchored by the US dollar and SWIFT; it is becoming a dual-track system where “State Control” (the East) and “Regulated Free Market” (the West) vie for the loyalty of global trade corridors.

The Great Bifurcation: mBridge and the Rise of the ‘Eastern Rail’

The most significant development of early 2026 is the operational maturity of Project mBridge. What began as a modest collaboration between the BIS and central banks in China, Hong Kong, Thailand, and the UAE has evolved into a high-volume corridor for cross-border trade.

By late 2025, transaction volumes on the mBridge ledger had surged, with the e-CNY (Digital Yuan) comprising the lion’s share of settlement volume. This is no longer a pilot; it is a parallel financial rail. For the first time, multinational corporations can settle intra-Asian trade instantly, without touching the US banking system or SWIFT. This “Eastern Rail” offers a proposition that is hard for developing nations to ignore: settlement times reduced from days to seconds, and costs slashed by up to 50% by removing correspondent banking fees.

Why It Matters: This is the realization of the “de-dollarization” fear—not as a collapse of the dollar, but as the creation of a viable alternative. The 2026 pivot sees the mBridge ledger acting as a geopolitical shield. For BRICS nations, particularly new entrants like Iran or Saudi Arabia, the ability to settle energy trades in digital national currencies protects them from the reach of Western financial sanctions. The mBridge platform allows these nations to regain monetary sovereignty, ensuring that their liquidity cannot be frozen by a foreign treasury department.

The American Response: Privatized Dollars and the Stablecoin Shield

While China pushed the state-run e-CNY, Washington made a tactical masterstroke in 2025 that is paying off in 2026. Recognizing that a retail CBDC would face insurmountable privacy concerns from the American public, US policymakers chose to “privatize” the digital dollar.

The GENIUS Act created a federal framework for payment stablecoins, effectively deputizing issuers like Circle (USDC) and PayPal (PYUSD) to run the digital dollar rails. In 2026, this strategy is reshaping the crypto market. Major US banks and fintechs are integrating these regulated stablecoins into their core treasury operations. By providing legal clarity, the US has unleashed the private sector to innovate faster than any central bank could.

The Strategic Logic: The US aims to make the dollar the “native currency of the internet.” By allowing dollar-backed stablecoins to flood the global crypto ecosystem, Washington ensures that even in a decentralized Web3 world, the unit of account remains the USD. This is a “Trojan Horse” strategy: while other nations build walled gardens, the US is exporting its currency through open-source code, ensuring that the dollar remains dominant not by mandate, but by utility and liquidity.

The Three Pillars of Digital Finance (2026 Status)

| Feature | The Eastern Rail (mBridge/e-CNY) | The Western Rail (US Stablecoins) | The European Hybrid (Digital Euro) |

| Primary Issuer | Central Banks (PBoC, CBUAE, etc.) | Private Firms (Circle, PayPal, Banks) | European Central Bank (ECB) |

| Primary Goal | Sovereignty & Sanctions Resistance | Modernizing Settlement & Web3 Dominance | Monetary Anchor & Strategic Autonomy |

| Privacy Model | “Managed Anonymity” (State sees all) | KYC/AML Compliant (Transparent to Regulators) | Tiered (Private for small sums, traced for large) |

| 2026 Status | Production (High trade volume) | Scaling (Institutional adoption post-GENIUS Act) | Legislative Phase (Building infrastructure) |

| Key Risk | Geopolitical fragmentation | Counterparty risk of private issuers | Lack of consumer adoption |

Europe’s Digital Dilemma: Privacy, Policy, and the Programmability War

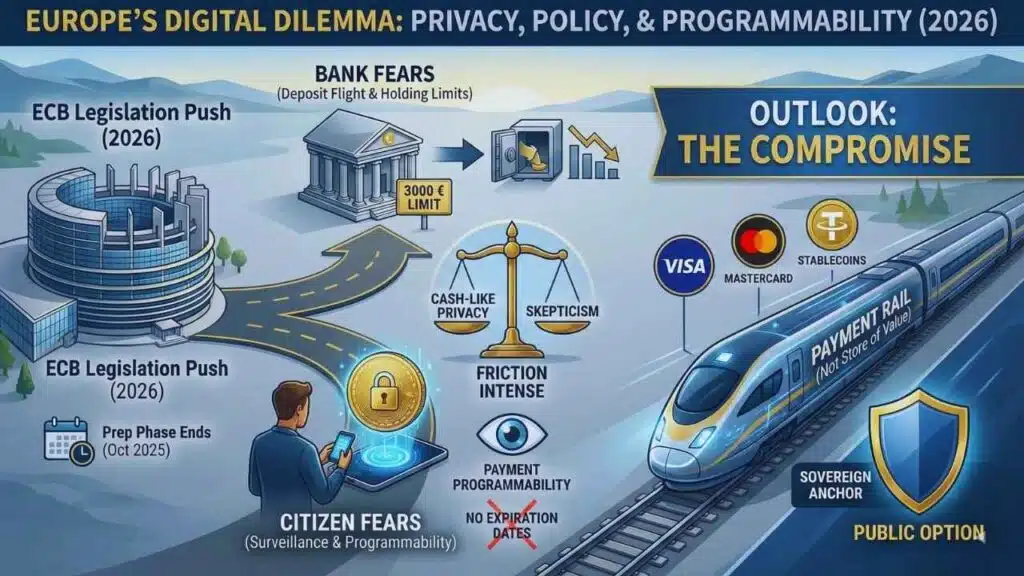

Caught between the state-run East and the corporate-run West, Europe is attempting to chart a “Third Way.” The Digital Euro is currently in its most critical phase. With the “preparation phase” successfully concluded in October 2025, the ECB is now pressing the EU Parliament to pass the enabling legislation before the end of 2026.

The friction this year is intense. The ECB promises “cash-like privacy” for low-value offline payments, but commercial banks and privacy advocates remain deeply skeptical. Banks fear the proposed “holding limits” (likely capped at €3,000 per citizen) will cause deposit flight, eroding their balance sheets during crises. Conversely, citizens fear the “programmability” of the currency. Although the ECB insists the money itself won’t be programmable (i.e., expiration dates or restricted spending), the payments will be, leading to fears of a surveillance state.

The Outlook: The legislation will likely pass in late 2026, but with significant concessions. To appease the banking lobby, the Digital Euro will likely be positioned strictly as a “payment rail” rather than a store of value. The ECB’s goal is not to replace commercial bank money, but to provide a sovereign anchor for the payment system—a public option to ensure Europe isn’t dependent on Visa, Mastercard, or foreign stablecoins.

The Infrastructure of 2026: Interoperability, Tokenized Deposits, and the New Banking Stack

While policymakers debate currencies, the real revolution of 2026 is happening in the plumbing of the financial system. The focus has shifted from assets to interoperability—the technology connecting these fragmented networks.

A silent war is being fought between “Tokenized Deposits” and “Stablecoins.” Commercial banks, threatened by the rise of non-bank stablecoin issuers, have aggressively rolled out Tokenized Deposits. Unlike a stablecoin (which is a bearer instrument like digital cash), a tokenized deposit is a claim on a specific bank, recorded on a blockchain.

In 2026, major institutions like JPMorgan (via Kinexys) and Citigroup are live with these systems. They allow multinational clients to move billions in liquidity 24/7, programmable via smart contracts, without the regulatory headaches of holding a “crypto asset.”

Analysis: This is the banking sector’s immune response. By upgrading their own deposits to behave like crypto, banks are trying to render stablecoins obsolete for institutional use. The battleground for 2026 is Chainlink’s CCIP (Cross-Chain Interoperability Protocol) and SWIFT’s new connector, which allow a “Digital Euro” on one chain to buy a “Tokenized US Treasury” on another. The winners of 2026 are not just the currency issuers, but the translators—the protocols that allow these walled gardens to speak to each other.

Comparative Timeline of the 2026 Pivot

| Period | Event / Milestone | Impact on Global Finance |

| July 2025 | US Passes GENIUS Act | Established federal rules for stablecoins; legitimized private digital dollars. |

| Oct 2025 | ECB Ends Prep Phase | Digital Euro moved from technical design to legislative negotiation. |

| Jan 2026 | mBridge Goes Live | Full handover to central banks; creating a permanent non-SWIFT trade rail. |

| Q1 2026 | JPM Kinexys Scaling | Tokenized deposits begin overtaking stablecoins for wholesale/institutional settlement. |

| Late 2026 | EU Vote (Projected) | Expected passage of Digital Euro Regulation; sets stage for 2027 pilots. |

| Late 2026 | BRICS Summit (India) | Expected formal launch of “BRICS Pay” retail integration. |

Expert Perspectives

The Geopolitical Realist:

“The US made a tactical masterstroke by abandoning the retail CBDC. By letting the private sector run with stablecoins, they have flooded the crypto ecosystem with dollars, making it harder, not easier, for the Digital Yuan to displace the greenback in retail commerce. The dollar is winning the code war.” — Senior Macro Analyst, London Think Tank.

The Privacy Advocate:

“The Digital Euro legislation being debated this year is a Trojan Horse. Once the infrastructure for programmable money is installed, the safeguards can be removed by a simple software update in the future. The battle of 2026 is for the right to transact anonymously, a right that is slowly evaporating.” — EU Digital Rights Group Spokesperson.

The Technologist:

“We are moving from a world of ‘Net Settlement’ (T+2 days) to ‘Atomic Settlement’ (T+0). The friction of 2026 is not technology; it is legal. The technology is ready to settle a stock trade in seconds, but the laws still assume it takes two days. Tokenized deposits are the bridge that fixes this without breaking the law.” — Head of Digital Assets, Major Wall St Bank.

Future Outlook: The Road to 2030 and the Battle for Utility

As we look toward the latter half of 2026 and beyond, three milestones will define the trajectory of the global economy:

- The EU Legislative Outcome: If the Digital Euro package passes in Q4 2026, expect a flurry of pilot announcements for 2027. If it stalls due to privacy concerns, the Eurozone risks falling behind the “Stablecoinization” of the economy, leaving the field open for US-backed stablecoins to dominate European fintech.

- BRICS Pay Expansion: Watch for the integration of Saudi Arabia or Iran into the mBridge rail. If energy trades begin settling largely in e-CNY or Digital Dirhams, the “Petrodollar” faces its first true digital rival. The 2026 summit in India will likely showcase the retail face of this alliance—”BRICS Pay”—allowing citizens to spend seamlessly across member nations.

- The “Unified Ledger” Concept: The BIS is pushing for a “Unified Ledger”—a single global platform where tokenized central bank money and commercial bank assets live together. 2026 will see the first major prototypes of this “Internet of Value,” likely led by a consortium of central banks attempting to regain control from the fragmented private blockchain ecosystem.

The 2026 Crypto Pivot is the realization that money is no longer just a store of value; it is a programmable data packet. The West has bet on private innovation regulated by the state; the East has bet on state infrastructure. The winner will not be decided by who has the better technology, but by who offers the most utility to the global supply chain. For the first time since Bretton Woods, the world has a choice in how it moves value.