For many individuals entering their golden years, the prospect of navigating the complex US tax code can be as daunting as the volatile markets themselves. One of the most powerful tools available to secure a stable financial future is the strategic movement of assets from a traditional tax-deferred account into a Roth IRA. Understanding how Roth Conversion Strategies work is essential for anyone looking to minimise their long-term tax liability and maximise the legacy they leave behind.

By paying taxes on your retirement savings today, you effectively buy out the government’s future interest in your wealth, allowing for tax-free growth and distributions.

Selection Methodology

To develop these insider tips, we consulted with senior tax professionals and financial planners to identify the most effective methods for managing retirement assets as of early 2026. Our criteria focused on strategies that provide the greatest flexibility in tax-bracket management, mitigation of Required Minimum Distributions (RMDs), and protection against future legislative changes. Each tip was selected based on its ability to help retirees maintain control over their marginal tax rates while ensuring that their Roth Conversion Strategies remain compliant with the latest IRS guidelines.

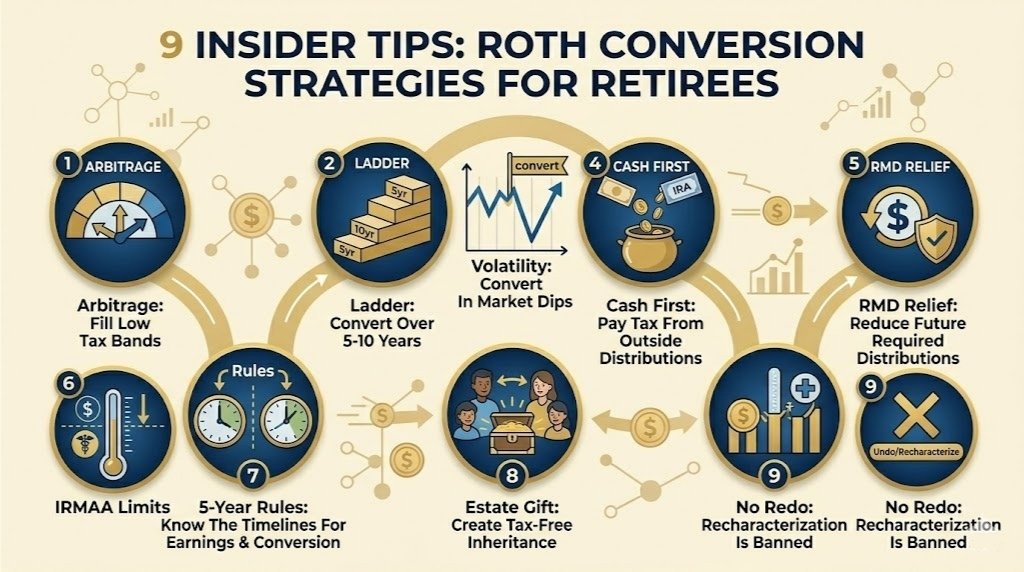

9 Insider Tips On How Roth Conversion Strategies Work For American Retirees

The following guide explores the nuances of moving wealth into a Roth environment. While the concept is straightforward—converting pre-tax dollars to post-tax dollars—the execution requires a delicate balance of timing, tax-bracket awareness, and cash flow management. These nine tips are designed to provide a sophisticated framework for retirees who want to protect their purchasing power against the certainty of future taxation.

1. Master The Art Of Tax Bracket Arbitrage

The primary goal of most Roth Conversion Strategies is to pay taxes at a lower rate now than you expect to pay in the future. Retirees often find themselves in a “tax valley”—the period after they stop working but before they are forced to take RMDs or start Social Security. Converting assets during these low-income years allows you to fill up your current low tax bracket without being pushed into a higher marginal rate.

Best for: Retirees in the early years of retirement with significant traditional IRA balances.

Why:

● It represents the most efficient use of the progressive tax system.

● It allows for the permanent “lock-in” of current historically low tax rates.

Things to consider: You must accurately estimate your total annual income to avoid accidentally triggering a higher tax bracket or affecting your Social Security taxation.

2. Implementation Of The Partial Conversion Ladder

Instead of converting a large sum in a single year—which could trigger a massive tax bill—insiders recommend a “laddering” approach. By performing partial conversions over a 5 to 10-year period, you spread the tax liability over multiple years. This strategy ensures that you are never paying a higher percentage in tax on your conversion than is absolutely necessary, preserving more of your principal for future growth.

Best for: Individuals with large 401(k) or traditional IRA balances who have at least five years before RMDs begin.

Why:

● It provides superior control over annual cash flow and tax outlays.

● It mitigates the risk of a single high-tax event during a peak income year.

Things to consider: Each annual conversion starts its own five-year clock for tax-free withdrawals of the converted amount, so meticulous record-keeping is essential.

3. Capitalising On Market Volatility

Market downturns are often viewed with dread, but for a savvy retiree, a “red” market is a “green” light for a Roth conversion. When the value of your traditional IRA drops, you can convert the same number of shares for a lower tax cost. When the market eventually recovers, that entire recovery happens inside the Roth IRA, where the growth is completely tax-free.

Best for: Investors who have a long-term horizon and the stomach to act during market corrections.

Why:

● It allows you to move more shares into the Roth environment for fewer tax dollars.

● It essentially uses the market’s recovery to pay for the future tax-free growth.

Things to consider: You must have the cash available outside of the IRA to pay the tax bill to make this strategy truly effective.

4. Paying The Tax Bill From Non-Retirement Accounts

To maximise the benefits of Roth Conversion Strategies, you should never use a portion of the converted funds to pay the resulting tax bill. If you are under 59.5, using IRA funds to pay the tax could trigger a 10% penalty. Even if you are older, using the funds reduces the amount of money that can grow tax-free. Using “outside” cash from a standard brokerage or savings account keeps 100% of your retirement capital working for you.

Best for: Retirees with sufficient liquidity in non-qualified accounts to cover the IRS payment.

Why:

● It maximises the compounding power of the Roth IRA by keeping the principal intact.

● It avoids potential early withdrawal penalties and unnecessary depletion of retirement assets.

Things to consider: You should set aside these tax funds in a high-yield savings account or money market fund well before the tax deadline.

5. Strategic Mitigation Of Future Required Minimum Distributions

Traditional IRAs and 401(k)s require you to take RMDs starting at age 73 or 75, regardless of whether you need the money. These forced distributions can push you into a higher tax bracket and increase your Medicare premiums. Roth IRAs, however, have no RMDs for the original owner. Converting early reduces the size of your tax-deferred bucket, thereby shrinking your future RMDs and giving you total control over your income.

Best for: High-net-worth retirees who do not expect to need their full RMD amount for living expenses.

Why:

● It removes the government’s ability to dictate when you must realise income.

● It provides a massive hedge against the risk of rising tax rates in the future.

Things to consider: While Roth IRAs have no RMDs for the owner, inherited Roth IRAs still have specific distribution rules for non-spouse beneficiaries.

6. Accounting For The IRMAA Surcharge

Retirees must be careful not to let a Roth conversion push their income above certain thresholds that trigger the Income Related Monthly Adjustment Amount (IRMAA). This surcharge can significantly increase your Medicare Part B and Part D premiums. Insiders often aim their conversions just below these “cliff” thresholds to ensure the tax savings of the Roth are not wiped out by higher healthcare costs.

Best for: Medicare-enrolled retirees who are close to the income thresholds for premium surcharges.

Why:

● It protects the retiree from hidden costs that are not visible on a standard tax return.

● It ensures a truly holistic approach to retirement wealth management.

Things to consider: IRMAA is based on your modified adjusted audited income from two years prior, so your 2026 conversion affects your 2028 premiums.

7. Understanding The Multiple Five-Year Rules

There is a common misconception that there is only one five-year rule for Roth IRAs. In reality, there is one for the account’s age to withdraw earnings tax-free and a separate one for each specific conversion to withdraw the converted principal penalty-free if under 59.5. Mastering these timelines is essential to ensure that you do not accidentally trigger a tax or penalty when trying to access your money.

Best for: Early retirees or those who may need to access their Roth principal before age 59.5.

Why:

● It provides the legal “safety rail” for accessing liquidity without financial damage.

● It ensures that the tax-free status of the account’s earnings is never compromised.

Things to consider: Always consult with a tax professional to track the specific “vintage” of each conversion in your ladder.

8. Roth Conversions As An Estate Planning Powerhouse

For those who wish to leave a legacy, a Roth IRA is perhaps the most valuable asset you can pass on. Under the SECURE Act, most non-spouse beneficiaries must empty an inherited IRA within 10 years. If they inherit a traditional IRA, that money is taxed at their likely peak-earning years’ rates. If they inherit a Roth, that 10 years of additional growth and the final distribution are entirely tax-free for them.

Best for: Retirees who prioritise generational wealth transfer and want to minimise their heirs’ tax burdens.

Why:

● It is one of the most effective ways to “pre-pay” the tax for the next generation at a lower rate.

● It allows the inherited assets to continue growing tax-free for a full decade after the owner’s death.

Things to consider: Your beneficiaries will still need to follow the 10-year distribution rule, even though the withdrawals are tax-free.

9. Staying Informed On The Prohibition Of Recharacterisation

Before 2018, taxpayers could “undo” a Roth conversion if the market dropped—a process called recharacterisation. This is no longer allowed under current law. Once you convert, the decision is permanent. This makes it even more important to be precise with your calculations and to ensure you have the funds to pay the tax bill, as you cannot change your mind later.

Best for: All retirees planning a conversion in the current legislative environment.

Why:

● It emphasises the need for professional planning over impulsive financial moves.

● It clarifies a major historical shift in the tax code that many still misunderstand.

Things to consider: Because you cannot undo the move, many retirees wait until late in the year (November or December) to perform their conversions when their annual income is clearly defined.

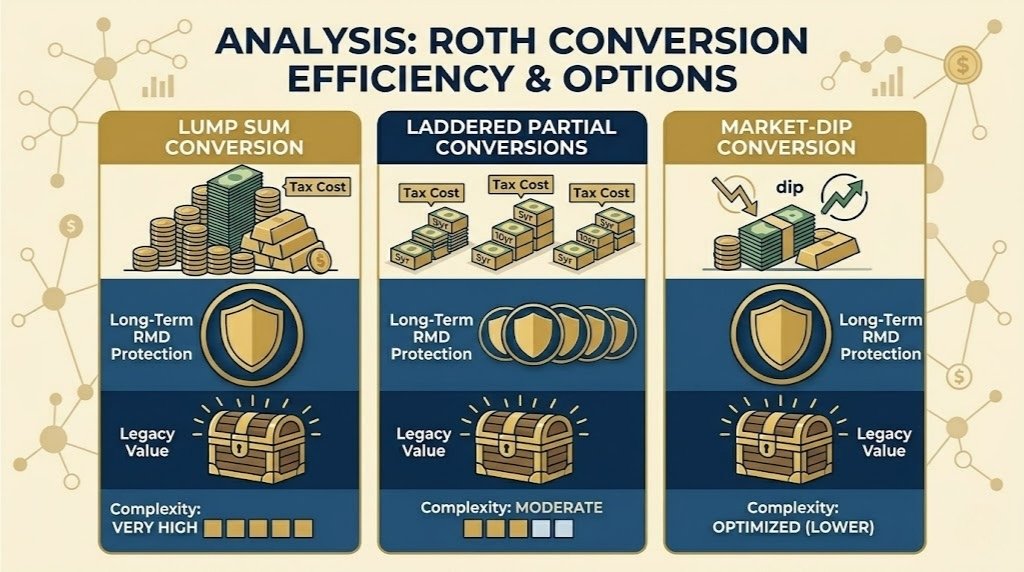

Strategic Analysis Of Roth Conversion Efficiency

To help you decide which approach fits your retirement timeline, we have provided a comparison of the most common methods for executing these tax-sensitive moves.

The following table compares the immediate tax impact versus the long-term benefit of various conversion styles.

Our Top 3 Picks And Why?

While every retiree’s situation is unique, these three strategies consistently provide the best results for those looking to stabilise their financial future through Roth Conversion Strategies.

-

Tax Bracket Arbitrage: It is the most logical way to take advantage of the current tax code before potential future rate hikes.

-

Laddered Partial Conversions: This method offers the perfect balance between tax efficiency and annual cash flow management.

-

Estate Planning Conversions: If your goal is to help your children or grandchildren, there is no better gift than a tax-free growing asset.

Preparation Checklist

Before you move assets into a Roth environment, ensure you have addressed these critical administrative steps to avoid common IRS pitfalls.

● Review Your Income: Calculate your expected Adjusted Gross Income (AGI) to see which tax bracket you are filling.

● Identify Tax Funds: Confirm you have cash in a non-retirement account to pay the resulting tax bill.

● Consult the IRMAA Chart: Check the Medicare premium thresholds to ensure you aren’t accidentally triggering a surcharge.

● Check the Calendar: Ensure the conversion is completed by 31 December to count for the current tax year.

● Notify Your Custodian: Confirm whether your brokerage requires a specific form for a partial versus a full conversion.

Defining Your Legacy Through Tax Efficiency

Executing a successful Roth conversion is not merely a one-time transaction; it is a declaration of independence from future tax uncertainty. By taking the time to understand how these strategies function, you are positioning yourself to enjoy your retirement years with the peace of mind that comes from knowing your income is protected. Whether you are focused on lowering your own RMDs or providing a tax-free windfall for your heirs, the moves you make today will define the strength of your financial foundation for decades to come.