As a healthcare professional in Australia, your dedication to improving the well-being of others is unparalleled. However, while you excel in caring for others, your financial well-being deserves equal attention.

Managing irregular incomes, high expenses, and complex tax obligations can be daunting, especially within the demanding healthcare sector. This is where tax-saving strategies for healthcare professionals in Australia become essential.

In this guide, we’ll explore 12 actionable tax-saving strategies tailored for healthcare professionals in Australia. From maximizing deductions to leveraging tax offsets, these tips will help you reduce your taxable income and achieve financial security.

Why Tax Planning Matters for Healthcare Professionals

Understanding your tax obligations and exploring effective tax-saving options is essential. Tax-saving strategies for healthcare professionals in Australia ensure compliance, unlock savings through deductions and offsets, and contribute to long-term financial growth.

Benefits of Strategic Tax Planning

- Compliance: Stay within Australian Tax Office (ATO) guidelines to avoid penalties.

- Savings: Leverage deductions and offsets to reduce taxable income.

- Financial Growth: Free up resources for investments, retirement planning, and long-term wealth building.

12 Tax-Saving Strategies for Healthcare Professionals in Australia

Here are 12 tax-saving strategies specifically tailored for healthcare professionals in Australia. Whether you’re a doctor, nurse, therapist, or allied health worker, these tips will help you optimize your finances and keep more of your hard-earned money

1. Maximize Work-Related Deductions

Work-related expenses can significantly reduce your taxable income.

Common deductions for healthcare professionals include:

- Uniforms: Costs for purchasing and laundering mandatory uniforms, including scrubs and safety shoes.

- Professional Development: Expenses for attending seminars, workshops, and training directly related to your role.

- Work-Related Travel: Travel between multiple work locations, including mileage for personal vehicles used for work purposes.

| Expense Type | Example | Documentation |

| Uniforms | Scrubs, safety shoes | Receipts, invoices |

| Professional Development | Conference registration fees | Receipts, program details |

| Work-Related Travel | Mileage, public transport tickets | Travel logs, receipts |

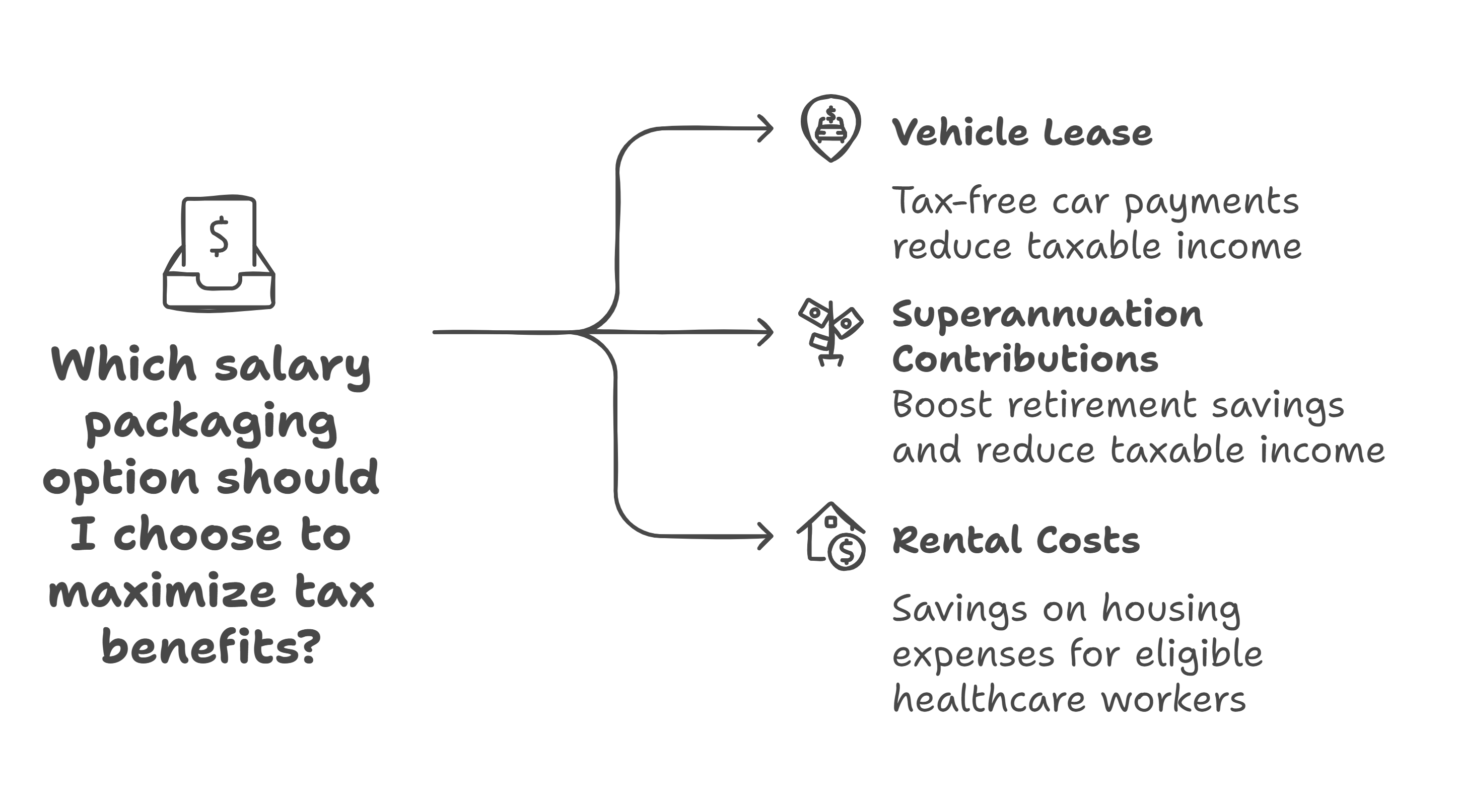

2. Salary Packaging

Salary packaging allows you to pay for certain expenses before tax, effectively reducing your taxable income. Popular options include:

- Vehicles: Lease payments for cars.

- Superannuation Contributions: Boost your retirement savings while saving on taxes.

- Rental Costs: Available to healthcare workers in specific sectors, such as public hospitals.

| Packaged Item | Benefit |

| Vehicle Lease | Tax-free car payments |

| Super Contributions | Reduced taxable income |

| Rental Costs | Savings on housing expenses |

Pro Tip: Check with your employer to see what salary packaging options are available to you.

3. Leverage Superannuation Contributions

Contributing to your superannuation fund is one of the most effective ways to save on taxes. Strategies include:

- Concessional Contributions: Up to $27,500 annually, taxed at 15% instead of your marginal rate.

- Non-Concessional Contributions: Tax-free contributions up to $110,000 annually. These can also be used strategically for wealth building.

- Catch-Up Contributions: If you haven’t maximized your concessional contributions in previous years, you may be able to carry forward unused amounts.

4. Claiming Home Office Expenses

With the rise of remote work, healthcare professionals can claim deductions for home office expenses. Eligible items include:

- Internet and phone bills.

- Depreciation on office equipment, such as computers and printers.

- Electricity and heating costs for your dedicated workspace.

| Expense | Eligibility |

| Internet and Phone | Work-related usage |

| Office Equipment | Depreciation over time |

| Electricity and Heating | Based on hours worked from home |

Pro Tip: Use the ATO’s fixed-rate method to simplify home office deductions if you don’t want to calculate actual expenses.

5. Invest in Continuing Education

Ongoing education is vital in healthcare. The ATO allows deductions for expenses directly related to your current role, such as:

- Tuition fees for professional courses.

- Costs for certifications and seminars.

- Learning materials like textbooks and subscriptions to industry journals.

Note: The education must be directly related to your current employment to qualify for a deduction.

6. Utilize Tax Offsets

Tax offsets directly reduce the amount of tax payable. Key offsets for healthcare professionals include:

- Low and Middle-Income Tax Offset (LMITO): Provides up to $1,500 in savings.

- Private Health Insurance Rebate: A rebate on premiums for eligible policies, encouraging private health coverage.

- Spouse Contributions: Tax offsets for contributing to your partner’s superannuation, especially if they have a lower income.

7. Income Splitting

If you have a partner in a lower tax bracket, consider income splitting to reduce your overall tax liability. This strategy works well for:

- Distributing investment income, such as dividends.

- Allocating business profits in private practice.

| Income Type | Split With |

| Investment Dividends | Lower-income spouse |

| Business Profits | Spouse working part-time |

8. Establish a Trust or Company Structure

For healthcare professionals in private practice, setting up a trust or company can help minimize taxes. Benefits include:

- Income Distribution: Allocate income to beneficiaries in lower tax brackets.

- Asset Protection: Safeguard personal assets from business liabilities.

- Flexibility: Adapt income structures to changing tax laws and financial circumstances.

Pro Tip: Consult with a tax professional to ensure compliance when setting up these structures.

9. Take Advantage of Asset Depreciation

Depreciation allows you to claim deductions for the wear and tear of assets used for work, such as:

- Medical equipment.

- Office furniture.

- Vehicles used for work purposes.

| Asset | Depreciation Type |

| Medical Equipment | Straight-line or diminishing |

| Office Furniture | Annual deduction |

| Vehicles | Based on work-related usage |

10. Invest in Tax-Effective Investments

Tax-effective investments can help you grow wealth while reducing your tax liabilities. Options include:

- Real Estate: Claim deductions for mortgage interest, property maintenance, and depreciation.

- Managed Funds: Access to investments with franking credits.

- Australian Shares: Benefit from dividend imputation, reducing the tax on your investment income.

11. Claim Travel Expenses

Healthcare professionals often travel for conferences, training, or between work locations. Eligible expenses include:

- Flights and accommodation.

- Meals and incidentals during work-related travel.

- Vehicle expenses for work-related trips.

Tip: Keep a detailed travel log to support your claims.

12. Work with a Tax Professional

A tax professional can provide personalized advice, ensuring you maximize deductions and stay compliant. Look for professionals experienced in healthcare taxation to navigate complex situations.

| Benefit of a Tax Professional | Impact |

| Maximize Deductions | Reduce taxable income |

| Ensure Compliance | Avoid penalties |

| Personalized Strategies | Tailored to individual needs |

Common Tax Mistakes to Avoid

- Overclaiming Deductions: Ensure all claims are directly related to earning income.

- Poor Record-Keeping: Maintain detailed records of all expenses and receipts.

- Missing Deadlines: Be aware of ATO filing and payment deadlines to avoid fines.

Tools and Resources for Tax Management

| Resource | Purpose |

| ATO Website | Guides on deductions and offsets |

| Professional Tax Software | Streamlines tax filing and record-keeping |

| Industry Associations | Tax-related advice tailored for healthcare |

Pro Tip: Subscribe to updates from the ATO for the latest changes in tax laws and offsets.

Takeaways

Financial success doesn’t have to be out of reach for healthcare professionals, even in the face of complex tax obligations. By adopting tax-saving strategies for healthcare professionals in Australia, you can create a solid foundation for long-term financial stability and growth.

These strategies allow you to maximize deductions, leverage tax offsets, and make informed investment decisions, all while staying compliant with the Australian Tax Office’s regulations.

Take the first step today by implementing the tips in this guide. With a strategic approach to your taxes, you can focus on what you do best—caring for others—while ensuring that your financial well-being is just as secure as the lives you help improve every day.